In 2026, receiving a home loan rejection isn’t a final verdict on your financial future; it’s often just a sign that you’re talking to the wrong lender. It’s completely natural to feel frustrated when a bank’s automated system ignores your hard work or when complex serviceability math feels like a moving target. You might even worry that a single “no” has permanently damaged your credit score or ruined your chances of homeownership.

We understand that this process feels heavy, but there is a clear path forward. This guide explains exactly what to do if home loan is rejected by helping you identify the root cause of the issue and matching your needs with the right lending policy. You’ll learn how to navigate the latest 2026 regulatory shifts, such as the elimination of mandatory minimum credit scores by Fannie Mae and Freddie Mac. We’ll show you how to turn that initial setback into a successful approval by finding a partner who sees the person behind the paperwork and understands your long-term goals.

Key Takeaways

- Reframe a loan decline as a simple policy mismatch rather than a personal financial failure to maintain your confidence.

- Discover how to categorize lender concerns into capacity, character, or collateral to identify the exact fix required for your situation.

- Learn exactly what to do if home loan is rejected by leveraging a broad network of lenders with diverse credit policies.

- Follow a structured 2026 recovery plan designed to move you from a “no” to a successful settlement through clear, logical steps.

- Understand the value of an expert collaborator who prioritizes your unique story and long-term milestones over a cold transaction.

Understanding the Rejection: Why “No” Is Not the End of the Road

Hearing “no” from a lender can feel like a door slamming shut on your future. It is frustrating and deeply personal when you have worked hard to save a deposit and plan for your new home. However, a rejection is rarely a commentary on your financial worth. In most cases, it is a simple mismatch between your current profile and a specific bank’s internal rules. One decline does not mean you are ineligible for a mortgage; it just means that particular lender isn’t the right fit for you right now.

In the 2026 market, lender “appetite” shifts constantly. Banks adjust their lending criteria based on their current portfolios and broader economic conditions. For instance, a bank might stop lending to certain postcodes or employment types if they already have too much exposure in those areas. This means you could be rejected by one bank on Monday and find another lender eager to work with you on Tuesday. Understanding the mortgage underwriting process helps you see that these decisions are based on risk algorithms rather than your character.

Knowing what to do if home loan is rejected starts with maintaining a calm perspective. A single rejection only becomes a problem if you react by making multiple, desperate applications. When handled with a steady hand and a clear strategy, your first decline can actually serve as a useful data point that leads you toward a more suitable lending partner.

The “Computer Says No” Phenomenon

Large institutions often rely on automated credit scoring systems to process applications quickly. These algorithms are designed to find “perfect” applicants who fit into very narrow boxes. If your situation involves unique income streams, self-employment, or a slightly lower credit score, the computer might automatically decline the file without a human ever looking at it. Smaller or specialist lenders often use manual underwriting. This approach allows a human credit officer to review the nuances of your application, often finding a path to “yes” that an algorithm completely missed.

