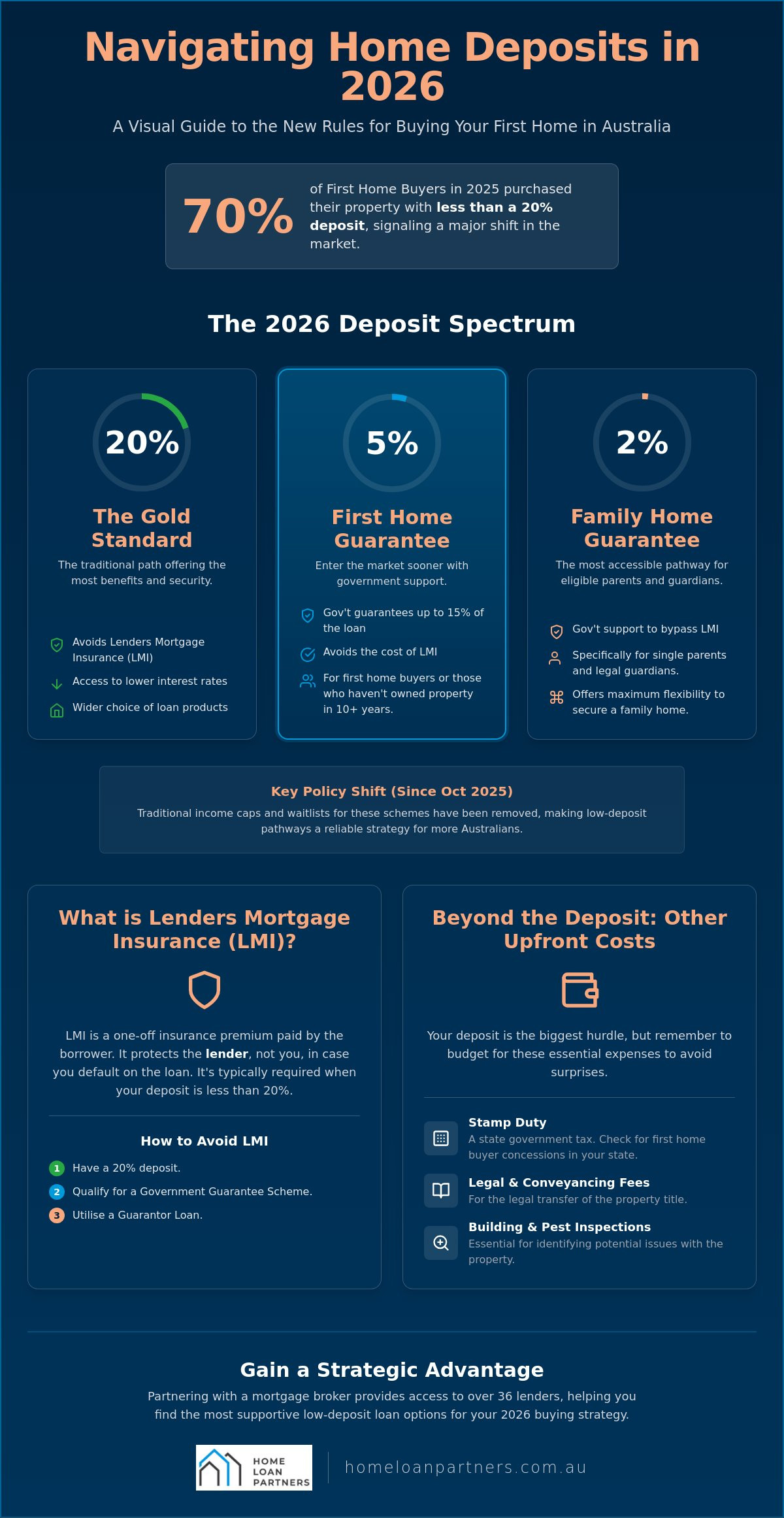

In 2025, 70% of first home buyers chose not to wait until they had saved a full 20% deposit before purchasing their property. If you are currently scanning listings and wondering, “how much deposit do I need for a house in 2026,” you are likely finding that the old rules no longer apply. Saving for a home while paying record-high rent can feel like running a race where the finish line keeps moving. It’s completely normal to feel overwhelmed by the updated government rules or the fear that Lenders Mortgage Insurance (LMI) will eat your hard-earned savings.

