Paying a $43,728 insurance premium just to secure a $1 million property shouldn’t be the price of entry for a medical professional. In 2026, an LMI waiver for doctors is your most powerful financial lever, turning your career stability into immediate market access without the need for a 20% deposit. You’ve spent years working long shifts and focusing on patient outcomes, so it’s frustrating when complex bank policies and rising house prices make homeownership feel like another administrative hurdle to clear.

We’re here to partner with you to simplify this journey. You’ll learn how to bypass Lenders Mortgage Insurance entirely and buy your home with as little as a 5% deposit. This guide previews the latest 2026 lender requirements for AHPRA-registered specialists and explains how to secure loans up to $5 million. We’ve distilled the fine print into a clear path forward, allowing you to focus on your practice while we handle the heavy lifting of your property goals.

Key Takeaways

- Secure your home sooner by leveraging a 5% or 10% deposit without the burden of Lenders Mortgage Insurance premiums.

- Identify if your specific medical profession and AHPRA registration qualify you for a tailored LMI waiver for doctors.

- Maximise your financial leverage by keeping your capital for other investments rather than tying it up in a traditional 20% deposit.

- Navigate the complexities of medical income, including overtime and allowances, to accurately assess your true borrowing power.

- Partner with a specialist broker to compare over 36 lenders and find the policy that best aligns with your long-term career goals.

Breaking the 20% Deposit Barrier: Why LMI Exists and How Doctors Bypass It

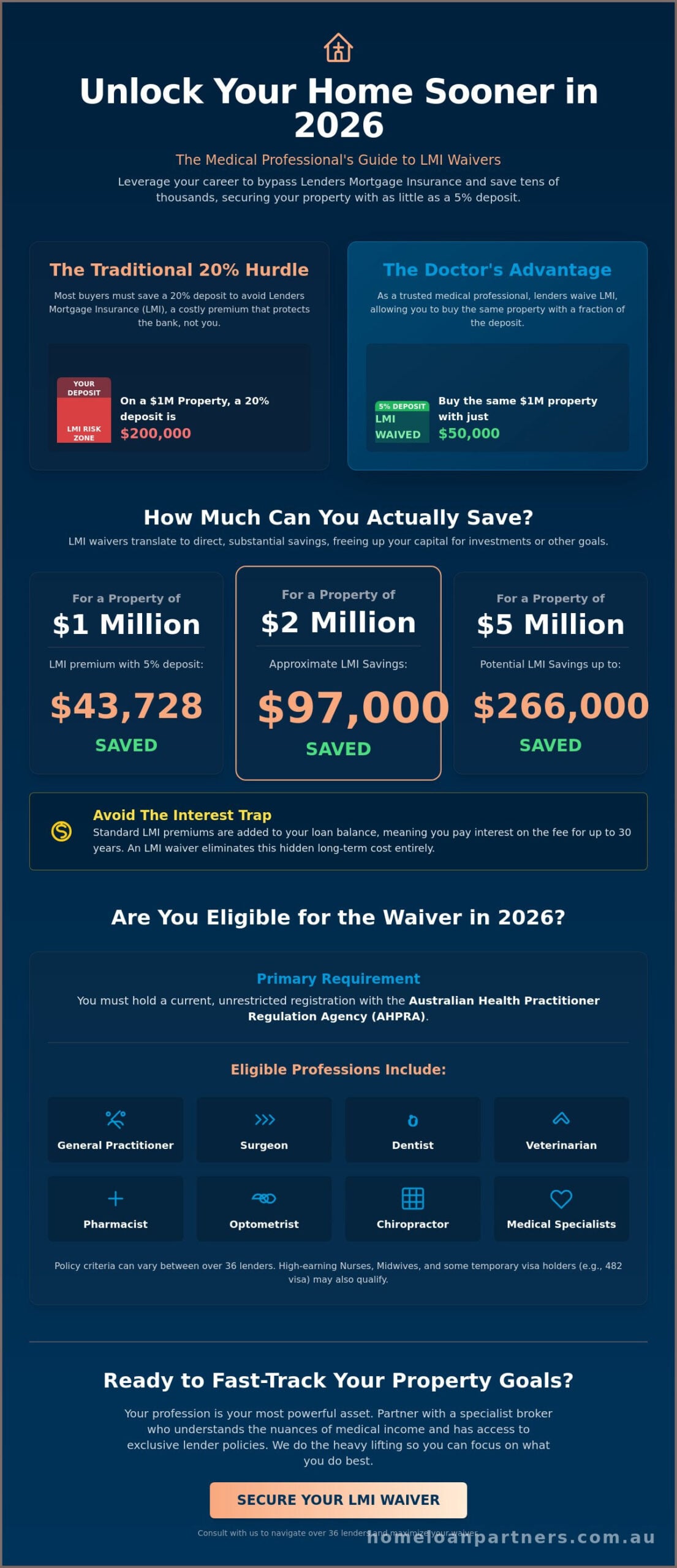

Traditionally, lenders require a 20% deposit to avoid Lenders Mortgage Insurance. This insurance protects the bank if you default on your loan, not you as the borrower. For most Australians, saving $200,000 for a $1 million home is a decade-long struggle that often feels out of reach. However, an LMI waiver for doctors changes this equation entirely. It’s a specialized professional benefit that acknowledges your unique career trajectory and financial reliability. We see this as a way to reward the years of dedication you’ve put into your medical training by removing the most significant hurdle to property ownership.

