What if the biggest hurdle to your dream home isn’t the total price tag, but the way you manage your cash flow during the construction phase? Many homeowners worry they’ll have to sell their current property just to start fresh, but learning how to get finance for a knockdown rebuild can unlock a much smoother path. With the average cost to build a new home in Australia sitting at approximately $492,410 as of mid-2026, securing the right funding is about more than just interest rates; it’s about protecting your lifestyle while you build.

We understand that the fear of a lender undervaluing your project or the stress of managing two sets of living costs can feel heavy. This guide is designed to provide you with a clear roadmap to funding your dream home, ensuring you feel supported at every milestone. You’ll gain a firm grasp on the differences between construction and bridging loans, learn how to use your existing equity effectively, and discover a strategy to handle progress payments without the usual headaches. By the end of this article, you’ll have the confidence to manage your borrowing power and move forward with your project.

Key Takeaways

- Understand the fundamental differences between standard mortgages and rebuild structures to ensure your funding aligns with your project’s unique timeline.

- Compare construction loans and bridging finance to choose the most cost-effective path for your living situation while learning how to get finance for a knockdown rebuild.

- Learn how “as-if-complete” valuations allow lenders to assess your borrowing power based on the future value of your finished home rather than just the land.

- Gain clarity on the progress payment schedule so you can manage builder invoices and bank draw-downs with absolute confidence.

- Discover how a mortgage broker simplifies the process by managing complex paperwork and coordinating directly with your builder and lender.

Understanding the Basics of Knockdown Rebuild Finance

A knockdown rebuild is a strategic financial and lifestyle choice that involves demolishing an existing structure to make way for a modern, purpose-built home on the same plot of land. Unlike a standard mortgage where the bank provides a single lump sum to purchase a finished asset, this process requires a specialized structure. Understanding how to get finance for a knockdown rebuild starts with recognizing that your lender is financing a project, not just a property. This creates a unique three-way relationship between you, your chosen builder, and your financial institution, where everyone must remain aligned to ensure the project stays on track.

The core difference lies in how the bank views security. When the old house is demolished, the bank’s collateral is essentially reduced to the value of the land for a short period. To manage this risk, lenders use a valuation based on the “as-if-complete” price of the project. This allows you to access the funds needed for both the demolition and the new construction phases, which usually follow a staged drawdown process rather than a single payment.

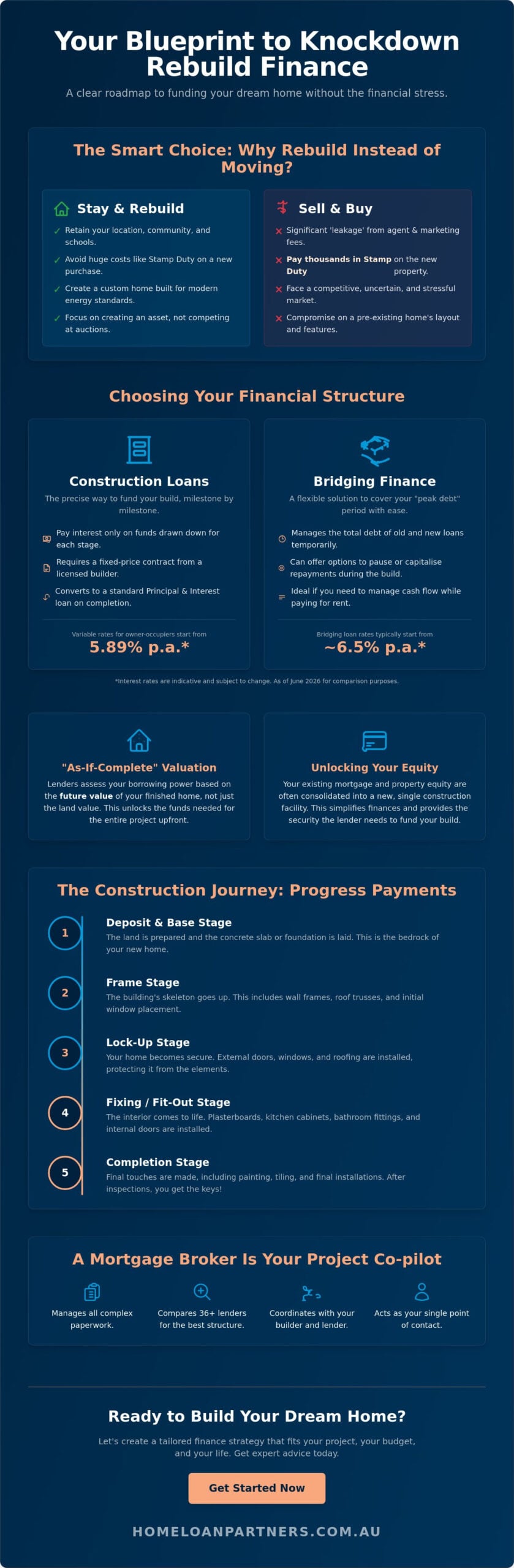

Why Stay and Rebuild vs. Selling and Buying?

