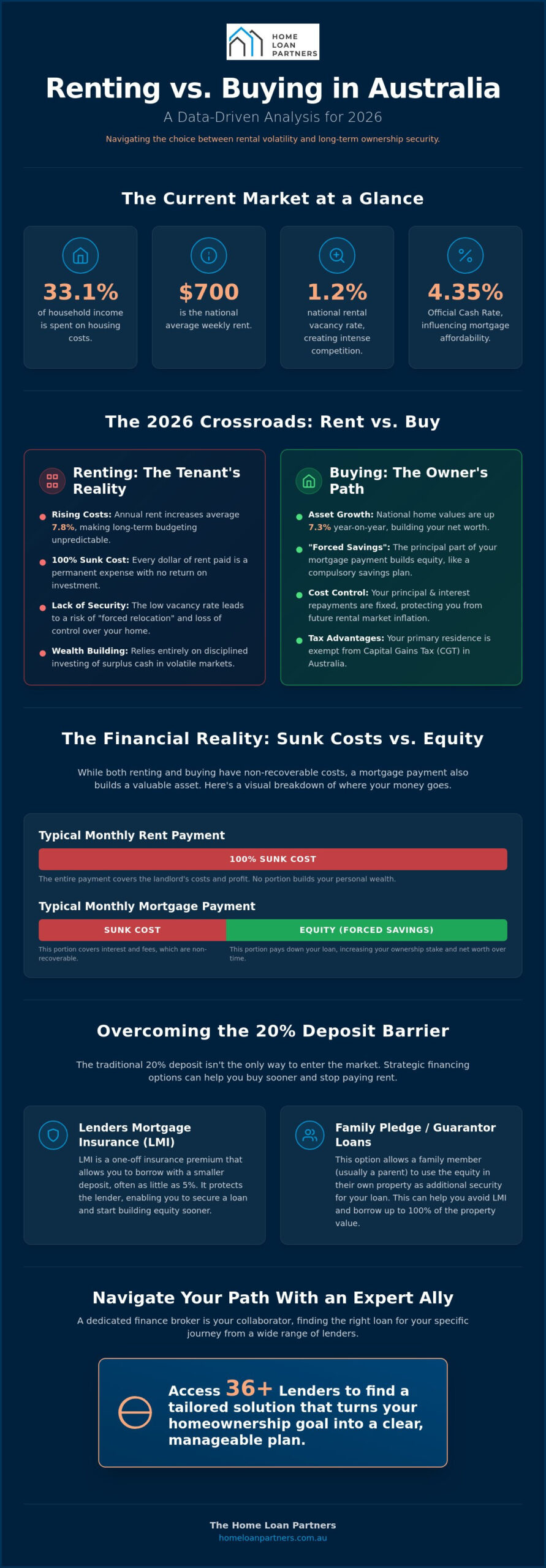

Did you know that Australian households are now spending a record 33.1% of their income just to keep a roof over their heads? With national average rents hitting $700 per week and vacancy rates at a razor-thin 1.2%, the pressure on your savings has never felt more intense. It’s completely natural to feel stuck between skyrocketing rental costs and the fear of buying at the peak of the market, especially with the official cash rate at 4.35%. This renting vs buying australia 2026 analysis cuts through the noise to provide the data-driven truth you need to decide your next move with total confidence.

We understand that saving a 20% deposit feels like a distant dream while living costs remain high. You’re likely looking for a way to stop the cycle of rent hikes without overextending yourself. We’ll show you exactly how the financial numbers stack up over the long term, comparing wealth creation through property against alternative investment paths. You’ll also discover practical strategies for entering the market with a smaller deposit, helping you turn a stressful financial crossroad into a clear, manageable plan for your future security.

Key Takeaways

- Understand the current rental crisis and whether the “Ownership Premium” of a mortgage offers better long-term security than volatile rent hikes.

- Discover how to distinguish between rental sunk costs and mortgage interest to build a “forced savings” equity pool for your future.

- Access a detailed renting vs buying australia 2026 analysis to evaluate if rent-vesting or direct ownership best aligns with your lifestyle and wealth goals.

- Learn how to bypass the traditional 20% deposit barrier using strategic financing options like Lenders Mortgage Insurance (LMI) or family-pledge guarantor loans.

- See how a dedicated finance broker acts as your expert collaborator, navigating 36+ lenders to find the right path for your specific financial journey.

