Last Tuesday, a local couple in Milsons Point spent four hours comparing 35 different lending products only to feel more confused than when they started. It’s a common story in a market where the average Australian now faces over 100 different lenders. When you’re searching for home loans north sydney, the sheer volume of options can make even the most confident buyer fear they’re missing out on a better deal. You deserve a path that feels steady rather than a race that leaves you exhausted.

We know that the mortgage application process often feels like a stressful second job. You want a seamless approval that respects your time and your long-term financial security. This guide shows you how a tailored approach can secure lower interest rates and a loan structure built for your future flexibility. We’ll walk through the essential steps to finding your ideal mortgage partner and explain how to turn the complexity of the Australian market into your greatest financial advantage.

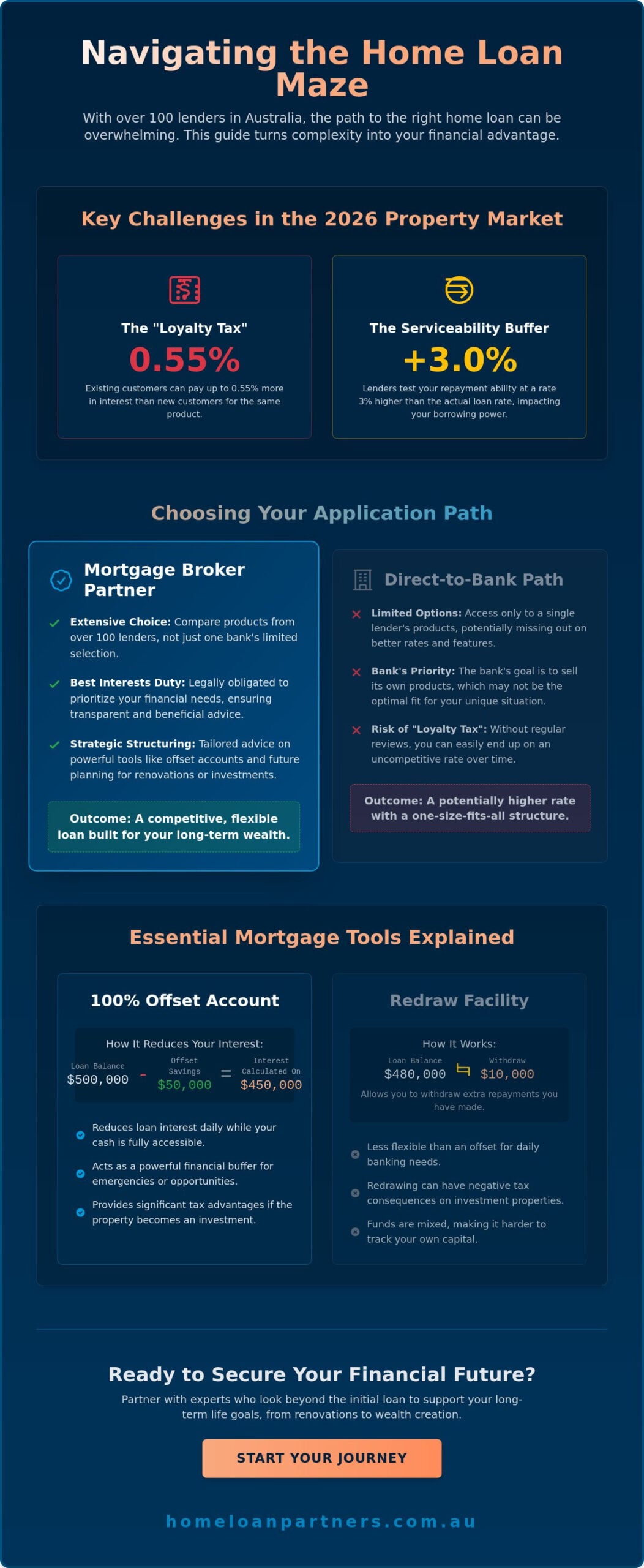

Key Takeaways

- Gain a clear understanding of the 2026 Australian lending landscape and how current interest rate trends influence your strategy in competitive property markets.