We’re here to show you that homeownership is closer than you think. You’ll discover the exact deposit requirements for the 2026 Australian property market, from the traditional 20% gold standard to 2% government-backed pathways that bypass LMI entirely. We will walk you through the removal of federal income caps, state-specific stamp duty concessions, and the strategic steps you can take to secure your 2026 buying strategy with confidence. Let’s map out your path to a new front door together.

Key Takeaways

- Master the difference between the 20% “gold standard” and lower entry points by understanding how Loan-to-Value Ratios (LVR) impact your borrowing power.

- Determine “how much deposit do I need for a house in 2026” by exploring the latest government pathways for first home buyers, single parents, and legal guardians.

- Uncover the true cost of Lenders Mortgage Insurance (LMI) and discover how guarantor loans can help you secure a home with no deposit at all.

- Identify the essential upfront costs beyond your deposit, including current 2026 stamp duty concessions and legal fees across different Australian states.

- Gain a strategic advantage by partnering with a mortgage broker who can access over 36 lenders to find the most supportive low-deposit loan options.

The 2026 Deposit Landscape: Is 20% Still the Standard?

The 20% deposit has long been hailed as the “gold standard” in Australian real estate. For decades, it was the benchmark that separated serious buyers from those still on the sidelines. To understand why this number matters, we need to look at the Loan-to-Value Ratio (LVR). This is a simple calculation lenders use to determine how much of the property’s value they are financing. If you have a 20% deposit, your LVR is 80%. Understanding what a mortgage is and how these ratios work is the first step toward a successful purchase. While this 20% figure remains a powerful goal, the answer to “how much deposit do I need for a house in 2026” is now far more flexible than it used to be.

Lenders use your deposit size to gauge the level of risk they are taking. A larger deposit provides a safety net for the bank, which is why they traditionally offer their best interest rates to those with at least 20% saved. However, your deposit size does more than just secure the loan; it dictates your monthly cash flow. A smaller deposit means a larger loan amount, which results in higher monthly repayments and more interest paid over the life of the loan. We work with you to balance these costs against the benefit of entering the market sooner.

Why Lenders Love a 20% Deposit

Lenders prioritize security and predictability. When you bring a 20% deposit to the table, you reduce the bank’s risk significantly. This lower risk usually rewards you with more competitive interest rates and a wider choice of loan products. You also skip the cost of Lenders Mortgage Insurance (LMI), which is a fee that protects the bank, not you. By starting with 20% equity, you’ve already built a financial buffer. If property prices fluctuate, you’re less likely to find yourself in a position where you owe more than the home is worth. It’s a position of strength that gives you immediate ownership of a significant portion of your asset.

The Shift in 2026 Property Entry Requirements

By 2026, federal policy shifts have effectively normalized 2% and 5% deposits by removing the traditional income caps that once restricted access to government guarantees. This change has triggered a massive psychological shift across the country. Buyers are no longer resigned to a decade of saving while property prices climb out of reach. Instead, many are choosing to enter the market sooner using government-backed schemes. While a smaller deposit means higher monthly repayments, it allows you to start building equity in your own home rather than paying off a landlord’s mortgage. In a market where prices often grow faster than savings, buying now with 5% can be a smarter long-term strategy than waiting years to reach 20%.

Federal Deposit Schemes: Buying with 2% or 5% in 2026

The path to homeownership in Australia changed significantly following the policy updates in late 2025. If you are currently calculating your savings and asking, “how much deposit do I need for a house in 2026,” the answer is no longer a fixed 20% wall. Federal interventions have moved these low-deposit pathways into the mainstream. Since October 1, 2025, the government has removed traditional income caps and waitlists for eligible buyers. This shift means that these programs are now a reliable strategy rather than a limited lottery for a lucky few.