The 2026 Property Landscape: Australia’s Rental Reality vs. Ownership

Deciding whether to sign another lease or commit to a mortgage has never felt more significant. In this renting vs buying australia 2026 analysis, we see a market that rewards those who prioritize long term stability over short term market timing. Many Australians currently face an “Ownership Premium” where monthly mortgage repayments exceed their current rent. However, this extra cost buys protection against a rental market that shows no signs of cooling. It is a trade off between the flexibility of today and the security of tomorrow.

The State of Australian Renting in 2026

Tenants are navigating a historically difficult environment. With the national vacancy rate sitting at a mere 1.2% as of May 2026, the power dynamic has shifted entirely toward landlords. Average weekly rents have climbed to $700.04, reflecting a 7.8% annual increase. This isn’t just about higher costs; it’s about the loss of control. Many families now experience “forced relocation” because they simply can’t keep up with the 33.1% of household income now required to cover rent. This volatility makes long term budgeting nearly impossible for those without a fixed housing cost.

Property Market Resilience: Why Prices Haven’t “Crashed”

It’s common to hear talk of a “market crash” just around the corner. The data tells a different story. While major cities like Sydney and Melbourne saw monthly dips in June 2026, national home values remain 7.3% higher than a year ago. This resilience comes down to basic math. Migration remains steady and new construction starts haven’t kept pace with our growing population. For a broader Australian property market overview, it’s clear that demand continues to outstrip supply, keeping entry costs high despite interest rate fluctuations.

Buying in 2026 is less about catching the “bottom” of the market and more about hedging against future inflation. When you own your home, you’re essentially capping your future housing costs. While a renter’s expenses rise with the tide of inflation every year, a homeowner’s principal debt remains static. Over a decade, that initial “Ownership Premium” often transforms into a massive financial advantage. We’re here to help you determine if now is the right time to stop chasing the market and start building your own security through a steady, guided process.

The Financial Deep-Dive: Sunk Costs, Equity, and the Wealth Gap

When you look beneath the surface of the “rent is dead money” argument, the financial reality is more nuanced. Both paths involve sunk costs that never return to your pocket. For tenants, the entire rent check is a sunk cost. For homeowners, sunk costs include mortgage interest, council rates, and ongoing maintenance. However, a renting vs buying australia 2026 analysis reveals a critical distinction: the principal component of a mortgage payment. This acts as a “forced savings” mechanism, building a net worth piggy bank that grows with every repayment you make.

The wealth gap between these two paths is often widened by the tax treatment of the family home. In Australia, your principal place of residence is exempt from Capital Gains Tax (CGT). This means every dollar of price growth stays with you. Researchers from the Economic Society of Australia have provided an in-depth financial analysis of renting vs. buying that underscores how these tax advantages, combined with long term capital growth, typically outweigh the benefits of renting and investing elsewhere over a ten year horizon.

Calculating the 10-Year Wealth Difference

Imagine a scenario where you rent for $3,000 per month versus paying a $4,500 mortgage. While the mortgage requires an extra $1,500 monthly, the homeowner is capturing the 7.3% annual growth seen in national property values through 2026. Over a decade, that equity upside doesn’t just build wealth; it provides a powerful “equity bridge” that allows you to borrow for future goals or upgrade your home as your family grows. Renters, conversely, must rely entirely on their ability to consistently invest their surplus cash in volatile markets.

The “Cost of Waiting” Analysis

Many Australians hesitate, hoping for a market dip to save a larger deposit. However, property price growth often outpaces the rate at which most people can save. If a $700,000 home increases by 5% in a single year, the price jumps by $35,000. It’s incredibly difficult to save an additional $35,000 in twelve months while also paying record-high rents. Watching the market move further out of reach can be exhausting, which is why exploring First Home Buyer Loans with a smaller deposit often makes more financial sense than waiting for a “perfect” entry point that may never arrive.

Rent-Vesting vs. Direct Ownership: Which 2026 Strategy Fits You?

Choosing your path in the current market isn’t always a binary choice between being a tenant or an owner-occupier. A modern renting vs buying australia 2026 analysis must account for rent-vesting, a strategy that has gained significant traction as property prices in premium suburbs remain high. This approach allows you to rent a home in the location you love while owning an investment property in a more affordable, high-growth area. It’s a way to enter the market without sacrificing your lifestyle or your proximity to work and community.

