What if waiting to save a full 20% deposit is actually costing you more in rising property prices than the insurance fee you’re trying to avoid? It’s a common fear for first-home buyers who feel stuck in a cycle of renting while trying to hit a moving financial target. Understanding what is lenders mortgage insurance and how to avoid it is the first step toward breaking that cycle. At The Home Loan Partners, we believe your path to a new home should be steady and transparent, not a source of hidden anxiety.

You might feel like LMI is a penalty, but in the 2026 property market, it’s often a strategic choice. Since the landscape for Australian buyers shifted recently with new government initiatives and lender exemptions, more buyers can now bypass this cost or use it to enter the market sooner. In this guide, we’ll explain how LMI works, explore specific 2026 exemptions, and help you decide whether to pay the premium or keep saving. We’ll provide the clarity you need to move forward with total confidence and a clear plan for your future.

Key Takeaways

- Master the 80% LVR rule to understand exactly how your deposit size influences your loan approval and overall costs.

- Discover what is lenders mortgage insurance and how to avoid it using professional strategies that align with the latest 2026 property market shifts.

- Evaluate the “cost of waiting” to see if paying a one-off premium today is more financially beneficial than chasing rising house prices.

- Explore how family guarantees and specific lender waivers can help you secure a home loan without needing a traditional 20% deposit.

- Learn how a dedicated mortgage partner compares premiums across dozens of lenders to find the most competitive, tailored deal for your journey.

What is Lenders Mortgage Insurance (LMI)?

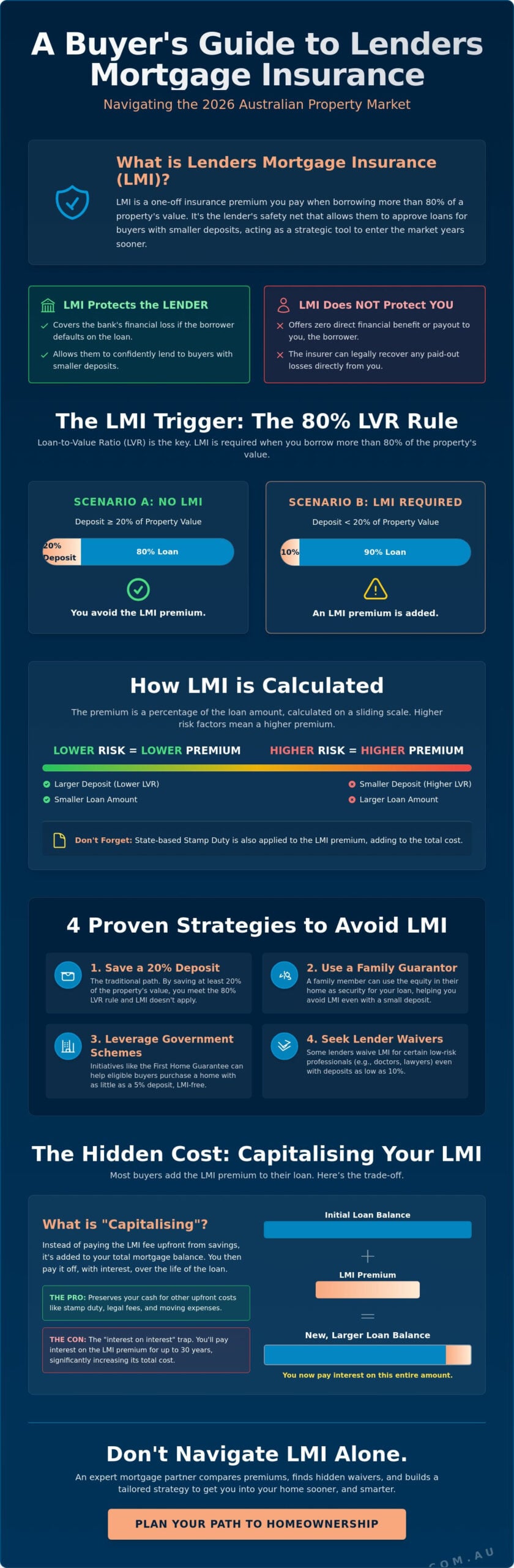

Lenders Mortgage Insurance is a concept that often causes a lot of stress for home buyers. Put simply, it’s a one-off premium you pay to the lender if your deposit is less than 20% of the property’s value. While it represents an extra cost, it’s also a powerful tool that has helped thousands of Australians enter the property market years earlier than if they had waited to save a massive deposit. Understanding what is lenders mortgage insurance and how to avoid it starts with knowing why banks use it as a safety net. At The Home Loan Partners, we focus on making this complex topic easy to understand so you can move forward with total confidence.