These schemes apply nationally across Australia. Whether you are looking at an established house in the suburbs or vacant land for a new build, these guarantees provide a steady hand to help you reach your goals sooner. By removing the financial barriers that once forced buyers to rent for decades, the 2026 landscape prioritizes your security and long-term stability.

The 5% Deposit Scheme Explained

The First Home Guarantee allows eligible buyers to enter the market with as little as a 5% deposit. Under this arrangement, the Australian Government guarantees up to 15% of the property’s value to the lender. This partnership allows you to bypass Lenders Mortgage Insurance (LMI), which is often one of the most substantial upfront costs of buying a home. This scheme is open to first home buyers and those who have not owned a property in the last 10 years. It’s important to remember that while the deposit is lower, lenders still look for “genuine savings.” This typically means showing that you’ve consistently saved a portion of the funds yourself over at least a three-month period.

The 2% Pathway for Single Parents and Guardians

For single parents and legal guardians, the Family Home Guarantee offers an even more accessible entry point with just a 2% deposit. This scheme is specifically designed to empower those with at least one dependent child to achieve the security of homeownership. In 2026, this pathway has become a vital tool for family stability. In many regions, property value caps have been significantly adjusted to ensure that families can actually find suitable homes in their local communities. This scheme has no property value caps in many regions to better reflect the reality of the 2026 housing market. If you are balancing the demands of parenthood with the desire for a permanent home, our experts in First Home Buyer Loans can help you navigate the eligibility process with ease.

Lenders Mortgage Insurance (LMI) vs. Guarantor Loans

Lenders Mortgage Insurance (LMI) is a one-off fee that often causes confusion for first-time buyers. While you pay the premium, the policy actually protects the lender if you default on your loan. It’s the primary tool banks use to manage the risk of low-deposit lending. When you are calculating “how much deposit do I need for a house in 2026,” you’ll find that LMI is usually required for any deposit under 20%. Instead of paying this fee upfront, most lenders allow you to “capitalize” the cost by adding it to your total loan balance. This means you pay it off slowly over time, though you will pay interest on that amount for the life of the loan.

Guarantor loans offer a different path by using a family member’s property equity as additional security. This partnership can effectively reduce your Loan-to-Value Ratio (LVR) to 80% in the eyes of the bank, even if you have no cash deposit at all. In 2026, this remains one of the most effective ways to enter the market without a decade of saving. It provides a steady, reliable way to bypass the high costs of insurance while securing a home today.

How to Avoid LMI Without a 20% Deposit

You don’t always need a massive savings account to skip LMI. The federal guarantee schemes we discussed earlier act as a government-backed substitute for LMI, allowing you to buy with 2% or 5% while the government “guarantees” the rest. Additionally, certain professionals like doctors, lawyers, and engineers may still qualify for professional waivers. These specialized loan products often allow for a 10% deposit without any LMI charges because lenders view these industries as low-risk. A guarantor loan is another powerful option, where a parent uses their own home equity to bridge the gap, potentially allowing you to secure a loan with a 0% cash deposit.

When Paying LMI Might Actually Make Sense

Paying LMI isn’t always a negative financial move. It’s often a strategic “buy-in” fee that allows you to stop paying rent and start building equity. If property prices are rising faster than you can save, waiting three years to reach a 20% deposit might cost you $50,000 in capital growth, whereas an LMI fee might only be $15,000. This is the “opportunity cost” of waiting. You can model these different scenarios and see the exact impact on your repayments by using our home loan calculator. Deciding “how much deposit do I need for a house in 2026” becomes much easier when you compare the cost of the insurance against the cost of a rising market.

Beyond the Deposit: Upfront Costs to Budget For in 2026

When calculating how much deposit do I need for a house in 2026, it’s easy to focus solely on the percentage required by the lender. However, the purchase price and the deposit are just the beginning of the financial picture. You need to account for a suite of government and professional fees that can add tens of thousands of dollars to your total requirements. These costs must be paid in cash at settlement and cannot usually be added to your home loan.