The Risk Profile of Medical Professionals

Banks view you as a “preferred borrower” because your profession offers unparalleled income stability and career longevity. Data from April 2026 continues to show that medical professionals have historically low mortgage default rates compared to the general public. Because your earning potential is high and consistent, lenders are willing to waive the usual insurance requirements. This trust allows you to enter the property market with as little as a 5% deposit, effectively bypassing the years of aggressive saving that stall other buyers. Your AHPRA registration acts as a golden ticket, signaling to banks that you’re a low-risk investment regardless of your current deposit size.

The Financial Impact of LMI on Your Purchase

The cost of LMI in 2026 is a significant financial burden that adds nothing to your property’s value. For a $1 million property with a 10% deposit, you’d typically pay an estimated $22,644 premium. If you only have a 5% deposit, that figure jumps to approximately $43,728 according to Finder data. These costs are even more staggering as property values rise. On a $2 million home, an LMI waiver for doctors can save you approximately $97,000. For high-end purchases of $5 million, the savings can reach as high as $266,000 as of April 27, 2026.

When you don’t have a waiver, banks usually capitalize this insurance premium into your loan. This means you aren’t just paying the fee; you’re paying interest on that fee for the next 30 years. By securing a waiver, you avoid this long-term interest trap and keep your capital for other purposes. Contrast these two strategies:

- The Traditional Way: Waiting 5 to 7 years to save a 20% deposit while property prices continue to climb.

- The Medical Professional Way: Buying now with a 5% deposit, saving up to $266,000 in insurance costs, and benefiting from immediate capital growth.

We’re here to help you choose the path that builds your wealth faster. Our team acts as your expert partner, ensuring you don’t pay a cent more than necessary to secure your Australian dream.

Eligibility Criteria for Medical Professional LMI Waivers in 2026

Qualifying for an LMI waiver for doctors isn’t just about your job title; it’s about meeting specific lender benchmarks that have evolved significantly as of May 2026. While the Moneysmart definition of LMI explains this insurance as a protection for the lender, banks are increasingly comfortable waiving it for a broad list of medical practitioners. You generally need to be a member of a relevant professional body, such as the Australian Medical Association (AMA), and hold current registration with the Australian Health Practitioner Regulation Agency (AHPRA).

The core list of eligible professions currently includes General Practitioners, Surgeons, Dentists, Veterinarians, Pharmacists, and Optometrists. Some tier-1 lenders have also expanded their policies to include Chiropractors and even high-earning nurses or midwives who earn over $90,000 per year. If you’re a temporary resident on a specific medical visa, such as a 482 or 491 visa, you aren’t automatically excluded. Several lenders offer tailored pathways for overseas-trained doctors, provided you have a pathway to permanent residency and a stable employment contract.

AHPRA Registration and Specialty Requirements

Your AHPRA registration is the primary proof of eligibility that banks use to fast-track your application. Lenders often have “preferred” lists of specialties that receive the most aggressive interest rate discounts alongside the LMI waiver. This includes high-demand roles like Cardiologists, Anaesthetists, and Radiologists. If your niche isn’t on a standard list, don’t worry. We often work with lenders to provide a manual assessment of your career path, ensuring your specific expertise is recognized. You can speak with our expert team to see where your specialty sits within current 2026 lender policies.

Registrars and Junior Doctors: Can You Qualify?

One common misconception is that you need to be a senior consultant to bypass Lenders Mortgage Insurance. This is no longer the case in 2026. Many banks now include interns, residents, and registrars in their waiver programs. Lenders look at your future earning potential rather than just your current base salary. They understand that a registrar’s income will scale rapidly, making you a safe bet for a 95% LVR loan. As long as you have a signed employment contract and your AHPRA registration is active, you can often secure a home loan with a 5% deposit while you’re still in the early stages of your training. This allows you to stop paying rent and start building equity years earlier than your peers in other industries.

