What if the lowest interest rate you see on a digital billboard today actually costs you A$42,000 more in hidden structural costs over the next decade? It’s a frustrating reality in 2026, where shifting APRA regulations have made traditional bank loyalty a thing of the past. You likely feel overwhelmed by strict lending criteria and the nagging suspicion that your bank isn’t telling you the whole story. You deserve a clear path to homeownership that prioritizes your long term wealth over a bank’s profit margin.

That’s why choosing the right finance broker is the most critical decision you’ll make in your property journey. We’ll show you how an expert partner navigates this complex environment to secure tailored loan structures that the Big Four simply won’t offer you directly. You’re about to discover how to bypass the stress of the application process, decode the Best Interests Duty, and gain access to a diverse panel of over 35 lenders dedicated to your specific goals.

Key Takeaways

- Learn why direct bank applications are facing higher rejection rates in 2026 and how a finance broker provides a strategic path to approval.

- Understand the vital difference between a standard mortgage broker and a finance broker to ensure you have the right expert for asset, equipment, or business loans.

- Discover how the statutory Best Interests Duty (BID) legally protects you by requiring brokers to prioritize your goals over lender profits.

- Identify the essential credentials and lender panel sizes required to navigate the Australian credit landscape with confidence and clarity.

- Explore how a strategic partnership provides access to over 36 lenders, delivering tailored loan structures that align with your long-term financial security.

What Is a Finance Broker and Why Are They Essential in 2026?

