What if your family home wasn’t just a roof over your head, but the strategic capital you need to launch your next chapter? Many Australians dream of entrepreneurship, yet the fear of risking their primary residence often keeps those goals on the shelf. You might feel overwhelmed by the 2026 lending environment or confused about how to manage the tax implications of using home equity to start a business. It’s a significant decision, and your desire to protect your family’s security while pursuing your passion is completely valid.

We want to help you bridge that gap with confidence and clarity. This guide explains how to safely unlock your property’s value without compromising your financial foundation. We’ll walk you through the process of determining your usable equity, structuring your loan to maximize tax benefits, and navigating the latest APRA debt-to-income requirements. You’ll gain a clear, stress-free path to funding that avoids the trap of high-interest unsecured debt, allowing you to focus on building your legacy with a steady hand and expert support.

Key Takeaways

- Learn how to calculate your ‘usable equity’ using the standard 80% Loan-to-Value Ratio (LVR) ceiling to protect your property’s security.

- Compare the flexibility of a Line of Credit against the cost-effectiveness of a lump sum refinance to find the right structure for your capital.

- Understand the critical ATO rules for using home equity to start a business and why debt separation is essential for maximizing your tax deductions.

- Identify the specific documentation and income projections needed to navigate the stricter 2026 lending environment with confidence.

- Discover how professional guidance helps you access a wider range of lenders and tailored financial structures that safeguard your family home.

What is Usable Equity for Business Purposes?

Understanding the financial foundation of your property is the first step toward your new venture. While you might have a general idea of what is home equity?, there’s a distinct difference between the total value built up in your home and what a lender will actually let you borrow. In the Australian market, total equity is simply the market value of your home minus your current mortgage balance. However, “usable equity” is the specific portion you can access for a strategic capital injection.

Lenders prioritize security. For this reason, they typically apply a safety ceiling known as the Loan-to-Value Ratio (LVR). As of early 2026, most major Australian banks cap cash-out refinances at 80% of the property’s value. This buffer ensures that even if the market fluctuates, the bank’s position remains secure. When you’re considering using home equity to start a business, this 80% limit is the most critical number in your calculations. It acts as a protective firewall for both you and the lender.

Your property’s 2026 valuation carries far more weight than your original purchase price. Since property values have shifted significantly in recent years, a professional valuation is the only way to confirm your current standing. Your existing mortgage balance also plays a heavy role. The more you’ve paid down, the more “usable” capital you have available to fund your goals. We focus on helping you identify this exact figure so you can plan your business launch with precision.