Immediate Steps to Protect Your Credit File

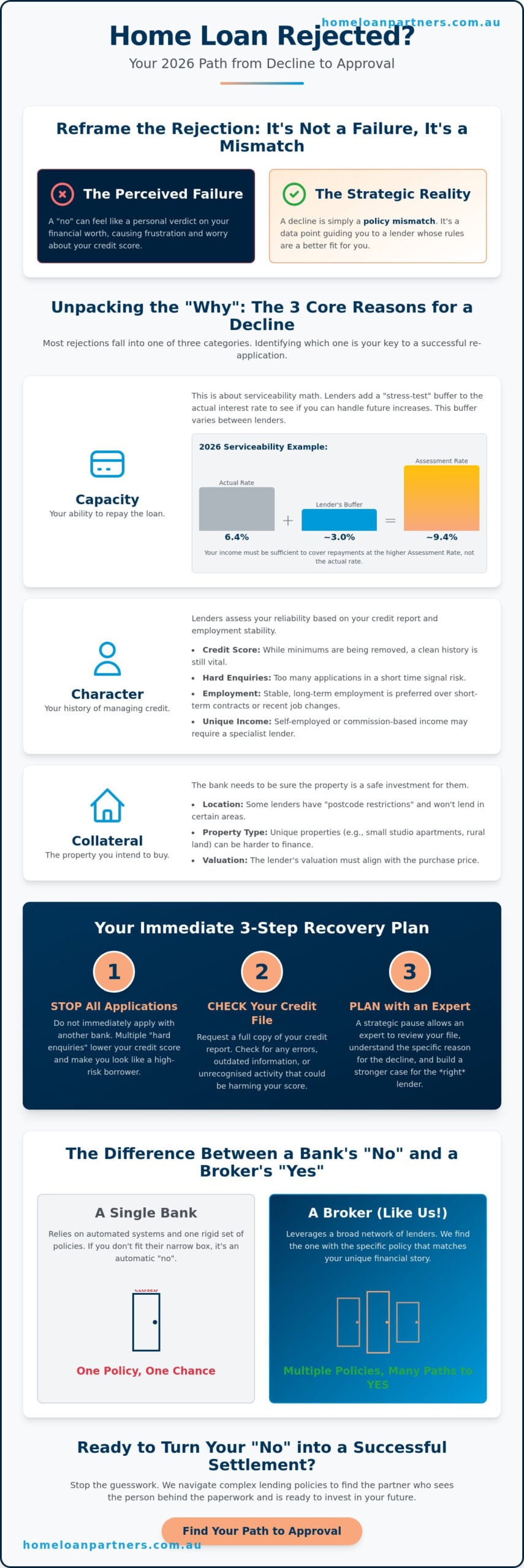

Your first instinct might be to apply with another bank immediately, but this is the most common mistake borrowers make. Every time you submit a formal application, the lender performs a “hard enquiry” on your credit report. Too many of these in a short period can lower your score and make you look like a high-risk borrower to future lenders. To protect your financial standing, follow these steps:

- Stop all new credit applications immediately, including “Buy Now, Pay Later” services.

- Request a copy of your credit report to check for any errors or outdated information.

- Wait for a professional review of your file before trying again.

A strategic pause is often the best thing you can do. It gives you time to understand the specific reason for the decline and allows us to build a stronger case for your next application. Knowing what to do if home loan is rejected involves patience and precision rather than speed. Most credit score impacts from a single enquiry are temporary, and we can typically prepare a fresh, successful strategy within a few weeks or months.

Unpacking the “Why”: Common Reasons Lenders Decline Applications

A mortgage rejection can feel like a personal critique of your lifestyle, but it is rarely about being “bad with money.” Most declines fall into three distinct categories: Capacity, Character, and Collateral. Capacity refers to your ability to repay the debt; Character looks at your credit history and employment stability; and Collateral focuses on whether the property itself is a safe investment for the bank. Understanding which category caused your setback is the first of many steps to take after a denial.

In 2026, the biggest hurdle for many is “serviceability math.” With average 30-year fixed rates sitting between 6.37% and 6.46% as of May 2026, lenders apply a stress-test buffer to ensure you can handle even higher repayments. Crucially, these buffers are not uniform across the industry. Some lenders use a strict 3% assessment rate above the current product rate, while others have more flexible internal policies. If you have been declined by one bank, it might simply be that their specific buffer calculation pushed your application over the edge. Determining what to do if home loan is rejected often starts with finding a lender whose math better aligns with your actual income.

Serviceability and Hidden Debts

Modern lenders have a laser focus on your monthly commitments. Australian banks treat HECS/HELP debt as a direct reduction of your take-home pay, which can slash your borrowing power by tens of thousands of dollars. Additionally, as of 2026, “Buy Now, Pay Later” (BNPL) payment history is now standard on credit reports. Even small, interest-free installments are viewed as ongoing liabilities that eat into your repayment capacity. To see where you stand, you can use our borrowing power calculator to self-assess before your next move.

Property and Security Issues

Sometimes, you are the perfect borrower, but the property is the problem. Lenders often “blackball” specific security types, such as apartments under 40 square meters or homes in postcodes they deem to have too much high-density supply. An unsatisfactory valuation can also trigger a rejection if the bank believes you are overpaying for the asset. Furthermore, if you have a smaller deposit, you must clear the hurdles of both the bank and their Lenders Mortgage Insurance (LMI) provider. If the LMI provider rejects the application, the bank has no choice but to say no.

If you’re feeling stuck, remember that a rejection is just a signal to pivot. As your expert collaborator, we can help you identify exactly what to do if home loan is rejected by matching your unique profile to a lender who values your specific situation.

The Difference Between a Bank’s ‘No’ and a Broker’s ‘Yes’

When you walk into a local bank branch, you are essentially asking a single provider if you fit their specific mold. If you don’t, they simply say no. They can’t recommend a competitor, even if that competitor has a policy that perfectly suits your needs. This is where the partnership with a broker changes the narrative. Instead of being limited to one set of criteria, you gain access to a “36+ Lender Advantage.” We act as your expert collaborator, translating your complex financial story into a language that different lenders understand.

