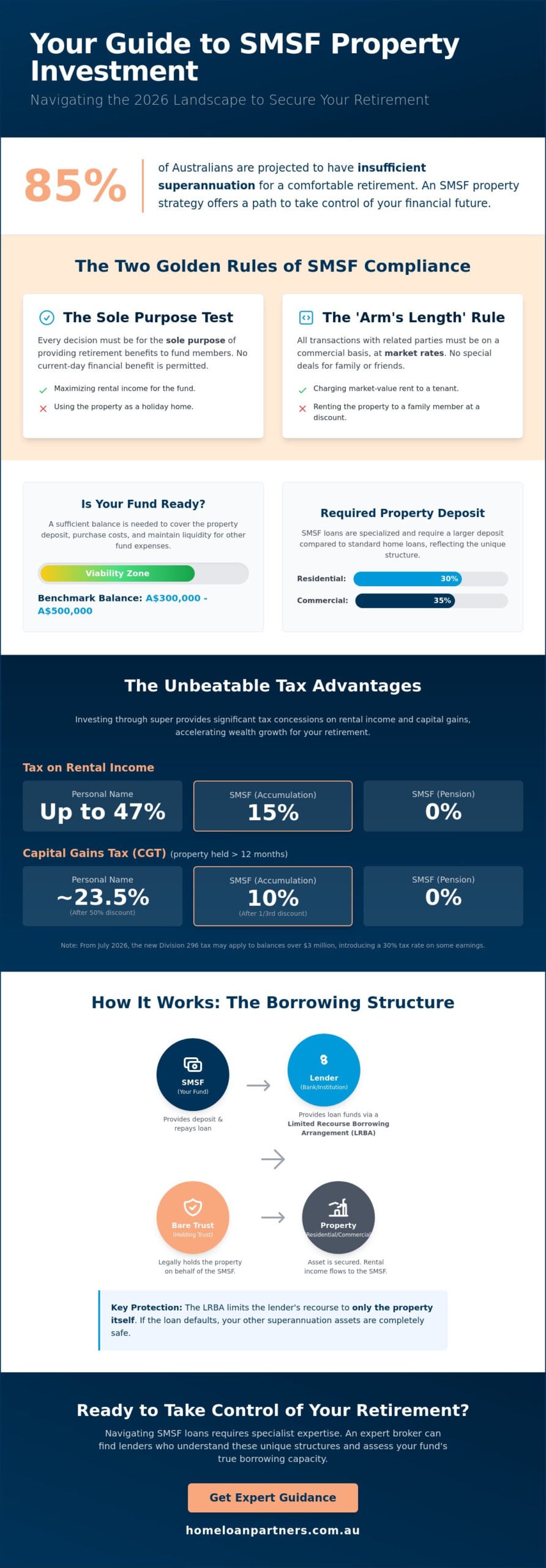

Did you know that more than 85% of Australians are projected to have insufficient superannuation balances for a comfortable retirement? It’s a sobering statistic that often leads to a search for more control over your financial future. You’ve likely felt the weight of complex ATO regulations or worried that high deposit requirements for property are out of reach. It’s completely normal to feel overwhelmed by the Sole Purpose Test or the technicalities of borrowing within a fund.

We’re here to help you understand exactly how to use smsf to buy investment property by breaking down the 2026 landscape into a clear, manageable roadmap. Our goal is to provide a sense of calm expertise as you explore this wealth-building strategy. This guide explores the latest Division 296 tax rules effective from July 2026, explains why a balance of A$300,000 to A$500,000 is often the benchmark for viability, and shows you how to find a lender that understands the unique structure of an SMSF loan. You’ll have a steady hand to help you master the rules, structures, and lending strategies required to secure your retirement through property.

Key Takeaways

- Learn how to navigate the ATO’s strict compliance framework, including the Sole Purpose Test and the essential Arm’s Length Rule.

- Follow our clear roadmap on how to use smsf to buy investment property through a robust corporate trustee structure and a documented investment strategy.