The Financial Leverage: How 5% or 10% Deposits Accelerate Property Ownership

Leverage is the strategic tool that transforms a high income into long-term wealth. While the LMI waiver for doctors eliminates a significant upfront cost, its true value lies in the Loan-to-Value Ratio (LVR) flexibility it grants you. Most borrowers are capped at an 80% LVR to avoid insurance. As the Insurance Council of Australia explains LMI, this product usually bridges the gap for lenders when a deposit is small. For medical professionals, banks remove this barrier, allowing you to reach a 95% LVR without the associated penalties. This means you can control a $1.5 million asset with just $75,000 down, rather than waiting to accumulate $300,000.

The opportunity cost of a traditional 20% deposit is often overlooked. If you have $250,000 in savings, placing it all into one property locks that liquidity away. By using an LMI waiver for doctors and opting for a 5% or 10% deposit, you keep a substantial portion of your capital liquid. You can redirect those “saved” funds into high-yield investments, practice equipment, or even use them as a deposit for a second investment property. This approach allows you to build a diversified portfolio much earlier in your career, rather than having your entire net worth tied up in a single primary residence.

Comparing the 20% vs. 5% Deposit Scenarios

The most critical factor in the Australian property market is time. Saving an additional 15% of a property’s value can take three to five years, even on a specialist’s salary. In a market where prices grow at a steady rate, the house you want today for $1.2 million could cost $1.4 million by the time you’ve saved a full 20% deposit. By entering the market now with a 5% deposit, you capture that capital growth immediately. You aren’t just saving on insurance; you’re avoiding the “bracket creep” of the real estate market. This speed to market is often the difference between buying in your preferred suburb today or being priced out of it tomorrow.

Tax Benefits and Investment Strategy

High LVR loans are a sophisticated choice for doctors looking to maximize their tax efficiency. When you borrow 90% or 95% for an investment property, the higher interest repayments can often be used as part of a negative gearing strategy to offset your high taxable income. We always suggest pairing these high LVR loans with an offset account. This allows you to deposit your surgical fees or overtime pay to reduce interest costs daily, while keeping the funds accessible for future tax obligations or personal use. This structure provides the perfect balance of aggressive debt leverage and conservative cash flow management, ensuring your home loan works as hard as you do.

Navigating the Application Process: Documentation and Lender Selection

Applying for an LMI waiver for doctors requires a strategic approach that differs from a standard home loan application. While the financial leverage of a 5% deposit is clear, the execution of your application determines how quickly you can move from the hospital to your new home. We view our role as your expert partner, managing the technical details so you can focus on your patients and your practice without the stress of chasing bank updates.

The process follows five clear steps to ensure a seamless experience. First, we confirm your current AHPRA registration and employment status. Second, we calculate your true borrowing power; this includes properly weighting your overtime, shift allowances, and private practice income, which many standard bank calculators often underestimate. Third, we select a lender whose specific “medical policy” aligns with your specialty. Fourth, we package your application with precision to trigger a fast-tracked approval. Finally, we oversee the settlement and establish an ongoing review process to ensure your loan structure remains optimal as your career advances.

Essential Documentation for Medical Loans

Lenders require specific evidence to grant an LMI waiver for doctors. You’ll need your current AHPRA registration and proof of any specialist college memberships, such as RACS or RANZCOG. If you’re a registrar or a junior doctor, your current and future employment contracts are vital. We also need a clear picture of your existing financial commitments. This includes any HECS/HELP debt or specialized medical equipment finance you’ve taken out for your practice. Having these documents ready allows us to present a “clean” file to the bank, which is the key to securing an approval within days rather than weeks.

Choosing the Right Lender for Your Specialty

Not all banks treat medical professionals equally. Some major lenders have strict caps on loan amounts for certain professions, while others offer “discretionary” waivers for high-net-worth specialists. For example, as of May 2026, some banks are more aggressive in their pursuit of surgeons and anaesthetists, offering them lower interest rates than GPs. Choosing the right lender today also protects your future. We ensure the bank we select for you allows for refinancing flexibility, so you aren’t trapped if you decide to buy an investment property or a private practice premises later. You can book a consultation with our medical loan experts to find the lender that best matches your professional trajectory.

Why Partnering with a Specialist Mortgage Broker Maximises Your Medical Waiver

Choosing a home loan shouldn’t feel like a second job. When you go directly to a major bank, you’re limited to their specific internal criteria and whatever generic rate their banker is authorized to offer that day. We take a different approach. By comparing 36+ lenders, we ensure you aren’t just getting a loan; you’re getting the most competitive LMI waiver for doctors available in the 2026 market. This market-wide view is essential because bank policies change frequently. A lender that was “medical-friendly” last month might have reached its quota for low-deposit loans today.

Translating complex medical income is where a specialist broker truly proves their value. Your pay slip likely includes shift penalties, overtime, and car allowances that standard bank algorithms often ignore or “shade” by 20%. We know how to present this income to credit assessors to ensure your borrowing capacity is fully realized. We act as your advocate, translating the technical language of your employment contract into the practical language that bank credit departments understand. This ensures you aren’t unfairly penalized for the very complexity that comes with a successful medical career.

