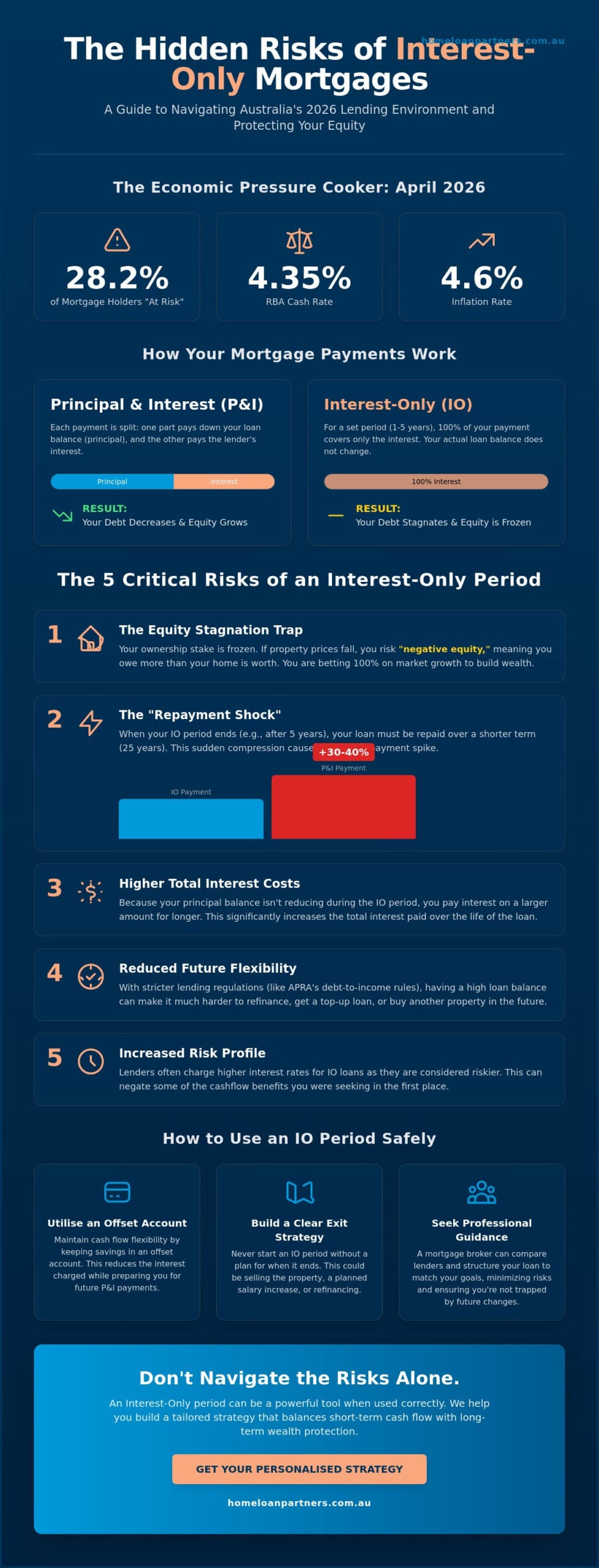

As of April 2026, a staggering 28.2% of Australian mortgage holders are officially classified as “at risk” of mortgage stress. With the RBA cash rate sitting at 4.35% and potentially hitting 4.6% this month, it’s no surprise that many families are looking for ways to lower their monthly outgoings. You’re likely feeling the pressure of 4.6% inflation and looking for a steady hand to help you manage your debt. While switching to a lower payment seems like a logical relief measure, understanding the hidden risks of an interest only mortgage is essential to protecting your long term wealth.

We understand that your home is more than just an asset; it’s your security. We’ll help you identify the strategic dangers of stagnant equity and the financial traps that lead to sudden repayment shock. This guide explores APRA’s latest debt-to-income regulations and provides a clear framework for building a safe exit strategy. Our goal is to ensure you can maximize your investment benefits and maintain your lifestyle without losing the equity you’ve worked so hard to build.

