The lowest interest rate on the market could actually be the most expensive mistake you make this year. While a 5.69% variable rate looks enticing on a screen, the true cost of your mortgage is often hidden in the fine print of monthly fees and rigid structures. Learning how to compare home loan offers effectively means looking past the headline numbers to see the full financial picture. It’s completely natural to feel overwhelmed by the sheer volume of choices available in 2026, especially when you’re trying to distinguish between advertised rates and the real-world comparison rates that impact your monthly budget.

We understand that the fear of hidden fees or missing a better deal can make the process feel like a high-stakes gamble. You deserve to feel confident that your loan is working for you, not the other way around. This guide will help you master the art of mortgage selection by focusing on the “Net Benefit” of every offer. We’ll provide a clear checklist to help you evaluate which features, like offset accounts or redraw facilities, are actually worth the cost. By the end, you’ll have a steady strategy to secure a loan structure that prioritizes your long-term security and personal goals.

Key Takeaways

- Learn why the lowest headline interest rate can sometimes be a “rate trap” if it’s paired with high annual fees or restrictive terms.

- Understand how to use the comparison rate as your most powerful tool to reveal the true “all-in” cost of any mortgage offer.

- Discover our strategic 5-step framework for how to compare home loan offers to ensure your choice aligns perfectly with your borrowing power and long-term goals.

- Evaluate the cost-benefit of features like offset accounts and redraw facilities to avoid paying for expensive add-ons you might not need.

- See how a mortgage broker’s legal obligation to act in your best interest provides access to competitive rates and tailored structures beyond public advertisements.

