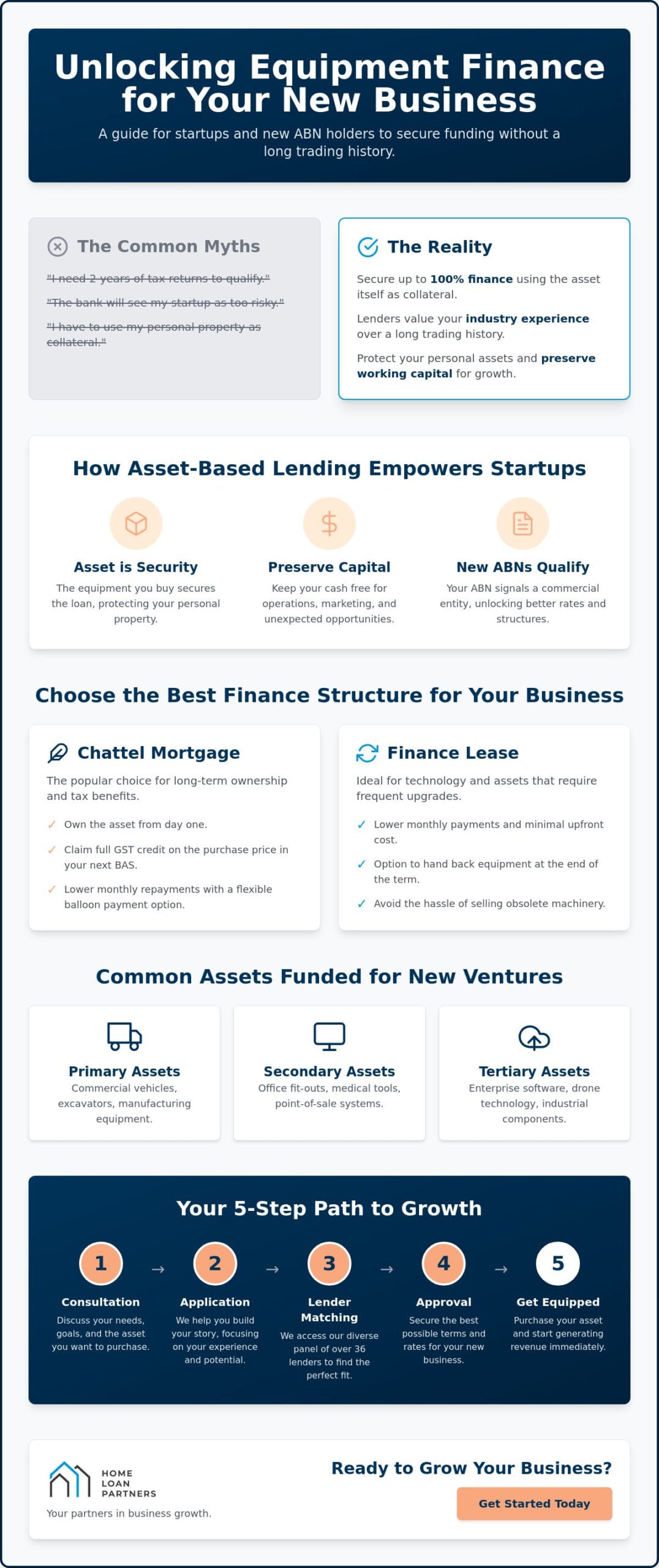

What if your business’s future wasn’t judged by your past tax returns, but by the potential of the tools you’re about to use? Most startup founders believe that without two years of trading history, the doors to major banks are firmly shut. You likely worry that a lack of a balance sheet makes you a high risk, or that you’ll have to risk your personal assets just to get the keys to your first excavator or server rack. It’s a stressful position to be in when you’re ready to grow but feel held back by rigid criteria.

We believe an equipment loan for new business should be a collaborative step forward, not a hurdle. This guide will show you how to secure up to 100% finance by focusing on the quality of the asset and your own industry experience. We’ll explore how to preserve your working capital while leveraging 2026’s tax benefits, such as the $2.56 million Section 179 deduction. You’ll also learn about competitive options like SBA 7(a) loans, which currently offer rates between 7% and 11%; providing a clear and steady path to launching your operations with confidence.

Key Takeaways

- Learn how to secure 100% finance by using the asset itself as collateral, protecting your personal property and business cash reserves.

- Compare the benefits of Chattel Mortgages and Finance Leases to find the structure that best supports your tax strategy and monthly cash flow.