The industry standard is the 80% Loan-to-Value Ratio (LVR) rule. If you borrow more than 80% of a home’s price, the bank considers the loan higher risk. This is where Lenders Mortgage Insurance (LMI) comes in. It acts as a security blanket for the bank, allowing them to lend to people who have smaller savings but strong incomes. Without LMI, most lenders would simply refuse any application with less than a 20% deposit, leaving many buyers stuck in the rent trap for decades.

Don’t confuse LMI with Mortgage Protection Insurance. While the names sound similar, they serve opposite purposes. Mortgage Protection Insurance is a policy you take out to cover your repayments if you lose your job or fall ill. LMI provides zero direct financial benefit to you as the borrower; it’s strictly there to protect the lender’s interests if things go wrong. We believe in complete transparency, so you always know exactly what you’re paying for and why.

Who does LMI actually protect?

It’s a common misconception that LMI covers the borrower if they can’t make their mortgage payments. In reality, it protects the bank. If you default on your loan and the bank has to sell your property at a loss, the LMI provider pays the bank the difference. However, your obligations don’t end there. Under a legal principle called the ‘Right of Subrogation,’ the insurance company can seek to recover those losses from you directly after they’ve paid the bank. The team at The Home Loan Partners acts as your expert guide to ensure your loan remains sustainable, so you never have to face this scenario.

The role of LMI providers in Australia

In the Australian market, major players like Helia (formerly Genworth) and QBE provide the majority of LMI policies. You usually don’t get to choose your insurer; that’s decided by the bank you pick for your home loan. This is a critical detail because LMI providers have their own strict lending criteria that can be even tougher than the bank’s own rules. Sometimes, a bank might be happy to lend to you, but their insurer says no. Having a dedicated partner to help you navigate these hidden hurdles is essential for a seamless approval process.

How is LMI calculated and paid in 2026?

Calculating LMI isn’t as simple as checking a fixed price tag. It operates on a sliding scale that shifts based on your Loan-to-Value Ratio (LVR) and the total amount you’re borrowing. As your deposit shrinks, the risk to the lender climbs, which pushes the premium percentage higher. For instance, a buyer taking out a $900,000 loan with a 10% deposit will face a much higher LMI rate than someone borrowing $400,000 with the same 10% deposit. This happens because the insurer’s potential exposure is far greater on the high-value property. At The Home Loan Partners, we help you understand what is lenders mortgage insurance and how to avoid it by modeling these specific costs for your target suburbs.

Many buyers are surprised to discover that LMI also attracts state-based costs. Moneysmart defines LMI as an insurance policy, and like most insurance products in Australia, it’s subject to stamp duty. This tax varies depending on which state or territory you’re buying in. It can add thousands to your final bill. When we act as your mortgage partner at The Home Loan Partners, we make sure these hidden figures are factored into your budget early so there are no shocks at settlement.

You generally have two ways to handle this cost. You can pay it upfront as a lump sum, or you can choose to “capitalise” it. Capitalising is the most common path for first-home buyers. It involves adding the LMI premium to your total loan balance, which preserves your hard-earned cash for things like moving costs or new furniture.

Capitalising LMI: Pros and Cons

Adding the premium to your mortgage helps you enter the market sooner, but it creates a long-term “interest on interest” trap. Because the LMI is now part of your principal, you’ll pay interest on that insurance fee for the entire life of the loan. This can nearly double the effective cost of the premium over 30 years. Capitalising the LMI premium increases your total loan amount and technically raises your LVR at the very start of your homeownership journey.

LMI Portability and Refunds

Refinancing early can be a major hurdle if you’ve paid LMI. Most LMI policies aren’t “portable,” meaning if you switch lenders while your equity is still under 20%, you’ll likely have to pay for a second policy with the new bank. While some insurers offer a partial refund if you pay off the loan within the first 12 to 24 months, these are often small and subject to strict conditions. Understanding what is lenders mortgage insurance and how to avoid it involves looking beyond the first year to ensure you aren’t trapped with one lender for too long.

The Strategic Choice: Is paying LMI worth it?

Most buyers view LMI as a hurdle, but it’s actually a strategic bridge. When you’re weighing up what is lenders mortgage insurance and how to avoid it, you must consider the speed of the 2026 property market. Waiting to save an extra $50,000 to reach a 20% deposit often takes years. In that time, a $800,000 home growing at a modest 5% annually will increase in price by $40,000. By the time you’ve saved your deposit, the home you wanted is now $40,000 more expensive. In this scenario, paying a $15,000 LMI premium is the more logical financial move.

LMI isn’t always the right answer. In a stagnant market where prices aren’t moving, or in high-interest environments where debt is expensive, the “cost of waiting” is lower. If property values aren’t rising faster than you can save, paying for insurance that protects the bank provides no benefit to your net wealth. We act as your expert partner to help you analyse these local trends, ensuring you don’t pay for insurance unless it gives you a clear head start on your long-term journey.

