What if the “perfect” credit score you’ve been chasing doesn’t actually exist? It’s incredibly frustrating to check three different apps only to find three different numbers, leaving you wondering what credit score do i need for a home loan in australia to finally secure your keys. We understand the weight of that uncertainty. You might worry that a missed phone bill or a few Buy Now Pay Later purchases will trigger an automatic rejection. It’s a common fear, but the reality of the 2026 lending market is much more nuanced than a single number on a screen.

Lenders today are looking for a steady partner, not just a high digit. While a score of 700 is generally considered “good” and 800 is “excellent,” your account conduct often tells the more important story. This guide is designed to replace that anxiety with a clear, actionable plan. We’ll explore the specific credit tiers Australian banks use, how to position your finances for a smooth approval, and exactly how to repair your standing if you’re starting from a lower base. By the end of this article, you’ll have the confidence to stop guessing and start moving toward your next big milestone with a reliable guide by your side.

Key Takeaways

- Identify how comprehensive reporting changes the way lenders view your financial health and why your numerical score is only the beginning of the story.

- Clarify exactly what credit score do i need for a home loan in australia by reviewing the 2026 Equifax tiers and industry benchmarks for successful approval.

- Understand the vital importance of “account conduct” and how avoiding overdraws or late fees can sometimes outweigh a high numerical score.

- Implement a proactive six-month financial cleanse to polish your bank statements and correct reporting errors before you submit a formal application.

- Leverage the expertise of a mortgage broker to navigate the unique credit appetites of over 36 lenders, ensuring your application is matched with the right partner.

Understanding Your Credit Score and Why Australian Lenders Care

Your Credit score is more than just a static number; it’s a dynamic reflection of your financial reliability in real-time. If you’re asking what credit score do i need for a home loan in australia, it’s vital to view this number as a living document that breathes with your every transaction. In the 2026 economic environment, lenders don’t just look for a single “pass” mark. They use your score as a window into your long-term habits and current stability. This score is generated by tracking your history with credit cards, utilities, and previous loans, then distilling that data into a figure between 0 and 1,200. Because this information is updated constantly, a score you see today might be different next month. This fluidity is actually good news, as it means you’re never truly stuck with a past mistake.

Lenders care about this number because it helps them quantify risk with precision. A high score suggests you handle debt with care, while a lower score might indicate you’ve faced hurdles in the past. However, your score is just the beginning of the conversation. It sets the stage for a deeper look at your bank statements and lifestyle choices. By maintaining a healthy score, you position yourself as a dependable partner, which is essential when you’re looking to secure significant financing for your future.

The Role of Credit Reporting Bodies in Australia

You might be surprised to find you actually have three different scores at once. Australia relies on three main credit reporting bodies: Equifax, Experian, and illion. Each agency uses its own proprietary algorithm, which explains why your score might fluctuate between different apps. While all three are important, Equifax is often the primary choice for major Australian banks. It’s a smart move to request your free annual credit report from each body to ensure your data is accurate. Understanding what credit score do i need for a home loan in australia starts with knowing exactly what these bureaus are saying about you. Since not every lender reports to every bureau, checking all three gives you a complete, transparent picture of your standing.

How CCR (Comprehensive Credit Reporting) Changed the Game

The shift to Comprehensive Credit Reporting (CCR) has fundamentally changed how lenders evaluate your application. Previously, your report only highlighted “negative” events like defaults or bankruptcies. Now, the system includes “positive” data, such as your history of making on-time repayments. This means that 24 months of clean, consistent account conduct can often outweigh a minor slip-up from years ago. CCR is the system that allows lenders to see both your credit successes and your slips. It provides a more balanced narrative, rewarding you for the responsible habits you practice every day. This transparency helps lenders feel more secure, making it easier for you to pursue major life milestones like First Home Buyer Loans with a sense of calm confidence.

Is There a Minimum Credit Score for a Home Loan in Australia?