Key Takeaways

- Understand the mechanics of interest-only periods within a standard mortgage and why your principal balance remains static.

- Identify the core risks of an interest only mortgage, including the long-term impact of frozen equity and compounding interest costs.

- Learn how the risk profile shifts between owner-occupiers and investors to ensure your loan structure matches your property goals.

- Discover strategic mitigation tools, such as offset accounts, to maintain cash flow flexibility while preparing for future repayment increases.

- Find out how professional lender comparisons and tailored loan structuring can help you navigate the stricter 2026 lending environment.

What is an Interest-Only Mortgage and Why is it Trending in 2026?

In the current 2026 financial climate, many Australians are looking for ways to breathe. With the official inflation rate hitting 4.6% in March and the RBA cash rate sitting at 4.35%, household budgets are stretched thin. You might be asking, What is an interest-only loan? and how does it fit into a standard 30-year mortgage? Essentially, an interest-only period is a set timeframe where your monthly payments only cover the interest charged on the loan. During this phase, you aren’t actually paying back the money you borrowed. While this lowers your immediate costs, it’s one of the primary risks of an interest only mortgage because your debt doesn’t shrink.

It is also vital to distinguish between an interest-only period and a dedicated interest-only loan product. Most residential borrowers have a standard 30-year loan with a temporary “IO phase,” while specific investment or SMSF loans might be structured with different terms. Understanding which path you’re on is the first step in managing your future security and avoiding a nasty surprise when the bill eventually changes.

The Mechanics of Interest-Only vs. Principal and Interest

In a standard principal and interest loan, your payment is split. One part pays the bank’s interest, while the other reduces the actual loan balance. With an interest-only arrangement, 100% of your payment goes toward the interest. None of it goes toward your equity. Most Australian lenders offer these periods for a duration of one to five years. An interest-only period is a temporary deferment of debt reduction that prioritizes immediate cash flow over long-term ownership. It means your ownership stake in the property remains frozen while the clock keeps ticking on your total loan term. Once the period ends, your payments will jump significantly because you’ll have less time to pay off the same amount of debt.

Why Borrowers are Flocking to IO Periods Right Now

Many of our clients are choosing this path to manage specific life transitions. With 28.2% of mortgage holders considered “at risk” of stress as of April 2026, the lower monthly commitment provides a vital safety net. We often see this strategy used for:

- Managing Life Changes: Providing relief during parental leave or a temporary career change when income might dip.

- Tax Efficiency: Property investors use these periods to keep non-deductible debt high, maximizing tax benefits through negative gearing.

- Market Bridging: Some buyers use it as a short-term strategy while waiting for property values to grow, intending to sell or refinance later.

While these reasons are valid, they must be balanced against the long-term risks of an interest only mortgage. Without a clear exit strategy, what feels like a relief today can become a significant financial hurdle tomorrow.

The 5 Critical Risks of an Interest-Only Mortgage

Choosing an interest-only period can feel like a temporary relief for your monthly budget, but it’s vital to look at the long-term journey. The primary risks of an interest only mortgage often hide in the fine print of your future. While your current payments are lower, you’re essentially standing still while the rest of the market moves. You’re paying for the right to live in the house without actually buying any more of it. This lack of progress can leave you vulnerable if your life circumstances change unexpectedly.

The Equity Stagnation Trap

Equity is your financial safety net. When you opt for an interest-only arrangement, your ownership stake is frozen at the level of your original deposit. If property prices in your area flatline or experience a slight dip, you could find yourself in a position of “negative equity.” This means you owe the bank more than the home is worth. This situation is particularly dangerous if you need to sell or move for work, as you’d have to pay the bank the difference out of your own pocket. Without principal repayments, you’re betting entirely on market growth to build your wealth rather than taking active steps to own your home.

The “Repayment Shock” at the End of the Term

The most significant hurdle many Australians face is the “repayment shock” when the interest-only period expires. Imagine your five-year IO term ends. Suddenly, you must start paying back the principal, but instead of having 30 years to do it, you only have 25. This compression often results in a 30% to 40% jump in your monthly commitment. Many households struggle with this transition because they’ve adjusted their lifestyle and spending habits to the lower payments. According to ASIC’s guide to interest-only loans, this shift can be a major source of financial stress if not planned for years in advance.

