According to data from the 2024 ANZ CoreLogic Housing Affordability Report, the time required to save a 20% deposit in NSW has climbed to over 10 years for the average household. You likely feel that the goalposts for homeownership move every time you check the listings, making a six-figure deposit feel like an impossible barrier. It’s natural to feel anxious about how guarantor home loan requirements nsw might impact your family, especially when bank jargon about limited guarantees only adds to the confusion. At Home Loan Partners, we believe your path to homeownership should be a collaborative journey, not a source of stress for your loved ones.

We’ve designed this guide to show you exactly how to secure your property sooner without the burden of Lenders Mortgage Insurance. You’ll discover how to protect your family’s assets while building your own future with confidence. We’ll explore current eligibility criteria, the legal boundaries of a guarantee, and the specific exit strategies you need to release your guarantor as your equity grows in 2026. Our goal is to provide the steady hand you need to make this transition seamless and secure.

Key Takeaways

- Understand how a ‘family pledge’ leverages existing property equity instead of cash to help you navigate the rising median prices in the 2026 NSW market.

- Master the specific guarantor home loan requirements nsw lenders look for, including the essential dual-approval process for both you and your supporting family members.

- Gain peace of mind by learning the hierarchy of lender recourse and how to build a robust exit strategy that protects your family’s long-term financial security.

- Follow a clear, step-by-step path from your initial borrowing power assessment to upfront property valuations for a seamless application experience.

- Discover how partnering with an expert who has access to over 36 lenders ensures you find the right bank ‘appetite’ tailored to your unique family circumstances.

What is a Guarantor Home Loan in NSW for 2026?

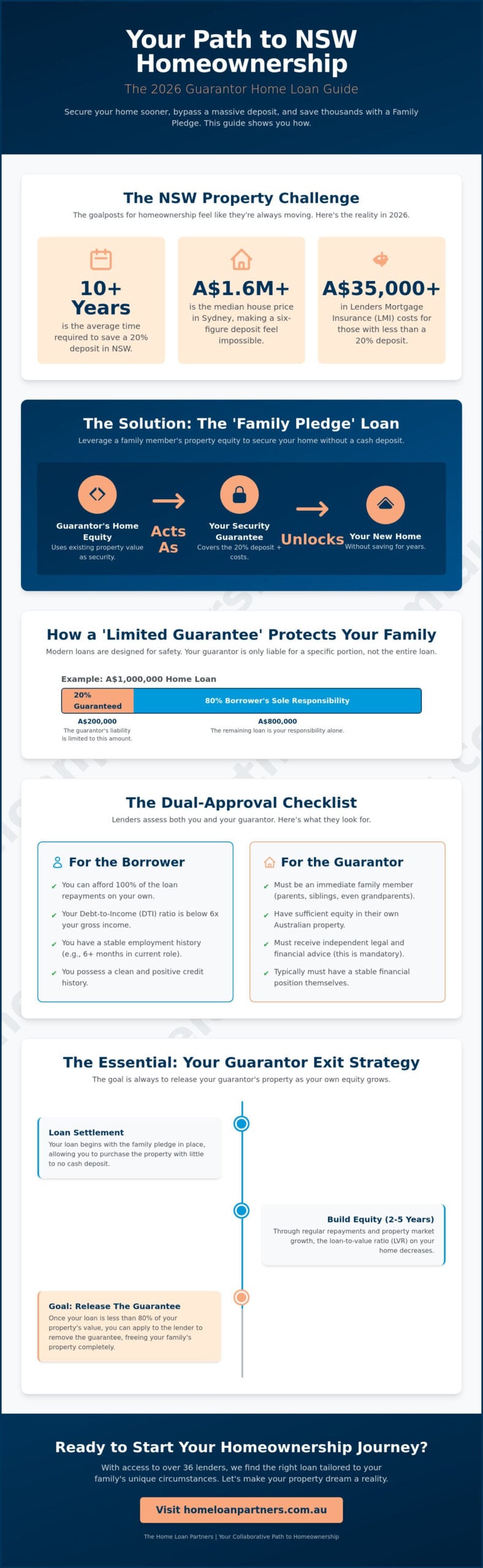

Entering the property market in New South Wales has become a significant milestone that often requires a creative approach. As we move through 2026, the median house price in Sydney remains above A$1.6 million, making a traditional 20% deposit a daunting hurdle for most first-home buyers. A guarantor home loan, often called a ‘family pledge’, offers a practical solution by allowing family members to use the equity in their own home as security. This arrangement helps you meet the guarantor home loan requirements nsw lenders set without needing a massive pile of cash upfront.