- Discover how an equipment loan for new business is possible for new ABN holders through specialized Low Doc pathways that don’t require years of tax history.

- Master the “story-building” approach to applications, ensuring lenders see the true value of your industry experience rather than just a balance sheet.

- Streamline your path to growth by partnering with a broker who can access a diverse panel of over 36 lenders to find your ideal startup fit.

Understanding Equipment Loans for New Businesses in 2026

Setting up a new venture is a bold step. It shouldn’t require draining your personal savings to get the tools you need. An equipment loan for new business is a specific finance structure where the item you’re buying serves as the security for the debt. This arrangement is a core part of Understanding Asset-Based Lending; it allows the lender to focus on the value of the equipment rather than just your trading history. Unlike a standard business term loan, which might require property as collateral or be used for general expenses, equipment finance is tied directly to the asset’s useful life. It’s a precise way to grow without overextending your personal reach.

Your Australian Business Number (ABN) is your most powerful tool in this process. Even if you’ve only been registered for a few months, your ABN signals to lenders that you’re operating a commercial entity. This opens doors to commercial rates and tax-effective structures that aren’t available to individual consumers. We often see that lenders are more comfortable with these arrangements because the asset itself provides a safety net. If the business pivots, the equipment maintains a resale value that protects both you and the lender.

Why Capital Preservation is Vital for Startups

Common Assets Funded for New Ventures

We see a wide variety of assets funded to help startups get off the ground. The key is that the asset must be used for a predominantly business purpose. Lenders typically categorize these items based on their liquidity and lifespan:

- Primary Assets: These are high-value items with strong resale markets. Think of commercial vehicles, excavators, and manufacturing plant equipment.

- Secondary Assets: These include essential infrastructure like office fit-outs, medical tools, and point-of-sale systems.

- Tertiary Assets: Many lenders now support niche needs. This includes specialized enterprise software, drone technology, and industrial components.

By understanding these categories, we can help you present a stronger case to the right lender. This collaborative approach ensures your equipment loan for new business aligns with your long-term goals and operational needs.

Choosing the Best Finance Structure for Your Business

Selecting the right structure for your equipment loan for new business is just as important as the asset itself. The way you frame your finance affects your tax position, your monthly budget, and how you eventually replace the gear. In 2026, business owners have several distinct paths, each offering different levels of control and financial flexibility. It’s not just about getting the money; it’s about ensuring the debt works in harmony with your operations.

Chattel Mortgage: The Popular Choice

A Chattel Mortgage is often the preferred route for startups looking for long-term ownership. Under this arrangement, your business owns the asset from the moment of purchase, while the lender takes a mortgage over it as security. This structure is highly valued because it typically allows you to claim the full GST credit on the purchase price in your next BAS, providing a significant cash flow injection early on. You also have the flexibility to structure the loan with a balloon payment, which is a final lump sum paid at the end of the term to significantly lower your monthly repayment costs.

Leasing vs. Buying: A Strategic Comparison

While ownership has its perks, it isn’t always the right move for every asset. For tech-heavy businesses or industries where gear becomes obsolete quickly, a Finance Lease might be more suitable. This option offers lower monthly commitments and gives you the “hand back” option at the end of the term, allowing you to upgrade to the latest technology without the hassle of selling old machinery. When comparing these paths, consider these factors:

- Balance Sheet Impact: Buying puts the asset and the liability on your books, while some leases may be treated as an operating expense.

- Upgrade Cycles: Leasing is often superior for assets with a short useful life, such as specialist software or high-end medical tools, which are essential when clinics explore Female Hair Loss Treatment as a new service offering.

- Tax Incentives: In 2026, the Section 179 deduction limit allows for up to $2.56 million on qualifying equipment, which can make immediate ownership very attractive.

For those looking for a middle ground, a Hire Purchase agreement allows you to use the equipment while paying it off in installments, with ownership transferring to you only after the final payment. Some businesses also find value in exploring the SBA 7(a) loan program for machinery purchases, which offers fixed rates and terms that align with the asset’s lifespan. Because every business has unique tax needs, it’s vital to consult with a professional guide who understands how an equipment loan for new business fits into your broader financial journey.

How to Qualify With Limited Trading History

Many entrepreneurs hit a wall when major banks ask for two years of audited tax returns. If your business is only six months old, that’s an impossible standard to meet. However, securing an equipment loan for new business doesn’t always require a mountain of historical paperwork. In 2026, the finance market has shifted toward “story-based” lending. This approach means lenders look at the strength of the asset and your personal professional background rather than just a historical balance sheet. It’s about where your business is going, not just where it has been.