- Master the mechanics of essential mortgage tools, such as offset accounts, to effectively reduce interest costs and safeguard your long-term financial security.

- Navigate the complexities of securing home loans north sydney with a tailored approach that aligns your loan structure with specific milestones, from first homes to investment portfolios.

- Learn how the “Best Interests Duty” legally binds brokers to prioritise your needs, ensuring a more transparent and supportive application path than traditional bank-direct routes.

- Discover the value of a professional partnership that looks beyond the initial settlement to help you leverage equity for future renovations or wealth-building opportunities.

Understanding the Market for Home Loans in North Sydney and Nationally

Securing home loans north sydney involves more than just comparing numbers on a screen. The 2026 property market is defined by its speed and complexity. You’ll find that North Sydney properties often attract multiple bidders within days of listing. This pace demands a sophisticated approach to your mortgage. We act as your expert partner to guide you through this finance maze, ensuring you aren’t just another number to a big bank. The Great Australian Dream remains a central pillar of our culture, yet achieving it in a high-demand area like North Sydney requires more than just a deposit. It requires a strategy that anticipates market shifts and bank behavior.

The Reality of the 2026 Property Market

Current lending conditions are shaped by APRA regulations that maintain a 3.0% serviceability buffer. This means banks test your ability to pay at a rate much higher than what’s advertised. Many borrowers don’t realise that staying with their current bank often leads to a “loyalty tax.” Data from early 2026 shows that existing customers often pay up to 0.55% more than new customers for the exact same product. National trends indicate that while some regional areas have cooled, the demand for home loans north sydney remains high due to proximity to the CBD and local infrastructure upgrades completed in 2025. We help you look past the local hype to see how national interest rate trends affect your specific borrowing power.

Defining Your Financial Goals Before You Apply

It’s easy to get caught up in chasing the lowest headline interest rate. While a low rate is helpful, it shouldn’t be your only metric for success. Long-term wealth creation often depends on how your debt is managed over ten or twenty years. We encourage our clients to look at the big picture. This involves several key considerations:

- Flexibility: Can you make extra repayments without penalties?

- Offset Accounts: Are you using your savings to reduce interest charges daily?

- Future Planning: Does this loan allow for equity release if you decide to renovate in 2028?

A tailored loan structure serves as the foundation of your financial security. It’s about finding a balance between your current lifestyle and your future aspirations. We don’t just find you a loan; we partner with you to build a framework that supports your life goals. This proactive approach turns a stressful transaction into a clear, manageable path toward homeownership.

Comparing Home Loan Features: A Roundup of Essential Mortgage Tools

Selecting the right mortgage involves looking well beyond the headline interest rate. For those seeking home loans north sydney, the specific features of a product often dictate long-term savings more than a few basis points ever could. Modern Australian mortgages are highly flexible, but they require a strategic approach to unlock their full potential. When choosing a home loan, you’re essentially building a toolkit for your financial future. Our role is to help you identify which tools will actually move the needle for your specific circumstances.

Offset Accounts vs. Redraw Facilities

An offset account is a transaction account linked directly to your mortgage. The balance in this account is subtracted from your loan principal before interest is calculated each day. An offset account acts as a financial buffer, reducing your interest while keeping your cash accessible. Because the money stays in a separate account, it generally doesn’t trigger the same tax complexities as a redraw facility if you eventually convert the property into an investment. This is a vital distinction for long-term wealth building.

Redraw facilities allow you to withdraw extra repayments you’ve made directly into the loan account. While redraw is often a standard, low-cost feature, it’s less flexible for daily banking than an offset. For borrowers who want to see their monthly interest charges drop while maintaining 100% liquidity for emergencies, the offset is the gold standard. It’s about keeping control of your cash while the bank treats it as a debt reduction.

