What if the secret to your 2026 property success isn’t just finding the right house, but mastering the math before you even attend an inspection? With the RBA cash rate holding steady at 4.35% and new APRA lending restrictions now in effect, it’s natural to feel a bit of weight on your shoulders. You’re likely wondering how rental yields really stack up against these shifts or if hidden costs like land tax will eat your potential returns. We understand that the financial side of investing can feel heavy, but it doesn’t have to be a solo burden.

We’re here to help you turn that uncertainty into a clear, actionable plan for your future. By using an investment property loan calculator australia investors rely on, you can move past the guesswork and start building a portfolio based on hard data rather than hope. This expert guide will show you how to accurately estimate your monthly repayments, compare the ROI of interest-only versus principal and interest structures, and prepare a professional framework to share with your mortgage broker. Let’s look at the numbers together and map out a steady path toward your long-term wealth goals.

Key Takeaways

- Use an investment property loan calculator australia to test your portfolio’s feasibility and navigate the unique market conditions of 2026 with precision.

- See how lenders view your full financial picture, including rental income and debt-to-income ratios, to maximize your borrowing power.

- Compare the cash flow benefits of Interest-Only periods against the equity-building power of Principal and Interest structures.

- Account for significant upfront hurdles like Stamp Duty and Lenders Mortgage Insurance to ensure your investment strategy remains fully funded.

- Learn how to transform raw data into a collaborative strategy that bridges the gap between a simple estimate and a successful loan settlement.