Deciding to stay on your current land often makes more financial sense than entering a competitive real estate market. When you sell and buy elsewhere, you face significant “leakage” in the form of agent commissions, marketing fees, and the substantial cost of stamp duty on a new purchase. By rebuilding, you retain your position in an established area while personalizing a home to meet 2026 energy efficiency standards and modern lifestyle needs. You avoid the stress of house hunting and the uncertainty of auction rooms, focusing instead on creating a high-performing asset that reflects your specific taste and future requirements.

The Two-Loan Reality: Existing Mortgage vs. New Build

If you still have an existing mortgage, it doesn’t simply disappear when the walls come down. Most homeowners will transition into a structure that incorporates their current debt with a new construction facility. During the build, lenders typically offer interest-only periods on the drawn-down amount. This is vital for managing your cash flow, especially if you’re paying rent elsewhere while your new home takes shape. While some might consider Bridging Finance to cover the gap between two properties, a dedicated construction loan is often the most direct path for a rebuild. Construction finance is a milestone-based lending facility. This specialized setup ensures that how to get finance for a knockdown rebuild remains a manageable journey rather than an overwhelming financial burden.

Choosing the Right Structure: Construction Loans vs. Bridging Finance

One of the most immediate concerns when planning your project is where your family will sleep while the old house is gone. Your living situation directly dictates how to get finance for a knockdown rebuild. If you plan to rent or stay with relatives, you might prioritize a construction loan with lower interest rates to keep monthly costs down. Variable construction loan rates for owner-occupiers currently start from 5.89% p.a. as of June 2026. However, if you’re juggling multiple financial commitments, bridging finance might be the steady hand you need. Lenders will scrutinize your debt-to-income (DTI) ratio to ensure you can manage the “peak debt” during the build. This is where a mortgage broker becomes an expert collaborator, comparing 36+ lenders to find a structure that fits your specific cash-flow needs.

How Construction Loans Work for Rebuilds

Construction loans are built for precision. Unlike some of the Best Home Improvement Loans, these facilities allow you to pay interest only on the “drawn-down” amount. This means you only pay for what you’ve actually spent at each construction milestone. Before a lender provides approval, they’ll require a fixed-price building contract from a licensed builder. This protects you from unexpected price hikes during the project. Once the final inspection is complete and you move in, the loan typically transitions to a standard principal and interest arrangement. It’s a logical path that keeps your repayments manageable while the site is still a work in progress.

The Power of Bridging Finance

Bridging finance offers a different kind of freedom. It’s particularly useful if you need to cover the peak debt period without the pressure of making immediate monthly repayments on the new build. Bridging loan interest rates currently start from around 6.5% p.a., though they can exceed 10% p.a. depending on your profile. In many cases, the interest is capitalized, meaning it’s added to the loan balance and settled once the project is finalized. You’ll need to determine if you’re an “end-debt” candidate, where you keep a mortgage after the build, or a “standard” candidate who clears the debt through other means. Choosing the right path is a collaborative journey. If you’re feeling overwhelmed by the options, our team can help you find the right loan structure for your future.

Assessing Your Equity and Borrowing Capacity

Determining your financial starting point is often more encouraging than you might expect. Many homeowners assume they need a large cash deposit to begin, but when you’re looking at how to get finance for a knockdown rebuild, your primary asset is already under your feet. Your useable equity is the difference between your property’s current market value (multiplied by 80%) and any debt you still owe. In 2026, with the RBA cash rate sitting at 4.35%, lenders are paying closer attention to your borrowing capacity. This makes it essential to understand exactly how much equity you can leverage before you start the demolition process.

The most critical step in this phase is the “as-if-complete” valuation. Unlike a standard home loan, the bank instructs a valuer to predict the future market value of your property based on your proposed building plans and the current land value. If the total cost of your build plus your existing land value exceeds this predicted market value, you face a “valuation gap.” This is a common hurdle where the bank may not lend the full amount you’ve requested. Managing this gap requires a steady hand and a clear strategy, such as adjusting your build specifications or contributing more equity to keep your project on track.