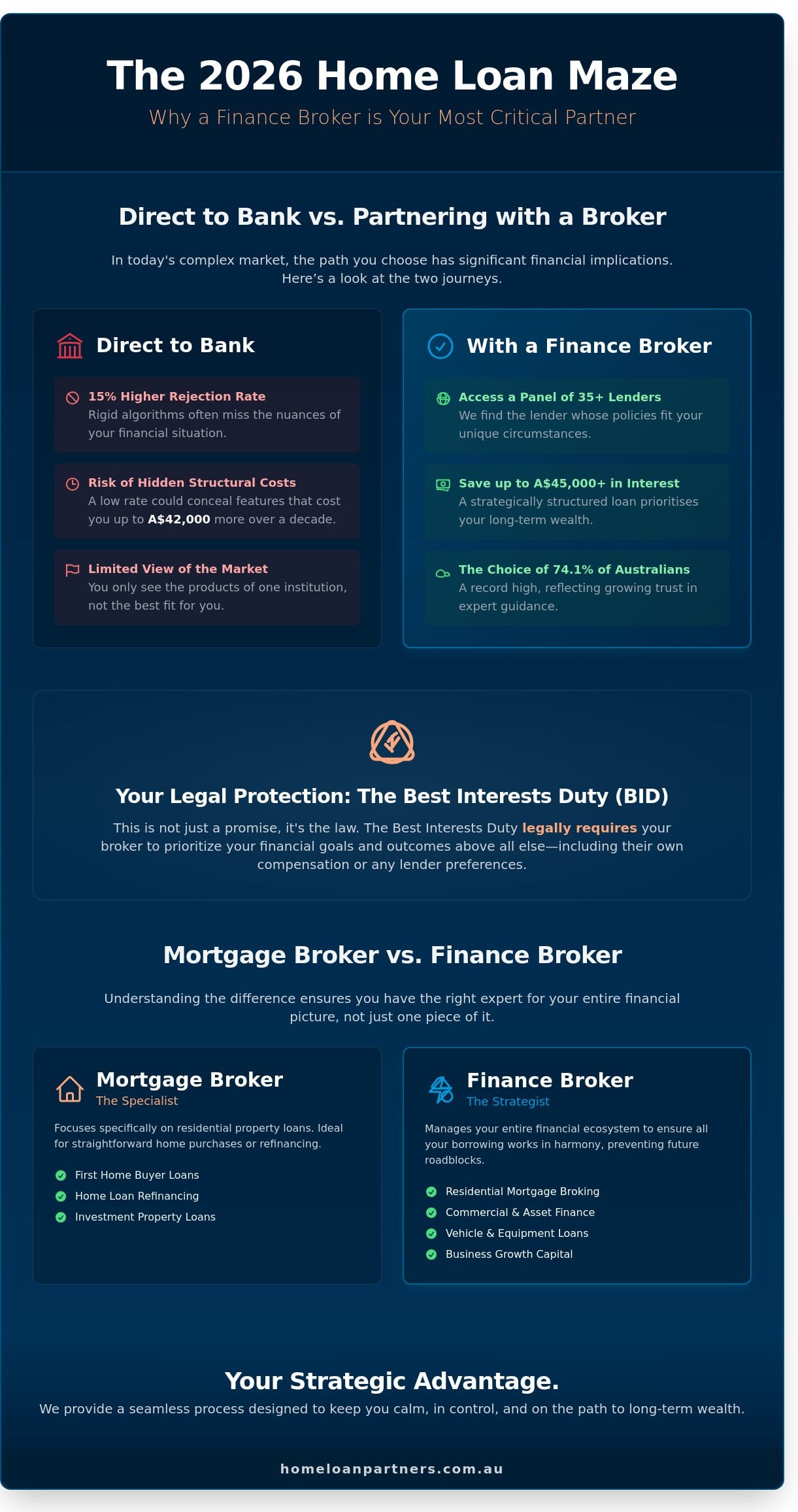

A finance broker acts as your professional intermediary, bridging the gap between you and a diverse panel of Australian lenders. Rather than you walking into a single bank branch, we work on your behalf to identify loan products that align with your specific goals. In the 2026 lending environment, this role has become a necessity. Recent data indicates that direct-to-bank applications now face rejection rates 15% higher than those managed by professionals. This shift occurs because banks have moved toward rigid, algorithmic assessments that often overlook the nuances of a borrower’s life.

We view our role as your trusted guide. The mortgage process is full of dense jargon that can feel overwhelming. We simplify concepts like equity, offset accounts, and Loan-to-Value Ratio (LVR) into plain English. Our focus is on your security and clarity. Statistics from the Mortgage & Finance Association of Australia (MFAA) show that 74.1% of Australians now use a broker to secure their home loans. This record high reflects a growing trust in experts who prioritize the client’s interests over a bank’s quarterly profits.

The Value of Choice: Accessing More Than Just the Big Four

Limiting yourself to one bank means you only see a fraction of the market. A single lender can’t be everything to everyone. Our panel includes dozens of institutions, from major banks to niche lenders that specialize in unique financial profiles. If you’re looking at a Self-Managed Super Fund (SMSF) loan or need bridging finance to secure a new home before selling your current one, a broker is vital. We understand the “hidden” credit policies that vary between lenders. For example, one bank might only recognize 50% of your bonus income, while another accepts 100%. We find the one that says yes.

Saving Time vs. Saving Money: Why You Need Both

DIY loan hunting carries a significant hidden cost. Every time you submit an application that isn’t a perfect fit, you risk a hit to your credit score. We do the heavy lifting by managing the paperwork and negotiating directly with credit managers. It’s about more than just finding the lowest headline rate. A correctly structured loan can save you upwards of A$45,000 in interest over the life of the mortgage. We ensure your loan is a tailored fit for your long-term journey, not just a temporary fix. It’s a seamless process designed to keep you calm and in control.

Mortgage Broker vs. Finance Broker: Understanding the Difference

While people often use these titles interchangeably, the distinction matters for your long-term wealth. A mortgage broker focuses specifically on residential property loans. In contrast, a finance broker manages a broader spectrum of credit products, from car loans to complex commercial facilities. Think of a mortgage broker as a specialist and a finance broker as a lead strategist who understands how every part of your financial health connects.

This holistic approach is essential if you’re a business owner or a self-employed contractor. Banks often view these borrowers through a different lens. Having a partner who understands your entire balance sheet ensures that a business equipment loan you take out today won’t accidentally sabotage your ability to buy a home next year. We look at the big picture so you don’t have to. We act as your advocate, ensuring your personal debt and business liabilities don’t clash.