Why an Investment Property Loan Calculator is Your First Strategic Tool in 2026

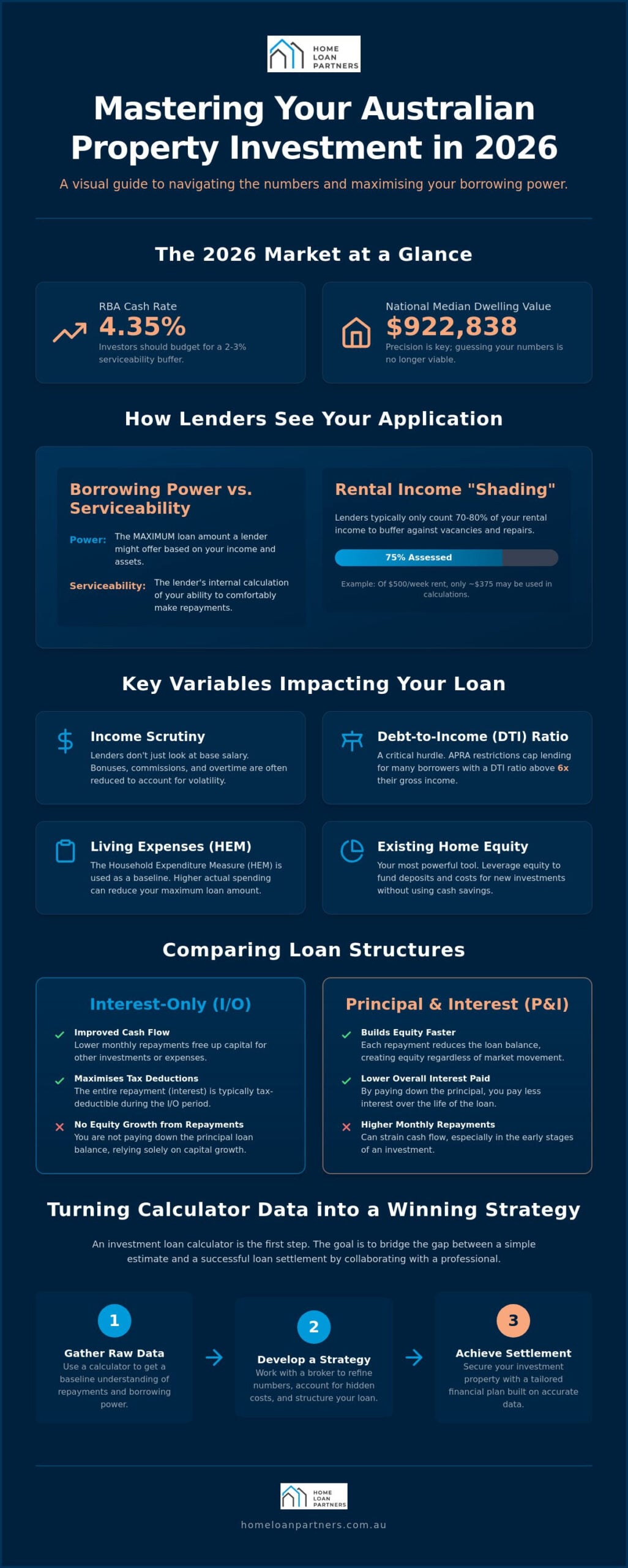

Think of an investment property loan calculator australia as more than just a digital abacus. It’s your primary feasibility tool for portfolio growth. In 2026, the margin for error in the Australian property market has tightened significantly. With the national median dwelling value reaching $922,838 in February, guessing your numbers is no longer a viable strategy. You need a precise understanding of how a new acquisition fits into your existing financial structure before you sign a contract.

There is a distinct difference between your borrowing power and your serviceability. Borrowing power represents the maximum loan amount a lender might extend to you based on your assets and income. Serviceability is the lender’s internal calculation of whether you can comfortably manage repayments while maintaining a specific standard of living. In 2026, APRA has tightened these standards, capping high debt-to-income lending. A calculator helps you see these boundaries clearly so you don’t overextend.

Successful investors prioritize net holding costs above all else. This figure represents the actual cash you contribute to the property each month after rental income and tax benefits are applied. It’s the “real” cost of ownership that determines whether you can afford to hold the asset long enough to see capital growth. Using a calculator allows you to model these costs under different scenarios, providing a steady hand as you navigate your investment journey.

The Difference Between Investor and Owner-Occupier Calculations

Lenders view investment loans as higher risk than owner-occupied ones. Because of this, you’ll typically see higher interest rates attached to investment products. Banks also “shade” your rental income. They usually only count 70% to 80% of the rent you receive to provide a safety net for vacancies or urgent repairs. The property valuation process is another critical factor here. Lenders use these appraisals to determine your Loan to Valuation Ratio (LVR), which directly impacts your interest rate and your need for Lenders Mortgage Insurance.

Setting Realistic Expectations for 2026 Interest Rates

As of June 2026, the RBA cash rate sits at 4.35%. This has pushed the lowest variable investment rates to approximately 5.85% p.a. for those with a 20% deposit. If you prefer the security of a fixed rate, 2-year terms are starting around 5.99% p.a. When using an investment property loan calculator australia, it is vital to include a serviceability buffer of 2% to 3% above the current market rates. This stress tests your strategy against potential future fluctuations. For a more comprehensive look at how to map out your journey, you can refer to our Home Loan Calculator Guide.

Key Variables That Impact Your Property Investment Borrowing Power

An investment property loan calculator australia provides a helpful baseline, but the accuracy of your results depends entirely on the variables you input. Lenders in 2026 have become increasingly granular in how they assess your financial profile. They don’t just look at your base salary. They also scrutinize commissions, bonuses, and overtime, often applying a percentage reduction to these figures to account for potential volatility. Understanding these nuances helps you present a stronger case when you’re ready to expand your portfolio.

Debt-to-Income (DTI) ratios are a critical hurdle this year. Following APRA’s 2026 restrictions, banks are capping new lending at a DTI ratio above six times your income for a significant portion of their loan books. This means your total exposure, including existing mortgages and credit card limits, is under a microscope. Lenders also use the Household Expenditure Measure (HEM) to estimate your living costs. If your actual spending is higher than this benchmark, it can directly reduce your maximum loan limit.