The Role of Equity as Your Deposit

One of the greatest advantages of a rebuild is that you often don’t need a traditional cash deposit. Your land value serves as the primary security for the construction facility, which can significantly lower your required upfront capital. Lenders will calculate your Loan-to-Value Ratio (LVR) based on the total project cost, which includes the construction contract and any remaining debt on the land. If your LVR remains below 80%, you’ll likely avoid the extra cost of Lenders Mortgage Insurance (LMI), making the journey much more affordable from the outset.

The Valuation Process: Navigating the Risks

Lenders are naturally conservative with “on-completion” valuations because they’re assessing a home that doesn’t exist yet. It’s vital to get this valuation done before you sign a fixed-price building contract. If the valuation comes in lower than expected, you still have the flexibility to work with your builder to reduce costs or choose a different lender who might view the area’s growth potential more favorably. Understanding how to get finance for a knockdown rebuild means being proactive with these numbers. By securing a valuation early, you protect yourself from being locked into a contract you can’t fund, ensuring your path to a new home remains clear and stress-free.

Navigating the Progress Payment Schedule

Managing the financial flow during construction is where your careful planning meets reality. Unlike a standard home loan, your bank doesn’t release the full amount at once. Instead, they use a staged drawdown process to pay your builder as specific milestones are reached. This structure protects you by ensuring that work is completed to a satisfactory standard before funds leave the account. Understanding how to get finance for a knockdown rebuild means being prepared for the paperwork involved in each stage. For every payment, your lender will require a signed claim form and a corresponding invoice from your builder. This collaborative process ensures that your project remains financially secure from the first site scrape to the final coat of paint.

The base and frame stages are the most critical milestones in your journey. These represent the physical foundation and the skeleton of your future home. Because these stages involve significant structural work, lenders often conduct inspections to verify progress before releasing funds. If your builder requests variations or if you’ve included “cost-plus” items like high-end kitchen appliances that weren’t in the original contract, you’ll need to manage these carefully. Most lenders prefer these to be settled using your own savings or contingency funds to avoid disrupting the primary loan balance.

The 6 Stages of Funding Your Build

While every project is unique, most follow a standard six-stage schedule. First is the Deposit and Prep stage, covering your plans, permits, and demolition costs. Next is the Base or Slab stage, where the foundation is poured. This is followed by the Frame stage, giving the house its shape. The Enclosed or Lock-up stage follows, where the roof, windows, and external doors are installed. The Fixing stage covers internal walls, cupboards, and plumbing. Finally, the Completion stage occurs once the Occupation Certificate is issued, triggering the final payment and allowing you to move in.

Managing Delays and Budget Overruns

Construction timelines can shift due to weather or material availability, so it’s wise to build a 10% to 15% contingency buffer into your finance application. This extra room provides a safety net for unexpected costs without requiring a completely new loan application. If your build timeline shifts, maintain open communication with your lender. They appreciate a proactive approach and can help you adjust your interest-only period if the construction phase takes longer than anticipated. Being aware of “prime cost” items is also essential, as these are estimated amounts for finishes that can fluctuate. If you’re ready to map out your specific payment milestones, speak with an expert today to ensure your cash flow remains steady throughout the build.

How a Mortgage Broker Simplifies Your Rebuild Journey

The complexity of a knockdown rebuild means you shouldn’t have to walk this path alone. While you focus on choosing floor plans and finishes, a mortgage broker manages the intricate heavy lifting of your financial application. Access to over 36 lenders is critical because rebuild projects don’t always fit the standard mold of the big banks. We act as your project’s financial advocate, coordinating the constant flow of paperwork between your builder and the lender. By understanding the nuances of how to get finance for a knockdown rebuild, we ensure your application is positioned for success from day one.

Our role is to project a sense of calm expertise throughout the entire process. We bridge the gap between technical industry jargon and your personal goals, translating complex staged-drawdown requirements into clear, manageable steps. This collaborative approach doesn’t just secure a loan; it builds a foundation of trust. We’re here to ensure your borrowing power is maximized and your cash flow is protected, allowing you to enjoy the creative journey of building your dream home.

Expert Guidance vs. Going Direct to a Bank

Walking into a local branch might seem like the easiest route, but many banks have rigid criteria for construction or bridging loans. Some lenders simply don’t offer bridging products, while others have conservative valuation policies that could create a “valuation gap” for your project. A broker identifies the specific lender whose policies align with your goals, whether that’s a higher LVR or more flexible progress payment terms. This unbiased advice is invaluable when you’re comparing complex products that will impact your financial security for years to come.