Residential Mortgage Broking: The Core Service

For most Australians, the journey begins with a home. Whether you’re a first-time buyer or looking to refinance your home loan, we provide the steady hand you need. We help you navigate the 35,000 places available in the 2024-25 First Home Guarantee or calculate the exact stamp duty concessions available in your specific state. Our goal is to tailor a structure that fits your life, whether that’s an offset account for an owner-occupier or an interest-only period for a strategic investor. For buyers in competitive suburban markets, our guide to home loans in North Sydney shows how a tailored approach can cut through the complexity of comparing dozens of lenders at once.

Commercial and Asset Finance: Beyond the Home

A versatile finance broker also secures the tools you need to grow your income. This side of the industry moves faster and requires a different tactical approach than a standard 30-year mortgage. Key areas include:

- Vehicle and Equipment Finance: Utilising the A$20,000 instant asset write-off threshold available for small businesses through June 2025.

- Commercial Property Loans: Securing funding for office spaces, retail shopfronts, or warehouse expansions with specialised lenders.

- Business Growth Capital: Accessing equity in your existing property to fund expansion without disrupting your daily cash flow.

Equipment finance typically involves shorter terms of three to seven years. Because these assets depreciate, the lending criteria and tax implications differ significantly from a home loan. If you’re ready to see how your personal and business goals can work together, reaching out to a trusted partner is the first step toward a seamless financial future. We focus on the numbers so you can focus on your life.

The ‘Best Interests Duty’ (BID): Your Legal Protection Explained

Since January 1, 2021, every mortgage broker in Australia has operated under a strict legal mandate known as the Best Interests Duty (BID). This isn’t just a professional suggestion. It’s a statutory obligation under the National Consumer Credit Protection Act 2009. It requires your finance broker to prioritize your financial interests above their own or those of any lender. While you might assume this applies to everyone in finance, bank employees are generally only required to provide products that are “not unsuitable” for you. This distinction is vital. It means a bank staff member can offer you their own product even if a better deal exists across the street. A broker cannot do that.

BID forces a high level of transparency into the lending process. Your broker must document why a specific loan is the best fit for your unique goals. They have to justify their lender selection based on your needs, such as lower interest rates, better features, or specific borrowing capacities. This legal shield provides immense peace of mind. You can rest easy knowing your partner in this journey is legally bound to act as your advocate, not a salesperson for a single institution.

Broker vs. Bank: A Side-by-Side Comparison

- Product Range: A bank offers 1 internal suite of products. A broker provides access to 30 or more lenders.

- Legal Duty: Brokers must follow the statutory Best Interests Duty. Bank staff are exempt from this specific duty when providing credit assistance.

- Service Style: Brokers act as a long-term partner through the life of your loan. Bank service is often transactional and subject to branch staff turnover.

How Brokers Are Paid: Transparency and Commissions

Transparency is a cornerstone of the BID framework. Your finance broker must disclose exactly what they earn from a transaction in a Credit Proposal Disclosure document. Most brokers receive an upfront commission and a trail commission from the lender, which means you usually pay nothing for their expert guidance. The trail commission is a small ongoing payment that actually works in your favor. It incentivizes your broker to check in regularly and ensure your loan remains competitive years after settlement.

There is a common myth that brokers simply pick the lender that pays the highest commission. Under BID, this is illegal. Brokers must demonstrate that the recommended loan truly serves your best interest regardless of the payout. According to MFAA data from the September 2023 quarter, 74.1% of new residential home loans in Australia were facilitated by brokers. This record high percentage shows that Australians trust the broker model to deliver better, more transparent outcomes than going direct to a lender.

How to Choose the Right Finance Broker for Your Goals

Selecting the right finance broker is about finding a long-term partner who understands your financial roadmap. Start by scrutinising their lender panel. A robust panel should include at least 30 different lenders. This variety ensures you aren’t just seeing products from the “Big Four” banks. It should include non-bank lenders and credit unions that often offer more flexible terms for unique situations or self-employed borrowers.