The Power of Split Loan Structures

Market forecasts for 2026 suggest continued interest rate volatility as the Australian economy navigates shifting inflation targets and global pressures. A split loan allows you to hedge your bets by dividing your debt into two parts. You can fix a portion of your loan, such as 50% or 70%, to lock in repayment certainty and protect your household budget. The remaining portion stays variable, providing access to essential features like an offset account and the ability to make unlimited extra repayments without penalty.

This “best of both worlds” approach is particularly beneficial for:

- First-home buyers who need the security of a fixed monthly cost.

- Refinancers looking to balance debt reduction with a predictable safety net.

- Investors who want to manage cash flow while still having the freedom to pay down the principal.

Loan portability is another crucial feature for the North Sydney market. It allows you to transfer your existing loan balance and terms to a new property when you move. This process can save you between A$600 and A$1,500 in discharge and application fees. It ensures your financial momentum isn’t stalled by administrative hurdles. We specialize in tailoring home loans north sydney to ensure every feature serves your long-term journey toward homeownership.

Strategic Loan Structures for Every Property Milestone

Securing home loans north sydney requires more than just finding a low interest rate. It’s about building a foundation that supports your long-term wealth. Whether you’re stepping into your first apartment in Milsons Point or upgrading to a family home in Cammeray, your loan structure dictates your financial flexibility. As highlighted in a report by The Australia Institute, the home lending market’s profitability often relies on borrowers staying in unsuitable products. We act as your partner to ensure you aren’t one of them.

Refinancers often find that their current loan no longer matches their lifestyle. If you’ve built up equity, you can leverage it to fund a major renovation or secure a deposit for an additional investment. This process involves unlocking the difference between your property’s value and your current debt. For those trying to buy and sell simultaneously, a bridging loan provides the necessary capital to secure a new home before your current one sells. This prevents the stress of finding temporary accommodation in a tight rental market.

Construction and renovation loans require a different level of oversight. Instead of a lump sum, banks release funds in stages as builders hit specific milestones. This protects your capital and ensures you only pay interest on the money you’ve actually spent. We guide you through the paperwork required for these progress payments, making the transition from a blueprint to a finished home feel seamless.

First Home Buyers: Navigating Grants and Guarantees

The 2026 landscape for first home buyers remains focused on accessibility. The First Home Guarantee continues to offer 35,000 places annually, allowing eligible buyers to enter the market with as little as a 5% deposit. If you don’t have a large deposit ready, a Family Guarantee can be a powerful tool. This allows a family member to use their own property equity as security, helping you avoid Lenders Mortgage Insurance (LMI) and saving you thousands of dollars upfront.

To ensure your application is bank-ready, follow this checklist:

- Genuine Savings: Demonstrate consistent savings over a six-month period.

- Stable Employment: Provide your two most recent payslips and a group certificate.

- Clean Credit: Resolve any outstanding debts or utility defaults before applying.

- Budget Clarity: Have a clear breakdown of your monthly living expenses ready for review.

Investment Property Loans and Debt Recycling

Successful investors use debt recycling to accelerate their wealth. This strategy involves using the income from an investment property or surplus cash to pay down non-deductible debt, like your home loan, and then redrawing that money for investment purposes. This effectively converts “bad” debt into tax-deductible “good” debt. Many investors choose interest-only periods for the first five years to maximize cash flow, though this means the principal balance doesn’t decrease during that time. For a deeper dive, read our Investment Property Loans: A Guide for Beginners to see how these structures fit your goals. Choosing the right partner means you’ll always have an expert hand guiding you through these complex financial choices.