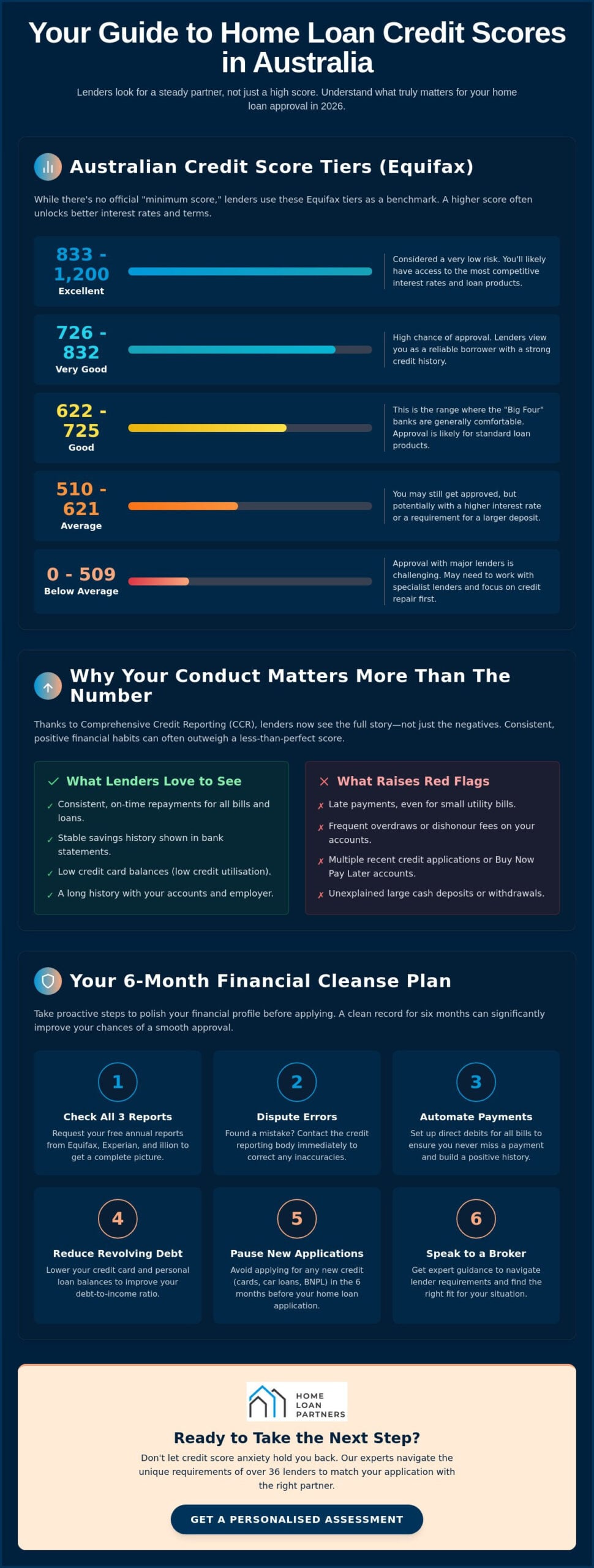

Many Australians look for a single, definitive number that guarantees a mortgage approval. In reality, there is no universal minimum credit score mandated by law or industry regulation. Instead, each lender sets its own internal benchmarks based on its appetite for risk. If you are asking what credit score do i need for a home loan in australia, the answer often depends on the specific loan product you are eyeing. While a score of 500 might be enough for some specialized lenders, the “Big Four” banks typically prefer to see a score in the “Good” range or higher to offer their most competitive products.

A higher score doesn’t just make approval more likely; it directly impacts the cost of your debt. Borrowers in the “Excellent” tier often unlock lower interest rates and higher Loan-to-Value Ratios (LVR). This means you could potentially secure a property with a smaller deposit while paying less interest over the life of the loan. If your score sits in the lower tiers, you might still get a “yes,” but the bank may require a larger deposit or apply a higher interest rate to offset the perceived risk. If you’re unsure where your current standing places you, exploring options for First Home Buyer Loans can provide clarity on which lenders might be the best fit for your specific profile.

Equifax vs. Experian: Deciphering the Tiers

Understanding your position is complicated by the fact that different bureaus use different scales. Equifax, the most common choice for major Australian banks, uses a scale up to 1,200. On this scale, a score of 622 is considered “Good.” However, Experian uses a scale that caps at 1,000, where a 625 might be viewed more favorably. This discrepancy is why a score of 600 might be labeled “Fair” on one report but “Poor” on another. Most experts recommend focusing on your Equifax score first, as it remains the industry standard for the majority of residential mortgage applications in Australia.

The “LMI Threshold”: Why 600 Might Be the Magic Number

The real challenge often isn’t the bank, but the Lenders Mortgage Insurance (LMI) provider. If you have less than a 20% deposit, an LMI provider like Helia must also approve your application. These providers often have stricter score requirements than the banks themselves, frequently looking for a score of at least 600. If your score falls below this threshold, you might find yourself needing a 20% deposit to bypass LMI requirements entirely. For those with scores in the 450 to 500 range, “non-conforming” lenders are an option, though these loans usually come with stricter conditions and higher costs to account for the increased risk.

Why Your Financial Conduct Matters More Than the Numerical Score

It’s a common point of frustration: an applicant presents an “Excellent” score of 900, yet receives a rejection letter. This happens because while your score is a helpful snapshot, it doesn’t tell the whole story of your daily financial habits. When people ask what credit score do i need for a home loan in australia, they often expect a simple pass/fail number. However, your account conduct, the granular detail of how you manage your money every day, is what lenders actually use to verify your reliability. A high score gets you through the door, but your bank statements are what keep you in the room.

