Your dream of homeownership in 2026 doesn’t require a 20% deposit, even though 68% of first-time buyers still believe this is the mandatory gold standard. You’ve likely spent over 45 hours this month researching suburbs and asking yourself, “how do i buy a house in australia” without finding a straight, simple answer. It’s exhausting to worry about hidden costs like stamp duty or the looming threat of a rejected loan application. We understand that this isn’t just a financial transaction; it’s your future security and peace of mind.

We’re here to be your expert partner throughout this entire journey. This guide provides a clear, 10-step roadmap that simplifies the complex lending environment into a seamless and predictable experience. You’ll learn exactly how to calculate your borrowing power, manage auction anxiety, and navigate the specific 2026 grant landscape with total confidence. We’ll walk through every milestone from the initial savings plan to the final settlement day so you can move forward without the stress.

Key Takeaways

- Learn how to build a solid financial foundation by navigating the deposit “gold standard” and understanding how Lenders Mortgage Insurance affects your initial costs.

- Discover the answer to “how do i buy a house in australia” by maximizing your borrowing power and leveraging a mortgage broker to secure a tailored pre-approval.

- Master the transition from searching to investigating properties with a guide to essential due diligence and non-negotiable building inspections.

- Gain the strategic confidence to negotiate successful offers and exchange contracts, whether you are buying through a private treaty or at a fast-paced auction.

- Understand the final legal transition on settlement day and how a long-term partnership ensures your mortgage continues to serve your future security.

Step 1: Building Your Financial Foundation and Deposit

Embarking on the journey toward homeownership is a major milestone that requires a solid plan. For many, achieving The Great Australian Dream starts with a clear look at your bank balance and a strategic approach to your savings. In 2026, understanding how do i buy a house in australia means looking beyond traditional myths and exploring modern financial tools that help you secure a home sooner.