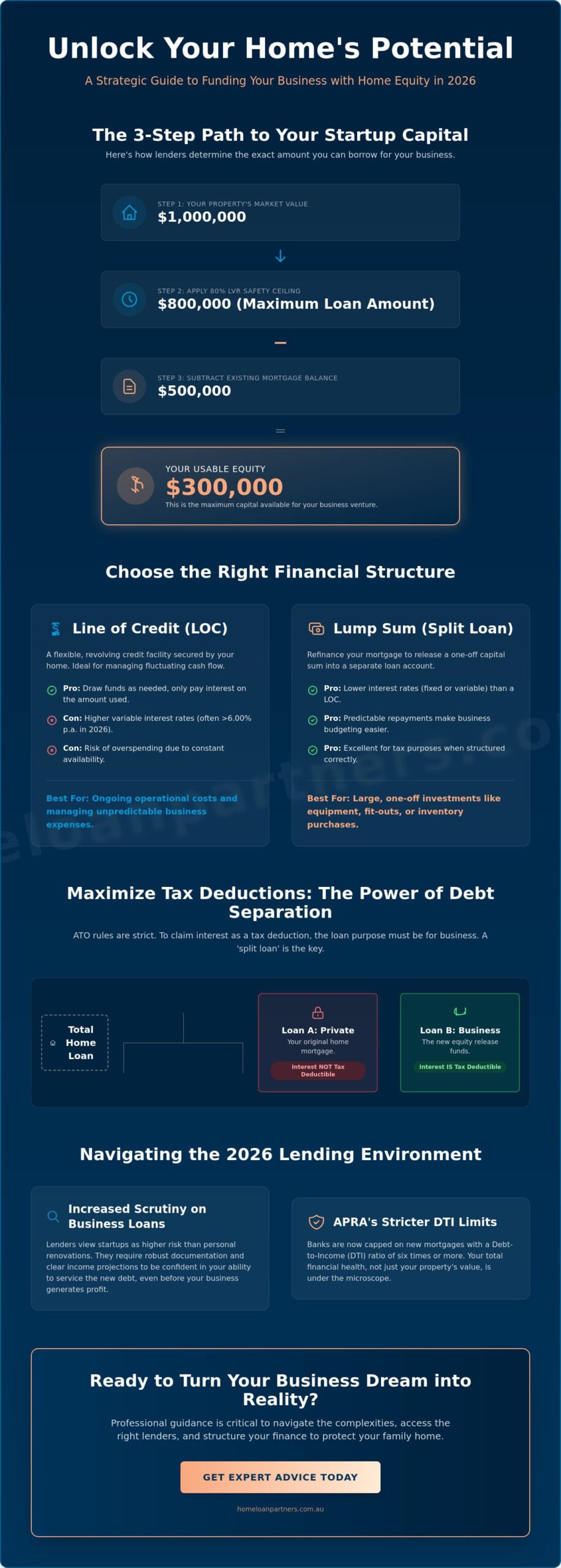

Calculating Your Usable Equity

Determining your borrowing power involves three clear steps. First, obtain a professional valuation. While online estimates give you a ballpark figure, lenders require a formal assessment to proceed. Second, calculate 80% of that total value. If your home is worth $1,000,000, your maximum lending limit is $800,000. Finally, subtract your current mortgage balance from that $800,000. If you owe $500,000, your usable equity is $300,000. This is the maximum amount available for your business venture.

Why Lenders Scrutinise Business-Purpose Equity

Lenders view business-use funds differently than a standard home loan. They see higher risk in a start-up compared to a personal renovation. Because of this, they’ll look closely at your serviceability. You must demonstrate that you can manage the increased loan repayments even before your business turns a profit. The 2026 regulatory environment, guided by APRA, has also introduced stricter debt-to-income limits. Banks are now limited to having no more than 20% of new mortgages with debt-to-income ratios of six times or more. This means your overall financial health is just as important as the bricks and mortar of your home when using home equity to start a business.

Financial Structures: Line of Credit vs. Lump Sum Refinance

Once you’ve identified your usable equity, the next step is choosing a structure that supports using home equity to start a business without straining your household budget. This choice often comes down to two main paths: a Line of Credit (LOC) or a lump sum refinance. Each has distinct advantages depending on whether you need a flexible safety net or a one-off capital injection to get your venture off the ground.

The Line of Credit Approach

An equity-based Line of Credit functions much like a high-limit credit card secured by your property. It’s a popular choice for new entrepreneurs because it provides a pool of funds you can access whenever a business need arises. You only pay interest on the amount you actually draw down, which is incredibly helpful for managing month-to-month cash flow. However, this flexibility comes at a price. LOCs typically carry higher interest rates than standard term loans. With variable rates in May 2026 often exceeding 6.00% p.a., even a small rate premium can add up. There’s also the risk of overspending, as the funds remain constantly available at your fingertips.

Lump Sum Refinancing for Capital Expenditure

For businesses that require a significant upfront investment, such as purchasing specialized machinery or securing a professional lease, a lump sum refinance is often the more economical choice. By refinancing your existing mortgage and taking out an additional portion as a standard variable or fixed-rate loan, you can often secure a lower interest rate than an LOC. This structure provides predictable monthly repayments, which makes it much easier to build a reliable business budget from day one.

Structuring this as a “split loan” is a smart way to protect your family home while pursuing your goals. This arrangement gives you one account for your home mortgage and a separate sub-account for the business funds. This separation is vital for tracking the tax implications of using your home for business. Many lenders also offer interest-only periods for the business portion, which can significantly reduce your overheads during the critical first year. While this means you aren’t paying down the principal yet, it keeps your cash liquid while you’re using home equity to start a business and finding your feet in the market.

Tax Deductibility and the Importance of Debt Separation

The Australian Taxation Office (ATO) follows a simple yet strict principle: the deductibility of interest is determined by how the funds are used, not by the asset used as security. When you are using home equity to start a business, your family home acts as the collateral, but the purpose of the loan is commercial. This distinction is the key to unlocking significant tax advantages. However, many entrepreneurs fall into the trap of “mixing” their funds, which can lead to a complicated accounting mess and potentially lost deductions.

A common error is redrawing funds from a personal home loan and depositing them into a private bank account before paying business expenses. This creates a “mixed purpose” loan. Once personal and business debts are blended in a single account, it becomes incredibly difficult to prove to the ATO exactly how much interest belongs to the business side. To maintain a clean paper trail, you should always keep these two worlds separate. While there are various business funding options available, using equity remains one of the most cost-effective provided you manage the structure with precision.