Professional services are essential for a secure purchase. Conveyancing and legal fees typically range from $1,000 to $2,500; building and pest inspections generally cost between $400 and $800. Skipping these inspections might save a few hundred dollars today, but it risks thousands in future repairs. State governments also charge mortgage registration fees. As of June 2026, this is $175.70 in New South Wales and $125.70 in Victoria. These smaller costs add up quickly, so including them in your initial savings plan is vital for a stress-free experience.

The Reality of Stamp Duty in 2026

Stamp duty remains the largest hurdle beyond the deposit itself. Fortunately, 2026 brings several concessions for first home buyers. In New South Wales, you’ll find full exemptions for properties up to $800,000, with concessions available up to $1 million. Victoria offers exemptions up to $600,000, while Queensland provides them for established homes up to $700,000. For buyers targeting the Queensland market, Brisbane City Home Loans can help you navigate these local concessions and lender requirements. It is vital to remember that if your property falls outside these thresholds, you must have the full stamp duty amount ready as “cash on hand” on top of your deposit. This means your total savings goal must be your deposit plus these additional government charges.

The ‘Buffer’ Fund: Preparing for the Unexpected

Lenders often look for a “buffer” in your savings to ensure you aren’t financially stretched the moment you get the keys. This fund covers moving costs, utility connections, and those minor initial repairs that every new home seems to need. We recommend setting aside an additional 1-2% of the purchase price for peace of mind. Having this safety net ensures your transition into homeownership is a celebration rather than a source of stress. If you’re ready to see how these costs fit into your specific budget, our team can help you prepare for First Home Buyer Loans with a clear, step-by-step plan.

How a Mortgage Broker Optimises Your 2026 Deposit Strategy

The complexity of the current market means that finding the answer to “how much deposit do I need for a house in 2026” is only half the battle. Once you’ve identified a 2% or 5% pathway, you need a lender whose internal policies actually support those specific government guarantees. Not every bank treats these schemes the same way. We act as your intermediary, filtering through a panel of over 36 lenders to identify the ones that offer the most favourable terms for your specific deposit size. This precision-oriented approach ensures you aren’t just getting a loan, but the right loan structure for your long-term security.

Our role involves more than just comparing interest rates. We translate the technical jargon of 2026 lending into a clear, actionable plan. Terms like “capitalised LMI,” “shared equity,” and “LVR thresholds” can feel overwhelming, but we distill these into manageable concepts. By managing the heavy lifting of the application process, we allow you to focus on finding the right property. We help you understand exactly how much deposit do I need for a house in 2026 by looking at your total financial picture, including your income, existing debts, and long-term goals.

Navigating the Panel of 36+ Lenders

Going direct to a single bank limits your options to their specific products. If their current policy isn’t “low-deposit friendly,” you might be told you need a larger savings pot than is actually required. As your expert collaborator, we provide unbiased advice across a vast range of products. We understand which lenders allow you to “stack” government grants with professional LMI waivers or guarantor support. This collaborative approach maximizes your borrowing power while minimizing your initial cash outlay. We prioritize your understanding above all else, ensuring you feel confident in the lender we select together.

Your Partner in the Property Journey

We recognize that buying a home is one of the most significant life milestones you’ll ever achieve. It’s an emotional journey that deserves a steady hand and a protective guide. Our role extends far beyond the initial settlement of your First Home Buyer Loans. We stay by your side as your equity grows, helping you plan for future Refinancing once you hit that 20% equity mark to secure even better rates. This focus on longevity ensures your financial strategy remains robust as your life evolves. If you’re ready to see how much you need, Connect with our team for a personalised strategy.

Your Path to Property in 2026 Starts Today

The 2026 property market offers more flexibility than ever before. Whether you’re aiming for the 20% gold standard or utilizing a 2% government pathway, the answer to “how much deposit do I need for a house in 2026” depends entirely on your personal goals and financial health. Success comes down to balancing your initial savings with the reality of upfront costs like stamp duty and professional fees. By understanding these diverse options, you’ve already taken the first step toward long-term security and family stability.