- Balance the long-term tax advantages of superannuation property with the practicalities of setup costs and liquidity requirements.

- Understand the vital role of an expert broker in finding lenders who accept SMSF structures and assessing your fund’s borrowing capacity.

- Discover how to protect your fund’s assets using a bare trust, which is a mandatory requirement for any Limited Recourse Borrowing Arrangement.

Understanding SMSF Property Investment: The 2026 Basics

Many Australians are looking at their retirement savings through a new lens. While traditional industry funds offer a “set and forget” approach, a Self-Managed Super Fund (SMSF) provides a level of control that’s becoming increasingly attractive. In essence, learning how to use smsf to buy investment property involves transforming your superannuation from a list of stocks and bonds into tangible Australian real estate. Whether it’s a residential house or a commercial warehouse, the fund becomes the legal owner of the asset, and all rental income flows directly back into your retirement pot.

The core foundation of this strategy is the Sole Purpose Test. Every decision your fund makes must be for the single purpose of providing retirement benefits to its members. This isn’t just a guideline; it’s a strict regulatory requirement monitored by the ATO. In 2026, investors are turning to property because of the volatility seen in other asset classes. Bricks and mortar provide a sense of security and a physical hedge against inflation. However, you must remember the distinction between types of property. You cannot live in or rent a residential property owned by your SMSF, nor can any of your family members. It’s strictly an investment for your future self.

This structure sits within the broader context of Superannuation in Australia, which is designed to reduce reliance on the age pension. By taking the reins, you’re choosing a path of active management and direct ownership.

What is an SMSF Property Loan?

An SMSF property loan isn’t like a standard residential mortgage you might get for your own home. Because the borrower is a super fund, the lending environment is more specialized and comes with specific protections. A Limited Recourse Borrowing Arrangement (LRBA) is the legal structure used to protect your fund; it ensures that if the fund defaults on the loan, the lender’s rights are limited to the property itself and they cannot touch your other super assets. You’ll generally need a larger deposit than a standard loan. In the current market, lenders typically require at least a 30% deposit for residential properties and around 35% for commercial real estate.

Key Benefits of Investing Through Super

The primary driver for most trustees is the significant tax advantage. While your personal income might be taxed at high marginal rates, rental income within an SMSF is generally taxed at just 15% during the accumulation phase. If you hold the property until you reach the pension phase, that tax rate can drop to 0%. Capital Gains Tax (CGT) benefits are equally compelling. If the fund holds the property for longer than 12 months, the effective CGT rate is only 10% in the accumulation phase. Another powerful feature is the ability to pool super balances. You can have up to six members in one fund, allowing family members or business partners to combine their savings and increase their total buying power.

The Sole Purpose Test and the ‘Arm’s Length’ Rule

Understanding the regulatory boundaries is the first step toward a successful investment. The Australian Taxation Office (ATO) views your superannuation as a sacred vehicle for one specific goal: funding your life after work. This is the essence of the Sole Purpose Test. Every decision, from the initial purchase to ongoing maintenance, must be made to maximize retirement benefits for members. If a transaction provides a present-day benefit to you or a related party, it likely fails this test.

The ‘Arm’s Length’ Rule acts as a safeguard for the fund’s integrity. It dictates that all dealings must be conducted as if the parties were unrelated. There’s no room for personal bias or “mates’ rates” here. Whether you’re setting the rent or hiring a contractor for repairs, the terms must reflect current market conditions. This transparency builds a protective wall around your retirement savings, ensuring the fund isn’t disadvantaged by personal relationships.

A frequent area of concern for those learning how to use smsf to buy investment property is the strict prohibition on residential usage. You, your family members, and your business associates cannot reside in a property owned by your SMSF. This includes using the property as a holiday home, even for a single weekend. The rules are absolute; any personal use is a direct breach of the Sole Purpose Test. Similarly, using fund money for “renovations” that actually serve to upgrade a property for your own future personal enjoyment is a major red flag for auditors.