Creating a Professional Debt Firewall

We recommend setting up a dedicated sub-account or a separate loan facility specifically for your business capital. This acts as a professional firewall. When you draw down on this specific account, the funds should go directly to a business-only bank account. Never pay for a new laptop or office lease directly from your home loan’s redraw facility. This direct path ensures that every cent of interest charged on that sub-account is clearly linked to your income-producing activities. You should also align this structure with your business entity. Whether you’re operating as a sole trader or under a company structure, your loan arrangement must reflect your legal setup to ensure your tax position is protected.

Maximising Your Tax Position in 2026

Strategic debt management can do more than just fund your start-up; it can transform your overall financial health. Through a process often called debt recycling, you can effectively replace non-deductible personal debt with deductible business debt. This shift can lower your taxable income while you build your new enterprise. As of 2026, the ATO has increased its scrutiny on loan purposes, making the “purpose test” more important than ever. You must be able to demonstrate that the loan was intended to produce assessable income. Because of these complexities, a close partnership between your mortgage broker and your accountant is essential. We work alongside your tax professionals to ensure your loan structure is as efficient as possible, giving you the peace of mind to focus on your entrepreneurial goals while using home equity to start a business.

A Step-by-Step Guide to Accessing Equity in 2026

Moving from the conceptual stage to receiving your capital requires a methodical approach. The process of using home equity to start a business is more structured than a standard mortgage top-up, particularly with the 2026 focus on responsible lending and tighter debt-to-income (DTI) ratios. Since the Australian Prudential Regulation Authority (APRA) limited banks to having no more than 20% of new mortgages at high DTI levels, your application must be airtight to succeed.

The journey begins with an honest assessment of your current financial position. We look at your existing loan terms and compare them against current 2026 market rates, which for variable products often sit between 6.00% p.a. and 8.00% p.a. A fresh valuation is essential here. It confirms exactly how much of that 80% LVR safety ceiling is available for your venture. Once we know the “number,” we can begin the heavy lifting of documentation.

Preparing Your Application

Lenders in the current environment require more than just a signature. You’ll need to gather the “Big Three” to prove your readiness:

- Comprehensive Financials: This includes at least two years of personal tax returns and recent bank statements to demonstrate stable management of your current mortgage.

- A Solid Business Case: You must provide a clear business plan that outlines your goals, market research, and how the equity will be spent.

- Income Projections: Lenders want to see realistic cash flow forecasts that show how you’ll cover the new loan repayments while the business is in its infancy.

Presenting a clear exit strategy is equally vital. Lenders feel more secure when they understand your “Plan B.” Whether it’s a future refinance or a specific revenue milestone, showing a path to repayment builds the trust necessary for approval.

Navigating the Lender Panel

Not all Australian banks view business risk the same way. Some major lenders have become more cautious with cash-out refinancing for new ventures, while certain non-bank lenders specialize in supporting self-employed individuals. Each institution uses a different serviceability calculator; a loan that gets rejected by one bank might be easily approved by another based on how they “shade” your projected income.

This is where the broker advantage becomes your greatest asset. With 74.1% of new residential loans in Australia now being written by brokers, the expertise of a steady collaborator is the norm, not the exception. We handle the complex negotiations across a broad panel of lenders to find a competitive rate and a structure that suits your specific goals. If you’re ready to see which lenders align with your vision, we can help you explore commercial and business loans that leverage your equity safely. Once approved, settlement typically takes between two to four weeks, providing the capital injection you need to move forward with confidence.

Why Professional Guidance is Critical for Business-Purpose Lending

Accessing the right capital isn’t just about finding the lowest number on a screen. When you’re using home equity to start a business, the stakes are deeply personal because your family’s security is on the line. While a single bank can only offer you their own specific suite of products, a professional mortgage broker provides access to a panel of over 36 lenders. This diversity is crucial in 2026, as major banks have tightened their criteria for cash-out refinancing and high-risk lending. By looking beyond the traditional big four, we can identify non-bank and private lenders who often show more flexibility toward self-employed individuals and new SMEs.

Our team at The Home Loan Partners manages the heavy lifting of the application process, from coordinating professional valuations to organizing the complex documentation required for business-purpose loans. This proactive approach allows you to focus your energy on the actual launch of your business rather than being bogged down by lender requirements. We act as an intermediary, distilling complex financial arrangements into manageable, punchy statements that prioritize your understanding. It’s about ensuring your loan structure doesn’t just work for today but remains a steady foundation for your future goals.

Expertise Beyond the Transaction

We act as a steady hand through the inherent stress of business financing. Our role is to translate technical industry jargon into practical, actionable language so you always feel in control of your financial journey. We don’t just look at the immediate transaction; we ensure your loan structure aligns with your five-year and ten-year financial milestones. As the 2026 market continues to evolve with shifting interest rates and new APRA regulations, having an expert collaborator ensures you aren’t navigating these hurdles alone. We provide the precision-oriented guidance needed to protect your home while fueling your entrepreneurial aspirations.