Beyond the payment jump, you also face higher variable rate exposure. Because your loan balance isn’t shrinking, every RBA rate hike hits your entire debt. In 2026, with rates at 4.35% and potential increases on the horizon, this compounding cost adds up quickly. You end up paying significantly more interest over the life of the loan compared to a standard principal and interest structure. This extra cost can delay your retirement or other major life milestones by years.

Lastly, don’t overlook the difficulty of switching paths later. APRA’s 2026 debt-to-income limits mean lenders are more restrictive than ever. If your income has changed or your debt has grown, you might find you no longer pass the “serviceability test” required to extend your IO period or move to a different lender. If you’re feeling uncertain about your current structure, exploring your options for refinancing with a professional can help you find a more sustainable path forward. Understanding these risks of an interest only mortgage is the first step in protecting your family’s future security.

Risk Analysis: Investors vs. Owner-Occupiers

The primary difference between a savvy financial move and a dangerous trap often depends on your long-term goal. While the mechanics of the loan stay the same, the risks of an interest only mortgage shift significantly depending on whether you’re an investor or an owner-occupier. For those living in their property, every month spent on an interest-only plan is a month you aren’t actually getting closer to owning your home. This can push your “mortgage-free” date deep into your retirement years, creating a heavy burden when your income might be lower. We always encourage our clients to visualize their life at 65; if you’re still paying off a principal balance then, your lifestyle could be compromised.

Investors, however, often use these loans as a surgical tool. In the 2026 market, where APRA has capped high debt-to-income (DTI) lending at six times income for 20% of new loans, investors must be more precise with their structures. By choosing an interest-only period, an investor can keep their non-deductible debt (the loan on their own home) as the priority for repayment, while maintaining the tax-deductible debt on their investment property. This is a common strategy, but it still requires a rock-solid exit plan to avoid the “repayment shock” we discussed earlier. Without that plan, even the best tax benefits won’t save you from a cash flow crisis when the interest-only term ends.

When Interest-Only is a Calculated Strategic Move

When used correctly, this structure can help you build wealth faster. Debt recycling is a popular technique where you use the cash flow saved from interest-only payments to pay down a non-deductible home loan, then redraw those funds for further investment. This effectively converts “bad” debt into “good,” tax-deductible debt. You might also use this path if you’re undertaking a renovation. By lowering your commitments during the construction phase, you can preserve cash for the build, which ideally adds immediate value to the property. As Moneysmart’s guide to interest-only loans suggests, these strategies only work if you have a clear timeline and a disciplined approach to the “saved” money.

When Interest-Only is a Red Flag for Your Finances

The most dangerous reason to choose this path is because you simply can’t afford the principal and interest repayments. If your budget only balances when you’re ignoring the principal, you’re in a precarious position. This is a significant red flag, especially with the 2026 cash rate potentially rising to 4.6%. Without a secondary savings plan or an offset strategy, you’re effectively gambling on property prices rising fast enough to cover your lack of equity growth. Interest-only should never be a permanent solution for home ownership; it’s a temporary bridge, not a destination. If you find yourself leaning on this structure just to get by, it’s time to review your overall strategy to ensure your risks of an interest only mortgage don’t outweigh the benefits.

Risk Mitigation: How to Use IO Without Losing Your Wealth

Managing your mortgage shouldn’t be a source of constant anxiety. While we’ve explored the potential downsides, it’s possible to use these periods as a strategic tool if you have the right safeguards in place. The key is to be proactive rather than reactive. By building a robust framework around your loan, you can enjoy the lower commitments today without falling into a trap tomorrow. This involves more than just keeping an eye on the calendar; it requires a disciplined approach to your cash flow and regular check-ins with your financial partners. We’re here to act as your steady hand, ensuring your strategy remains aligned with your long-term security.