Mortgage Brokers vs. Banks: Evaluating Your Application Path

When you’re searching for home loans north sydney, you’ll face a choice between walking into a local bank branch or partnering with a professional mortgage broker. A bank can only offer you the products sitting on their own shelves. This often leads to a “square peg, round hole” situation where you’re forced to fit their rigid criteria. Brokers operate differently. Since January 2021, mortgage brokers in Australia have been legally bound by the Best Interests Duty (BID). This regulation requires brokers to act in your best interests throughout the entire process. Banks don’t share this legal obligation; their primary goal is to sell you their specific products, regardless of whether a better deal exists down the street.

The Advantage of 36+ Lenders

Every lender has a unique “appetite” for different types of borrowers. Some banks prefer high-income professionals in corporate sectors, while others are more comfortable with self-employed applicants or those with smaller deposits. If one bank declines your application, it’s rarely a reflection of your overall creditworthiness; it’s often just a mismatch with that specific bank’s current risk profile. A broker acts as your single point of entry to dozens of banks, saving your credit score from multiple inquiries. According to data from the Mortgage & Finance Association of Australia (MFAA), brokers now facilitate over 71.5% of all new residential mortgages as of the September 2023 quarter. This shift happened because borrowers recognize the value of having an expert scan the entire market to find a tailored fit for their specific financial goals.

The “Lender-Paid” Model Explained

A common misconception is that broker services come with a hidden cost or higher interest rates. In reality, the lender pays the broker for the work they do in preparing and managing the application. This typically involves an upfront commission of 0.60% to 0.70% of the loan amount paid at settlement. Additionally, brokers receive a small “trail commission” of approximately 0.15% per year. This trail payment is vital for you as a borrower. It incentivizes your broker to provide ongoing support and conduct regular rate reviews long after you’ve moved into your home. It ensures you have a partner who’s motivated to help you switch products if your current bank stops being competitive. You can explore more about this relationship by reading Why Use a Mortgage Broker in Australia? to see how transparency builds long-term trust.

Ready to see how the market compares for your next property? Contact our expert team today to explore your options across 36+ lenders.

Why The Home Loan Partners is Your Guide to the Australian Property Market

Choosing a mortgage isn’t just about finding the lowest interest rate available this week. It’s about securing your financial future through a collaborative relationship. At The Home Loan Partners, we’ve moved away from the cold, transactional nature of traditional banking. We prefer a partnership model that prioritizes your peace of mind over simple volume. Our reach extends across Australia, yet our focus remains deeply personal. We understand that securing home loans north sydney requires a nuanced understanding of the local market and the specific lending criteria of over 30 different lenders.

Our philosophy is built on the idea that you deserve a guide, not just a broker. We translate complex bank jargon into plain English so you can make decisions with total confidence. By acting as your intermediary, we ensure the banks compete for your business, rather than you having to plead for theirs. This shift in power is essential in a market where lending standards can change overnight.

A Personalized Path to Settlement

Our team handles the heavy lifting throughout the entire application process. We manage the endless paperwork and the complex back-and-forth with credit assessors that often causes so much stress for buyers. This proactive approach allows you to focus on finding your property while we ensure the financial structure is sound. We don’t just present options; we design a strategy.

Whether that involves maximizing your borrowing capacity or setting up multiple offset accounts to reduce interest, our goal is to find a structure that fits your ten-year plan. We maintain a calm, professional tone even when deadlines are tight. You’ll always know exactly where your application stands because we value clarity above all else. This steady guidance is why so many residents seeking home loans north sydney trust us to manage their most significant financial commitments.

Beyond the Settlement: Your Long-Term Partner

A mortgage is a marathon. Your needs will inevitably change as your life evolves. You might decide to renovate, start a family, or build an investment portfolio in the next few years. We stay by your side long after you’ve picked up the keys. We conduct regular loan health checks to ensure your interest rate remains competitive against current market benchmarks.

If the market shifts or a better product emerges, we’re already on the phone to negotiate on your behalf. Having a partner who understands your long-term goals makes future refinancing or equity releases much faster. We’re committed to your success for the life of your loan, providing a seamless experience that takes the weight off your shoulders.

