Fixing your mortgage isn’t actually a bet against the banks; it’s a premium you pay for the luxury of a good night’s sleep. With the Reserve Bank of Australia holding the cash rate at 4.35% as of June 2026, many homeowners feel caught between a rock and a hard place. You’re likely asking, “should I fix my home loan rate now australia,” because you want to protect your family’s budget from another unexpected jump in monthly repayments while inflation remains stubborn at 4.0%. It’s a stressful position to be in, especially when you’re trying to balance future security with the fear of being locked out of potential rate cuts or facing expensive break fees if your plans change.

We understand that managing a mortgage is about more than just numbers; it’s about the home and life you’re building. This guide provides the strategic framework you need to decide if locking in your rate is the right move for your specific financial journey this year. We’ll walk through the current lending landscape, the reality of break fees, and how to weigh the cost of certainty against the risks of staying variable. By the end, you’ll have a clear path forward to manage your debt with confidence and precision.

Key Takeaways

- Understand how the 4.35% RBA cash rate and current 4.0% inflation impact your mortgage repayments in the 2026 property market.

- Learn how to evaluate “should I fix my home loan rate now australia” by balancing the peace of mind of budget certainty against the need for financial flexibility.

- Discover why your property timeline, including plans to sell or renovate, is a critical factor in avoiding expensive break fees when locking in a rate.

- Compare the strategic advantages of fixed, variable, and split loan structures to find a personalized fit for your household budget.

- Explore how partnering with an expert to access a panel of over 36 lenders ensures your interest rate strategy remains aligned with your long-term goals.