Why Comparing Home Loan Offers is More Than Finding the Lowest Rate

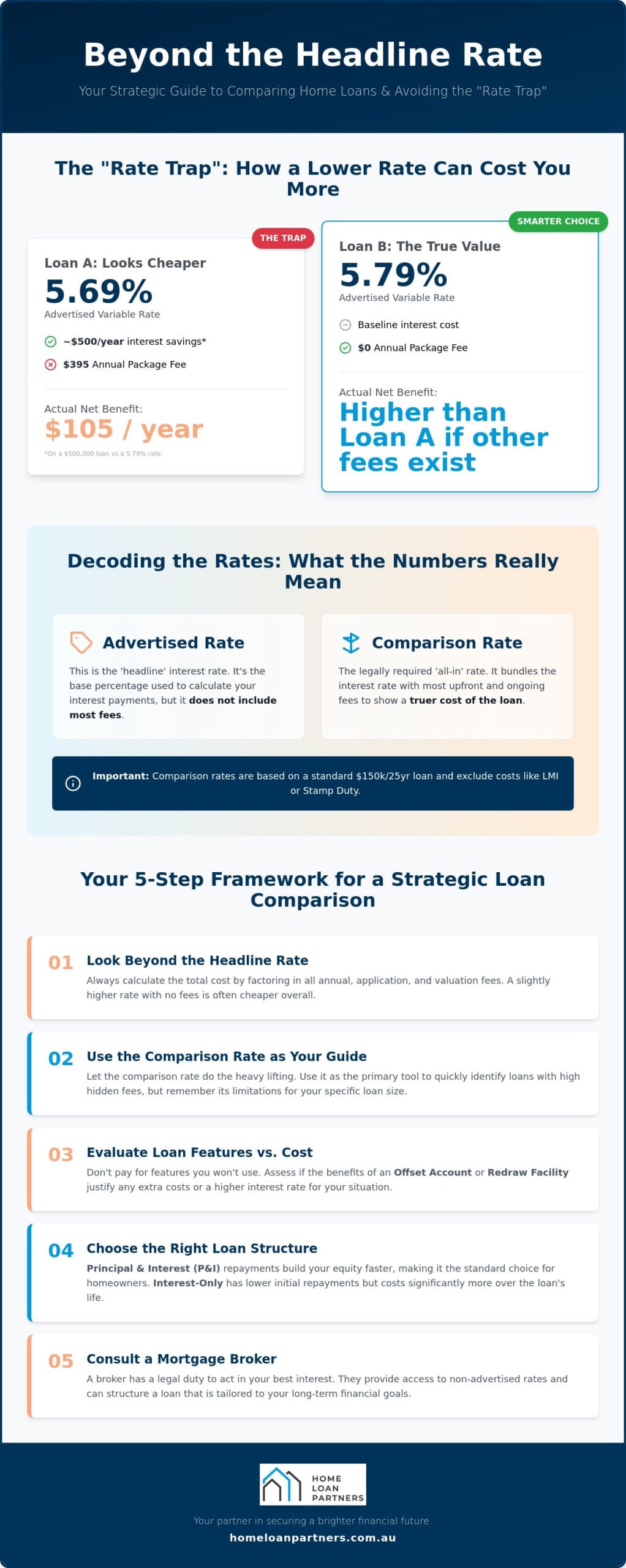

Choosing a home loan is likely the most significant financial commitment you’ll ever make. We understand that the pressure to find the “perfect” deal can feel overwhelming, especially when you’re staring at dozens of competing percentages. However, focusing solely on the lowest interest rate can lead you into a common trap. Mastering how to compare home loan offers requires a shift in perspective; you need to look at the total cost of the loan over its entire lifespan rather than just the headline number on a flyer.

Consider the “Rate Trap” that catches many Australian borrowers. A 0.10% difference in interest rates might seem like a clear win, but if that lower rate comes with a $395 annual package fee, the savings could be completely wiped out. On a typical $500,000 loan, that tiny rate difference saves you about $500 a year in interest, leaving you with a net gain of just $105 after the fee. If the loan also carries higher application or valuation costs, you might actually end up worse off. This is why we distinguish between “Loan Price” (the interest rate) and “Loan Structure” (the features, fees, and flexibility that determine your long-term success).

In 2026, market volatility remains a key factor for Australian households. With the RBA cash rate at 4.35%, the ability to pivot your strategy is often more valuable than a slightly lower fixed rate that locks you in for years. A flexible structure allows you to adapt as your life changes, whether you’re starting a family, renovating, or looking to invest.

The True Cost of Home Ownership Over 30 Years

To truly understand your options, you first need a firm grasp of what is a mortgage loan and how its components interact over decades. Small interest differences compound dramatically. A fraction of a percent can translate into tens of thousands of dollars in extra interest by the time you’ve made your final payment. You should also be wary of “honeymoon rates” that offer a deep discount for the first year, only to revert to a much higher standard variable rate later. In the Australian mortgage market, a loyalty tax is the additional interest paid by existing customers who remain on older, higher-rate products while the lender offers lower rates to attract new business.

Structure Matters: P&I vs Interest-Only

When learning how to compare home loan offers, you must decide between Principal and Interest (P&I) or Interest-Only repayments. P&I loans are the standard choice for most homeowners because they ensure you’re actually paying down the debt each month. Interest-Only offers can lower your immediate out-of-pocket costs, which might be helpful for investors, but they result in significantly higher total interest charges over the life of the loan. To see how these choices impact your specific numbers, you can use our Home Loan Calculator Guide to model different repayment scenarios and find the path that offers the greatest long-term security.

Decoding the Comparison Rate: The Most Important Number

If you’ve spent any time looking at bank websites, you’ve noticed two different percentages listed for every product. While the advertised interest rate gets all the marketing attention, the comparison rate is actually the most powerful tool you have when learning how to compare home loan offers. By law, Australian lenders must display this number prominently to help consumers see the “all-in” cost of a loan. It combines the base interest rate with most of the upfront and ongoing fees, providing a more transparent view of what you’ll actually pay.