The Power of the “Low Doc” Pathway

Low Documentation (Low Doc) loans are specifically designed for new ABN holders who haven’t yet reached the traditional two-year trading milestone. To qualify for these products, you typically need an active ABN and GST registration. If you’re a property owner, even with an existing mortgage, lenders often view you as a “backed” borrower, which can significantly streamline the approval process. While these loans might carry slightly higher interest rates compared to fully documented ones, they provide the speed and access necessary to start generating revenue immediately. In some cases, high-equity borrowers may even find “No Doc” options where the strength of the collateral carries the entire application.

Leveraging Industry Experience

Your personal history is often the “silent partner” in your startup loan application. If you’ve spent five or more years working in the same industry before starting your own venture, lenders see you as a lower risk. We help you prepare a “Statement of Position” that highlights this expertise, proving you have the technical knowledge to make the business succeed. Your personal credit history also carries significant weight in these early stages. Verified data shows that while many direct lenders accept FICO scores as low as 600, a score of 700 or higher can unlock much more competitive rates and lower down payment requirements.

The type of equipment you choose also dictates how easy it is to qualify. Financing a “primary asset” like a Toyota HiLux or a standard excavator is usually straightforward because these items have high resale value and a liquid market. It’s much easier for a lender to approve an equipment loan for new business when the asset is a common vehicle they can easily sell if the business pivots. If you’re looking for niche or custom-built gear, you might need to provide a larger deposit to offset the lender’s risk. Focusing on high-demand assets early on is a strategic way to build your business’s credit profile during its first year of operation.

Your 5-Step Application Process for 2026

Securing an equipment loan for new business should feel like a partnership, not a series of hurdles. We’ve streamlined the journey into five clear stages to ensure you stay informed and confident throughout. The process begins with a Consultation and Story Building phase. Here, we look beyond the numbers to understand your professional background and the specific role this equipment will play in your success. Next, you’ll move to Asset Selection, where you obtain a formal quote from your chosen supplier. The third stage is the Submission and Assessment, where we present your case to the most suitable lender. Once we secure an Approval, you’ll sign the loan documents. In 2026, this is typically done through secure digital signatures, though physical signing remains an option if you prefer. Finally, Settlement occurs; the lender pays the supplier directly, and you take delivery of your new asset.

Gathering the Right Paperwork

A complete application is a fast application. To keep the momentum, you should have your primary ID, ABN registration details, and at least three months of recent business or personal bank statements ready. The equipment quote is a critical piece of the puzzle. It must be a formal document that includes the total price, the GST amount, and the serial or engine numbers for the specific unit you’re buying. This precision allows the lender to register their interest correctly on the Personal Property Securities Register (PPSR). You’ll also be asked to sign a digital Privacy Consent form, which is a standard step that allows us to securely manage your data as we navigate the lender panel on your behalf.

What to Expect During Credit Assessment

The speed of your approval often depends on the size of the loan. For requests under $250,000, the turnaround is remarkably efficient, with many lenders providing funding within 24 to 72 hours. If you’re looking to finance major plant or machinery between $250,000 and $1 million, the process is slightly more detailed and usually takes 3 to 7 business days. During this assessment, lenders look for consistency and reliability. They’ll review your bank statements for any red flags, such as missed personal loan repayments or high levels of existing consumer debt. A clean financial history combined with your industry experience creates a compelling case for approval. If you’re ready to take the next step without the stress of complex jargon, you can begin your equipment finance journey here with a team that values your growth.

Partnering with The Home Loan Partners for Business Growth

Building a business is a significant life milestone. It requires more than just capital; it needs a strategy that protects your future while fueling your present. When you’re seeking an equipment loan for new business, you don’t just need a lender. You need a partner who understands the nuances of your industry and the specific hurdles of startup life. At The Home Loan Partners, we act as your steady hand, managing the heavy lifting of the application process so you can focus on what you do best: running your business.

Our role is to translate your vision into a compelling case for finance. We don’t just submit paperwork; we build your story. Most major banks have rigid criteria that new businesses rarely meet. By looking at the quality of the asset and your professional background, we find pathways that traditional institutions often overlook. We see our involvement as a long-term journey. Our support doesn’t end when the equipment is delivered; we’re here to help you navigate future growth, whether that involves refinancing or securing your next commercial property.

Unbiased Advice Across 36+ Lenders

Going directly to a single bank limits your options to their specific products and risk appetite. If they say “no,” it can feel like a dead end for your ambitions. We provide a different experience by accessing a panel of over 36 lenders. This includes niche commercial specialists who understand the resale value of heavy machinery and medical gear better than a generalist bank ever could. We compare these options side-by-side to ensure you get a structure that preserves your working capital and aligns with your tax goals.