Navigating these compliance hurdles is much easier when you have a steady hand guiding you. If you’re feeling uncertain about the rules, speaking with an SMSF loan specialist can provide the clarity you need to move forward with confidence.

Severe Penalties for Non-Compliance

The ATO identifies breaches through mandatory annual audits and data-matching programs. If your fund is found to be non-compliant, the financial consequences are significant. Income from transactions not conducted at a market-based rate may be taxed at 45% rather than the usual 15%. In extreme cases, the fund can lose its tax-concessional status or be disqualified entirely. To stay safe, always prioritize independent valuations and ensure every cent of rent paid into the fund matches market expectations.

Commercial Property: The Exception to the Rule

While residential rules are rigid, commercial property offers a unique opportunity for business owners. Under the ‘Business Real Property’ (BRP) exception, your SMSF can purchase a commercial premises and lease it back to your own business. This allows you to pay rent into your own super fund rather than to a third-party landlord. The transaction must still occur at market value, and the business must pay market-rate rent. It’s a sophisticated way to build wealth while supporting your current business operations. For business owners looking at specialized property niches, Homes For Workers offers an example of how dedicated housing can be effectively structured for professional teams.

How to Buy Investment Property with SMSF: Step-by-Step

Moving from the idea of property investment to the actual purchase requires a methodical approach. The process is more technical than a standard home loan, but following a clear sequence helps maintain compliance and reduces stress. Your journey starts with the foundation of the fund itself. You’ll need to establish a Corporate Trustee structure; this is generally preferred over individual trustees because it offers better legal protection and simplifies the process if fund members change later. Once your fund is active, you must ensure your SMSF Investment Strategy explicitly allows for property. This document acts as your fund’s governing logic, and the ATO requires it to be reviewed regularly to justify your asset choices.

Understanding how to use smsf to buy investment property also means preparing for a specialized lending environment. Unlike a standard mortgage, you’ll need to secure a Limited Recourse Borrowing Arrangement (LRBA). This involves obtaining a loan pre-approval through a broker who understands the specific serviceability requirements of a super fund. When you’re ready to make an offer, the property contract must be in the correct legal name. This usually involves the name of the Bare Trustee, not your personal name or even the name of the SMSF itself. Getting this detail wrong can result in double stamp duty or significant legal costs to rectify the title.

The Role of the Bare Trust

A Bare Trust is a mandatory legal requirement for any SMSF that borrows money to buy property. It acts as a legal “firewall” that holds the title of the property on behalf of the super fund until the loan is fully repaid. This structure ensures that the lender only has recourse to the property itself if things go wrong. It protects the rest of your superannuation assets, such as your cash and shares, from being seized by the bank. By keeping the asset separate, you’re fulfilling the legal requirements of the LRBA and ensuring your fund remains compliant with Australian law.

Managing the Settlement Process

Coordinating an SMSF settlement requires close collaboration between your solicitor, accountant, and mortgage broker. It’s a team effort where timing is everything. You must ensure the deposit is paid directly from the SMSF bank account; using personal funds for a deposit can be seen as an illegal contribution or a breach of the arm’s length rule. Be prepared for a longer timeline than a standard residential purchase. SMSF settlements often take 60 to 90 days because of the extra layers of documentation and the need for lenders to review the trust deeds and the Bare Trust setup. Staying patient and organized during this window ensures a smooth transition to property ownership.

Pros, Cons, and Financial Risks of SMSF Property

Deciding to move your retirement savings into real estate is a significant step. It involves weighing the freedom of choice against a higher level of responsibility. The primary draw is tax efficiency. While you’re in the accumulation phase, rental income is taxed at a flat 15%. If you hold the asset until you transition into the pension phase, that tax can drop to zero. You also gain complete control. Instead of a fund manager choosing shares, you pick the exact street, suburb, and property type that fits your vision.

