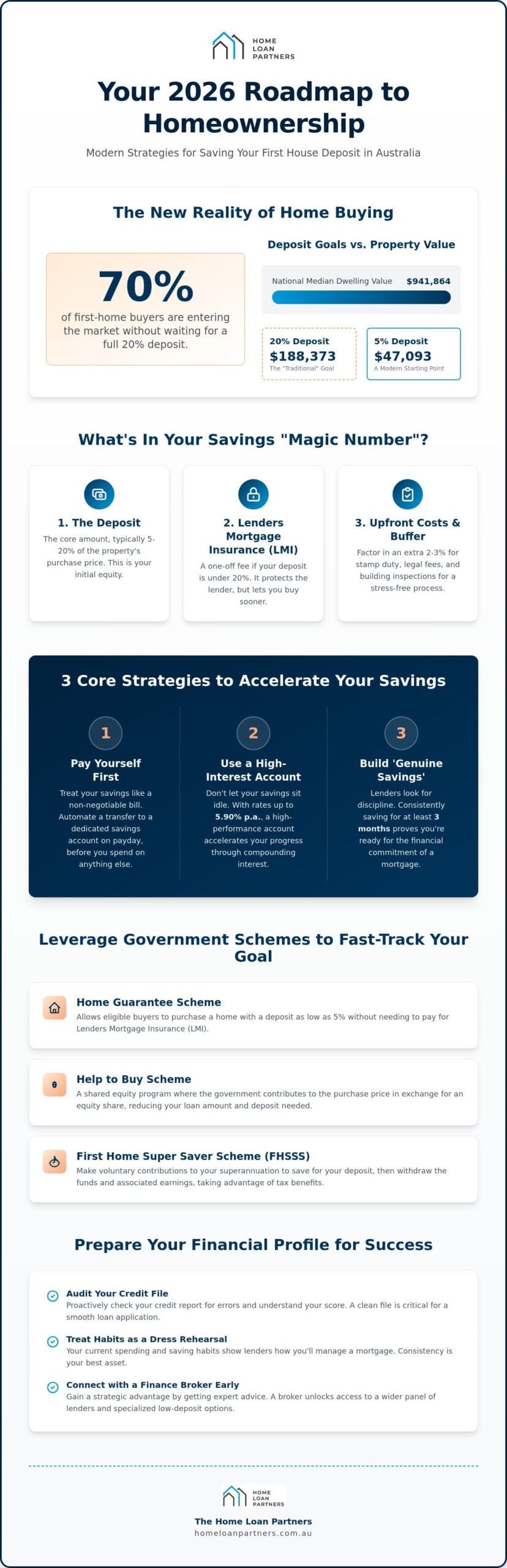

Did you know that 70% of first-home buyers last year decided to stop waiting for a full 20% deposit before entering the market? In an environment where the national median dwelling value has reached $941,864, the old rules of thumb often feel outdated. You’ve likely felt the frustration of watching property prices climb while your savings account struggles to keep pace with the rising cost of living. It’s completely understandable to feel overwhelmed by the complexity of the current market, but finding the right saving for a house deposit strategies is about working smarter with the tools available to you right now.

We’re here to help you cut through the noise and build a clear, actionable path toward your homeownership goals. This guide provides a comprehensive roadmap for 2026, showing you how to master modern financial tactics that reduce stress and accelerate your progress. We’ll explore the latest government shortcuts, including the updated Home Guarantee Scheme and the Help to Buy shared equity program, while explaining how to leverage high-interest savings and the First Home Super Saver Scheme. By the end of this article, you’ll have the confidence and the specific knowledge needed to start your buying journey with a steady hand.

Key Takeaways

- Understand why a 20% deposit isn’t always necessary in 2026 and how to automate your progress with the ‘pay yourself first’ model.

- Master modern saving for a house deposit strategies by leveraging tax-effective tools like the First Home Super Saver Scheme and current government guarantees.

- Discover how your current habits act as a dress rehearsal for a mortgage and learn to audit your credit file effectively before you apply.

- Learn the strategic benefits of connecting with a finance broker early to access a broad panel of lenders and specialized low-deposit options.

Defining Your 2026 House Deposit Goal

A house deposit is the first significant step toward achieving the Great Australian Dream of property ownership. It serves as your initial equity in the home, acting as a security for the lender and demonstrating your ability to manage long-term financial commitments. While traditional advice often suggests you need a 20% down payment, the 2026 market requires more flexible saving for a house deposit strategies. With the national median dwelling value sitting at $941,864 as of May 2026, waiting to save nearly $190,000 can feel like a moving target that’s always just out of reach.

