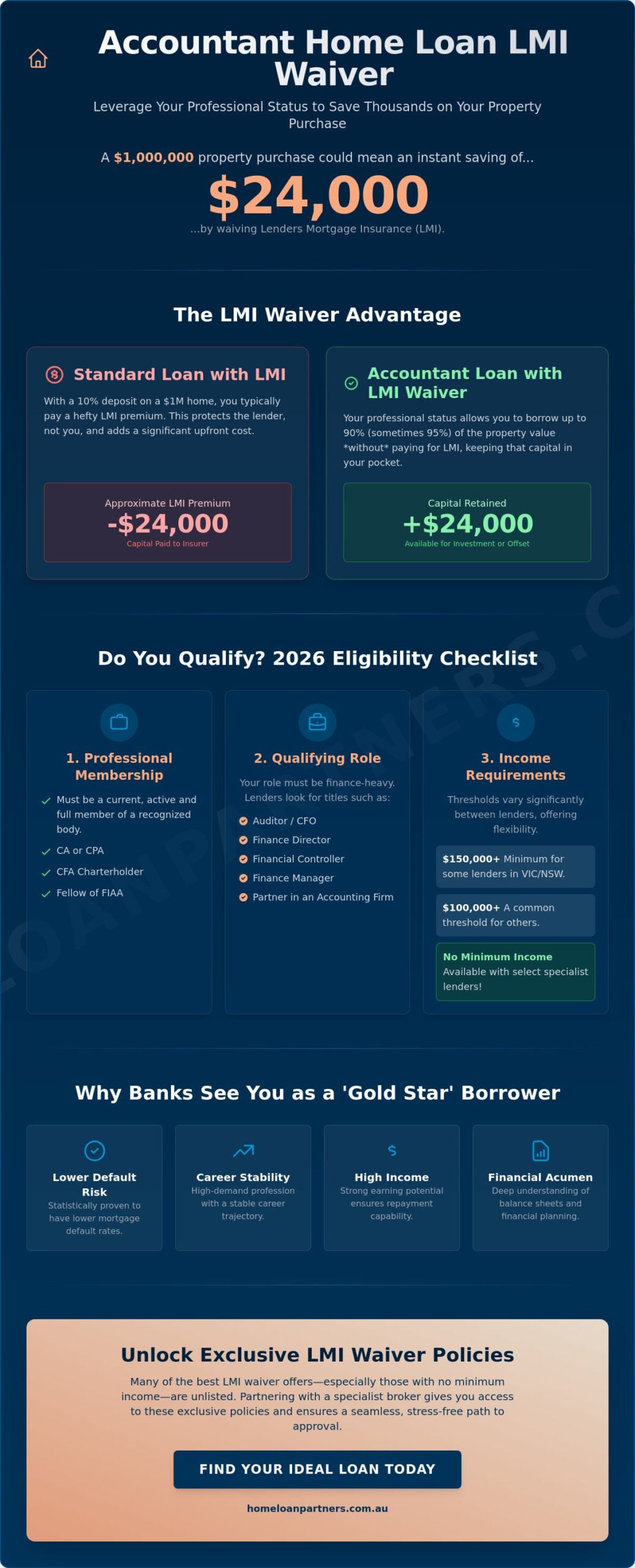

Did you know that your professional accreditation could instantly save you $24,000 on a $1,000,000 property purchase? Most lenders view your career as a low-risk investment, yet many professionals still find the high cost of insurance eating into their hard-earned equity. You’ve dedicated years to achieving your status, and it’s only fair that your mortgage reflects your financial reliability. At The Home Loan Partners, we understand the frustration of meeting strict lending criteria when your income and career trajectory tell a much stronger story.

This guide explains how to secure an accountant home loan LMI waiver so you can borrow up to 90% of a property’s value, or even 95% for some owner-occupiers, without paying a cent in insurance premiums. You’ll learn the exact 2026 requirements, from flexible income policies to the varying thresholds across different Australian states. We’ll walk you through the recognized professional bodies and help you find a partner who values your expertise. By the end of this article, you’ll have a clear, stress-free path to your Australian dream, keeping your capital exactly where it belongs: in your pocket.

Key Takeaways

- Leverage your professional status to bypass Lenders Mortgage Insurance and keep tens of thousands of dollars in your pocket.

- Navigate the 2026 eligibility landscape for an accountant home loan LMI waiver, including lenders that offer no minimum income requirements.

- Unlock the potential to borrow up to 90% or 95% of your property’s value while maintaining a smaller deposit.

- Learn how to prepare a seamless application by gathering the right evidence of your professional membership and income.

- Discover why partnering with a specialist broker provides access to exclusive, unlisted policies tailored to finance professionals.

What is an Accountant Home Loan LMI Waiver?