However, this control comes with specific costs. Setting up the necessary trust structures involves upfront legal and accounting fees. Every year, you’ll also pay for an independent audit and an ATO levy to keep the fund compliant. The most significant hurdle for many is limited liquidity. Unlike a portfolio of shares, you can’t sell a single bedroom if the fund needs quick cash for an emergency repair. In the 2026 market, balancing your portfolio with liquid assets like cash or shares is essential for maintaining a healthy, functional fund.

Liquidity and Cash Flow Requirements

Your fund must be able to stand on its own two feet. This means maintaining a liquidity buffer to cover rates, insurance, and unexpected maintenance. If the property sits vacant for three months, the fund still needs to meet loan repayments without struggle. Lenders generally want to see that rental income covers at least 100% to 110% of the interest-only repayments. If the rent stops, you’ll need enough cash reserves in the fund or consistent member contributions to keep the arrangement afloat. Relying solely on rental income is a risk that requires careful planning.

SMSF vs. Individual Property Investment

Understanding how to use smsf to buy investment property requires a direct comparison with personal investing. When you buy property in your own name, negative gearing can offset your high personal tax rate, which is often as high as 47%. Inside an SMSF, those losses only offset a 15% tax rate. This makes the strategy less “tax-effective” for high earners in the short term. Borrowing is also tighter. While you might get a 95% loan personally, SMSF lenders usually cap the loan at 70% or 80% of the property value.

Choosing the right path depends on your long-term vision and current super balance. If you’re ready to explore your options and see if this strategy aligns with your goals, our team of SMSF loan experts can help you compare structures and find a lender that fits your specific needs.

Securing Finance: Why a Mortgage Broker is Essential

Finding a path through the Australian lending market for superannuation investments can be a daunting task. Many of the major traditional banks have scaled back or completely exited the SMSF lending space in recent years, leaving a specialized and often fragmented pool of lenders. This is where a professional broker becomes your most valuable asset. Instead of knocking on doors only to find them closed, you gain access to a curated selection of lenders who specifically understand the nuances of Limited Recourse Borrowing Arrangements. At The Home Loan Partners, we leverage a panel of 36+ lenders to find the specific match for your fund’s unique financial position.

A broker does more than just find a rate. They act as a steady hand, ensuring that your loan structure is perfectly aligned with strict ATO compliance rules. When you are learning how to use smsf to buy investment property, the way the loan is documented is just as important as the interest rate. If the names on the loan documents don’t match the Bare Trust and Corporate Trustee exactly, you risk significant legal hurdles and potential tax penalties. We manage this heavy lifting for you, coordinating with your other professional advisors to ensure the foundation of your investment is rock solid.

One significant advantage of borrowing within your super fund is the impact on your personal finances. Because these are limited recourse loans, they often don’t affect your personal borrowing capacity for a future home loan as heavily as a standard investment mortgage would. This allows you to grow your retirement wealth without necessarily capping your ability to buy a primary residence or a personal investment property elsewhere.

Proving Serviceability to SMSF Lenders

Lenders look at “serviceability” through a different lens when a super fund is the borrower. They aren’t just looking at your personal salary; they are analyzing the fund’s ability to meet repayments through a combination of rental income and ongoing member contributions. Specialized SMSF Loans require proof of consistent employer contributions and a history of “Genuine Savings” within the fund. Most lenders will want to see that the projected rent covers a specific percentage of the loan costs, often between 100% and 110%, to ensure the fund remains liquid and healthy even during vacancy periods.

Your Next Steps in the SMSF Journey

Securing your financial future through property is a collaborative journey that requires a dedicated professional team. You’ll need to work closely with your accountant to manage the annual audits, a financial planner to document your investment strategy, and a specialist broker to navigate the finance. For expert guidance on managing your fund’s specific tax obligations, you can learn more about The Sphere Group. Before you begin, review your current super balance to ensure it sits within the recommended A$300,000 to A$500,000 range for viability. The right loan structure is the foundation of a successful SMSF property strategy, providing the security and growth potential you need for a comfortable retirement.