Navigating the 2026 Interest Rate Environment in Australia

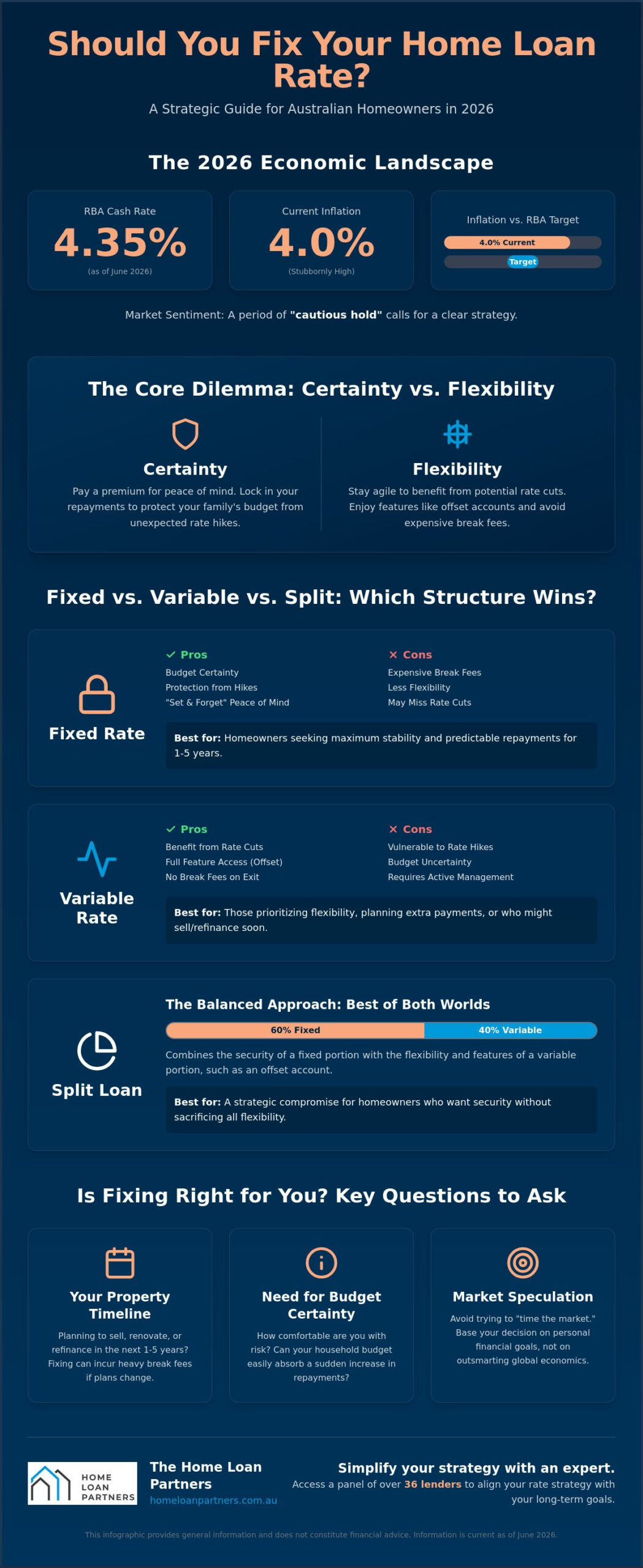

The Australian property market in 2026 has entered a phase of watchful waiting. With the Reserve Bank of Australia (RBA) maintaining the official cash rate at 4.35% as of June, many homeowners are feeling the weight of persistent inflation, which sat at 4.0% in May. This environment makes the question “should I fix my home loan rate now australia” more relevant than ever. When you choose to fix, you’re essentially buying a contract for certainty. You agree with your lender that your interest rate won’t change for a specific period, typically one to five years. To get a handle on the basics, it helps to understand what is a fixed-rate mortgage? and how it differs from a fluctuating variable rate.

Current market sentiment is defined by a “cautious hold.” While we aren’t seeing the rapid-fire hikes of previous years, the door remains open for further increases if inflation doesn’t retreat toward the RBA’s 2-3% target. For borrowers, this means 2026 is a pivotal year to evaluate whether they prefer the flexibility of a variable loan or the “set and forget” nature of a fixed rate. When you’re looking at offers, remember to prioritize the comparison rate. This figure includes both the interest rate and most associated fees, providing a more transparent view of the loan’s true cost over time.

How the RBA Cash Rate Influences Your Repayments

The cash rate is the benchmark for all Australian lending. It represents the interest rate that banks pay to borrow money from each other overnight. When the RBA moves this lever, there’s often a slight lag before your bank adjusts your variable rate. It’s rarely an instant transition. Interestingly, fixed rates don’t just follow today’s cash rate. Lenders price their fixed products based on where they expect the economy to be in two or three years. This is why you might see 1-year fixed rates starting around 5.99% p.a. even when variable rates are slightly lower; the bank is essentially pricing in their forecast of future risk and economic stability.

The 2026 Outlook: Stability or Volatility?

The 2026 economic landscape is currently a tug-of-war between a cooling job market and sticky inflation. While trimmed mean inflation has dipped to 3.6%, it’s still not quite where the RBA wants it. This makes a “wait and see” strategy for your mortgage potentially risky. Many Australians try to “time the market” to find the absolute bottom of a rate cycle, but this is incredibly difficult to get right. If you’re asking “should I fix my home loan rate now australia,” the answer often lies more in your personal need for budget protection than in trying to outsmart global economic shifts. Waiting too long for a cut that may not arrive quickly could leave you exposed to further volatility if global geopolitical tensions or local productivity issues spark another round of inflation.

Fixed vs. Variable vs. Split Loans: Which Structure Wins?

Deciding how to structure your mortgage is often the most critical step after asking “should I fix my home loan rate now australia.” While a fixed rate offers a rigid shield against rate hikes, a variable rate moves with the market. For many, the decision isn’t a binary choice between one or the other. You can consult this government guide to choosing a home loan to see the standard trade-offs, but the 2026 market requires a more nuanced strategy that considers your specific cash flow needs.

