What if you could secure your dream home today without waiting for your current property to sell or spending months in a temporary rental? Many homeowners find themselves stuck in a stressful “chicken and egg” dilemma, fearing they’ll be trapped with two mortgages or lose their perfect property while waiting for a buyer. Understanding what is a bridging loan is the first step toward removing that uncertainty and taking control of your next move. This specialized finance acts as a strategic tool, designed to bridge the gap between your purchase and your sale with precision.

We know the logistics of moving are heavy enough without the added pressure of financial confusion. You’ve likely felt the weight of coordinating settlements or wondered how interest is charged during the bridge. This comprehensive 2026 guide explains exactly how bridging finance works in Australia to provide you with financial certainty. We’ll explore how you can secure up to 75% of a property’s value, the importance of a credible exit strategy, and the steps our expert collaborators take to ensure a seamless transition. By the end, you’ll see how to avoid the cost of temporary accommodation while securing your future with confidence.

Key Takeaways

- Discover exactly what is a bridging loan and how it serves as a supportive tool to help you secure a new home before selling your current one.

- Learn the difference between peak debt and end debt so you can manage your financial commitments with confidence throughout the move.

- Find out how to avoid the stress of temporary rentals and double-moving by staying in your current home until your new one is ready.

- Understand the specific equity requirements and lending limits needed to ensure your application is structured for success.

- See how an expert guide can help you access flexible options across multiple lenders to find the right fit for your family’s goals.