Take Control of Your Retirement Future

Building a retirement portfolio with Australian real estate is a sophisticated journey that offers unparalleled control over your financial destiny. You now understand the critical importance of the Sole Purpose Test and how a correctly structured Limited Recourse Borrowing Arrangement acts as a protective shield for your other fund assets. By following a clear roadmap and maintaining a healthy liquidity buffer, you can navigate the complexities of the 2026 regulatory environment with confidence. Mastering how to use smsf to buy investment property isn’t a solo task; it requires a partnership with experts who understand the specialized lending landscape.

At The Home Loan Partners, we provide nationwide service and access to a panel of 36+ lenders, including specialist providers who manage complex SMSF loan structures every day. We’re here to handle the technical heavy lifting and provide the steady expertise you need to reach your major life milestones. Book a professional SMSF strategy session with The Home Loan Partners today to begin your journey. Your future security is a long-term project, and we’re ready to guide you every step of the way.

Frequently Asked Questions

Can I live in a house bought through my SMSF?

No, you cannot live in a residential property owned by your fund. This restriction applies to you, your family members, and any related parties. Doing so would fail the Sole Purpose Test, which requires the fund to exist only for retirement benefits. The ATO monitors this strictly, and breaches can lead to the fund being declared non-compliant, resulting in heavy tax penalties or the disqualification of trustees.

How much super do I need to buy an investment property in 2026?

While there’s no legal minimum, a combined balance of A$300,000 to A$500,000 is generally recommended. This range ensures you can cover the 30% deposit, stamp duty, and legal fees while maintaining a cash buffer. Understanding how to use smsf to buy investment property effectively means ensuring the fund remains viable after the purchase. Having sufficient liquidity is vital for managing ongoing costs like repairs, insurance, and audits.

Can my family members rent my SMSF investment property?

No, your family members are prohibited from renting or living in a residential property held by your SMSF. These related party rules are designed to ensure all fund investments are conducted at arm’s length. However, a different rule applies to commercial real estate. If your fund owns a business premises, your own business can lease it at market rates, providing a strategic way to build retirement wealth while supporting your current operations.

What is a Limited Recourse Borrowing Arrangement (LRBA)?

An LRBA is a specific loan structure where the lender’s rights are limited to the property being purchased. If the fund defaults, the bank cannot claim any other assets held within your super, such as cash or shares. This arrangement requires a Bare Trust to hold the legal title until the loan is fully repaid. It’s a mandatory protection under Australian law that keeps the rest of your retirement savings safe from the lender.

Can I use the First Home Super Saver (FHSS) scheme with an SMSF?

No, the FHSS scheme and SMSF property investing serve completely different purposes. The FHSS scheme helps individuals save for a home they intend to live in, whereas an SMSF property must be a strict investment for retirement. You cannot use FHSS funds to buy a property through your SMSF. Each strategy has its own set of rules and compliance requirements that must be managed separately to avoid significant tax issues.

Are interest rates higher for SMSF property loans?

Yes, interest rates for SMSF loans are typically higher than standard residential mortgages. This is because these loans are more complex to set up and carry higher risks for the lender due to the limited recourse nature. Lenders also face higher regulatory and administrative costs when processing these applications. Working with a specialist broker helps you compare the current market and find a competitive rate among the specialized lenders active in this space.

Can I use my super to pay off my existing home loan?

No, you cannot use your superannuation to pay off a personal mortgage while you are in the accumulation phase. Super is preserved for your retirement and cannot be accessed for personal debt reduction before you meet a condition of release. Learning how to use smsf to buy investment property involves keeping your personal finances and your fund’s investments completely separate. Using fund assets for personal benefit is a major compliance breach with severe penalties.

What happens to the SMSF property when I retire?

When you retire and move into the pension phase, the property can remain in the fund to provide a steady income. One of the greatest benefits is that rental income and any future capital gains may become tax-free once the fund is in the pension phase. You might also choose to sell the asset or transfer the title to yourself as an in-specie lump sum payment, provided your fund’s trust deed allows for such a transition.