The Variable Rate Advantage

Variable loans are currently a popular choice for those who value agility. If the RBA decides to lower the cash rate from its current 4.35% later this year, variable borrowers will be the first to see their monthly repayments drop. These loans typically offer full access to features like redraw vs offset accounts, which can significantly reduce the interest you pay over the life of the loan. Since there are no break fees, you’re free to sell your property or switch lenders without the heavy financial penalties often associated with fixed contracts. This makes them ideal for homeowners who prioritize flexibility over a static budget.

Why a Split Loan Might Be the Smartest 2026 Move

A split loan is often the most balanced answer to the question of whether you should fix my home loan rate now australia. By dividing your mortgage into two portions, you get the best of both worlds. For instance, you might fix 60% of your loan to ensure your core repayments remain stable while leaving 40% variable. This structure allows you to use an offset account on the variable side to save on interest while enjoying the security of a “set and forget” budget on the fixed side. It’s a precision-oriented approach that caters to your specific risk tolerance in an economy where inflation and interest rates are still finding their footing.

It’s vital to check which features your lender allows on a fixed loan portion. While almost all variable loans include redraw and offset facilities, many fixed-rate products restrict these or cap extra repayments at a certain dollar amount per year. If you plan to make large lump-sum payments from a bonus or inheritance, a pure fixed-rate loan might actually cost you more in lost interest savings than you gain in rate protection. Balancing these features is key to ensuring your loan works for you, not the other way around.

Finding the right balance requires a steady hand and an understanding of your long-term goals. If you’re feeling unsure about which structure fits your lifestyle, reaching out for a professional refinancing review can provide the clarity you need to move forward with confidence.

The Strategic Case for Fixing: Certainty vs. Flexibility

Choosing to fix your interest rate is less about predicting the future and more about securing your present. In a market where the RBA cash rate sits at 4.35%, many households find that the primary value of a fixed loan is the ability to plan with precision. When you ask yourself, “should I fix my home loan rate now australia,” you’re really weighing the cost of a potential rate drop against the immediate benefit of knowing your exact monthly expenses. This approach turns your mortgage into a predictable utility rather than a variable stressor that changes with every economic headline.

The Psychological Benefit of Rate Certainty

For many Australians, the true value of fixing is the reduction in financial anxiety. In a high-cost-of-living environment where inflation is at 4.0%, having one major expense remain static is a significant advantage. It allows you to focus on other life milestones or long-term investment planning without the constant fear of a rate hike. Essentially, fixing is a premium for peace of mind rather than a market bet. According to Moneysmart’s guide to choosing a home loan, this stability is a key factor for those with tight monthly budgets or fixed incomes who need to protect their cash flow from unexpected shocks.

The Risks: What to Watch Out For

However, this certainty comes with distinct trade-offs. The most significant risk is locking in a rate just before a market downturn. If the RBA eventually cuts rates, you won’t benefit from lower repayments, and you could find yourself paying significantly more than the current market average. There is also the “revert rate” trap to consider. When your fixed term ends, your loan often automatically switches to the lender’s standard variable rate. This rate can be much higher than their best available offer, so you’ll need to be ready to act once the term expires.

You must also consider flexibility. Most fixed products limit your ability to make extra repayments, often capping them at small annual amounts. If you need to refinance your home loan or sell your property before the term is up, you may face substantial break costs. These costs are calculated based on market rate movements since you locked in; if rates have fallen, the fee to exit can be thousands of dollars. Currently, many borrowers are finding a sweet spot in one to three-year fixed terms. This duration provides enough time to weather short-term volatility without being locked into a specific rate for so long that you miss the next economic cycle.

Key Indicators: How to Tell if It is Time to Fix Your Rate

Deciding “should I fix my home loan rate now australia” requires looking inward at your household budget as much as outward at the Reserve Bank. While economic forecasts provide a general direction, your personal financial resilience is the most reliable compass. A practical starting point is to conduct a simple stress test on your cash flow. If variable rates were to climb by another 1.0%, could you comfortably absorb the increased monthly repayments without sacrificing your quality of life? If that extra cost feels like a significant burden, the certainty of a fixed rate acts as a protective shield for your family’s future.