This investment strategy often requires a high level of financial oversight to ensure tax efficiency and asset growth. Many successful rent-vesters rely on firms like KHT Accounting & Wealth to help them manage their portfolios and align their investment choices with their overall wealth-building goals.

Deciding which strategy suits your goals involves modeling your specific numbers. We recommend using a home loan calculator to see how different mortgage sizes and interest rates impact your monthly cash flow. Whether you’re comparing a “rent and invest in shares” model against a “buy and hold property” strategy, seeing the figures clearly helps remove the emotional weight of the decision. Our role is to act as your expert collaborator, helping you interpret these results within the context of your long term financial journey.

The Rent-Vester Advantage in 2026

Rent-vesting offers unique financial leverage that direct ownership doesn’t provide. Because the property you own is an investment, you can often access tax benefits like negative gearing and depreciation. These can help offset the costs of holding the asset. In 2026, this strategy is particularly effective for those who want to build a property portfolio while living in suburbs where a $2 million plus mortgage would be restrictive. By partnering with a dedicated agency like Elite Agents & Partners for property management, you’re essentially letting a tenant help pay off your asset while you maintain the flexibility to move as your life changes.

Direct Ownership: The Traditional Path to Security

Overcoming the 2026 Deposit Gap: Strategic Financing Options

Saving a full 20% deposit while paying $700 in weekly rent can feel like an impossible climb. However, our renting vs buying australia 2026 analysis shows that waiting to reach that 20% milestone often costs more in missed capital growth than the cost of Lenders Mortgage Insurance (LMI). By leveraging LMI, you can often enter the market with as little as a 5% deposit. Alternatively, many clients use a “Family Pledge” or Guarantor Loan. This allows a family member to use their own home equity to secure your deposit, helping you bypass the cash hurdle entirely and start your ownership journey sooner.

For those already in the market looking to upgrade, bridging finance provides a vital safety net. It allows you to secure your next home before selling your current one, ensuring you don’t miss out on the right property in a fast moving market. We also see more Australians exploring SMSF Loans to use their superannuation balance for investment property purchases, providing a different path to long term wealth outside of traditional home ownership.

Government Grants and Incentives in 2026

The 2026 landscape includes several federal and state level supports designed to bridge the affordability gap. The First Home Guarantee scheme continues to help eligible buyers purchase with a small deposit without paying LMI. Stamp duty concessions also play a major role in lowering upfront costs. For instance, in New South Wales, exemptions apply for first home buyers on homes up to $800,000, while Victoria offers similar relief up to $600,000. If you’re feeling overwhelmed by the paperwork, our buying a house in Australia guide breaks the entire process into manageable steps.

Innovative Loan Structures

Choosing the right loan structure is just as important as the interest rate itself. Offset accounts and redraw facilities allow you to keep your cash liquid while effectively reducing the interest you pay. For those looking to build, construction loans offer a way to manage progress payments and potentially save on stamp duty by only paying for the land value initially. A dedicated broker finds tailored structures across 36 plus lenders to ensure your loan matches your lifestyle and long term aspirations. If you’re ready to see what’s possible for your situation, you can explore our First Home Buyer Loans today.

Navigating Your Path: Why a Finance Broker is Your Best 2026 Ally

Deciding between staying in the rental market or committing to a home loan is a choice that carries significant emotional and financial weight. While this renting vs buying australia 2026 analysis provides the data you need, a finance broker provides the steady hand to guide you through the execution. The traditional “Bank vs. Broker” debate is easily settled when you consider the power of choice. A single bank can only offer you their own specific products. A broker gives you access to more than 36 lenders, significantly increasing your odds of finding a competitive rate and a loan structure that aligns with your future.

Our team acts as your expert collaborator, translating complex industry jargon into practical language that actually makes sense for your life. We don’t just process paperwork. We manage the heavy lifting so you can focus on finding the right property. This partnership doesn’t end when you get your keys, either. We provide ongoing support throughout the duration of your loan, ensuring your finance remains optimized as the market shifts. This long term commitment helps alleviate the stress of the process, turning a complex financial hurdle into a clear, predictable path forward.

Personalised Financial Guidance

Many Australians are surprised to find that their actual borrowing power is often higher than what a bank’s basic online calculator suggests. Those apps use generic algorithms that don’t account for your specific career trajectory or unique financial strengths. We provide the unbiased advice necessary to navigate a high stakes 2026 market with precision. By looking at your total financial picture, we help you secure a mortgage quote that reflects your real world goals rather than just a computer generated estimate.