Our team is here to manage the heavy lifting and provide the steady hand you need. With access to over 36 leading Australian lenders and dedicated offices in Greenwich and Port Macquarie, we offer the expert guidance first home buyers and investors deserve. We pride ourselves on building lasting partnerships that extend far beyond your first settlement. We’re ready to translate complex jargon into a clear, stress-free strategy tailored to your future.

Start your stress-free home buying journey with a tailored loan strategy. We look forward to helping you achieve your major life milestones with confidence and precision.

Frequently Asked Questions

Can I use the First Home Super Saver Scheme (FHSS) for my deposit in 2026?

Yes, you can use the FHSS to save for your deposit by making voluntary contributions to your superannuation fund. In 2026, this remains a tax-effective way to build your savings because you can withdraw these contributions plus associated earnings to put toward your home purchase. This strategy works well alongside government guarantees, helping you reach your required savings goal faster while reducing your taxable income during the saving phase.

Is Lenders Mortgage Insurance (LMI) refundable if I pay off my loan early?

Generally, LMI is not refundable once it has been paid or capitalized into your loan balance. It is a one-off premium that protects the lender for the entire duration of the risk period rather than a recurring fee. While some lenders previously offered partial refunds if the loan was refinanced within a very short window, this practice is rare in 2026. Most buyers should view LMI as a necessary cost to enter the market sooner.

Do I need ‘genuine savings’ if I have a guarantor for my home loan?

Most lenders still require you to demonstrate some level of genuine savings even when using a guarantor loan. While the guarantor’s equity covers the deposit percentage, banks want to see that you have the financial discipline to save and manage your money. Typically, this means showing a history of savings or consistent rent payments equivalent to 5% of the property value over at least a three-month period. This helps the bank feel confident in your repayment ability.

How much does stamp duty cost for a first home buyer in 2026?

Your stamp duty cost depends entirely on the state where you are buying and the value of the property. In 2026, many first home buyers pay zero stamp duty due to expanded exemptions. For example, in New South Wales, properties up to $800,000 are fully exempt. If you buy above these thresholds, the cost can range from a few thousand to tens of thousands of dollars. We recommend checking your specific state’s current thresholds during your planning phase.

Can I buy a house with a 2% deposit if I am not a single parent?

Yes, you can potentially access a 2% deposit pathway through the Help to Buy shared equity scheme if you meet specific income requirements. While the Family Home Guarantee is reserved for single parents and guardians, the shared equity program is open to other eligible buyers. In this arrangement, the government provides a portion of the purchase price in exchange for a share of the equity, significantly lowering your initial “how much deposit do I need for a house in 2026” requirement.

What happens if the property valuation comes in lower than my deposit calculation?

If the bank’s valuation is lower than the purchase price, you may need to increase your cash deposit to cover the shortfall. Lenders calculate your Loan-to-Value Ratio (LVR) based on the lower of the purchase price or the valuation. For example, if you planned a 5% deposit on a $600,000 home but it values at $580,000, the bank only lends against that $580,000. You would need to find the $20,000 difference in cash to proceed.

Are there income limits for the 5% Deposit Scheme in 2026?

No, the federal government removed the traditional income caps for the First Home Guarantee as of October 1, 2025. This change makes the scheme accessible to a much broader range of Australians regardless of their annual earnings. The 2026 rules focus primarily on your status as a first-time buyer or someone who hasn’t owned property in the last decade. This shift simplifies the path to homeownership for many households that were previously excluded based on their income.

How long does it take to get a home loan approved with a 5% deposit?

Approval times for low-deposit loans typically range from five to ten business days depending on the lender’s current volume. Because these loans involve government guarantees or LMI, the credit assessment can be slightly more rigorous than a standard 20% deposit application. Providing all your documentation upfront, such as payslips and bank statements, helps us speed up the process. We work closely with our panel of lenders to ensure your application moves through the system efficiently.