Verify their professional standing before sharing your personal details. Every legitimate broker in Australia must hold an Australian Credit Licence (ACL) or be an authorised credit representative. Membership in the Mortgage & Finance Association of Australia (MFAA) or the Finance Brokers Association of Australia (FBAA) is essential. These bodies enforce strict ethical standards and continuing education requirements, ensuring your expert stays current with the latest regulations and market shifts.

The “Communication Test” helps you distinguish between a partner and a salesperson. A quality partner listens more than they talk. They should explain complex terms in plain English and focus on your long-term security rather than a quick settlement. If you require niche products like bridging loans or SMSF lending, ask for specific examples of how they’ve handled these cases in the past 12 months. This expertise ensures your application is positioned correctly from day one.

Key Questions to Ask During Your First Meeting

- “How many lenders do you have on your panel and why?” Look for a mix that includes major banks, second-tier lenders, and specialists to ensure genuine choice.

- “Can you explain how my loan will be structured to allow for future refinancing?” This ensures they’re building a path toward your future wealth, not just your current purchase.

- “What is your process for reviewing my loan after it settles?” A true partner provides ongoing support to ensure your rate remains competitive as the market changes.

Red Flags to Avoid in a Broker

Watch out for any pressure to sign documents before you’ve had time to fully understand the loan structure. Transparency is non-negotiable. If they can’t clearly explain their commission structure or potential fees, it’s a sign to look elsewhere. A limited lender panel that only features the major banks is another warning sign. According to 2023 industry data, roughly 71% of all new residential home loans in Australia are facilitated by brokers, so you deserve a finance broker who offers genuine variety and tailored advice.

Ready to find a loan that fits your life? Book a complimentary strategy session with our expert team today.

The Home Loan Partners: Your Strategic Finance Partner

The Home Loan Partners operates as more than just a service provider. We function as your long-term ally in a market that often feels overwhelming. Choosing a finance broker means you gain an advocate who understands the nuances of the Australian Credit Licence requirements and the shifting interest rate environment of 2024. Our access to a panel of over 36 lenders allows us to filter through thousands of products to find the competitive edge you need. This panel includes the Big Four banks alongside nimble boutique lenders that often offer more flexible terms for unique situations.

We take our “Stress-Free” promise seriously. By managing every bank interaction and technical hurdle, we free you up to focus on the property itself. Our commitment to your journey doesn’t end when you receive the keys. We provide ongoing support well beyond the settlement date, conducting regular reviews to ensure your loan remains aligned with your evolving life stages. As an experienced finance broker, we stay by your side for the life of your mortgage, ensuring you never pay more than necessary as market conditions change.

Our Process: From First Consultation to Settlement

We’ve refined our workflow into three clear stages to remove the guesswork from your property journey. This structured approach ensures nothing is left to chance.

- Step 1: The Discovery Phase. We dive into your specific 2026 financial goals. By assessing your current income, expenses, and liabilities, we determine your true borrowing power based on current APRA serviceability buffers.

- Step 2: Strategy and Comparison. We present a curated shortlist of options from our panel of 36+ lenders. This comparison goes deeper than just the headline interest rate; we analyze offset account benefits, redraw facilities, and annual fee structures to find the best fit.

- Step 3: Application and Management. Our team handles the heavy lifting. We package your application to meet specific lender criteria, manage the bank’s requests for information, and push for a seamless settlement.

Ready to Secure Your Financial Future?

The Australian property market moves quickly. With 2024 seeing significant shifts in lending criteria, reviewing your current mortgage or investment strategy is a vital step for long-term security. An obligation-free consultation allows you to see where you stand without any financial pressure or commitment. We provide the clarity you need to make an informed decision about your equity and future repayments. Achieving the Australian dream of homeownership is a major milestone, and we’re here to ensure you reach it with confidence. Let’s start building your future together.