Using Offset Accounts as a Risk Buffer

An offset account is perhaps the most powerful tool in your arsenal. It acts like a standard savings account linked to your loan, where every dollar you keep in there reduces the interest you pay. This creates a “best of both worlds” scenario. You maintain the flexibility of an interest-only payment while effectively reducing the interest as if you were making principal repayments. We often suggest our clients simulate a principal and interest (P&I) payment by putting the difference between the two amounts directly into their offset account. This builds a “Repayment Buffer” that you can access if an emergency arises, while simultaneously lowering your total interest bill. For a deeper look at how this works, you can read our guide on Redraw vs Offset Account.

The 12-Month Countdown: Planning the Transition

The biggest mistake we see is borrowers waiting until the month their interest-only period ends to think about their next move. To avoid the repayment shock mentioned earlier, you should start your exit strategy at least 12 months in advance. This gives you time to review your serviceability under the 2026 APRA guidelines, which currently restrict high debt-to-income lending. If your income or expenses have changed, you need this lead time to adjust your budget or explore options for refinancing to a more competitive P&I rate before the jump occurs.

A 12-month window also allows for a gradual lifestyle adjustment. Instead of a sudden 40% jump in your monthly costs, you can start increasing your voluntary offset contributions slowly. This mental and financial preparation ensures that when the transition finally happens, it’s a non-event for your household budget. Regular equity check-ins with your mortgage broker are essential during this time. We can help you track your property’s value and ensure you have enough of a safety net to negotiate the best possible terms for the next stage of your home ownership journey. Understanding and managing the risks of an interest only mortgage is much easier when you have a professional partner guiding the way. If you’re approaching the end of your term, speak with an expert today to secure your path forward.

How a Mortgage Broker Minimises Your Interest-Only Risks

Choosing the right loan structure shouldn’t feel like a gamble. When you work with a professional broker, you gain a dedicated collaborator who looks beyond the immediate monthly payment. Our role is to identify the potential risks of an interest only mortgage before they impact your financial security. We don’t just look at what you can afford today; we map out how your loan fits into your 10-year wealth plan. This foresight is vital because a structure that works now might become a hurdle if your family grows or your career path shifts. We take the heavy lifting off your shoulders by analyzing the fine print that often contains hidden traps.

One of the most significant benefits of our partnership is the “Panel Advantage.” Instead of being limited to the handful of products offered by a single bank, we compare policies across more than 36 Australian lenders. This is crucial because every lender has a different appetite for interest-only terms. Some may offer more competitive rates, while others provide greater flexibility for those looking to manage their debt-to-income ratios under the 2026 APRA guidelines. Having this breadth of choice allows us to find a solution that prioritizes your safety and long-term goals.

Our advice is always unbiased and focused on your best interests. Sometimes, the most valuable part of our relationship is when we advise against an interest-only structure. If the numbers suggest that the lack of equity growth will hinder your future plans, we’ll tell you. We’re here to ensure you don’t just get a loan, but that you get the right loan for your specific journey.

Accessing Specialist Lenders and Better IO Terms

It’s a common misconception that the big banks always offer the best deals. In reality, major institutions often charge higher interest rates for interest-only periods to discourage what they perceive as higher-risk lending. We specialize in finding lenders with more flexible “IO extension” policies, which can be a lifesaver if you need more time before transitioning to principal and interest. This is particularly relevant for those managing Investment Property Loans, where tax efficiency is a primary goal. By looking outside the standard options, we can often secure terms that provide the cash flow you need without the excessive costs that eat into your returns.

Creating a Stress-Free Path Forward

We believe that with the right structure and a clear exit strategy, an interest-only period can be a safe and effective financial tool. Our approach at The Home Loan Partners is built on partnership rather than simple transactions. We stay with you for the long haul, helping you manage the eventual switch to principal and interest so you aren’t caught off guard by repayment shock. We provide ongoing support, checking in regularly to ensure your strategy still fits the 2026 economic environment. We’re here to act as your steady hand, navigating the complexities of the market with precision and care. If you’re ready to build a mortgage strategy that protects your equity and your future, Book a strategy session with The Home Loan Partners today.