The size of your deposit directly influences your Lenders Mortgage Insurance (LMI) costs. LMI is a one-off premium that protects the lender, not you, if you default on your loan. If you provide less than a 20% deposit, you’ll likely need to pay this fee, though it’s often capitalized into the total loan amount. Understanding this trade-off is vital; sometimes paying LMI is a strategic choice that allows you to enter the market sooner before prices rise even further in high-growth cities like Perth or Brisbane.

The Reality of LVR (Loan-to-Value Ratio)

LVR is the relationship between your loan amount and the property’s value. It’s a key metric lenders use to assess risk and determine your interest rate. A lower LVR typically unlocks more competitive rates and smoother approval processes. While a 20% deposit (80% LVR) is the standard for avoiding LMI, many modern buyers successfully secure loans with a 5% or 10% deposit. We help many clients prioritize market entry over the perfect 80% LVR to avoid being priced out of rapidly evolving regional markets.

Setting a Realistic Timeline

Success starts with knowing your “magic number.” You can use a home loan calculator to work backward from the median price in your target suburb. For example, if you’re eyeing a property in Brisbane where the median price is $1,126,149, a 5% deposit would be roughly $56,307. Developing effective saving for a house deposit strategies involves factoring in more than just the bare minimum. You’ll need a “buffer” for upfront costs like stamp duty, legal fees, and building inspections. In 2026, these costs can add significant weight to your total requirement, so building a 2-3% safety margin into your timeline ensures a much smoother transition into your new home.

Core Saving Strategies for the Modern Australian Market

Building a deposit in 2026 requires more than just a piggy bank; it demands a proactive approach to cash flow management. The ‘Pay Yourself First’ model is one of the most effective saving for a house deposit strategies because it removes the temptation to spend. By treating your savings like a non-negotiable bill that leaves your account on payday, you ensure your property future grows before you pay for lifestyle expenses. This shift in mindset transforms saving from a chore into a primary financial commitment.

Your choice of bank matters significantly in the current environment. As of July 2026, the highest introductory savings rates have reached 5.90% p.a., while the best ongoing bonus rates sit around 5.75% p.a. If your money is sitting in a standard transaction account earning negligible interest, you’re losing ground to inflation and rising property values. Moving your funds to a high-performance account can shave months off your timeline through the power of compounding interest. While reducing discretionary leakages is important, you don’t need to sacrifice every luxury; it’s about identifying the small, recurring costs that don’t actually add value to your life.

The Power of Automation and Bucketing

Separating your money into specific “buckets” creates psychological barriers against overspending. We recommend setting up dedicated accounts for fixed bills, daily lifestyle, and your house deposit. While micro-investing apps are popular, be cautious. Frequent small transfers to volatile assets can sometimes complicate a lender’s view of your spending patterns. A locked savings account with a different institution can act as a circuit breaker for emotional spending, keeping your deposit safe from impulsive decisions.

Demonstrating Genuine Savings

Lenders don’t just look at the total amount; they look at the story behind it. ‘Genuine savings’ usually refers to funds you’ve accumulated through consistent effort over at least three months. While a generous gift from family is helpful, most banks still want to see that you have the discipline to save a portion of the deposit yourself. This 3-month rule acts as a trial run for your future mortgage repayments.

Documenting this journey is vital for a stress-free application. Avoid large, unexplained cash deposits that might raise red flags during the credit assessment. If you’re unsure how your current banking habits might look to a lender, speaking with a specialist can help you refine your strategy before you apply. Consistency proves to a lender that you can handle the responsibility of a home loan, making your eventual approval much more likely.

Leveraging Government Schemes to Accelerate Your Deposit

The property market in 2026 presents unique challenges, but it also offers some of the most robust support systems we’ve seen in decades. While traditional saving for a house deposit strategies focus on personal discipline, the most successful buyers are those who treat government initiatives as a core component of their financial plan. These schemes aren’t just supplementary; they are designed to reduce the total cash you need upfront, potentially shaving years off your waiting time. By understanding how to stack these benefits, you can move from the sidelines into your own home with much more speed and less stress.

One of the biggest hurdles for buyers is the sheer volume of cash required to avoid Lenders Mortgage Insurance. National initiatives now act as a powerful bridge. For instance, the Home Guarantee Scheme allows eligible buyers to purchase with as little as a 5% deposit because the government acts as a guarantor for the remaining 15%. This effectively removes the LMI barrier. As of July 2026, property price caps have been adjusted to reflect current values, with Sydney reaching $1,500,000 and Brisbane at $1,000,000, ensuring these programs remain useful in even the most competitive suburbs.