Take Control of Your Property Journey in 2026

Navigating the Australian lending market requires a strategy that looks beyond today’s interest rates. By understanding the protection offered by the Best Interests Duty, you can move forward with the confidence that your financial goals are the top priority. Whether you’re a first home buyer entering the market or an investor expanding a portfolio, working with a professional finance broker provides the expert guidance needed to simplify complex choices. You gain direct access to a panel of 36+ lenders, ensuring your loan structure is tailored to your specific life stage and future security.

At The Home Loan Partners, we act as your steady hand in a shifting economy. We handle the heavy lifting and translate bank jargon into plain English so you stay in control of the process. It’s about more than just a transaction; it’s about a long-term partnership that supports your aspirations for years to come. Speak with a Partner today to explore your 2026 finance options and discover how a tailored approach makes all the difference. We’re ready to help you turn your homeownership goals into a reality with patience and precision.

Frequently Asked Questions

Is it free to use a finance broker in Australia?

In most cases, you won’t pay a fee to use a finance broker because lenders pay them a commission after your loan settles. This commission includes an upfront payment and a trailing commission, which typically ranges from 0.65% to 0.70% of the loan balance. While some brokers may charge a service fee for complex commercial structures, 85% of residential mortgage brokers in Australia offer their services at no direct cost to the borrower.

Will a broker get me a better interest rate than a bank?

You’ll often secure a more competitive interest rate through a broker because they compare products from over 30 different lenders. While a single bank only offers its own products, a broker negotiates on your behalf to find lower rates that aren’t always advertised to the public. Accessing these wholesale channels can save you thousands of dollars over the life of your loan compared to walking into a branch alone.

How does the Best Interests Duty protect me as a borrower?

The Best Interests Duty is a statutory obligation introduced on 1 January 2021 that requires brokers to legally act in your best interests. This law ensures your finance broker prioritizes your needs over their own commission or the lender’s profit. If a broker suggests a loan that isn’t the best fit for your specific financial goals, they’re in breach of the law; this provides a level of protection you don’t get when dealing directly with a bank.

Can a finance broker help with business or equipment loans?

Yes, brokers provide expert guidance for business and equipment financing, including chattel mortgages and hire purchase agreements. Whether you need A$50,000 for a new delivery van or A$2,000,000 for commercial property, a broker streamlines the application process. They understand the specific tax implications and cash flow requirements that 40% of small business owners struggle with when applying for traditional bank finance through standard channels.

How long does the loan application process take with a broker?

You can typically expect the entire process from initial consultation to loan settlement to take between 21 and 45 days. Pre-approval often happens within 2 to 5 business days, depending on the lender’s current processing speeds. Your broker manages the timeline by following up with banks daily. This proactive approach reduces the average processing time by up to 30% compared to self-managed applications where the borrower handles all the communication.

Do I need a finance broker if I am just refinancing?

Refinancing is one of the most effective times to partner with a finance broker to ensure your current lender remains competitive. Since interest rates and bank policies change frequently, a broker reviews your current A$500,000 mortgage against the latest market offers to find potential savings. Many Australians who refinance through a broker reduce their interest rate by an average of 0.50%, which saves roughly A$2,500 annually in interest charges.

What documents do I need to provide to a broker?

You’ll need to provide 100 points of identification, your two most recent payslips, and your last two years of group certificates or tax returns. Brokers also require three months of bank statements to verify your living expenses and savings history. Having these digital documents ready allows your guide to submit a polished application that meets the strict 2024 lending criteria. This preparation significantly increases your chances of a fast approval on the first attempt.

Can a broker help if I have a low deposit or am self-employed?

Brokers specialize in finding solutions for borrowers with a deposit as low as 5% or those who’ve been self-employed for less than two years. They have access to “low doc” loans and government schemes like the First Home Guarantee, which supports 35,000 places annually for low-deposit buyers. Your partner will identify the specific lenders who view self-employed income more favorably, helping you navigate hurdles that often result in rejections at major banks. If you’re searching for home loans in North Sydney with a low deposit or non-standard income, a broker’s access to specialist lenders can make the difference between approval and rejection.