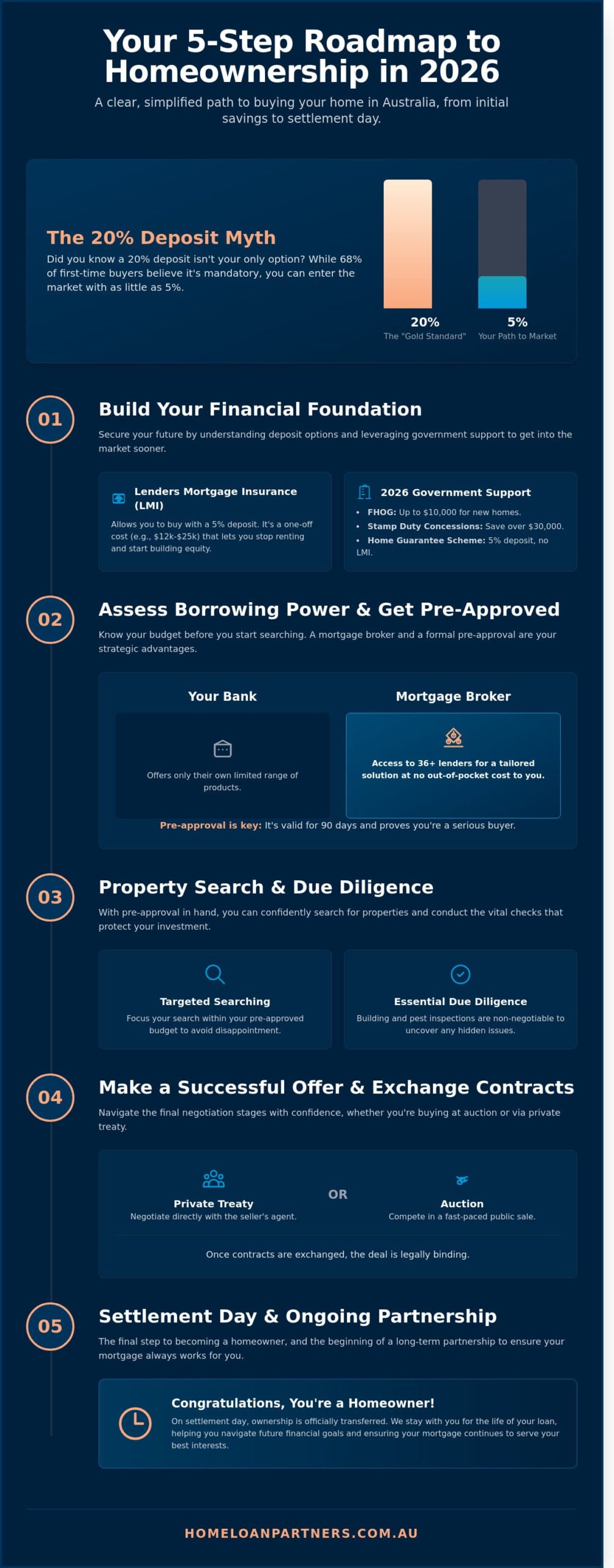

The Reality of the 20% Deposit

Saving $160,000 for an $800,000 property takes many households years of disciplined effort. While a 20% deposit is the gold standard because it avoids extra costs, it isn’t your only option. Lenders Mortgage Insurance is a one-off insurance premium that protects the lender against financial loss if you default on your loan, not the borrower. By paying LMI, you can enter the market with a deposit as low as 5%, or even 2% for eligible single parents. While this adds an upfront cost, often ranging from $12,000 to $25,000 depending on your loan size, it allows you to stop renting and start building equity today.

Government Support and Incentives

The Australian government provides several pathways to bridge the deposit gap. Learning how do i buy a house in australia involves maximizing these 2026 incentives to keep more cash in your pocket. These programs include:

- First Home Owner Grant (FHOG): In 2026, many states offer up to $10,000 for buyers purchasing or building brand-new homes.

- Stamp Duty Concessions: These can save you over $30,000 in upfront costs. For example, in New South Wales, full exemptions often apply to homes priced up to $800,000. Learn exactly how these thresholds work and whether you qualify in our detailed guide to first home buyers stamp duty NSW exemptions and savings.

- Home Guarantee Scheme: This federal initiative provides 35,000 places annually, allowing you to buy with a 5% deposit without paying any LMI.

Lenders also require “genuine savings” to prove your financial reliability. This usually means showing that 5% of the purchase price has been held in your account for at least 90 days. It can’t be a one-time gift or a lucky win. We’ll partner with you to review your statements and ensure your savings meet these strict criteria. This preparation ensures your transition from renter to owner is a seamless, supported experience.

Step 2: Assessing Borrowing Power and Securing Pre-Approval

Understanding your financial ceiling is a vital part of learning how do i buy a house in australia. Borrowing power is the maximum amount a lender will permit you to commit to based on your income, expenses, and existing debts. In the 2026 lending environment, banks look closely at your Debt-to-Income (DTI) ratio. Most Australian lenders flag applications where the DTI exceeds 6.0; this means if your total debt is more than six times your gross annual income, your options may narrow. Our detailed guide to understanding your debt to income ratio in the 2026 Australian property market explains exactly how lenders calculate this figure and what steps you can take to optimize your profile before applying. We help you manage these figures to ensure your application remains strong and attractive to lenders.

The Mortgage Broker Advantage

Choosing a mortgage broker over a single bank provides a significant strategic advantage. While a bank can only offer you their own limited products, a broker acts as a dedicated partner with access to 36 or more different lenders. This allows for a tailored loan structure that fits your specific life goals rather than a one-size-fits-all solution. The process is seamless because brokers operate on a no-cost model; the lender pays the broker a commission, meaning you receive expert guidance without an out-of-pocket fee.

The Path to Pre-Approval

You shouldn’t start attending open homes until you have a formal pre-approval in hand. This document proves to real estate agents that you’re a serious contender and gives you a firm budget to work with. It’s a key milestone mentioned in the Australian Government’s guide to buying a house as it protects you from overextending financially. To secure this, you’ll need to gather several documents:

- Three months of recent payslips and a summary of your employment history.

- Tax returns and Notice of Assessments for the last two financial years.

- Detailed statements of your monthly living expenses, including subscriptions and credit card limits.

Most pre-approvals are valid for 90 days. If you don’t find the right property within that window, we can help you refresh the application to keep your buying power current. If you’re ready to see where you stand, use our borrowing power calculator for an initial estimate. This tool provides a clear starting point for your journey. As your expert guide, we’ll then refine these numbers to show you exactly how do i buy a house in australia with confidence. If you’d like a more personalized assessment, feel free to reach out to our team for a chat about your unique goals.

Step 3: Property Search and Essential Due Diligence

Transitioning from a casual browser to a serious buyer requires a shift in mindset. You’re no longer just looking for a layout that fits your lifestyle; you’re hunting for potential risks that could impact your financial security. If you’re wondering how do i buy a house in australia while avoiding common pitfalls, the secret is in the details that don’t appear on a glossy real estate brochure. We act as your partner during this phase, helping you look past the staging furniture to the bones of the investment.