What is a Bridging Loan? Defining the Financial Bridge

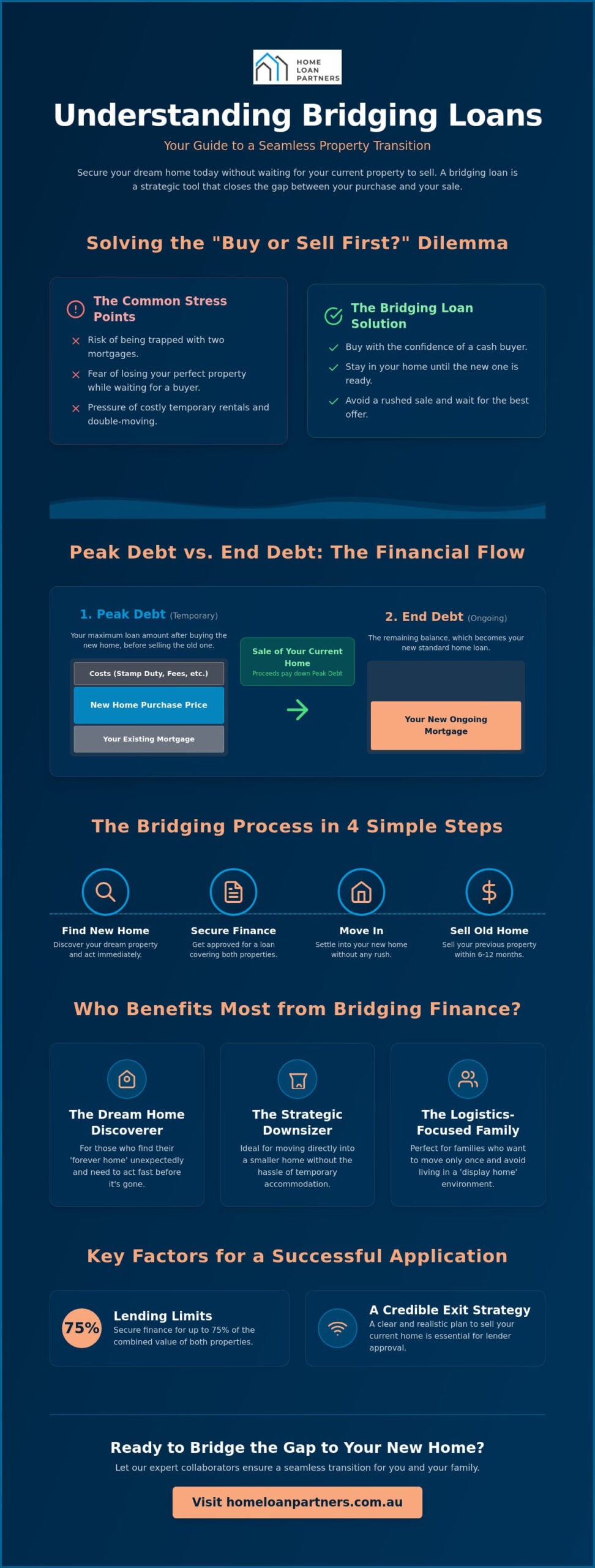

If you’ve found the perfect property but haven’t sold your current one, you’re likely asking, “what is a bridging loan?” At its heart, this is a short-term financing solution designed to help you transition between properties without the pressure of a forced sale. Think of it as a financial “bridge” that connects your current home’s equity to your future residence. In the Australian market, this bridging period typically lasts between 6 and 12 months. This generous timeframe gives you the breathing room to market your old home properly while already living in the new one. It removes the panic of a ticking clock, allowing you to focus on the logistics of moving rather than the fear of missing out on a great deal.

The Core Mechanism: How Bridging Finance Works

During this transition, your lender uses both your current property and your new purchase as security for the total debt. This arrangement is often an add-on to your existing financial structure, meaning you don’t necessarily have to start from scratch with a completely new lender. Essentially, a bridge loan covers the gap between the purchase price of your new home and the eventual proceeds from your sale. It’s a tactical tool for homeowners in a fast-moving market who need to act quickly. By leveraging the equity you’ve already built, you can secure a contract on a new property with the same confidence as a cash buyer. Our role is to ensure this structure remains manageable, providing a steady hand while you navigate two property transactions simultaneously.

Who is Bridging Finance For?

This type of finance isn’t just for high-end investors; it’s a practical choice for many families and individuals looking for a seamless transition. Consider these common scenarios where this tool becomes invaluable:

- The Dream Home Discovery: You stumble upon your forever home before you’ve even thought about listing your current house. Bridging finance lets you pounce on the opportunity immediately.

- The Strategic Downsizer: You want to move directly into a smaller, more manageable home without the stress of finding temporary accommodation or paying for furniture storage.

- The Logistics-Focused Family: Moving is hard enough. Bridging allows you to move once, settle in, and then sell your old place at your own pace without kids and pets living in a “display home” environment.

Choosing this path means you’re prioritizing your family’s comfort and your financial strategy. Instead of rushing a sale and potentially accepting a lower price, you can wait for the right offer, perhaps by using a global platform like HomesGoFast to attract international interest. Understanding what is a bridging loan gives you the power to act when the right opportunity arises, transforming a high-pressure situation into a controlled, logical step toward your long-term goals. We see this as more than just a transaction; it’s about protecting your equity and ensuring your next chapter starts on the right foot.

Understanding the Structure: Peak Debt vs. End Debt

While the initial concept focuses on the transition, the real clarity comes from understanding the underlying numbers. Peak debt represents the highest point of your financial commitment during this period. It combines your existing mortgage, the purchase price of your new home, and associated costs like stamp duty or legal fees. It’s a temporary figure. This is the total amount the lender provides to ensure you can settle on your new property before your old one sells. Once your original home sells, the proceeds are used to pay down this peak debt, leaving you with your “end debt” or ongoing balance. This remaining figure becomes your standard long-term mortgage.

Lenders require a clear “Exit Strategy” before approving any finance of this nature. This isn’t just a formality; it’s a roadmap that ensures you won’t be left in a precarious position if your sale takes longer than expected. Most often, the sale of your current home is the primary exit. However, having a secondary plan, such as refinancing or using other assets, builds a sense of security for both you and the bank. If you’re feeling overwhelmed by these calculations, our team at The Home Loan Partners can help you map out these figures with precision.

Closed vs. Open Bridging Loans

Lenders generally categorise these loans into two types based on your progress. A “closed” bridge is the preferred path for many. This occurs when you already have a signed, unconditional contract of sale for your existing property. Because the exit is guaranteed, lenders view this as lower risk and often offer more competitive terms. Conversely, an “open” bridge applies when your home is on the market but hasn’t sold yet. This requires a much stronger equity position and a solid backup plan, as the lender is taking on more uncertainty regarding the timing and final sale price.

Interest-Only Repayments and Capitalisation

To keep your daily life manageable, most bridging arrangements use interest-only repayments during the bridge. In many cases, you don’t even have to make these payments out of pocket. Instead, the interest is “capitalised,” which means it’s added to your peak debt and settled when your house sells. While this slightly increases your end debt, it prevents the strain of making two mortgage payments at once. When considering Is a Bridging Loan Right for You?, evaluating your cash flow versus your long-term equity goals is key. This managed approach ensures that what is a bridging loan remains a supportive tool rather than a source of stress, allowing you to move into your next home with your finances firmly under control.