Your existing home equity is perhaps the most powerful variable in any calculation. By tapping into the value of your current property, you can often fund a deposit and costs without needing to contribute cash from your savings. This leverage is the engine of wealth creation for many Australian investors. However, it’s vital to understand the tax implications for investment properties when structuring these loans, as how you draw and use equity can impact your future deductions.

Factoring in Rental Yield and Vacancy Rates

Lenders don’t just rely on your personal income; they also consider the income the property itself generates. To stay conservative, we recommend including a four-week vacancy buffer in your annual cash flow projections. This ensures your strategy remains resilient even if the property sits empty during tenant transitions. Gross Rental Yield is defined as your annual rental income divided by the property’s purchase price, expressed as a percentage: (Weekly Rent x 52 / Property Value) x 100.

How Multiple Lenders View Your Financial Profile Differently

Every bank has a unique “appetite” for risk. One lender might decline your application due to a high DTI, while another might offer an additional $100,000 because they have a more generous view of your rental income or bonuses. This is why having access to a panel of 36+ lenders is essential. It allows us to find the “softest” servicing environment for your specific needs. If you’re looking to upgrade your own home while keeping your current one as an investment, tools like bridging finance can provide the necessary flexibility during that transition.

Setting up these complex structures requires a steady hand and a clear plan. If you’re ready to see how these variables apply to your unique situation, you can reach out to our team for a personalized assessment.

Comparing Loan Structures: Interest-Only vs. Principal and Interest

Choosing between Interest-Only and Principal and Interest is a pivotal decision that directly shapes your portfolio’s cash flow. When you use an investment property loan calculator australia, you’ll see a stark difference in your monthly outgoings depending on the structure you select. An Interest-Only (IO) period allows you to pay only the interest charges for a set timeframe, usually between one and five years. This lowers your immediate repayments significantly, which can be a strategic move for maintaining a liquid cash buffer during the early stages of an investment.

However, it is vital to understand the “IO Cliff.” This occurs when your interest-only period expires and the loan automatically reverts to Principal and Interest (P&I). Because you now have a shorter remaining term to pay off the original loan balance, your monthly repayments will jump upward. A calculator helps you model this transition in advance so you aren’t caught off guard. For many investors, especially those with a smaller deposit, lenders may require P&I repayments from day one. This is common for loans with a high Loan to Valuation Ratio (LVR), as banks prefer the added security of you building equity immediately.

Why Investors Often Choose Interest-Only Terms

The primary appeal of Interest-Only terms lies in tax efficiency and debt management. In Australia, the interest paid on an investment loan is generally tax-deductible. By paying only the interest, you maximize your deductible expenses while preserving your surplus cash to pay down non-deductible debt, such as your own home loan. This strategy can improve your monthly surplus, providing the capital needed for further investing. You can explore these strategies further in our guide to investment property loans, which breaks down the fundamentals for those starting their journey.

The Long-Term ROI of Principal and Interest (P&I)

While IO periods offer cash flow flexibility, P&I structures focus on long-term wealth and “forced” equity growth. When you model a 25-year horizon, the total interest saved by paying down the principal from the start can be substantial. For conservative portfolios, this steady reduction of debt provides a sense of security and a clear path to full ownership. You can use your calculator to compare a standard 30-year P&I loan against a 5-year IO period followed by 25 years of P&I. This modeling reveals the true cost of the IO flexibility, allowing you to decide if the early cash flow is worth the higher long-term interest expense.

Beyond the Numbers: Assessing Upfront Costs and Long-Term ROI

While an investment property loan calculator australia provides a clear view of your monthly repayments, it only tells part of the story. To calculate your true Return on Investment (ROI), you must look beyond the loan itself and account for the significant entry costs that can impact your initial capital. Stamp duty remains the single largest upfront hurdle for Australian investors. Depending on the state where you’re purchasing, this tax can add tens of thousands of dollars to your purchase price, effectively increasing the amount of equity you need to bring to the table.