Buying a home usually involves a strict 20% deposit rule if you want to avoid extra costs. For most Australians, Lenders Mortgage Insurance (LMI) represents a significant financial hurdle. It’s a one-off premium that protects the bank, not the borrower, in case of a default. On a $1,000,000 property with a 90% loan, this insurance can cost approximately $24,000. That’s a substantial amount of capital that could stay in your offset account or fund a renovation rather than being handed over to an insurer.

An accountant home loan LMI waiver is a specialized financial product that removes this cost entirely. It allows you to borrow up to 90% of the property value, and in some cases 95% for owner-occupied homes, without the insurance premium. Banks offer this because they recognize the unique value of your professional qualifications. It’s often the most significant discount available to professionals in Australia today. By saving that $24,000 upfront, you can enter the property market years earlier or maintain a larger liquidity buffer for future investments.

The “Low Risk” Advantage for Financial Professionals

Banks aren’t just being generous; they’re following data. They use sophisticated risk-weighting models that show CA and CPA qualified professionals have statistically lower default rates than the general population. Your career stability and high income-earning potential make you a “gold star” borrower in their eyes. This waiver is a strategic risk-mitigation trade-off by the lender. They’re willing to accept a smaller deposit because your professional standing suggests you’re highly likely to meet your repayments over the long term. Since you understand balance sheets and financial planning, lenders view you as a partner in the loan process who is less likely to experience financial distress.

LMI Waiver vs. Low Deposit Home Loans

It’s easy to confuse these waivers with standard low-deposit schemes. Most 5% or 10% deposit loans for the general public come with higher interest rates or “risk fees” that can negate the benefit of a smaller deposit. With an accountant home loan LMI waiver, you typically keep access to standard or even discounted interest rates. You aren’t penalized for having a smaller deposit. We help you find the lenders that offer these unlisted discounts, ensuring your career translates into actual savings. Lenders still look for a clean credit history, though. Even with your professional status, banks expect to see a pristine record of financial responsibility before they’ll waive the LMI requirement. This ensures the professional tier remains exclusive to those with a proven track record of managing their finances well.

Eligibility Criteria: Who Qualifies in 2026?

In 2026, lenders have refined their approach to professional lending. While the core benefit remains the same, the gatekeeping criteria have become more granular. To secure an accountant home loan LMI waiver, you must satisfy three specific pillars: your professional membership, your specific role, and your annual income. Banks are competing for your business, but they’re also looking for evidence that you’re a low-risk, high-value client who fits their specific credit profile.

Recognized Professional Memberships and Roles

Lenders aren’t just looking for anyone with a finance degree. You need to be a current, active member of a recognized body like Chartered Accountants Australia & New Zealand (CA) or Certified Practising Accountant (CPA). Other professions eligible for LMI waivers include Chartered Financial Analysts (CFA) and Fellows of the Institute of Actuaries of Australia (FIAA). If your membership is currently at an “Associate” level or has lapsed, most institutions will likely decline the waiver until you achieve full status. This policy applies to a broad range of finance-heavy roles. Auditors, Chief Financial Officers, Finance Directors, and Financial Controllers all fall under this umbrella. Even specific management roles, such as Finance Managers, can qualify if they hold the right credentials.

Income Requirements and Employment Type

Income is where the 2026 landscape gets interesting. While some lenders require a minimum income of $150,000 in Victoria or New South Wales, other major Australian institutions currently have no minimum income requirement for eligible professionals. Some banks sit in the middle with a $100,000 threshold. For employees, lenders look at standard PAYG slips. However, if you’re a Partner in an accounting firm, the process is different. Banks will look at your profit share and partnership distributions rather than a standard salary. This is a common point of confusion that a mortgage partner at The Home Loan Partners can help clarify by reviewing your specific partnership agreement.

Self-employed accountants typically need two years of tax returns to satisfy standard criteria. If you’ve been in business for less than that, some lenders offer “low-doc” options, though these rarely include the full accountant home loan LMI waiver. It’s also worth noting that if you’re applying with a partner who isn’t an accountant, you can often still qualify for the waiver based on your professional status alone. This flexibility allows many couples to enter the property market sooner by leveraging the higher-earning partner’s career status to bypass the 20% deposit requirement.

Calculating the Savings: LMI Waiver ROI

For a professional who manages balance sheets every day, the return on investment of an accountant home loan LMI waiver is easy to quantify. Lenders Mortgage Insurance is a non-refundable sunk cost that adds zero value to the property. It doesn’t increase your equity, and it doesn’t improve the resale price of your home. Instead, it’s a one-way premium that protects the lender’s risk. By removing this expense, you’re effectively receiving a tax-free cash injection into your property purchase, allowing your capital to work harder elsewhere.