Starting Your Journey with The Home Loan Partners

Our approach is fundamentally professional, reassuring, and deeply client centric. We understand that you aren’t just looking for a loan; you’re looking to secure your future and achieve a major life milestone. From your initial aspirations to the day of settlement, we maintain a steady and logical rhythm that fosters security. If you’re ready to move past the uncertainty and see the data driven truth of your own situation, we’re here to help. You can Book a consultation with The Home Loan Partners to begin your stress free journey toward ownership today.

Securing Your Financial Future in the 2026 Market

This renting vs buying australia 2026 analysis underscores that the right choice depends on your specific life goals and financial capacity. Whether you choose the stability of direct ownership or the flexibility of rent-vesting, the key is to move from a state of uncertainty into a position of control. By understanding the “forced savings” of a mortgage and leveraging government incentives, you can stop reacting to rental price hikes and start building tangible wealth. It’s about finding the path that offers you the most security for the long term journey ahead.

You don’t have to navigate these complex decisions alone. Our team acts as your expert collaborator, offering unbiased national advice tailored to your specific journey. As specialists in first home and investment loans, we provide access to over 36 lenders and manage the heavy lifting to find the structure that fits your aspirations. Let us help you navigate the 2026 property market; contact The Home Loan Partners today. We’re here to be your reliable guide, ensuring you reach your milestones with confidence and clarity.

Frequently Asked Questions

Is it better to rent or buy in Australia in 2026?

The decision depends on your personal financial goals and need for long term security. A thorough renting vs buying australia 2026 analysis shows that while renting offers flexibility, the national vacancy rate of 1.2% makes it increasingly difficult to find stable, affordable housing. Buying helps you lock in your housing costs and build a net worth piggy bank through principal repayments, even if the monthly mortgage cost is initially higher than rent.

What is the “cost of waiting” to buy a house?

The cost of waiting is the potential capital growth you miss while property prices continue to rise. Despite monthly fluctuations, national home prices were 7.3% higher in June 2026 than the previous year. If you wait twelve months to save a larger deposit, the property’s price may increase by more than your total savings during that same period, making the entry point even harder to reach.

Can I buy a house in 2026 with only a 5% deposit?

Yes, you can enter the market with a 5% deposit by using Lenders Mortgage Insurance (LMI) or government support like the First Home Guarantee. These options are designed to help you bypass the traditional 20% deposit hurdle. While you’ll have a larger loan balance, entering the market sooner allows you to start building equity while property values are still growing.

Does renting and investing in shares beat property ownership?

Renting and investing in shares can be profitable, but it often lacks the powerful leverage and tax advantages found in a renting vs buying australia 2026 analysis. Your primary residence is generally exempt from capital gains tax, which is a benefit share portfolios don’t share. Additionally, property allows you to build wealth on the full value of the asset rather than just your initial cash investment.

How much extra does it cost to own a home vs. rent (maintenance and rates)?

Homeowners should budget for ongoing costs such as council rates, building insurance, and general maintenance. These expenses vary significantly by location and property type, but they are essential for protecting your investment. While these costs don’t exist for tenants, they’re often offset by the long term stability and equity growth that ownership provides over time.

What happens to my mortgage if interest rates rise further in 2026?

If interest rates rise beyond the current 4.35% cash rate, your monthly variable mortgage repayments will increase. We help you prepare for this by assessing your borrowing capacity with a buffer rate to ensure you can manage potential hikes. You might also consider fixing a portion of your loan to provide more certainty in your monthly household budget.

Is rent-vesting still a viable strategy in 2026?

Rent-vesting remains a highly effective strategy for those who want to live in premium areas but can’t afford to buy there yet. It allows you to rent your preferred lifestyle while owning an investment property in a more affordable growth corridor. This approach balances your current happiness with your long term financial security by getting you onto the property ladder sooner.

How does a mortgage broker help me decide between renting and buying?

We act as your reliable guide, helping you evaluate your borrowing power across 36 plus lenders to see what’s actually possible. Our team translates complex jargon into a clear path forward, comparing the wealth gap between your current rent and potential mortgage repayments. This expert support ensures you feel confident and secure in your choice, no matter which path you decide to take.