The Rent vs. LMI Calculation

The math often reveals a surprising truth. If your weekly rent is $600, you’re paying over $31,000 a year to a landlord. If an LMI premium for your target home is $12,000, paying that fee allows you to stop “throwing away” rent immediately. You start building equity in your own asset instead of someone else’s. The break-even point for an LMI purchase is reached when the combined cost of the premium and interest is lower than the total rent paid and price growth experienced during the extra time spent saving.

Market Entry Timing

Time in the market usually beats timing the market. Using LMI to secure a property in a high-demand area today protects you from being priced out of that suburb tomorrow. There’s also a significant psychological benefit to homeownership that a spreadsheet can’t capture. Moving out of the rental cycle provides a sense of security and a permanent place for your family. While what is lenders mortgage insurance and how to avoid it is a financial question, the answer often involves your lifestyle goals and the peace of mind that comes with owning your own front door.

Proven strategies to avoid LMI in Australia

The most traditional way to sidestep this extra cost is to save a full 20% deposit. While this remains the most direct path, we know that saving six figures while paying record-high rents is a massive challenge in 2026. Fortunately, the lending environment has evolved. Understanding what is lenders mortgage insurance and how to avoid it now involves looking at professional exemptions and expanded government support that didn’t exist a few years ago. If you’re ready to start your journey, our first home buyer loans specialists can help you identify which of these paths fits your specific situation.

The key to avoidance is reducing the lender’s perceived risk. Whether through your profession, a government backing, or a family member’s support, there are multiple ways to reach that “magic” 80% LVR threshold without actually having the cash in your bank account. We act as your expert partner to navigate these options, ensuring you don’t spend years in the rent trap when a solution might be available to you today.

Professional LMI Waivers in 2026

Lenders often view certain high-income earners as low risk due to their stable career paths and high earning potential. If you work in the “Big Four” professions, doctors, lawyers, accountants, or engineers, you might qualify for a 90% LVR without paying a cent in LMI. Banks offer these waivers because data shows these professionals have incredibly low default rates. Income thresholds apply, usually requiring a minimum annual salary between $120,000 and $150,000 depending on the lender. For those who qualify, this is a powerful, cost-free shortcut to homeownership.

Government Schemes: First Home Guarantee (FHBG)

The landscape for government support changed significantly on October 1, 2025. The First Home Guarantee now offers unlimited places and has removed previous income caps, making it accessible to a much wider range of Australians. Under this scheme, the Federal Government acts as a guarantor for your 15% deposit gap. This allows you to buy with as little as a 5% deposit while completely avoiding LMI. With property price caps now sitting at $1.5 million in Sydney and $1 million in Brisbane, these schemes are more aligned with actual market prices than ever before. Permanent residents are also now eligible, expanding the dream of homeownership to more members of our community.

The Guarantor Strategy: Benefits and Risks

A family guarantee is another effective way to bridge the 20% gap without using your own cash. Instead of a cash gift, your parents use a portion of the equity in their own home as security for your loan. We typically recommend a limited guarantee. This means the guarantor is only responsible for the 20% portion of the loan rather than the whole amount. It’s vital to have a clear exit strategy; you can release the guarantor once your property value has grown or you’ve paid down the loan enough to reach 80% LVR. Because this involves family assets, parents must obtain independent legal advice to ensure everyone is protected during the process.

How a Mortgage Partner helps you navigate LMI

Finding the right path through the Australian property market doesn’t have to be a solo effort. While you now understand what is lenders mortgage insurance and how to avoid it, applying that knowledge requires a deep dive into the specific policies of over 36 different lenders. LMI premiums are not standardized. The cost can vary by thousands of dollars from one bank to the next for the exact same property and deposit. We act as your expert partner to scan the entire market, identifying lenders who currently offer internal waivers or ‘LMI specials’ that could save you a significant amount of money at settlement. This wide lens ensures you don’t miss out on boutique lenders who specialize in your specific professional background or property type.

Structuring your application is just as vital as choosing the right lender. LMI providers have their own set of guidelines that are often stricter than the bank’s own criteria. They look closely at your employment history, the type of property you’re buying, and even the suburb it’s located in. We do the heavy lifting by ensuring your financial profile meets these specific insurer requirements before you even hit submit. This proactive approach creates a seamless experience and protects your credit score from unnecessary rejections. Our involvement continues well beyond your first home purchase. We help you plan for the long term, identifying the exact moment you can refinance to remove the ‘LMI shadow’ once your equity reaches that crucial 20% mark.

Custom Loan Structuring

When we sit down to look at your options, we don’t just look at the lowest interest rate. We analyze the total cost of the loan over time. If you choose to capitalise your premium, we can help you set up an offset account to mitigate the extra interest costs. Sometimes, a lender with a slightly higher interest rate but a much lower LMI premium actually works out cheaper over the first five years of your loan. We provide the clarity you need to make these complex decisions with ease. Learn more about our First Home Buyer services to see how we tailor these strategies to your unique goals and future security.