The Inspection Phase

A second walkthrough is your chance to investigate the property’s health. Look for sagging ceilings, damp smells, or windows that stick, as these can be signs of structural movement or poor drainage. In the 2026 market, expect to pay between $600 and $900 for a comprehensive professional building and pest inspection. This report identifies termite activity or major structural defects that could cost you over $35,000 to repair later. We recommend attending the inspection so the expert can show you exactly what they find in real time.

Legal and Contractual Review

Engaging a solicitor or conveyancer early provides a protective layer for your interests. They perform a Title Search to ensure the vendor has the legal right to sell and to check for encumbrances. These are restrictions, such as a utility company’s right to access pipes under your land, which might prevent you from building a deck or pool. Learning how do i buy a house in australia involves more than just bidding; it requires a disciplined approach to the fine print of the contract of sale.

The Section 32, or Vendor Statement, is the most critical document you’ll review with your legal team. It contains information about zoning, council rates, and any heritage overlays that limit renovations. We always advise our clients to include a “Subject to Finance” clause in their offer. This ensures that if your final bank valuation falls short, you can withdraw without losing your 10% deposit. The Australian government’s guide to buying a house highlights that understanding these legal obligations early prevents costly surprises at settlement. Our team works closely with your conveyancer to ensure every document aligns with your long-term financial security.

Step 4: Making a Successful Offer and Exchanging Contracts

Finding the right property is a major milestone. Securing it requires a strategic approach and a clear head. When you ask how do i buy a house in australia, the answer often hinges on the method of sale. Most properties sell through private treaty or at auction. Each path demands a different mindset to protect your interests and your budget. We’re here to guide you through these high pressure moments so you can sign with confidence.

Private Treaty vs. Auction

Private treaty sales offer a measured negotiation process. You have the benefit of time to discuss the price and include protective conditions. You might make an offer “subject to finance” or “subject to a satisfactory building inspection.” This gives you a safety net if your 2026 property report reveals unexpected structural issues. Most private treaty sales include a cooling-off period, typically five business days, though this varies by state. It acts as a final chance to review your decision before the deal becomes binding.

Auctions operate with total transparency because you see your competition in real time. However, they’re intense and leave no room for second guessing. An unconditional contract at auction means you are legally bound the moment the hammer falls. There is no cooling-off period. You must have your 10% deposit ready for immediate transfer and your legal checks completed before the first bid is placed. Many successful buyers in 2026 now use digital deposit bonds or instant bank transfers to handle this on the spot.

The Settlement Countdown

Once contracts are exchanged, the settlement period begins. This usually spans 30, 60, or 90 days depending on what you negotiated with the seller. During this window, your legal representative works with the lender to finalize the title transfer. You aren’t just waiting for the keys; you’re preparing for the responsibilities of homeownership. You must organize building insurance before the settlement date. Most Australian lenders require a Certificate of Currency naming them as an interested party before they’ll release your funds.

Your final inspection is your last chance to ensure everything is in order. Schedule this 24 to 48 hours before settlement day. During this walk-through, check the following:

- All appliances, including ovens and dishwashers, are in working order.

- Light switches and plumbing fixtures function correctly.

- The seller has removed all rubbish and personal belongings.

- No new damage has occurred since you signed the contract.

If you find issues, your solicitor can request repairs or a price reduction before the final payment. We know this phase feels complex, but you don’t have to manage it alone. Our team can partner with you to ensure a seamless transition from offer to ownership.

Step 5: Settlement Day and Ongoing Mortgage Partnership

Settlement day is the official moment you finally become a homeowner. It’s the legal process where ownership transfers from the seller to you. Understanding the final steps of how do i buy a house in australia means focusing on this digital exchange. In 2026, this happens almost entirely through PEXA, the electronic platform that handles over 99% of Australian property transfers. This technology ensures your funds reach the seller and your title is registered with the state government instantly. It removes the risk of manual errors and paper delays that used to cause stress for buyers.

What Happens on Settlement Day

The heavy lifting on this day is done by your solicitor and your mortgage partner. They coordinate the electronic exchange of funds and the lodgement of land title documents through a secure digital workspace. You don’t need to attend a physical meeting or sign any last-minute papers. Once the digital “keys” are handed over in PEXA, your real estate agent will call you to collect the physical keys. This usually happens between 2:00 PM and 4:00 PM on the agreed date. To prepare for your new financial commitment, you can use our mortgage repayment calculator to map out your first month of payments and ensure your budget is ready for the transition.

The Long-Term Partnership

Your journey doesn’t end when you get the keys. A common question when researching how do i buy a house in australia is what happens after the sale. We believe in staying by your side for the life of the loan. Brokers receive a “trail commission” from the lender, typically between 0.15% and 0.20% of your loan balance annually. This isn’t an extra cost to you. It’s a payment from the bank that ensures we’re available to answer your questions and manage your loan long after settlement.