The Australian government’s guide to choosing a home loan emphasizes that this rate is designed to level the playing field. However, it’s vital to understand its limitations. A comparison rate is typically calculated based on a loan of $150,000 over a 25-year term. In 2026, where the average Australian property price often requires a much larger mortgage, this standard calculation can be misleading. Fees that represent a large percentage of a $150,000 loan have a much smaller impact on an $800,000 loan, meaning the comparison rate you see in an ad might not reflect your specific reality. It also excludes certain costs like government stamp duty or Lenders Mortgage Insurance (LMI), which can add significant amounts to your initial outlay.

Advertised Rate vs Comparison Rate

The gap between these two numbers tells a story about the loan’s fee structure. If you see an advertised rate of 5.80% and a comparison rate of 6.20%, it’s a clear signal that the loan carries high annual or upfront fees. Conversely, if the two rates are identical or very close, you’re likely looking at a “no-fee” or low-cost product. You should always look for the small warning text that accompanies these rates; it reminds you that the comparison rate is only accurate for the specific example provided. To get a clear picture of how these fees apply to your specific borrowing amount, you might find it helpful to speak with an expert collaborator who can run the numbers for your unique situation.

Fees That Can Break Your Budget

When you’re evaluating how to compare home loan offers, keep a close eye on these common costs that the comparison rate captures:

- Upfront Fees: These include application fees (which can reach $600), property valuation fees, and legal or settlement fees.

- Ongoing Fees: Many “packaged” loans charge an annual fee of up to $500 in exchange for rate discounts or offset accounts. Others may charge a monthly service fee of around $10.

- Exit Fees: While early exit fees on variable loans were abolished years ago, you’ll still face a discharge fee (often around $795) when you eventually pay off or move your loan.

Understanding these costs ensures you aren’t blindsided by the price of “free” features. A higher interest rate with zero fees is often cheaper over the long run than a low-rate loan burdened by expensive annual packages.

Evaluating Loan Features: Are You Paying for What You Use?

Finding the right loan isn’t just about the numbers; it’s about how the loan fits into your daily life and your long-term aspirations. When you’re looking at how to compare home loan offers, you’ll quickly notice a divide between “Basic” loans and “Professional Packages”. Basic loans typically offer the lowest variable rates, often starting around 5.69% for borrowers with a 60% LVR. However, these products are often stripped of the tools that provide financial agility. Professional packages, while offering more features, frequently carry an annual fee of up to $500.

The psychological benefit of having a flexible loan can be significant. Knowing you can access cash in an emergency or save interest with your daily savings provides a sense of calm. But you should always weigh this comfort against the mathematical cost. If a package costs you $395 a year in fees, you need to keep enough cash in your linked accounts to save at least $395 in interest just to break even. This is why our previous discussion, which explains the comparison rate, is so vital. It helps you see if a feature is a genuine benefit or just an expensive add-on that doesn’t align with your spending habits.

Offset Accounts vs Redraw Facilities

Two of the most debated features are offset accounts and redraw facilities. An offset account is a separate transaction account linked to your mortgage. The balance in this account is “offset” against your loan balance, reducing the interest you’re charged. A redraw facility allows you to pull back extra repayments you’ve made directly into the loan. While they sound similar, the tax implications differ significantly. If you eventually turn your home into an investment property, money in an offset account preserves your tax-deductible debt far better than a redraw facility does. For a detailed breakdown of which choice suits your specific strategy, read our guide on Redraw vs Offset Account.

Portability and Split Loans

Life is rarely static, and your loan shouldn’t be either. Loan portability is a feature that allows you to transfer your existing loan from your current property to a new one when you move. This can save you thousands in discharge and application fees. Additionally, many borrowers in 2026 choose split loans. This allows you to fix a portion of your debt for certainty while keeping the rest variable to take advantage of features like offsets. When you learn how to compare home loan offers, always check for repayment flexibility. Some fixed-rate loans limit extra repayments to $10,000 a year or prohibit them entirely. If you plan to pay down your debt faster, a loan that allows unlimited extra repayments without penalty is a feature that truly pays for itself.