Your Partner in Entrepreneurial Growth

A collaborative partnership beats a cold, transactional bank encounter every time. We understand the emotional weight of significant investments and provide the supportive, encouraging environment you need to make informed decisions. Our advice remains unbiased because our commitment is to your long-term success, not a single lender’s quota. As your business grows, we continue to work alongside you, adjusting your loan structures to reflect your increasing turnover or changing equipment needs. This focus on longevity signals that our involvement continues throughout the duration of your business journey.

If you’re ready to explore the possibilities within your property, we are here to help you navigate the path forward with patience and precision. You can start your business journey with a free equity assessment from The Home Loan Partners to discover the most secure way to fund your vision while keeping your family home protected.

Launch Your Entrepreneurial Vision with Confidence

Using home equity to start a business is a powerful way to fund your future, provided you have the right safeguards in place. You now understand how to identify your usable equity and why maintaining a strict debt firewall is essential for protecting your tax deductions. These structural choices don’t just secure your funding; they provide the long-term stability your family needs while you build your enterprise.

Navigating the 2026 lending market doesn’t have to be a solo journey. We provide personalized, jargon-free financial guidance and specialized expertise in complex business-purpose structures. With access to over 36 Australian lenders, we do the heavy lifting to find the most competitive path forward for your specific goals. If you’re ready to transform your property’s value into a strategic capital injection, we are here to guide you through every step with precision and care.

Your journey from homeowner to business owner starts with a clear strategy. Book a Strategy Session with The Home Loan Partners today to explore your options. We look forward to helping you achieve this major life milestone.

Frequently Asked Questions

Is interest on a home equity loan tax-deductible if used for a business?

Yes, interest is generally tax-deductible in Australia if the funds are used for income-producing activities. The ATO looks at the purpose of the loan rather than the property used as security. To maximize this benefit, you must keep the business portion of your debt clearly separated from your personal mortgage. Mixing these funds in one account can complicate your tax return and potentially lead to lost deductions.

Can I use home equity to start a business if I am currently unemployed?

Serviceability is the main hurdle in this scenario. Lenders require proof that you can meet the repayments even if your business is still in its early stages. If you don’t have a current salary, you might need a co-borrower with stable income or significant liquid assets. While using home equity to start a business is a strategic move, banks must follow responsible lending guidelines to ensure you aren’t placed in financial hardship.

What is the maximum LVR for a business-purpose home equity loan in Australia?

Most Australian lenders cap cash-out refinances for business purposes at a Loan-to-Value Ratio (LVR) of 80%. This means you can borrow up to 80% of your property’s current market value, minus your existing mortgage balance. This 20% buffer serves as a safety net for both you and the bank, protecting your equity position even if property market values fluctuate during your business launch.

How long does it take to access home equity for a business launch?

You can typically expect the process to take between two and four weeks. This timeline includes the initial application, a professional property valuation, and the formal settlement of funds. Having your documentation ready, such as tax returns and a clear business case, can help speed up the process. Working with a broker ensures that your application is submitted to the most efficient lender for your specific needs.

Do I need a business plan to get a home equity loan for a startup?

Yes, a comprehensive business plan is usually mandatory when you’re using home equity to start a business. Lenders want to see how the capital will be used to generate income and how you plan to manage repayments. Your plan should include realistic cash flow projections and a clear exit strategy. This documentation provides the bank with the confidence that your venture is a viable investment rather than a high-risk gamble.

What happens to my home if my business fails and I’ve used equity?

Because your home is the collateral, it remains at risk if you default on the loan. If the business fails and you cannot meet the repayments, the lender has the legal right to sell the property to recover the debt. This is why we emphasize the importance of a professional firewall between your debts and having a solid repayment plan. Protecting your family home is our priority throughout the loan structuring process.

Can I use an offset account with a business-purpose equity loan?

Yes, many lenders offer offset accounts for business-purpose sub-accounts. This is a highly effective way to manage your cash flow while reducing the interest you pay. By keeping your business’s operating capital or tax savings in an offset account, you can lower the daily interest charge on your equity loan. It’s a flexible tool that helps your money work harder while you build your new enterprise.

Is it better to use a line of credit or a standard refinance for business capital?

It depends on your specific capital needs. A line of credit offers great flexibility, allowing you to draw down funds as needed and only pay interest on what you use. However, a standard refinance into a variable or fixed-rate loan often provides a lower interest rate for large, upfront purchases like equipment. We help you compare these structures to find the one that best suits your first-year business budget.