The real benefit lies in the “Opportunity Cost” of your deposit. Without a waiver, you’d likely need a 20% deposit to avoid LMI. On a $1,500,000 property, that’s a $300,000 commitment. With a professional waiver, you can secure the same property with just 10% down, or $150,000. You can then place the remaining $150,000 into an offset account, significantly reducing your interest payments while maintaining total liquidity for future investments or lifestyle goals.

LMI Savings Comparison Table

The table below illustrates the immediate cash savings across common 2026 property price points. These figures are based on a 90% Loan-to-Value Ratio (LVR), where the waiver eliminates the standard insurance premium entirely. It’s important to remember that most lenders “capitalize” LMI, meaning they add it to your loan balance. This results in “Hidden Interest” where you pay interest on the insurance premium for the next 30 years.

| Property Value | Loan Amount (90% LVR) | Estimated LMI Cost (Standard) | Upfront Cash Saved |

|---|---|---|---|

| $800,000 | $720,000 | $19,200 | $19,200 |

| $1,500,000 | $1,350,000 | $36,000 | $36,000 |

| $2,000,000 | $1,800,000 | $48,000 | $48,000 |

Impact on Borrowing Power

An accountant home loan LMI waiver does more than just save you money; it increases your effective purchasing power. By reducing the required deposit from 20% to 10%, you can enter the market years earlier. In a rising market, the capital growth you achieve by buying now rather than waiting to save a larger deposit often far outweighs the cost of the loan itself. For those looking to build an investment property portfolio, this waiver is a powerful tool. It allows you to spread your available capital across multiple deposits rather than tying it all up in a single 20% stake. We help you map out this journey, ensuring your professional status acts as a catalyst for long term wealth creation.

The Application Process: From Professional Status to Approval

Securing an accountant home loan LMI waiver requires more than just a membership card. It’s about presenting a bulletproof case to the right lender. While the process mirrors a standard application, the professional layer adds specific requirements that can make or break your approval. We act as your guide through this journey, ensuring every document is perfectly positioned to trigger the waiver automatically.

The first step involves verifying your professional standing. Lenders won’t just take your word for it; they require formal evidence of your CA or CPA status. Once your identity and credentials are confirmed, we move to income verification. For employees, this means the last two PAYG slips. For partners or those with equity in a firm, we’ll need to demonstrate the stability of your partnership distributions or profit shares. This stage is crucial because the way your income is “packaged” can influence which lender’s professional policy is most favorable for your situation.

After documentation, we help you select a lender that actively seeks accounting professionals. Not every bank offers these waivers, and those that do often change their internal “Professional Lists” without notice. Once a lender is chosen, managing the property valuation becomes the priority. If a valuation comes in lower than the purchase price, your Loan-to-Value Ratio (LVR) might accidentally exceed the 90% threshold, which could void the waiver. We monitor this closely, ensuring the final approval includes a formal confirmation that your LMI is waived entirely.

Required Documentation for Accountants

- A copy of your university degree certificate and your current professional body membership certificate (CA, CPA, CFA, or FIAA).

- Your two most recent Group Certificates or full Tax Returns to verify consistent earning power.

- For firm Partners, a letter from the practice manager or a partnership agreement verifying your equity stake and distribution history.

- Evidence of a “clean” credit history, as professional waivers are reserved for those with high credit scores.

Common Pitfalls to Avoid

- Applying with a lender whose professional policy excludes your specific niche, such as specific types of financial controllers or auditors.

- Inaccurate LVR calculations. Remember that the 90% limit is strict; even being 0.1% over can trigger an insurance premium of tens of thousands of dollars.

- Failing to mention the waiver at the very beginning. It’s much harder to have LMI removed once a standard pre-approval has been issued.

If you’re ready to see which lenders currently offer the most competitive terms for your specific role, contact our expert team today for a tailored assessment of your eligibility.

Partnering with The Home Loan Partners for Your Mortgage

Securing an accountant home loan LMI waiver is a significant financial milestone, but it’s only the beginning of your property journey. While many brokers simply look for the lowest interest rate, we act as your dedicated partner to ensure your mortgage structure supports your long term wealth goals. We provide access to a panel of over 36 lenders. This extensive network includes major banks and boutique lenders who often maintain unlisted professional policies that aren’t available to the general public. We do the heavy lifting by filtering these options to find the specific credit appetite that matches your career trajectory.

Our commitment to your success doesn’t end when you receive your keys. We’ve built our reputation on being a steady hand throughout the entire life of your loan. As your career progresses from a senior associate to a partner, your lending needs will evolve. We’re here to manage those transitions, whether you’re looking at investment property loans or considering refinancing to take advantage of new equity. We prioritize clarity and simplicity, translating complex bank requirements into a seamless experience that respects your time and expertise.