We work with you, not just for you. This collaborative approach means we explain the logic behind every recommendation. Whether we’re discussing the benefits of a Chattel Mortgage or the flexibility of a Finance Lease, we prioritize your understanding. Because our team understands both mortgage and asset finance, we can ensure your business debt doesn’t negatively impact your personal borrowing power for future home or investment loans. It’s about looking at your entire financial picture with precision and care.

Start Your Business Journey Today

Your initial consultation is entirely stress-free and designed to give you clarity on your options. We take the time to listen to your goals and assess your current position without any high-pressure tactics. As mortgage and finance brokers, we’re paid by the lender you choose, which means there’s no upfront cost for our expert advice and guidance. It’s a risk-free way to explore how the right equipment loan for new business can accelerate your growth. You can speak with The Home Loan Partners about your equipment needs today and take the first step toward a more secure and prosperous business future.

Building Your Business Legacy with Confidence

Your business potential shouldn’t be limited by the age of your ABN. We’ve explored how a strategic equipment loan for new business focuses on the value of the asset and your professional expertise rather than just your historical tax returns. By choosing the right structure, whether it’s a tax-effective Chattel Mortgage or a flexible Finance Lease, you can preserve your vital cash reserves for daily operations. You now have the roadmap to navigate the application process with confidence, moving from asset selection to settlement through a clear, five-step path.

Success in 2026 relies on having a steady hand to guide you through the complex lending market. We provide national support with a personal touch, ensuring you never feel like just another transaction. With access to a panel of over 36 leading Australian lenders and specialized expertise in “Low Doc” finance, we’re here to help you overcome the startup hurdle. You can secure your business equipment with expert guidance from The Home Loan Partners today. We’re ready to join you on this long-term journey and help you achieve your next major milestone.

Frequently Asked Questions

Can I get an equipment loan if my business is less than 6 months old?

Yes, it’s possible to secure an equipment loan for new business even with less than six months of trading history. Many niche lenders focus on your industry experience and the asset’s value rather than the age of your ABN. If you have a clean personal credit history and a solid business plan, we can often find a pathway through specialized startup finance products that don’t require years of tax returns.

What is the minimum deposit required for a new business equipment loan?

Most new businesses can expect a deposit requirement between 10% and 20% for new equipment. However, for well-qualified borrowers with strong industry backgrounds or property ownership, 100% finance is often achievable. The exact amount depends on the asset type and your credit profile. We work with you to structure the loan in a way that minimizes your upfront costs and preserves your operational cash.

Will I need to provide my house as security for a truck or machinery loan?

No, you generally don’t need to use your home as security for a truck or machinery loan. Equipment finance is typically a “self-securing” arrangement where the asset itself serves as the collateral for the debt. This protective structure keeps your personal assets separate from your business obligations. While directors usually provide a personal guarantee, your family home remains detached from the specific equipment mortgage. To understand specialized HGV and truck financing options, read more.

What is a “balloon payment” and how does it help a new business?

A balloon payment is a final lump sum paid at the end of your loan term to lower your monthly repayments. This is particularly helpful for new ventures as it improves your month-to-month cash flow during the critical early growth phases. By deferring a portion of the principal, you keep more capital available for marketing and operations while you’re establishing your brand and building a steady customer base.

Can I buy used equipment from a private seller with a business loan?

Yes, you can buy used gear from a private seller, though the process involves a few extra steps. Lenders will typically require an independent mechanical inspection and a clear PPSR search to ensure there is no existing finance on the item. We manage these details for you, ensuring the private sale is handled professionally and that the funds are transferred securely to the seller once the title is verified.

How do interest rates for new businesses compare to established ones?

Interest rates for new businesses are typically slightly higher than those for established companies to reflect the initial startup risk. While an established business might access the lower end of the 5.5% to 25% APR range, a startup might sit in the middle depending on their credit score. We mitigate this by comparing over 36 lenders to find the most competitive equipment loan for new business rates available for your specific situation.

Does equipment finance offer any tax benefits for a startup?

Yes, equipment finance offers significant tax advantages for startups. You can generally claim the interest component of your repayments and the depreciation of the asset as tax deductions. In 2026, the Section 179 deduction limit allows businesses to deduct up to $2.56 million on qualifying equipment in the year it’s placed in service. This can provide a substantial reduction in your taxable income during your first year of trading.