Market signals also offer valuable clues. The “big four” banks price their fixed-rate products based on where they expect interest rates to be in the coming years. If you notice that fixed rates are starting to sit significantly higher than current variable offers, the banks are signaling they expect rates to remain elevated. Conversely, a narrow spread between the two suggests a more stable outlook. You should also consider your property timeline. If you plan to sell your home or undertake major renovations in the next three years, the rigidity of a fixed contract might lead to expensive break fees that outweigh any interest savings.

A 4-Point Checklist for the Fix-Rate Decision

To help you move forward with precision, we recommend following this straightforward checklist:

- Assess your buffer: Determine exactly how much of a rate hike your current income can support.

- Review future plans: Account for upcoming life changes, such as starting a family or taking parental leave, which may temporarily reduce your household income.

- Compare the spreads: Look at the difference between the lowest variable rates, currently around 5.69% p.a., and the available fixed terms.

- Consult a professional: Reach out to a finance broker to access off-market offers and tailored advice that banks might not disclose directly.

Understanding the Revert Rate

The rate you land on after your fixed term expires is just as critical as the fixed rate itself. This is known as the “revert rate.” Many borrowers are surprised to find they’ve been automatically shifted onto a lender’s standard variable rate, which is often much higher than the competitive rates offered to new customers. We suggest conducting a “mortgage health check” at least six months before your fixed term ends. This proactive approach gives you enough time to negotiate a better deal with your current lender or prepare for a stress-free transition to a new one. If you’re ready to see how your current loan stacks up against the latest 2026 market offers, our team can help you explore your refinancing options today.

How The Home Loan Partners Simplify Your Interest Rate Strategy

Deciding “should I fix my home loan rate now australia” is a significant financial choice, but you don’t have to make it in isolation. While online comparison tools often prioritize the lowest headline rate, they rarely account for the structural nuances that make a loan truly effective. We provide access to a diverse panel of over 36 lenders, including specialized non-bank institutions that often offer more competitive fixed-rate terms and greater flexibility than the major banks. Our role is to act as your expert collaborator, translating complex market data into a clear, stress-free path forward that prioritizes your family’s long-term security.

We take the heavy lifting off your shoulders by managing the entire application process and negotiating directly with lenders on your behalf. Our commitment to your journey doesn’t end when your loan is settled. We provide ongoing support by monitoring market shifts and RBA announcements, ensuring your interest rate strategy remains aligned with your goals as the economy evolves. By focusing on a partnership rather than a transaction, we help you navigate the 2026 property market with a sense of calm and steady expertise.

Beyond the Interest Rate: Structuring for Success

A successful mortgage strategy is built on more than just a percentage; it’s about how the loan is structured to fit your life. We help you determine the ideal split ratio for your household, balancing the protection of a fixed rate with the agility of a variable portion. Our team identifies lenders that offer sophisticated features, such as partial offset accounts on fixed-rate products, which are often overlooked by standard comparison sites. Whether your next milestone involves buying a house or expanding an investment portfolio, we ensure your debt structure supports those aspirations without unnecessary restrictions.

Start Your Stress-Free Property Journey

Choosing a mortgage through a personal relationship with a broker offers a level of precision that a cold online algorithm simply can’t match. We take the time to understand the emotional weight of your investment, providing protective guidance that shields you from common pitfalls like high break fees or restrictive revert rates. Our “trail support” means we stay by your side for the duration of your loan, ready to reassess your options whenever your circumstances change. If you’re ready to gain clarity on whether you should fix my home loan rate now australia, contact us today for a personalized assessment of your options and a clear plan for your financial future.