We conduct annual reviews to ensure your interest rate remains competitive against the rest of the market. With the Reserve Bank of Australia now meeting 8 times a year to determine the cash rate, having a trusted guide is vital for reacting to market changes. As your property value grows, we’ll help you unlock equity. If your home value increases by $100,000, you might access a portion of that to fund a renovation or secure an investment property. We’re here to turn your first home into a foundation for your future security and long-term wealth.

Take the Next Step Toward Your Australian Home

Securing your place in the 2026 property market requires a blend of financial readiness and strategic action. You’ve seen that building a strong deposit and obtaining a formal pre-approval are the essential first steps to becoming a competitive buyer. By conducting thorough due diligence and mastering the contract exchange process, you protect your future equity and ensure a smooth transition to settlement day. When you find yourself wondering how do i buy a house in australia without the stress, remember that expert support makes all the difference. Our team provides access to over 36 lenders, ensuring you receive a tailored solution rather than a generic bank product. We offer expert guidance for first home buyers and deliver unbiased, professional advice that prioritizes your interests at every stage of the journey. We’re ready to act as your long-term partner, navigating the complexities of the lending landscape so you can focus on finding the perfect front door. Start your home buying journey with a Trusted Partner. Your dream home is within reach, and we’re here to help you claim it.

Frequently Asked Questions

Can I buy a house in Australia as a temporary resident or on a visa?

Yes, you can purchase property as a temporary resident, but you’ll typically need to obtain approval from the Foreign Investment Review Board (FIRB). This application process currently involves a fee of $14,100 for properties valued at $1 million or less. We’ll partner with you to navigate these requirements, as most lenders look for at least 12 months remaining on your visa before they’ll approve a mortgage.

How much are the hidden costs of buying a house, such as stamp duty and legal fees?

You should budget between 4% and 6% of the total purchase price to cover essential transaction costs. For a $800,000 home in New South Wales, stamp duty costs approximately $31,000, while professional conveyancing fees usually range from $1,500 to $3,000. Understanding these specific figures is a vital part of learning how do i buy a house in australia so you can plan your savings with total confidence. If you’re purchasing in NSW, our complete breakdown of first home buyers stamp duty NSW rules and eligibility thresholds can help you calculate your exact upfront costs.

What is the difference between an offset account and a redraw facility?

An offset account is a separate transaction account that reduces your loan interest, while a redraw facility lets you access extra repayments you’ve already paid into your loan. If you have $20,000 in a 100% offset account against a $500,000 mortgage, the bank only charges interest on $480,000. Offset accounts offer more day to day flexibility, whereas redraw facilities might have minimum withdrawal limits of $500 depending on your lender.

How long does the entire process of buying a house usually take in Australia?

The journey from your initial search to the final settlement day typically takes between 90 and 120 days. You’ll likely spend 30 to 60 days attending open homes and researching markets before you find the right property. Once your offer is accepted, the standard settlement period in states like Victoria or Queensland is usually 30, 60, or 90 days. We guide you through every milestone to ensure the experience is seamless.

Is it better to buy a house or an apartment as a first-time buyer in 2026?

Choosing between a house or an apartment depends on your budget, though houses generally offer 2% to 3% higher annual capital growth according to historical CoreLogic data. Apartments provide a more affordable entry point, with median prices in major capital cities often sitting $250,000 lower than houses. If your priority is long term equity, a house is often the better choice, while apartments suit those seeking a low maintenance lifestyle.

What happens if my home loan application is declined after I make an offer?

You can legally withdraw from the contract without penalty if you’ve included a “subject to finance” clause in your agreement. Without this protection, you risk losing your 10% deposit, which is a $75,000 loss on a $750,000 property. We work proactively to secure a pre-approval for you first, which reduces the risk of a late stage decline and gives you a steady hand when you start bidding.

Do I need to pay a mortgage broker for their services?

Most mortgage brokers don’t charge you a direct fee because the lender pays them a commission once your loan settles. This payment usually includes an upfront commission of 0.65% of the loan amount and a small ongoing trail commission. You get expert advice and a tailored loan strategy without adding another expense to your moving costs. It’s a partnership that focuses on your long term goals rather than a simple transaction.

What is a “subject to finance” clause and why is it so important?

A “subject to finance” clause is a protective condition that makes the property sale contingent on your bank’s final approval of your loan. It’s a critical safety net when you’re figuring out how do i buy a house in australia safely. This clause typically gives you 14 days to secure your funding. If the bank’s valuation is lower than expected or your finance fails, you can walk away with your deposit intact.