Secure Your Future in the North Sydney Property Market

Navigating the competitive landscape of the Australian property market requires more than just a low interest rate. It demands a strategic loan structure and a clear understanding of how different mortgage features impact your long-term wealth. Whether you’re a first home buyer, an investor, or looking to refinance, the right mortgage path is built on expert insight and tailored advice that grows with you.

Finding the most suitable home loans north sydney has to offer doesn’t have to be a source of stress. As your trusted guide, The Home Loan Partners provides access to a diverse panel of 36+ major and boutique lenders. We’re legally bound by the Best Interests Duty (BID), which means our recommendations always prioritize your financial well-being. We handle the heavy lifting by comparing thousands of products to find the one that fits your specific needs perfectly.

Your journey toward homeownership or investment success deserves a steady hand and a personal touch. Book a free consultation with The Home Loan Partners today to start your journey with confidence. We’re here to help you turn your property aspirations into a reality.

Frequently Asked Questions

Is it better to get a home loan through a broker or a bank?

Choosing a mortgage broker gives you access to a panel of 30 or more lenders, whereas a bank only offers its own branded products. This variety is essential when searching for home loans north sydney locals can rely on for long-term value. We act as your expert partner to navigate these options, doing the heavy lifting so your experience is seamless and tailored to your goals.

How much deposit do I need for a home loan in 2026?

You generally need a 20% deposit to avoid Lenders Mortgage Insurance (LMI), though many lenders accept 5% or 10% if you’re comfortable with the extra cost. For 2026, government initiatives like the First Home Guarantee continue to support 35,000 buyers annually with deposits as low as 5%. We’ll guide you through these eligibility requirements to help you achieve the Australian dream of homeownership sooner.

What is the current average interest rate for home loans in Australia?

The average variable interest rate for owner-occupiers in Australia currently sits between 6.0% and 7.0%, following the Reserve Bank of Australia’s decision to hold the cash rate at 4.35%. Rates vary based on your loan-to-value ratio and whether you’re an investor or owner-occupier. We monitor these market shifts constantly to ensure your mortgage remains a competitive part of your financial security.

Can I get a home loan if I am self-employed?

You can certainly get a home loan while self-employed by providing two years of tax returns and financial statements to prove your income stability. If your paperwork isn’t fully up to date, “alt-doc” loans allow us to use six months of Business Activity Statements (BAS) instead. We’ll work as your partner to package your application so it meets lender criteria and secures a steady path forward.

How does an offset account actually save me money?

An offset account saves you money by treating your savings as a direct reduction of your loan principal for interest calculations. If you have a A$600,000 mortgage and keep A$60,000 in your offset, the bank only charges interest on A$540,000. It’s a powerful tool that helps you pay off your debt years earlier while keeping your cash accessible for emergencies or future goals.

What is the difference between a fixed and variable interest rate?

Fixed interest rates stay the same for a set period, often one to five years, protecting you from potential market hikes. Variable rates move up or down based on economic conditions, offering more features like unlimited extra repayments and redraw facilities. Many homeowners choose to split their loan, providing a blend of predictable costs and the flexibility needed for a successful long-term journey.

How much can I borrow based on my current salary?

Most lenders calculate your borrowing capacity at roughly four to six times your gross annual salary, though this depends on your specific expenses and debts. For instance, a single applicant earning A$120,000 might be eligible for a loan between A$480,000 and A$720,000. We’ll perform a detailed analysis of your finances to provide a clear, realistic figure that aligns with your lifestyle and aspirations.

What are the hidden costs of buying a home in Australia?

Hidden costs like stamp duty, conveyancing fees, and building reports can add 5% to 7% to your total purchase price. For a A$900,000 home in New South Wales, stamp duty alone costs roughly A$35,000, unless you qualify for first-home buyer exemptions. Factoring in these concrete numbers early ensures your transition into your new home is as stress-free and predictable as possible.