Lenders in 2026 now use sophisticated AI tools to scan your last three to six months of bank statements with precision. These systems look for specific red flags that a numerical score might miss, such as frequent overdraws, late payment fees, or excessive gambling activity. Even if you’ve never defaulted on a loan, a pattern of living right at the edge of your means can signal risk to a credit assessor. Banks want to see a calm, predictable financial life where your income comfortably covers your expenses with room to spare. This steady expertise in managing your own cash flow is often the deciding factor in a successful application.

The BNPL Effect: Afterpay, Zip, and Your Mortgage

Buy Now Pay Later (BNPL) services like Afterpay and Zip have changed the assessment process significantly. Even if your balance is zero, lenders often treat the entire account limit as an active debt. A $2,000 limit on a BNPL app can directly reduce your borrowing capacity, as the bank must assume you could spend that money at any time. Frequent small transactions can also suggest a lack of financial discipline to some traditional lenders. For the best results, it’s a wise strategy to close these accounts at least three to six months before you start your application journey to clear your path of any unnecessary hurdles.

Genuine Savings vs. Credit History

A perfect credit history is a great asset, but it can’t replace the need for genuine savings. Most lenders require a deposit of at least 5% to 10% that has been accumulated through consistent saving over time, rather than a one-off gift or a sudden windfall. This proves you have the discipline to manage the ongoing costs of a mortgage. Lenders value the ability to save money as much as the history of paying it back. By demonstrating a steady saving pattern that aligns with your future mortgage repayments, you show that you’re ready for the long-term commitment of home ownership and provide the security the bank is looking for.

Strategic Steps to Improve Your Credit Position Before Applying

Improving your financial standing is a deliberate journey, not an overnight fix. If you’re currently asking what credit score do i need for a home loan in australia, the best time to start preparing is six months before you intend to apply. This window allows you to perform a “financial cleanse” that polishes your bank statements and removes unnecessary obstacles. One of the most effective moves you can make is starting a “credit limit diet.” Even if you don’t owe anything on your credit cards, lenders treat the total limit as a potential debt. Reducing a $10,000 limit to $2,000 can significantly increase your borrowing power because it lowers your perceived risk profile.

Be cautious of “credit repair” companies that promise to wipe your record clean for a high fee. Many of these services charge for actions you can legally perform yourself for free. Instead of paying for a quick fix, focus on steady, verifiable discipline. Our team at The Home Loan Partners can help you review your report for red flags and guide you through the process of applying for First Home Buyer Loans with a clear strategy in place. Taking these proactive steps ensures that when you finally sit down with a lender, your application reflects a calm and controlled financial life.

Correcting Errors and Disputing Defaults

Errors are more common than many buyers realize, and they can unfairly drag down your score. You have a legal right to have incorrect data removed for free by contacting the credit reporting body directly. Check your report for incorrect residential addresses, duplicate listings of the same debt, or defaults that remain marked as “unpaid” despite being settled. Removing just one misplaced default can cause your score to jump significantly, opening doors to better interest rates. It’s a simple process that requires patience but pays massive dividends when it’s time to buy.

The 24-Month “Clean Conduct” Rule

Modern lending focuses heavily on your most recent behavior. While a default from five years ago stays on your record, the last 24 months of history carry about 90% of the weight in a lender’s decision. This is your window of opportunity. Even if you’ve had a rough financial past, you can outrun it with two years of perfect discipline. Automation is your best friend here. By setting up automated repayments for every utility bill and credit account, you eliminate the risk of a single late payment tarnishing your record. This consistency proves to the bank that your past mistakes don’t define your current reliability.

How a Mortgage Broker Navigates Credit Requirements Across 36+ Lenders

Finding the right mortgage is rarely about hitting a single, universal target. It’s about matching your unique financial profile to the right credit policy at the right time. At The Home Loan Partners, we act as your expert guide through a complex maze of over 36 different lenders. If you’re still asking what credit score do i need for a home loan in australia, it’s important to realize that the answer varies wildly depending on which door you knock on. Some institutions prioritize high numerical scores above all else, while others are more interested in the specific context and stability of your application.

Every bank has a different “appetite” for risk that can change based on their current portfolio. A major lender might have a strict internal cutoff that excludes anyone with a minor default from three years ago. Conversely, a smaller, more flexible lender might see your recent history of discipline as a sign of strength. We manage the heavy lifting by filtering through these diverse policies to find the path of least resistance for your specific situation. This collaborative approach ensures we aren’t just looking for a transaction; we’re building a long-term relationship that supports your major life milestones.