Expert Guidance for Financial Professionals

We speak your language. Our team understands the nuances of complex income structures, including partnership distributions, trust income, and sophisticated tax strategies. You won’t have to explain your balance sheet to us. Instead, we negotiate directly with credit assessors to secure exceptions and ensure your accountant home loan LMI waiver is applied correctly from the start. We’ve helped professionals across Australia navigate these hurdles with a calm, expert approach that removes the inherent stress of the mortgage process. We focus on tailored solutions, such as high-functioning offset accounts and flexible redraw facilities, that allow high earners to manage their cash flow with precision.

Ready to Leverage Your Professional Status?

Your professional accreditation is more than just a certificate on the wall; it’s a powerful financial asset. By starting your application today, you can unlock immediate savings and purchase property with a deposit as low as 10% or 5% without the burden of insurance costs. We invite you to book a confidential strategy session with our expert team to map out your path forward. We’ll review your current standing, verify your eligibility across our 36 lenders, and provide a clear, stress-free roadmap to settlement. Let us partner with you to secure your LMI waiver today and take the first step toward your next property investment with confidence.

Turn Your Professional Accreditation into Property Equity

Your journey to homeownership doesn’t have to be delayed by the slow process of saving a 20% deposit. By leveraging an accountant home loan LMI waiver, you can secure your future today while keeping your hard-earned capital for other investments. You’ve seen how your CA or CPA status can eliminate tens of thousands in insurance costs and provide access to 90% or 95% LVR options that aren’t available to the general public.

As an Australian owned and operated firm, we pride ourselves on being specialist professional waiver experts. We provide you with direct access to over 36 lenders, ensuring we find a partner that understands your specific income structure and career goals. Our team handles the complex negotiations with credit assessors so you can focus on your professional life. Book a Professional Loan Strategy Session with our experts today to unlock the full potential of your career status. We’re ready to guide you through a seamless, stress-free path to your new home.

Frequently Asked Questions

Do all Australian banks offer LMI waivers for accountants?

No, not every lender in Australia provides this benefit. While several major institutions have established professional packages, many smaller banks and credit unions don’t offer an accountant home loan LMI waiver. We actively monitor over 36 lenders to identify those with the most favorable unlisted policies, ensuring you don’t miss out on significant savings by applying with the wrong institution.

Can I get an LMI waiver if I have a 5% deposit as an accountant?

Yes, select lenders in 2026 offer waivers for accountants with a deposit as low as 5%. This 95% Loan-to-Value Ratio (LVR) option is typically reserved for strong applicants with a pristine credit history who are purchasing an owner-occupied property. It’s a significant shift from the traditional 20% deposit requirement, allowing you to secure your home years sooner than the general public.

What is the minimum income required for an accountant to waive LMI in 2026?

Income thresholds vary by lender. Some major Australian institutions have no minimum income requirement for eligible professionals. Others require at least $100,000 per year, while some maintain thresholds between $120,000 and $150,000 depending on your location. At The Home Loan Partners, we help you navigate these differing policies to find the lender that best matches your current salary.

Does the LMI waiver apply to investment properties or just my home?

Most lenders extend these waivers to both owner-occupied residences and investment properties. This flexibility is a powerful advantage for professionals looking to build a property portfolio. By using an accountant home loan LMI waiver for an investment purchase, you can preserve your capital to fund multiple deposits rather than being restricted by the standard 20% equity requirement for each asset.

Is the interest rate higher if the LMI is waived?

No, you won’t be penalized with a higher interest rate for receiving a waiver. In fact, because banks view accountants as low-risk borrowers, you’ll often have access to discounted professional interest rates that are lower than standard retail offers. Unlike generic low-deposit loans that often come with risk fees or higher margins, these professional packages reward your career status with both insurance savings and competitive pricing.

What accounting bodies are recognized for the home loan waiver?

Lenders primarily recognize members of Chartered Accountants Australia & New Zealand (CA) and Certified Practising Accountants (CPA). However, the list of recognized bodies in 2026 also includes the Chartered Financial Analyst Institute (CFA) and the Fellowship of the Institute of Actuaries of Australia (FIAA). You must hold a current, full membership with one of these bodies to satisfy the bank’s professional criteria.

Can I get an LMI waiver if I am a part-time accountant?

Yes, part-time professionals can still qualify as long as they meet the lender’s total annual income threshold. Banks focus on your total earning capacity and professional membership rather than the specific number of hours you work each week. If your part-time salary or partnership distributions meet the $100,000 or $150,000 requirements set by specific banks, you can still enjoy the full benefits of the waiver.

What happens to my LMI waiver if I leave the accounting profession?

The waiver is a one-off benefit applied at the time of your loan’s approval and settlement. If you decide to change careers or leave the accounting profession in the future, the bank won’t retrospectively charge you for Lenders Mortgage Insurance. Your original waiver remains intact for the life of that specific loan, provided you continue to meet your regular mortgage repayments as agreed.