Securing Your Financial Path in a Shifting Market

Navigating the 2026 property market requires more than just looking at your next monthly statement. While lower payments offer temporary breathing room, actively managing the risks of an interest only mortgage is the only way to ensure you don’t compromise your equity or long-term retirement goals. By utilizing strategic tools like offset accounts and preparing for the inevitable transition to principal and interest at least 12 months in advance, you can maintain total control over your financial journey.

You don’t have to manage these complex decisions alone. Our NSW-based specialists provide expert guidance and access to more than 36 lenders across Australia to help you find the most protective structure for your needs. Because we offer a lender-paid service for standard home loans, you can access professional expertise without worrying about direct broker fees. We’re here to act as your steady hand and long-term partner, ensuring your home remains your greatest asset rather than a source of stress.

Secure your financial future; get an expert review of your loan structure today. We look forward to helping you achieve your next major life milestone with confidence and precision.

Frequently Asked Questions

Is it harder to get an interest-only mortgage in 2026?

Yes, it is generally more difficult to secure an interest-only period in 2026. APRA’s recent debt-to-income restrictions mean lenders are scrutinizing applications more heavily, especially for investors. You’ll need to demonstrate strong serviceability and provide a clear, strategic reason for the request. We can help you navigate these stricter standards by comparing policies across our panel of 36+ lenders to find a suitable match for your profile.

Can I switch from interest-only to principal and interest early?

Most lenders allow you to switch to principal and interest repayments before your interest-only term expires. This is often a smart move if your income increases or you want to start building equity sooner. It’s usually a straightforward process, but you should check if there are any administrative fees involved. Making this switch early can significantly reduce the long-term risks of an interest only mortgage by shortening the time your debt remains static.

Do interest-only loans have higher interest rates?

Interest-only loans typically attract higher interest rates than standard principal and interest loans. Lenders view these arrangements as higher risk because the principal balance isn’t being reduced. In the current market, you might see a difference of 0.2% to 0.5% between the two types. While the monthly payment is lower, the higher rate means you’re paying more for the same amount of debt over the life of the loan.

What happens if I can’t afford the repayments when my interest-only period ends?

If you’re concerned about the jump in payments, you should contact us at least 12 months before your term ends. We can look at refinancing your loan to a lower rate or extending the loan term to reduce the monthly burden. If you’re in immediate financial difficulty, lenders have hardship teams that can provide temporary relief. Proactive planning is the best way to avoid the stress of a sudden repayment shock.

Can I extend my interest-only period indefinitely?

No, you cannot extend an interest-only period indefinitely. Most Australian lenders cap these periods at five years for owner-occupiers and up to ten years for investors. Every time you request an extension, you’ll need to go through a full credit assessment. Because the remaining loan term gets shorter with each extension, your eventual principal and interest payments will become much higher, which can lead to a rejection of the request.

Does an interest-only mortgage affect my credit score?

Simply having an interest-only mortgage doesn’t negatively impact your credit score. Your score is primarily affected by your payment history and how consistently you meet your obligations. However, if the higher repayments at the end of the term lead to missed payments, your credit file will be impacted. Some lenders may also view a long history of interest-only debt as a sign of lower financial resilience during future loan applications.

Is interest-only better for tax purposes if I am an investor?

Many investors find interest-only periods beneficial for tax purposes because they keep the deductible debt balance high. This can maximize negative gearing benefits while allowing you to redirect cash flow toward paying down non-deductible debt, like the mortgage on your own home. It’s a common strategy, but it only works if the tax savings outweigh the higher interest rate typically charged on interest-only loan products.

How much more interest will I pay over the life of the loan if I start with 5 years of interest-only?

Starting with a five-year interest-only period can add tens of thousands of dollars to your total interest bill. Because you don’t reduce the principal for those first five years, you’re paying interest on the full loan amount for a longer duration. Additionally, the remaining principal must be repaid over 25 years instead of 30, which requires a higher monthly commitment. This compounding effect is one of the most significant risks of an interest only mortgage.