Finding the Right Fit: Tier 1 vs. Specialty Lenders

If a Big 4 bank says “no” because of your score, it doesn’t mean your home-buying journey has reached a dead end. We have access to “non-bank” and specialty lenders that don’t have a presence on the local high street. These institutions often specialize in helping borrowers who have slightly lower scores or complex financial backgrounds. While a specialty loan might start with a slightly different structure, we often view this as a temporary stepping stone. Once you’ve established a consistent repayment history, we can work with you on refinancing your loan to a prime rate with a major lender in the future.

Protecting Your Score During the Application Process

One of the biggest risks of “shopping around” on your own is the accidental damage it can do to your credit file. Every time you submit a formal application, the lender performs a “hard enquiry,” which can temporarily lower your score. If you receive multiple rejections in a short period, it creates a pattern that makes future approvals even harder to secure. We protect your standing by performing a single “soft” assessment. This allows us to check your eligibility across our entire panel without leaving a mark on your record. It’s a safer, more strategic way to discover what credit score do i need for a home loan in australia to achieve your specific property goals.

Speak to The Home Loan Partners for a stress-free credit assessment

Take the Next Step Toward Your Property Goals

Securing a mortgage in 2026 is about more than just a digit on a screen. While you now understand what credit score do i need for a home loan in australia to access the most competitive rates, remember that your daily financial discipline and account conduct carry significant weight. Whether you’re a first-home buyer or managing a complex credit history, the right strategy can turn a “no” into a “yes.” You don’t have to navigate this journey alone or risk your score with multiple hard enquiries that could set you back.

We’re here to act as your steady hand and expert collaborator. By partnering with us, you gain access to a panel of over 36 Australian lenders and receive unbiased, professional advice tailored to your long-term security. We specialize in finding the right fit for every situation, providing the expert guidance needed to navigate even the most complex credit environments. It’s time to stop worrying about the benchmarks and start building your future with clarity and confidence.

Book a free consultation with The Home Loan Partners to assess your borrowing power and discover the clear, stress-free path to your next milestone. Your home ownership journey is a significant life event, and we’re committed to staying by your side every step of the way.

Frequently Asked Questions

What is considered a “good” credit score for a home loan in Australia?

When determining what credit score do i need for a home loan in australia, a figure of 700 or above is generally considered “good” by most lenders. A score of 800 or higher is viewed as “excellent,” which often unlocks the most competitive interest rates available. While these numbers are important, they’re only one part of the story. Lenders also examine your income stability and daily spending habits to ensure you’re a safe bet for a long-term loan.

Can I get a home loan with a 500 credit score?

Yes, it’s possible to secure a loan with a 500 credit score, though your options will likely be limited to specialty or “non-conforming” lenders. These loans often come with higher interest rates and may require a deposit of 20% or more to offset the risk. If you’re in this position, focusing on 24 months of clean repayment history can help you eventually refinance to a more traditional lender with a lower interest rate.

How much does one late payment affect my mortgage application?

A single late payment is unlikely to cause an automatic rejection, but it will be visible on your report for 24 months under Comprehensive Credit Reporting. Lenders look for patterns rather than isolated incidents. If you have a strong explanation and subsequent on-time payments, most banks will view it as a minor slip. It’s best to ensure your last six months are completely clear before you start your application journey.

Does checking my own credit score lower it?

No, checking your own credit score is considered a “soft” enquiry and has no impact on your numerical rating. You can check your file as often as you like through platforms like Equifax or Experian without worry. In contrast, “hard” enquiries occur when you formally apply for credit. These are recorded on your file and can lower your score if you make too many applications in a short period of time.

How long does a default stay on my credit report in Australia?

A standard default remains on your credit report for five years from the date it was listed. Even if you pay the debt in full, the default stays on your record, though it will be updated to show as “paid.” This transparency helps lenders see how you handled past financial hurdles. Maintaining perfect account conduct after a default is the best way to prove your current reliability to a potential credit provider.

Will my partner’s bad credit score affect our joint home loan application?

Yes, when you apply for a joint mortgage, lenders assess the credit history of both applicants. A low score from one partner can impact the interest rate offered or even lead to a rejection from some banks. If one partner has a challenging history, it’s often helpful to seek professional advice on which lenders have a higher appetite for complex credit situations before you submit a formal application together.

Can I get a home loan if I have no credit history at all?

Starting with no credit history isn’t a deal-breaker, but it does mean lenders will scrutinize your other financial habits more closely. They’ll look at your rental history, employment longevity, and your ability to build genuine savings over time. If you’re asking what credit score do i need for a home loan in australia with a blank file, the answer lies in proving your reliability through clean bank statements and consistent saving patterns.

How long does it take to improve my credit score for a mortgage?

You can often see a noticeable improvement in your credit score within six to twelve months of consistent, on-time repayments. While some minor errors can be corrected in weeks, building a robust “clean” history typically takes 24 months under the current reporting system. This period of discipline allows you to demonstrate to lenders that you’re a stable and dependable partner for a long-term financial commitment like a home loan.