Your Step-by-Step Roadmap to Approval

Your journey begins with a detailed consultation to assess your equity and borrowing capacity. From there, we help you gather the essential documents, including your fixed-price building contract, council-approved plans, and demolition permits. We handle the submission and follow up with the lender to ensure a smooth approval process. Our relationship doesn’t end when the slab is poured; we stay by your side through every progress payment until the keys are in your hand. We aim to create a long-term loan structure that works just as well after you move in as it did during the construction phase. Reach out to The Home Loan Partners today for a tailored rebuild finance strategy.

Secure Your Future in the Home You’ve Always Imagined

Building a new home on your existing land is a powerful way to upgrade your lifestyle without leaving the community you love. By mastering the balance between construction loans and bridging options, you can protect your cash flow throughout the build. You’ve seen how land equity can act as your deposit and how a structured payment schedule keeps your builder accountable. Understanding how to get finance for a knockdown rebuild is simply the first step in a much larger, more rewarding journey.

At The Home Loan Partners, we act as your steady hand through this complex process. With access to over 36 leading Australian lenders and deep expertise in complex bridging and construction finance, we provide the personalized service you need to navigate every milestone. We’re committed to managing the heavy lifting so you can focus on the excitement of your new build. Our team specializes in creating financial structures that support your long-term security across Australia.

Book a free strategy session with The Home Loan Partners to fund your rebuild today. Let’s work together to turn your vision into a reality with a financial plan that’s as solid as your new home’s foundation.

Frequently Asked Questions

Can I get a construction loan if I still have a mortgage on my current home?

Yes, you can secure a construction loan while holding an existing mortgage. Most lenders will refinance your current debt into a new facility that includes the funds for your build. This allows you to manage one set of repayments while the bank uses your land as security for the new construction stages. It’s a common way to transition into a new home without needing to sell your land first.

What is the difference between a bridging loan and a construction loan for a rebuild?

A construction loan pays your builder in stages and charges interest only on what’s been spent, while a bridging loan covers your total “peak debt” during the transition. Bridging finance is particularly helpful if you need to manage two properties or significant debt without making full repayments immediately. Each option serves a different cash-flow strategy depending on whether you’re renting or staying elsewhere during the project.

How much equity do I need for a knockdown rebuild in Australia?

Most lenders prefer you to have at least 20% useable equity in your land to avoid the additional cost of Lenders Mortgage Insurance. Because your land value acts as your deposit, you often don’t need a cash contribution to start the project. Calculating your equity correctly is a vital part of learning how to get finance for a knockdown rebuild without unnecessary stress.

Do I have to pay interest on the full loan amount from day one?

No, you only pay interest on the funds that have been drawn down to pay the builder at each milestone. If your total loan is $500,000 but you’ve only used $100,000 for the slab and frame stages, your interest is calculated only on that $100,000. This staged approach saves you significant money during the construction phase compared to a traditional lump-sum loan.

What happens if the builder goes bust during my knockdown rebuild?

If your builder becomes insolvent, Domestic Building Insurance (DBI) is designed to protect your project and provide the funds to finish the work. Your lender will pause all progress payments immediately until a new licensed builder is appointed and a new contract is reviewed. This protective measure ensures that no further funds are released until your project is back on track with a reliable partner.

Can I use a first home owner grant for a knockdown rebuild project?

Yes, you can often access First Home Owner Grants for a rebuild if you meet the eligibility criteria and haven’t owned property in Australia before. Each state has different rules, such as the $30,000 grant in Queensland for contracts signed before June 30, 2026, or the $10,000 grant in New South Wales. We’ll help you identify which government schemes and stamp duty concessions apply to your specific situation.

How long does it take to get finance approved for a rebuild?

Approval typically takes between four to six weeks once you provide a complete application to the lender. The timeline often depends on how quickly the “as-if-complete” valuation is finalized and how soon your council provides the necessary permits. Being proactive with your paperwork and having a fixed-price contract ready can help speed up the bank’s decision process significantly.

What documents do I need to provide to the bank for a construction loan?

To secure approval, you’ll need a signed fixed-price building contract, council-approved plans, and your builder’s public liability and warranty insurance details. Lenders also require standard proof of income, recent bank statements, and a detailed breakdown of the demolition costs. Having these documents ready when you’re looking at how to get finance for a knockdown rebuild ensures a much smoother application journey.