While a bank officer is bound by their employer’s rules, a broker’s loyalty lies with your goals. We look beyond the common reasons for loan denial to find the one lender whose “appetite” matches your profile. It’s about finding the path of least resistance to your approval. If you’re wondering what to do if home loan is rejected, the answer is often to stop knocking on the same door and instead use a master key that opens dozens of others.

Policy Niches You Might Not Know About

Lending policies are not a monolith. Some banks are exceptionally friendly to self-employed borrowers or contractors with shorter work histories. Others might count 100% of your overtime, bonuses, or rental income, while a competitor might only consider 80%. These small variations in policy can be the difference between a decline and a settlement. A skilled finance broker identifies these specific niches to rescue an application that a traditional bank might have dismissed. We don’t just look for non-bank alternatives; we often find traditional lenders who simply have a different perspective on your specific income type.

The Power of a Pre-Submission Review

One of the most valuable services we provide is the “heavy lifting” before your application ever reaches a lender’s system. We use sophisticated software to simulate lender assessments, allowing us to see how an application will perform against various credit models, including the newer 2026 scoring models like VantageScore 4.0. This vetting process is crucial for anyone figuring out what to do if home loan is rejected. By identifying potential red flags early, we can address them or pivot to a different lender before a hard enquiry hits your credit file. This proactive approach ensures a stress-free experience, turning a complex financial hurdle into a predictable, steady journey toward homeownership.

Your 2026 Recovery Plan: Steps to a Successful Re-application

Moving from a rejection to a successful settlement is a process of refinement. It’s not about hiding your past; it’s about presenting your future in the best possible light. When you’re figuring out what to do if home loan is rejected, transparency with your expert collaborator is your greatest asset. We need to know exactly why the previous lender said no so we can build a wall of evidence that proves your reliability. Often, this restructuring doesn’t just get you an approval; it results in a cleaner financial profile that qualifies you for a more competitive interest rate.

Focus on a 90-day window of financial hygiene. Lenders typically look at your last three months of bank statements to assess your lifestyle and spending habits. By tightening your belt for just one quarter, you can demonstrate the discipline required for a long-term mortgage commitment. This steady approach alleviates the inherent stress of the process by giving you a clear, achievable goal.

Audit Your Financial “Digital Footprint”

Your first step is to download your credit report from providers like Equifax or Experian. In 2026, credit reports now include “Buy Now, Pay Later” (BNPL) history, but they also exclude paid medical collections and debts under $500. Check your file for errors. Sometimes a simple administrative mistake, like an incorrect address or a debt that should have been marked as paid, can trigger an automatic rejection. If you find a discrepancy, dispute it immediately. This is a proactive way to manage the heavy lifting before your next application.

Next, look at your bank statements through a lender’s eyes. Excessive subscriptions, frequent gambling transactions, or erratic spending patterns can signal risk. Cleaning up these digital footprints for three months creates a pristine window that gives a manual underwriter the confidence to say yes. It’s about showing that you’re in control of your financial journey.

Restructuring and Debt Consolidation

One of the fastest ways to boost your borrowing power is to close unused credit cards. Banks don’t care if your balance is zero; they assess you on the total credit limit. A $10,000 limit can reduce your borrowing capacity significantly, even if you never use the card. Consolidating smaller debts, like car loans or personal finance, into a single manageable payment can also improve your serviceability profile. This structural simplicity helps to build trust with a new lender.

If you’re a first-time buyer, check our first home buyer guide for long-term saving strategies that align with 2026 lending standards. If you’re ready to start your recovery journey today, reach out to our team for a confidential review of your situation. We’ll help you navigate the path from a “no” to a keys-in-hand “yes” with patience and precision.

How The Home Loan Partners Navigate the Path to Approval

At The Home Loan Partners, we act as your steady hand and expert collaborator throughout the recovery process. We understand that a mortgage rejection feels like a significant hurdle, but we see it as a prompt to refine your strategy. Our team takes a deeply client-centric approach, prioritizing your unique story over a bank’s automated checklist. When you are deciding what to do if home loan is rejected, we step in to manage the heavy lifting, ensuring you feel supported rather than overwhelmed by complex financial jargon.

Our philosophy is simple: we assess the person, not just the paperwork. While a bank’s algorithm might only see a set of numbers, we look at your career trajectory, your long-term aspirations, and the context behind your financial history. This personal relationship allows us to build a narrative that resonates with the right credit officers. We are committed to your long-term journey, meaning our partnership continues long after you receive your keys, helping you manage your mortgage as your life milestones evolve.