Mastering the First Home Super Saver Scheme

The First Home Super Saver (FHSS) Scheme is a tax-effective powerhouse that many buyers overlook. By making voluntary contributions to your superannuation, you’re essentially saving for your home using pre-tax dollars. These contributions are typically taxed at only 15%, which is significantly lower than most marginal income tax rates. This means more of your hard-earned money stays in your pocket and goes toward your property goal. Eligible individuals can contribute up to $15,000 per financial year, with a total lifetime cap of $50,000 allowed for withdrawal through the First Home Super Saver Scheme. When you’re ready to buy, you can withdraw these contributions plus ‘deemed earnings’, giving your deposit a significant boost compared to a standard savings account.

Low Deposit Schemes: Buying with 5%

Entering the market earlier with a smaller deposit can be a strategic move in a rising market. While having less equity means a larger loan, the absence of LMI through government guarantees saves you thousands of dollars in upfront costs. We often see clients combine these national guarantees with state-specific grants for maximum impact. For example, Queensland offers a $30,000 First Home Owner Grant for new homes until June 30, 2026, while the Northern Territory provides a substantial $50,000 grant. These regional “boosts” can be the final piece of the puzzle, providing the confidence you need to start your buying journey with a steady hand.

Optimizing Your Financial Profile for Future Lenders

Lenders view your bank statements as a window into your future. While your saving for a house deposit strategies focus on building the pot, lenders focus on your ability to service the debt. It’s helpful to think of your current saving habits as a dress rehearsal for your mortgage. If you can consistently put away a specific amount each month now, it gives a bank the confidence that you’ll manage a similar mortgage repayment later. This transition from saver to homeowner is smoother when your financial behavior tells a story of discipline and reliability.

A 6-month pre-purchase audit of your credit file is a vital step in your roadmap. You should check for any forgotten defaults or simple administrative errors that could derail an application. Similarly, you need to manage your “liability traps” like credit card limits and Buy Now, Pay Later (BNPL) accounts. Even if your balance is zero, a lender often assesses a $10,000 credit card limit as if it were fully drawn. This significantly impacts your debt-to-income ratio and can reduce your borrowing power by tens of thousands of dollars.

The Impact of Living Expenses

In 2026, lenders use sophisticated digital tools to categorize every transaction on your bank statements. They compare your actual spending against the Household Expenditure Measure (HEM), which is a benchmark for what a typical household spends. If your 90-day history shows excessive discretionary spending or multiple unused subscriptions, it may lower your assessed borrowing capacity. Tidying up your accounts 90 days before you apply is a proactive way to present your best financial self. We often guide clients through this process to ensure their statements reflect a stable, low-risk lifestyle.

Debt Management as a Saving Strategy

Sometimes, the most effective way to “save” is actually to pay down existing debt. Reducing a $5,000 credit card limit often boosts your borrowing power more than adding that same $5,000 to your savings account. This is because lenders calculate your capacity based on your total available credit and monthly obligations. Consolidating high-interest personal loans into a single, manageable payment can also free up the monthly cash flow lenders want to see. For a broader view of the entire process, you can explore our guide on how do i buy a house in australia.

If you’re ready to see how your current financial profile stacks up against lender requirements, connect with our team for a personal assessment to help you prepare for a successful application.

The Strategic Advantage of a Finance Broker

Many aspiring buyers treat saving as a solo marathon, only seeking professional help once they’ve reached their goal. However, involving a professional early in the process is one of the most effective saving for a house deposit strategies you can employ. A broker acts as a strategic collaborator, helping you reverse-engineer your target based on real-time lender policies rather than generic online estimates. By understanding your borrowing power today, we can help you set a precise savings goal that accounts for the nuances of the 2026 market. This collaborative approach ensures you aren’t aiming for an arbitrary number but a figure that actually unlocks the door to your target property.

With access to a panel of 36+ lenders, we can identify “low deposit” specialists who are comfortable with 5% or 10% deposits. Every bank has a different appetite for risk, and their rules around genuine savings or income types vary significantly. We take the heavy lifting off your shoulders by matching your unique financial profile with the right institution. This ensures your loan structure isn’t just a transaction but a tailored plan that aligns with your long-term wealth goals and future security. Transitioning from a saver to a homeowner is a significant life milestone, and having a steady hand to guide you through the final hurdles makes the process feel much more manageable.

Reverse-Engineering Your Purchase

A broker calculates your exact target by looking at current lender servicing calculators and policy shifts. We identify which lenders are most favorable to your specific income type, whether you’re a PAYG employee, a freelancer, or a small business owner. This level of precision prevents you from over-saving for a goal you’ve already met or under-saving for a property that requires a specific LVR. Establishing a professional finance broker relationship early provides the peace of mind that your efforts are moving you in the right direction. It allows us to monitor market changes and adjust your saving for a house deposit strategies as property values or interest rates fluctuate.