The Pros and Cons: Is a Bridging Loan Right for You?

We understand that the primary concern for most homeowners is the cost of interest on a larger debt. While it’s true that your total borrowing increases during the bridge, this expense is often offset by the savings found elsewhere. When you partner with an expert collaborator to structure your finance, you can weigh the interest costs against the very real expenses of double moving, short-term lease breaks, and storage fees. For many, the financial certainty of a single, controlled transition is worth far more than the temporary interest cost.

The Advantages of Staying in Control

One of the most significant benefits of bridging finance is the emotional and logistical freedom it provides. You can avoid the nightmare of moving twice, which means no double removalist fees and no paying for professional cleaning on two different properties in the same month. More importantly, you don’t have to rush the sale of your current home. By staying in control of the timeline, you can wait for the right buyer and the best price rather than accepting a low-ball offer just to settle a debt. This comprehensive guide to bridge loans highlights how this flexibility serves as a safety net for residential buyers.

Risks and Considerations to Discuss with Your Broker

While the benefits are clear, we believe in a transparent approach that acknowledges the risks. The most common concern is what happens if your property doesn’t sell within the typical 12-month window. If the market slows down, you might be forced to lower your asking price to meet the lender’s deadline, which could affect your final end debt. Additionally, interest rates on bridging products can differ from standard mortgages. We work closely with you to ensure your exit strategy is robust and realistic. By evaluating your equity and the local market, we help you decide if what is a bridging loan aligns with your long-term security and lifestyle goals.

Eligibility and Costs: Qualifying for Bridging Finance

Understanding the mechanics of what is a bridging loan is only half the journey. You also need to know if you qualify for this specific type of finance. When lenders evaluate your application, they look for a healthy “equity buffer” in your current home. Most Australian lenders set a Loan-to-Value Ratio (LVR) limit of 80% across both properties. This means the total amount you owe across both homes shouldn’t exceed 80% of their combined value. We help you navigate these limits by providing a clear, steady hand throughout the assessment process, ensuring your application is structured for success.

Standard costs are a part of any property transition, and bridging is no different. You’ll need to prepare for valuation fees for both your current and future homes, as the lender requires an accurate picture of their security. Application fees and legal costs are also typical. A reassuring point for many homeowners is that lenders assess your “servicing” ability based on your end debt, not the peak debt. They want to know you can comfortably afford the mortgage that remains after your sale. This makes the process much more accessible, as you don’t need to prove you can pay two full mortgages simultaneously.

What Lenders Look For in a Bridging Application

Lenders prioritize the viability of your exit strategy above all else. They’ll scrutinize your credit history and current income, but the focus is really on how you’ll pay back the bridge. A realistic property valuation for both homes is the foundation of a strong application. If your current home’s value is overestimated, your exit strategy becomes shaky. We work with you to gather comparable sales data, ensuring the numbers you present to the lender are grounded in current market reality. This collaborative approach builds trust and increases your chances of a smooth approval.

Calculating Your Potential End Debt

To find your end debt, you need to look at your estimated sale price and subtract agent commissions, marketing fees, and your existing mortgage balance. It’s always safer to be conservative with your sale price estimates. If you sell for more, it’s a bonus; if you sell for less, you want to know your end debt is still manageable. You can model these different scenarios using our bridging loan calculator australia to see how the figures align with your goals. If you’re ready to move forward with a plan tailored to your family, contact our team of expert collaborators to discuss your options today.

How a Mortgage Broker Simplifies Your Bridging Journey

Moving houses is one of the most significant milestones you’ll ever experience. While you now understand what is a bridging loan, trying to secure one on your own can feel like an overwhelming addition to your already busy life. A mortgage broker acts as your expert collaborator, managing the heavy lifting of the application process so you can focus on the logistics of your move. We don’t just find a loan; we navigate a panel of 36+ lenders to identify the specific policy that aligns with your family’s goals. This breadth of choice is essential because bridging policies vary wildly across the Australian market. Some lenders are far more flexible than others regarding timelines and equity requirements.