Access to Specialist and Non-Conforming Lenders

A “no” from a Big Four bank is often just the beginning of a more targeted search. Many of the most flexible lenders in the 2026 market do not deal directly with the public, preferring to work through professional intermediaries who understand their specific requirements. We provide you with a direct line to these specialist and non-conforming lenders. For borrowers with unique financial structures, such as the self-employed or those with multiple income streams, we can leverage “Alt-Doc” loans. These products allow us to use alternative evidence of income to find a solution that traditional institutions might overlook. Knowing what to do if home loan is rejected often involves looking toward these specialized paths that offer the precision your situation requires.

A Partnership Built on Transparency

We believe in a collaborative process where transparency is the foundation of our success. Together, we will build a “bulletproof” application by addressing every potential lender concern before the file is submitted. This proactive method minimizes the risk of further declines and protects your credit score. Our support doesn’t end at settlement; we provide ongoing reviews to ensure your loan remains aligned with the current market, which is a core benefit of our long-term partnership model. If you’re ready to move past a recent decline and find a clear path forward, it’s time to book a strategy session with The Home Loan Partners. We’ll review your rejection with patience and precision, helping you secure the future you’ve worked so hard to build.

Secure Your Path to Homeownership Today

A mortgage rejection is not the final word on your homeownership dreams. It is often a sign that your current lender’s automated systems don’t fully understand your unique financial story. By auditing your credit report and refining your bank statements over a 90 day window, you can present a much stronger case to a lender whose policy actually fits your life. Small adjustments to how you manage debt or present your income can completely change the math in your favor.

Knowing what to do if home loan is rejected means looking beyond the initial “no” and partnering with a guide who can navigate the complexities of 2026 interest rate buffers and HECS debt for you. We provide access to 36+ Australian lenders and offer professional, stress-free guidance from your first audit to the final settlement. Our team is here to manage the heavy lifting so you can focus on the excitement of your new home.

Let our expert brokers turn your rejection into an approval; contact The Home Loan Partners today. Your journey is still very much alive, and we’re ready to help you take that next steady step with confidence.

Frequently Asked Questions

Does a home loan rejection hurt my credit score?

A home loan rejection doesn’t appear as a “decline” on your credit report, but the hard enquiry made during the application process does. Each formal enquiry can temporarily lower your score. If you make multiple applications in a short period, it signals to lenders that you may be in financial distress. This is why it’s vital to pause and review your strategy before trying again.

How long should I wait to apply again after being rejected?

We generally recommend waiting three to six months before submitting a new application. This window allows you to establish a pristine 90 day history of “financial hygiene” on your bank statements. It also gives your credit score time to stabilize after the previous enquiry. During this time, we focus on identifying what to do if home loan is rejected to ensure your next move is precise.

Can I get a home loan with a different bank after one says no?

You can certainly secure an approval with a different bank because every lender operates with unique “appetite” and assessment buffers. A “no” from one institution is often just a sign that you didn’t fit their specific algorithm at that moment. We match your profile with a lender whose internal policies are more favorable to your specific employment type or property choice.

Will a lender tell me the exact reason my loan was declined?

Lenders are required to provide a reason for a decline, but these explanations are often automated and frustratingly vague. You might receive a letter citing “unsuitable credit history” or “insufficient capacity” without seeing the specific math behind the decision. We help you look past the template response to find the actual root cause that the bank’s computer system missed.

Can I use a mortgage broker if I have already been rejected by a bank?

Using a mortgage broker after a rejection is the most effective way to turn your situation around. We act as an expert collaborator to review your previous file and find a lender with a policy that actually fits. We have access to over 36 Australian lenders, many of whom specialize in applications that don’t fit the narrow boxes of the major banks.

What is the most common reason for home loan rejection in 2026?

In 2026, the most common reason for rejection is a mismatch in serviceability buffers. With average 30 year fixed rates between 6.37% and 6.46%, many borrowers are falling just short of the bank’s “stress test” requirements. Lenders are also heavily scrutinizing “Buy Now, Pay Later” (BNPL) habits and HECS debt, which can reduce your borrowing power more than in previous years.

Can I still get a home loan if I have a small deposit or HECS debt?

You can still achieve homeownership with a small deposit or HECS debt by choosing a lender with more flexible assessment rules. Some banks treat HECS repayments as a smaller hit to your take-home pay than others. We help you figure out what to do if home loan is rejected by identifying the specific lenders who are “friendly” to first-time buyers with existing student liabilities.

Is it possible to appeal a lender’s decision to reject my application?

While you can request a manual review or “appeal” a decision, it is rarely successful if you simply don’t fit that bank’s core policy. It’s usually much more effective to pivot to a different lender whose rules already align with your financial profile. We help you find the path of least resistance rather than trying to force an approval from a lender that isn’t the right fit.