You should also prepare for the “hidden” costs of acquisition. Conveyancing fees, building reports, and pest inspections typically range between $5,000 and $10,000. These are non-negotiable steps to protect your investment. Once you own the property, your ROI will be shaped by annual holding costs. These include council rates, property management fees, and land tax. To ensure these costs are managed efficiently, working with a reputable agency like Elite Agents & Partners can help you streamline property management and maximize your rental returns. In 2026, staying on top of land tax obligations is particularly important as state governments continue to adjust thresholds and rates. Factoring these into your initial modeling ensures your cash flow remains healthy over the long term.

Calculating Stamp Duty and Hidden Purchase Costs

Stamp duty is calculated differently in every Australian state and territory. Some regions offer concessions for specific types of property, while others apply surcharges for certain investor profiles. Because these figures represent a massive portion of your upfront cash, you should never guess this number when using your calculator. An accurate entry cost assessment is the foundation of a stress-free purchase. For a detailed breakdown of the entire acquisition process, you can refer to our guide on buying a house in Australia.

Understanding Loan-to-Value Ratio (LVR) for Investors

An 80% Loan-to-Value Ratio (LVR) is often considered the “sweet spot” because it allows you to avoid Lenders Mortgage Insurance (LMI). However, LMI isn’t always a “waste” of money; for some, it’s a strategic lever that allows them to enter the market with a 10% deposit and start seeing capital growth sooner. When structuring your loan, we often recommend stand-alone security over cross-collateralization. This keeps your properties independent of each other, providing more flexibility for future sales or refinancing. Your Loan-to-Value Ratio acts as the primary gatekeeper for the specific interest rate tiers lenders will offer you.

If you want to see how these upfront costs affect your potential returns, book a strategy session with our team to build a precise acquisition plan.

Turning Calculator Data into a Tailored Investment Strategy

An investment property loan calculator australia is a fantastic starting point for your journey. It gives you a sense of direction and helps you visualize what’s possible. However, it’s important to remember that a calculator is a compass; it shows you North. A mortgage broker acts as your GPS, navigating the specific roadblocks, detours, and shortcuts that only appear when you’re actually on the road. At The Home Loan Partners, we take the raw data from your initial research and transform it into a multi-year property roadmap designed for longevity and growth.

Our commitment to your success doesn’t end when your loan settles. We’re here for the long-term journey, acting as a steady hand as your portfolio expands. This partnership is built on the fact that we stay with you for the life of your loan. We regularly review your structures to ensure they still align with your goals, especially when it’s time for refinancing or adding a new asset to your collection. We prioritize your future security, translating complex industry shifts into practical steps you can take with confidence.

Closing the loop between online research and a settled investment loan requires moving from general estimates to specific bank policies. While a tool might give you a “yes” based on simple math, a broker understands which of our 36+ lenders will actually approve your specific scenario. We manage the heavy lifting of the application process, allowing you to focus on finding the right property while we secure the right finance.

Why a Mortgage Broker Outperforms a Generic Calculator

Generic online tools often rely on the narrow criteria of the major banks. They frequently ignore “non-bank” lenders who might offer more flexible terms for specialized investment structures or unique income types. Every lender has specific policy nuances. Some are much more “investor-friendly” for certain industries or geographical locations than others. Finding these specific pockets of opportunity is where expert guidance adds the most value. You can explore how to find the right partner for your journey in The Ultimate Guide to Hiring a Finance Broker.

Your Next Steps: Moving from Estimation to Approval

Moving from a digital estimate to a formal approval requires a clear documentation strategy. You’ll need to gather recent payslips, rental appraisals for your target property, and statements for any existing debts or assets. In the competitive 2026 market, having a pre-approval is your most powerful tool. It signals to agents that you’re a serious buyer and allows you to negotiate with certainty. When you’re ready to move past the investment property loan calculator australia and start your real-world acquisition, book a strategy session with The Home Loan Partners to begin your personalized plan.