We see ourselves as the steady hand in your transition. Our team takes a proactive approach, distilling complex financial arrangements into clear, manageable steps. By acting as your intermediary, we translate specialized industry jargon into practical language you can trust. This supportive guidance ensures you feel protected and informed from the moment you find your new home until the day your old one sells. We prioritize your understanding and financial security above all else, making the entire process feel predictable and calm.

Access to a Wider Panel of Lenders

Your current bank might seem like the logical place to start, but they can only offer you their own specific bridging products. This limitation can be a hurdle if their criteria don’t match your unique situation. Niche lenders often provide tailored solutions for complex scenarios, such as for self-employed borrowers or those with non-standard income. We compare multiple bridging structures simultaneously, evaluating interest rates and fees across a wide spectrum. This comprehensive search ensures you aren’t just settling for what’s available, but securing a structure that prioritizes your long-term financial health.

Your Partner for the Long-Term Property Journey

Our commitment to your success continues long after the initial settlement. A bridging loan is a tactical, short-term tool, but the mortgage that remains afterward defines your financial future. We stay by your side as you transition from the bridge into a competitive long-term home loan. This focus on longevity ensures your finance remains optimized as your life evolves in your new home. By demystifying what is a bridging loan and managing the transition with precision, we help you achieve your property dreams without the typical stress. Ready to secure your dream home? Speak with The Home Loan Partners today.

Take the Next Step Toward Your New Home with Confidence

Securing your next property doesn’t have to be a source of stress or uncertainty. By understanding exactly what is a bridging loan, you’ve already taken a vital step toward a more seamless transition. You now know how to manage the shift from peak debt to your final mortgage while avoiding the logistical nightmare of temporary rentals. This financial tool empowers you to act quickly in a competitive market, ensuring you never miss out on the perfect home just because your current one hasn’t sold yet. It’s about protecting your equity while prioritizing your family’s comfort.

Our team provides a steady hand throughout this journey. We offer national service with a deeply client-centric approach, giving you access to over 36 Australian lenders to find the most flexible structure for your needs. Whether you’re navigating complex peak debt calculations or seeking a clear exit strategy, we manage the heavy lifting so you don’t have to. Book a free consultation with our bridging finance experts today. We’re here to ensure your next move is a rewarding milestone on your long-term property journey.

Frequently Asked Questions

How long do I have to sell my house with a bridging loan?

In Australia, you typically have between 6 and 12 months to sell your property. This timeframe is designed to give you enough breathing room to find the right buyer and achieve the best possible sale price. If you’ve already signed a contract of sale, the bridging period will usually be shorter to align with your specific settlement dates.

Do I need a deposit for a bridging loan if I have equity?

You often don’t need a cash deposit if you have enough equity in your current property. The lender uses the value of your existing home to secure the new purchase. This allows you to act immediately when you find the right property, removing the need to save a separate cash deposit while your wealth is tied up in bricks and mortar.

Can I get a bridging loan if I have bad credit?

Securing finance with credit issues is more complex, but it’s not always impossible. Mainstream banks prefer a clear credit history, but specialist lenders might consider your application if your equity and exit strategy are strong. We can help you navigate these options, acting as a steady guide to find a lender whose policies align with your specific financial situation.

Is the interest rate higher on a bridging loan than a normal mortgage?

Generally, interest rates are higher than standard mortgage rates because the loan is short-term. When you look at what is a bridging loan, you’ll see it’s a specialized tool designed for speed and flexibility. While the rate is higher, the duration is short, so the total cost is often less than paying for temporary rental accommodation and storage fees.

What happens if my house doesn’t sell within the bridging period?

If your home hasn’t sold by the end of the term, you should speak with your lender about an extension. Lenders generally prefer a successful sale and may grant more time if you show a proactive marketing plan. In some cases, you might need to adjust your price or explore alternative refinancing options to settle the peak debt and move forward.

Can I use a bridging loan for a renovation or construction?

Do I have to make repayments on two loans at the same time?

You usually don’t need to make repayments on two loans at once. Most Australian lenders capitalize the interest, which means they add the monthly interest to your total loan balance. You simply continue with your existing mortgage payments. This arrangement protects your monthly cash flow, ensuring the transition to your new home remains a calm and steady process.

Is bridging finance available for investment properties?

Bridging finance is definitely an option for your investment portfolio. While many homeowners ask what is a bridging loan when moving house, investors use it to snap up new opportunities before selling another property. This strategy keeps your capital working for you and ensures you don’t miss out on a high-growth asset while waiting for a settlement.