The 5-Step Framework for a Strategic Loan Comparison

To move from confusion to confidence, you need a repeatable system. We’ve developed a steady, five-step framework that simplifies how to compare home loan offers by focusing on your specific goals rather than just the lender’s marketing. This structured approach helps you filter out the noise and identify the loan that offers the highest net benefit for your household.

Step 1: Determine your borrowing power. Before looking at rates, use a reliable calculator to understand what lenders are likely to offer based on your current income and expenses. This sets a realistic boundary for your search. Step 2: Decide on your must-have features. Revisit the features we discussed earlier. Do you actually need an offset account to reach your goals, or would a basic loan with a lower rate serve you better? Step 3: Collect at least three Key Facts Sheets. These standardized documents are essential for an accurate comparison. Step 4: Calculate your annual cost. Add the yearly interest to any annual or monthly fees. This reveals your true out-of-pocket expense, which is often different from what the headline rate suggests. Step 5: Review your exit strategy. Life changes quickly. Check the discharge fees and costs associated with refinancing in case you need to move your loan in two or three years.

Using Key Facts Sheets to Your Advantage

Every Australian lender is legally required to provide a Key Facts Sheet on request. This document is your secret weapon for an apples-to-apples comparison. It highlights the “Total Amount to be Repaid” over a 30-year term, which is a powerful reality check. Seeing this total figure in black and white often provides the clarity needed to choose a slightly higher rate with lower fees over a “discount” rate that costs more over the long term. It strips away the marketing jargon and shows you the raw numbers.

The Role of Lenders Mortgage Insurance (LMI)

If your deposit is less than 20%, you’ll likely face Lenders Mortgage Insurance. This one-off cost can change your comparison entirely. Some lenders offer LMI waivers for certain professions, such as medical practitioners or accountants, which can save you thousands of dollars upfront. Always check if the LMI is portable; usually, it isn’t. This means you’d have to pay it again if you refinance with a new lender before you’ve built up enough equity. If the math feels heavy, we’re here to help. You can connect with our team to have an expert collaborator handle the heavy lifting of these calculations for you.

Why a Mortgage Broker is Your Ultimate Comparison Tool

While our five-step framework provides a solid foundation for your research, the sheer complexity of the Australian mortgage market in 2026 can still feel like a heavy lift. This is where a professional guide becomes invaluable. Unlike searching on your own, working with a mortgage broker provides a layer of legal protection known as the Best Interests Duty (BID). This isn’t just a marketing slogan; it’s a legal obligation for brokers to act in your favour. It ensures the advice you receive is tailored to your specific financial situation rather than a bank’s quarterly sales targets.

Brokers act as an intermediary, translating complex industry jargon into practical language you can actually use. They often have access to “broker-only” rates or discretionary discounts that simply aren’t advertised on public comparison websites. Because they manage the heavy lifting of the paperwork and the back-and-forth negotiation with credit assessors, they significantly reduce the emotional weight of the process. Best of all, the lender-paid model means you receive this expert advocacy and a deep dive into how to compare home loan offers without paying an upfront fee to the broker. This makes professional comparison accessible to every borrower, regardless of their budget.

Accessing 36+ Lenders in One Meeting

When you walk into a single bank, you only see their specific products. It’s a narrow view that limits your potential savings. A broker provides a panoramic perspective. With access to a panel of 36+ lenders, we can compare hundreds of options in a single session. This is particularly helpful if you have a unique situation, such as needing bridging loans for a fast move or complex SMSF loans for your retirement strategy. Niche lenders often provide better terms for these specific needs than the big four banks. For a deeper look at these advantages, explore our article on Why Use a Mortgage Broker in Australia?

Personalised Guidance for the Long-Term Journey

Our partnership doesn’t end when you get the keys to your new home. We view settlement as the beginning of a long-term journey together. As market conditions shift and new offers emerge, we continue to track your rate against the rest of the market. If a better structure becomes available that aligns with your evolving life milestones, we’ll reach out to suggest refinancing. This proactive care ensures you never pay a “loyalty tax” or remain on an outdated product. Ready to take the stress out of your property journey? Book a personalised loan comparison with The Home Loan Partners today and let us help you find the security you deserve.