Securing Your Financial Future with Precision

Choosing how to manage your mortgage in 2026 isn’t just a mathematical equation; it’s about finding the structure that allows you to live your life without constant financial worry. We’ve explored how fixing your rate can provide essential budget certainty and why a split loan often serves as a balanced middle ground for those seeking both protection and flexibility. By aligning your loan structure with your personal property timeline and cash flow needs, you can turn your mortgage into a steady foundation for your long-term goals.

If you’re still weighing up whether you should I fix my home loan rate now australia, remember that you don’t have to navigate these complex markets alone. At The Home Loan Partners, we act as your expert guide, providing access to a panel of over 36 Australian lenders to find the specific fit for your needs. We pride ourselves on offering expert guidance on loan structuring and providing ongoing support for the life of your loan. Book a free rate strategy session with The Home Loan Partners today to gain the clarity you need. We’re here to ensure your property journey is smooth, predictable, and successful.

Frequently Asked Questions

Is it better to fix my home loan for 1, 3, or 5 years in 2026?

Choosing a term length depends on your personal need for certainty versus your desire to benefit from potential future rate cuts. In the 2026 market, many Australians find that a 1 to 3-year term offers a balance between immediate budget protection and the flexibility to reassess as economic conditions evolve. While 5-year terms provide maximum stability, they carry a higher risk of being locked into a rate if the market eventually trends downward.

Can I still use an offset account if I fix my mortgage rate?

Most traditional fixed-rate loans don’t offer full offset accounts, though some specialized lenders have introduced partial offset features or redraw facilities. If you’re asking “should I fix my home loan rate now australia” but want to keep using your savings to reduce interest, we can identify specific lenders that offer these flexible features. Alternatively, a split loan structure allows you to maintain a full offset account on the variable portion of your debt.

What are the typical break fees for a fixed-rate home loan in Australia?

Break fees are calculated based on how much market interest rates have dropped since you locked in your fixed rate. If you choose to sell your home or refinance before your term ends, these costs can potentially reach thousands of dollars. It’s a critical factor to consider if you plan on moving or changing your financial structure within the next few years, as the fee compensates the bank for the loss of interest income.

What happens to my repayments at the end of a fixed-rate term?

When your fixed term expires, your mortgage typically rolls over to the lender’s standard variable rate, also known as the “revert rate.” This rate is often significantly higher than the best available market offers, which can lead to a sudden jump in your monthly repayments. We recommend starting a mortgage health check six months before your term ends to negotiate a new competitive rate or transition to a different loan structure without stress.

Can I switch from a variable to a fixed rate at any time?

You can typically switch from a variable rate to a fixed rate at any time by contacting your lender or working with a broker. This process is usually straightforward and doesn’t require a full refinance if you stay with the same lender. It’s a common move for homeowners who notice rising volatility in the market and want to secure their budget against future interest rate hikes while inflation remains above the target range.

Is a split loan better than a fully fixed home loan?

A split loan is often considered a more versatile strategy than a fully fixed loan because it hedges your risks across two different structures. You get the budget certainty of a fixed portion while maintaining the features and potential rate-cut benefits of a variable portion. This structure is particularly effective in 2026, as it allows you to utilize an offset account on the variable side while protecting your debt from unexpected rate increases.

How much extra can I pay off my home loan if it is fixed?

Most fixed-rate products cap extra repayments at a specific dollar amount, often between $10,000 and $20,000 per year depending on the lender. If you exceed this limit, you may be charged a break fee or an early repayment penalty. If you expect a significant windfall or plan to pay down your debt aggressively, keeping a portion of your loan variable will allow for unlimited extra repayments without any financial penalties.

Will interest rates go down in late 2026?

While some economic forecasts suggest a potential easing of rates, the RBA maintains a cautious hold as inflation remains at 4.0%, which is still above the 2-3% target. Predicting the exact timing of a rate cut is difficult, and waiting for a bottom in the market can be a risky strategy. Most experts suggest making decisions based on your personal cash flow requirements and “should I fix my home loan rate now australia” rather than trying to time global economic cycles.