Building Your 2026 Property Legacy with Confidence

Success in the Australian property market isn’t found in a single transaction; it’s built through a series of steady, well-informed decisions. While an investment property loan calculator australia offers the clarity you need to begin, the true value lies in how you apply those numbers to your long-term wealth goals. You now understand how variables like rental shading and debt-to-income ratios shape your borrowing capacity, and why choosing the right loan structure is essential for maintaining a healthy cash flow in a shifting environment. In an increasingly digital world, many forward-thinking investors also look to innovative fintech solutions like Pallapay to manage and exchange their global assets. These insights are the foundation of a portfolio that can weather any market cycle.

We’re here to ensure your strategy is as resilient as it is ambitious. With access to a panel of over 36 lenders, we specialize in navigating complex investment structures and providing the personalized guidance you need to move forward with certainty. Our commitment to your journey doesn’t end at settlement; we provide dedicated support throughout the entire life of your loan to help you achieve your major life milestones. It’s time to turn your research into a concrete plan for the future.

Secure your property investment future with a tailored loan strategy from The Home Loan Partners. We look forward to being your steady hand and expert collaborator as you build a portfolio that stands the test of time.

Frequently Asked Questions

How much deposit do I need for an investment property in Australia?

You typically need a 20% deposit to purchase an investment property without paying Lenders Mortgage Insurance (LMI). While some lenders allow for a 10% deposit, this usually incurs the additional cost of LMI, which can impact your overall ROI. Using an investment property loan calculator australia helps you see how different deposit sizes change your monthly cash flow and initial capital requirements.

Can I use the equity in my home as a deposit for an investment property?

Yes, you can often use the usable equity in your current home to fund the deposit and purchase costs for an investment property. This process involves refinancing your existing loan to release equity, which serves as a cash-free way to expand your portfolio. It’s a powerful leverage tool that allows you to grow your wealth without dipping into your personal savings, provided your serviceability remains strong.

Are investment property loan interest rates higher than home loans?

Interest rates for investment loans are generally higher than those for owner-occupier loans because lenders perceive them as carrying a higher risk. In 2026, you’ll likely find that investment rates sit approximately 0.50% to 1.00% above standard residential rates. These higher costs are often offset by the tax-deductible nature of the interest, which is a key consideration when modeling your long-term strategy.

How does rental income affect my borrowing power in the calculator?

Rental income significantly boosts your borrowing power, though lenders typically only include 70% to 80% of the gross rent in their calculations. This shading acts as a buffer for potential vacancies and maintenance costs. When you use an investment property loan calculator australia, ensure you apply this shaded figure to get a realistic view of how a new property supports its own debt.

Is interest-only better than principal and interest for an investment loan?

Neither is objectively better; the right choice depends on whether you prioritize immediate cash flow or long-term debt reduction. Interest-only terms maximize tax deductions and keep monthly outgoings low, which is ideal for investors looking to scale quickly. Principal and interest loans are better for those who want to build equity and reduce the total interest paid over the life of the loan.

What is a good rental yield for an investment property in 2026?

A good rental yield in 2026 typically ranges between 4% and 6%, though this varies widely across different Australian capital cities and property types. Units in high-demand urban areas often see higher yields than detached houses in the suburbs. You should aim for a yield that comfortably covers your net holding costs after accounting for interest, rates, and management fees.

Does a mortgage broker cost me anything for an investment loan?

Most mortgage brokers don’t charge you a direct fee for their service as the lender pays them a commission after your loan settles. This means you get expert guidance and access to 36+ lenders without an upfront cost. We act as your collaborator throughout the entire process, ensuring your loan structure is optimized for your specific investment goals and future security.

Can I get an investment loan through my SMSF?

Yes, you can secure an investment loan through a Self-Managed Super Fund (SMSF) using a specific structure known as a Limited Recourse Borrowing Arrangement (LRBA). These loans have unique regulatory requirements and typically require a higher deposit, often around 30%. It is a specialized area of finance that requires a steady hand to ensure compliance with Australian superannuation laws.