Take Control of Your Property Journey

You now have a strategic roadmap to look past the marketing hype of low headline rates. By using the comparison rate to reveal the true cost of borrowing and selecting features that align with your daily life, you’re ready to make a decision based on data rather than stress. Mastering how to compare home loan offers is about more than a single transaction; it’s about building a foundation for your long-term financial security and achieving those major life milestones with ease.

Our role is to act as your expert collaborator, managing the heavy lifting so you can focus on the excitement of your new home or investment. As NSW-based experts serving borrowers nationally across Australia, we provide access to over 36 Australian lenders to ensure you find the right fit. We’re legally bound by the Best Interests Duty, which means our advice is always tailored to your specific goals and future protection. Compare your options with an expert mortgage broker today and move forward with the confidence of a steady hand by your side. Your future self will thank you for the care you take today.

Frequently Asked Questions

What is the difference between an advertised interest rate and a comparison rate?

The advertised rate is the base interest percentage a lender charges on your loan balance, but it doesn’t tell the whole story. The comparison rate is a more transparent tool that includes the interest rate plus most upfront and ongoing fees. It’s designed to help you see the “true cost” of the loan, though it’s important to remember that it’s calculated on a standard $150,000 loan over 25 years, which may differ from your actual loan amount.

Are online comparison sites 100% accurate for Australian home loans?

Online comparison sites are helpful for a general overview, but they aren’t always 100% accurate for your specific situation. These platforms often use generic data and can’t account for your unique credit history, specific property location, or exact Loan-to-Value Ratio (LVR). Many sites are also commercially supported by the lenders they feature, which means the “top” results might not always be the most competitive options available to you.

Should I always choose the home loan with the lowest comparison rate?

Not necessarily. While a low comparison rate is a strong indicator of value, it doesn’t account for the flexibility or features you might need, such as loan portability or the ability to make unlimited extra repayments. If you’re borrowing a large amount, the impact of the fees included in the comparison rate is diluted, so a loan with a slightly higher comparison rate but better features might actually save you more over time.

Is it worth paying an annual fee for a home loan with an offset account?

It’s worth the cost only if your typical savings balance is high enough to offset the fee. When you’re learning how to compare home loan offers, you should calculate your break-even point. If the interest you save by keeping cash in your offset account exceeds the annual package fee, which is often around $395, then the feature is providing a genuine financial benefit to your household.

How many home loan offers should I compare before making a decision?

We recommend comparing between three and five high-quality offers. This range is usually enough to give you a clear view of the market without causing analysis paralysis. By looking at a mix of major banks and smaller, non-bank lenders, you can see how different fee structures and interest rates impact your monthly budget and long-term interest costs.

Can I negotiate a better interest rate than what is advertised by the bank?

Yes, negotiation is often possible, especially if you have a strong deposit or a stable employment history. Lenders have discretionary margins they can use to attract high-quality borrowers. This is where having a professional guide is beneficial, as they understand which lenders are currently looking to grow their loan books and are more likely to offer a discount below their published rates.

What are the hidden costs I should look for when comparing mortgages?

You should keep a close eye on discharge fees, valuation fees, and legal costs that might not be immediately obvious. While many of these are in the comparison rate, others, like government mortgage registration fees, are not. In 2026, discharge fees can be approximately $795 plus third-party costs, so it’s vital to understand these “exit” expenses if you plan to refinance or sell in a few years.

How does a mortgage broker compare loans differently than a website?

A website uses a basic algorithm to rank loans, but a broker provides a personalised comparison based on your life goals and lender credit policies. Brokers have a deep understanding of which lenders will accept certain property types or complex income structures. Most importantly, a broker is legally bound by the Best Interests Duty, ensuring their recommendation is focused on your security rather than a website’s advertising revenue.