Your Next Steps to Homeownership

Your journey toward the Australian dream starts with a clear understanding of your borrowing power. In the competitive 2026 market, having an expert guide is the difference between feeling stuck and moving forward with precision. We offer a comprehensive pre-assessment that maps out your path, whether you’re avoiding LMI or using it as a strategic tool to get into the market sooner. Our goal is to make the process as stress-free as possible while you master what is lenders mortgage insurance and how to avoid it. Book a strategy session with The Home Loan Partners today and let’s turn your homeownership aspirations into a reality.

Take Control of Your Homeownership Journey

Navigating the 2026 property market requires more than just a deposit; it requires a strategy that balances speed with long-term security. You’ve seen that LMI can be either a costly hurdle or a vital bridge to homeownership depending on your local market’s growth and your personal career path. By leveraging the expanded Home Guarantee Scheme or professional waivers, you can often bypass these premiums entirely. Understanding what is lenders mortgage insurance and how to avoid it empowers you to make a choice based on data rather than fear.

At Home Loan Partners, we act as your steady guide through this complex landscape. We provide access to 36+ Australian lenders and specialize in the latest First Home Buyer Schemes to ensure you never pay more than necessary. Our team focuses on building tailored loan structures that prioritize your wealth throughout the life of your mortgage. Ready to see if you can avoid LMI? Speak with a Home Loan Partner today. Your journey to the Australian dream is closer than you think, and we’re here to ensure it’s a seamless, rewarding experience from your first application to your final repayment.

Frequently Asked Questions

Is LMI a one-off payment or monthly?

LMI is a one-off premium paid at the start of your loan, not a recurring monthly bill. You can pay it upfront on settlement day or include it in your total loan balance. Most Australians choose to capitalize the cost so they don’t need extra cash immediately. This allows you to focus your savings on your deposit while the insurance cost is spread over the life of your mortgage.

Can I get LMI refunded if I refinance my loan?

You generally cannot get a full refund for LMI when you refinance, but some insurers offer a partial refund if you switch within the first 12 to 24 months. These refunds are typically small and decrease quickly as time passes. Since LMI isn’t portable between lenders, refinancing with a low equity position often means paying for a new policy. We help you calculate if the lower interest rate of a new loan outweighs the cost of a second premium.

How much is LMI on a $600,000 home with a 5% deposit?

For a $600,000 property with a 5% deposit, your LMI premium could range between $15,000 and $25,000 depending on the specific lender and insurer guidelines. This higher cost reflects the increased risk of a 95% Loan-to-Value Ratio. Because rates aren’t standardized, we compare options across 36+ lenders to find the most competitive pricing for your situation. Learning what is lenders mortgage insurance and how to avoid it can save you this entire amount through government schemes.

Does every bank charge the same amount for LMI?

No, LMI costs vary significantly between banks because lenders use different insurance providers like QBE or Helia. Some banks also have internal waivers or “LMI specials” for certain professions or loan types. We act as your expert partner to identify which lender offers the most favorable premium for your specific financial profile. This comparison can often save you thousands of dollars in upfront costs.

Can I avoid LMI if I am a first-home buyer in 2026?

Yes, you can absolutely avoid LMI in 2026 by accessing the expanded Home Guarantee Scheme. Since October 1, 2025, eligible buyers can purchase a home with as little as a 5% deposit without paying any insurance premiums. The removal of income caps and the introduction of unlimited places make this more accessible than ever. We guide you through the eligibility process to ensure you secure one of these spots and keep your hard-earned savings.

What happens to my LMI if I sell my house after two years?

If you sell your property, your LMI policy simply ends and provides no further benefit or value. The premium you paid at settlement is non-refundable upon sale and cannot be transferred to your next purchase. Because LMI protects the lender for that specific mortgage contract, a new loan for a new home will require a fresh assessment of your deposit and equity.

Is LMI tax-deductible for investment properties?

Yes, LMI is generally tax-deductible if the property is used for investment purposes. The Australian Taxation Office typically allows you to claim the cost of the premium over five years or the life of the loan, whichever is shorter. This deduction can help offset the cost of the premium over time. We recommend discussing your specific tax situation with an accountant to maximize these benefits as part of your long-term wealth strategy.

Can I add the LMI cost to my total loan amount?

You can add the LMI premium to your total mortgage through a process called capitalization. This means you don’t have to pay the cost out of your own pocket at settlement, which is helpful if your savings are tight. While this preserves your cash, it does increase your total loan balance and the amount of interest you’ll pay over the years. We help you weigh this trade-off to ensure it aligns with your financial goals.