Navigating the Final Stretch

As you approach your goal, we help you prepare for pre-approval while your final savings land in your account. This proactive approach means you’re ready to act the moment you find the right property, giving you a competitive edge in fast-moving markets. We manage the complex paperwork and communication with lenders, allowing you to focus on the excitement of your new home. Our role is to be your steady hand, navigating you through various options with patience and precision. Start your journey with a personalized strategy session from The Home Loan Partners to turn your savings plan into a successful property purchase.

Take the Next Step Toward Your 2026 Property Goals

Your journey to homeownership doesn’t have to be a solo climb. By focusing on modern saving for a house deposit strategies, you’ve already shifted your mindset from hope to action. You now understand that a deposit is more than just a number; it’s a reflection of your financial health and a strategic entry point into the Australian market. Whether you’re leveraging tax-effective schemes or “tidying up” your accounts to satisfy 2026 lender requirements, every step you take brings that front door key closer to your hand.

We’re here to help you navigate the complexities of personalised loan structuring and provide expert guidance for first-home buyers. With access to a panel of 36+ Australian lenders, we specialize in finding the right fit for your unique situation. Book a free strategy session with The Home Loan Partners to plan your deposit journey today. Our team is ready to act as your steady guide, ensuring your transition from saver to homeowner is as smooth and stress-free as possible. You’ve got the roadmap; now let’s start the engine together.

Frequently Asked Questions

How much deposit do I really need to buy a house in Australia in 2026?

You typically need between 5% and 20% of the property value plus enough to cover upfront costs like stamp duty. While 20% is the traditional benchmark to avoid insurance, many 2026 buyers use government guarantees to enter the market with just 5%. For a median-priced home of $941,864, a 5% deposit is approximately $47,093. You should also budget an extra 2% to 5% for legal fees and state-based taxes.

Is it better to save a 20% deposit or pay Lenders Mortgage Insurance (LMI)?

The right choice depends on your local market’s growth and your personal timeline. Saving 20% avoids LMI costs, but if property prices in cities like Perth or Brisbane rise faster than you can save, you might lose more in potential equity than you save on insurance. Paying LMI is often a strategic move to secure a home sooner. It allows you to stop paying rent and start building your own wealth earlier.

Can I use a gift from my parents as a house deposit?

Yes, you can use a gifted deposit, but lenders usually require proof of genuine savings as well. This typically means having at least 5% of the property value saved in your own account for at least three months. You’ll also need a signed “gift letter” from your parents. This document confirms the funds are a non-repayable gift rather than an undisclosed loan that would impact your borrowing power.

What is the First Home Super Saver Scheme and how does it help?

The First Home Super Saver (FHSS) Scheme is one of the most effective saving for a house deposit strategies because it uses pre-tax dollars. By making voluntary contributions to your super, you pay only 15% tax on that income instead of your usual marginal rate. You can contribute up to $15,000 per year, with a total lifetime limit of $50,000. When you’re ready to buy, you withdraw these savings plus deemed earnings.

How long does it take to save for a house deposit on an average salary?

Saving a full 20% deposit for a median-priced home can take over a decade on an average salary, but low-deposit schemes shorten this significantly. If you target a 5% deposit through the Home Guarantee Scheme, your timeline could drop to 2-4 years. Your speed depends on your ability to automate savings and reduce discretionary spending. We help clients map out these specific timelines based on their unique income and target suburbs.

Do lenders look at my rent history as proof of savings?

Some lenders accept a strong rental history as a substitute for a portion of the genuine savings requirement. If you’ve paid rent on time for 12 consecutive months, it proves you have the discipline to manage a mortgage. However, you still need the actual cash for the deposit and settlement costs. Using rent as evidence works best when combined with other consistent saving for a house deposit strategies to strengthen your application.

Can I buy a house with a 5% deposit without a guarantor?

Yes, you can buy with a 5% deposit without a family guarantor by using the federal Home Guarantee Scheme. The government acts as a guarantor for the remaining 15%, which allows you to bypass Lenders Mortgage Insurance entirely. As of 2026, the government has removed limits on the number of places available in this scheme. You simply need to meet the income eligibility and property price caps for your specific region.

How does my credit score affect my ability to get a home loan?

Your credit score is a primary indicator of your reliability as a borrower and impacts both approval and interest rates. A higher score gives lenders the confidence to offer you more competitive products and higher borrowing limits. If your score is low due to past defaults or too many credit inquiries, it may limit your options. We recommend a credit audit six months before you apply to ensure your profile is in top shape.