Access to Exclusive Professional Loan Products

Many of the most competitive medical loans aren’t advertised on billboards or public websites. We maintain direct relationships with specialist medical loan desks at major banks, giving us access to non-public interest rate discounts and flexible terms. These desks understand the high-income trajectory of a specialist or a senior registrar. Beyond the initial purchase, we structure your loan to allow for future equity release. This foresight ensures that when you’re ready to expand your practice or invest in a second property, your original loan doesn’t become a bottleneck. We plan for your 10-year journey, not just your first day in a new home.

The Stress-Free Path to Homeownership

We handle the heavy lifting of the application process while you focus on your patients. You won’t spend hours on hold with a call center or chasing up missing documents. We provide a single point of contact for the entire life of your mortgage, acting as a steady hand through every stage of your financial journey. Our commitment to you doesn’t end at settlement; we provide ongoing reviews to ensure your rate remains competitive as market conditions shift. We do the work. You save lives. Partner with The Home Loan Partners to secure your medical LMI waiver today.

Take Control of Your Financial Future Today

Your medical career has already demanded years of focus and sacrifice. You don’t need to wait another decade to save a 20% deposit while property prices climb. By utilizing an LMI waiver for doctors, you can enter the market today with as little as 5% down and keep your capital for other high-yield investments. Your AHPRA registration is the primary key to bypassing insurance premiums that can reach $266,000 on a $5 million property as of April 2026.

We’re here to act as your trusted guide throughout this entire journey. With access to over 36 lenders and specialized medical loan desks, we’ll find the specific policy that matches your unique income structure and professional goals. From our national service centers across Australia, we handle the heavy lifting so you can stay focused on your patients. You can secure your medical LMI waiver with The Home Loan Partners today. It’s time to turn your professional success into a permanent home.

Frequently Asked Questions

Do registrars and junior doctors qualify for an LMI waiver?

Yes, you can qualify for an LMI waiver for doctors even if you’re an intern, resident, or registrar. Lenders recognize your high future earning potential and the stability of your career path. As long as you hold current AHPRA registration and a signed employment contract, we can help you secure a loan with a 5% deposit while you’re still in the early stages of your training.

What is the maximum LVR a doctor can borrow without paying LMI?

Eligible medical professionals can borrow up to 95% of a property’s value without paying any Lenders Mortgage Insurance. This allows you to enter the market with just a 5% deposit. In some cases with very strict criteria, borrowing up to 100% of the property value is possible, though the 95% threshold is the standard for most major Australian lenders in 2026.

Does a medical LMI waiver mean I pay a higher interest rate?

No, you’ll typically receive a lower interest rate than the general public. Because banks view medical professionals as low-risk borrowers, they offer discounted rates and waived fees alongside the insurance waiver. You aren’t being penalized for a low deposit; you’re being rewarded for your career stability with some of the most competitive terms in the market.

Which medical specialties are eligible for an LMI waiver in 2026?

A broad range of AHPRA-registered practitioners are eligible, including General Practitioners, Surgeons, Dentists, Veterinarians, Pharmacists, and Optometrists. Specialists like Cardiologists and Anaesthetists are also highly sought after by banks. Since March 2024, some lenders have even expanded their policies to include registered nurses and midwives who earn a minimum of $90,000 per year.

Can I get an LMI waiver for an investment property as a doctor?

Yes, many lenders extend the LMI waiver for doctors to investment property purchases. While the lending criteria for investment loans can sometimes be more restrictive than owner-occupied homes, you can still reach a 90% or 95% LVR without the cost of insurance. This makes it much easier to build a property portfolio while you continue your medical practice.

Do I need to be a member of the AMA to get an LMI waiver?

Membership in a professional body like the Australian Medical Association (AMA) is a common requirement for many major banks. However, it isn’t a mandatory rule for every lender in the market. If you aren’t a member, we can guide you toward specific lenders that prioritize your AHPRA registration and income levels over industry body memberships.

What happens if my partner is not a doctor; do we still get the waiver?

You can still receive the waiver as long as the eligible medical professional is a co-borrower on the loan application. Your partner’s income can be used to increase your total borrowing capacity, but the loan is processed under the bank’s specialized medical policy. This is a common way for couples to secure a high-value home together with a smaller deposit.

How much income do I need to earn to qualify for the medical waiver?

While some lenders don’t have a strict income floor for doctors, many tier-1 banks prefer a minimum income of at least $90,000. For example, certain major Australian policies for allied health professionals often require a minimum earnings threshold of $90,000 per year to unlock these specific benefits. We’ll look at your base salary and consistent overtime to ensure you meet the specific requirements of your chosen lender.