To understand the legal foundation of this arrangement, it helps to ask: What is a loan guarantee? In essence, it’s a promise where a third party takes responsibility for a portion of your debt if you can’t pay. However, in the modern NSW mortgage market, your parents aren’t usually ‘giving’ you money. They’re providing a ‘security guarantee’ that covers a specific part of the loan, typically up to 20% of the purchase price plus associated costs like stamp duty. This isn’t a gift of cash; it’s a pledge of property value that acts as a safety net for the bank.

The primary advantage of this path is speed. By using a guarantor, you can bypass the years spent saving while property prices continue to climb. You also avoid Lenders Mortgage Insurance (LMI), which is a significant saving. On a A$1.2 million property, LMI can easily exceed A$35,000. Eliminating this cost means your mortgage starts with more equity and lower monthly repayments. Our role as your partner is to ensure this process feels seamless and transparent for both you and your family.

How the ‘Limited Guarantee’ Protects the Guarantor

Modern lending practices in 2026 prioritize safety for the person providing support. Most guarantees are now ‘limited’, meaning the guarantor is only liable for a specific portion of the loan, usually 20%, rather than the entire debt. This is a critical distinction from a full guarantee. Under Australian legal standards updated in 2025, banks must ensure guarantors receive independent legal advice. This protective layer ensures the family’s primary residence remains secure while still helping the next generation move forward.

The Concept of ‘Family Equity’ in the Current Market

Many NSW parents sit on significant capital growth but don’t have hundreds of thousands in liquid cash to gift. Family equity allows them to leverage that paper wealth. It’s often a superior alternative to a cash gift because it keeps their retirement savings intact. For the borrower, it simplifies the guarantor home loan requirements nsw by replacing a cash deposit with a legal charge over a portion of the parental property. This strategy turns the success of one generation into a stepping stone for the next.

Guarantor Home Loan Requirements: Eligibility for 2026

Securing a home in New South Wales often feels like a team effort. In 2026, meeting the guarantor home loan requirements nsw involves a dual-approval process. This means the lender scrutinizes both your financial health and the guarantor’s assets. It’s a collaborative path where both parties must pass strict criteria to ensure the loan is safe and sustainable.

Lenders typically limit guarantors to immediate family members to ensure there’s a genuine bond. While parents and siblings remain the most common choices, 2026 has seen a significant shift. Approximately 82% of major Australian banks now officially accept grandparents as suitable guarantors, recognizing the role of multi-generational wealth in the current property market.

The most critical factor for you as the borrower is serviceability. You must prove you can afford the full monthly repayments entirely on your own without any financial help from your family. Most lenders now enforce a Debt-to-Income (DTI) ratio limit of 6 times your gross annual earnings. If your total debts, including the new mortgage, exceed this 6x threshold, the application will likely struggle to gain approval even with a strong guarantor behind you.

Borrower Requirements: Income, Credit, and Stability

Lenders look for a steady track record. You’ll generally need at least 6 months of continuous employment with the same employer or 2 years within the same industry if you’re a contractor. A clean credit history is non-negotiable in the 2026 lending environment. Even a single default or multiple missed utility payments in the last 24 months can lead to an automatic rejection. Many buyers worry about the “Genuine Savings” myth. While some banks still prefer a 5% deposit, many now waive this requirement if you can show 12 months of consistent, on-time rental payments in NSW.

Guarantor Requirements: Equity and Financial Standing

Your guarantor needs sufficient “usable equity” in their Australian property. Most banks require them to maintain at least 80% equity in their own home after the guarantee is calculated. Age is another vital consideration. If a guarantor is over 65 or retired, lenders often require proof of a substantial superannuation balance or a clear exit strategy to ensure they aren’t put under financial

stress. Because of the risks of going guarantor, it’s a mandatory requirement for the guarantor to seek independent legal advice (ILA) before settlement. This protects their interests and ensures they understand the full scope of the commitment.

If you’re unsure if your family’s current equity meets these standards, our team can act as your expert partner to provide a clear assessment of your eligibility.

Evaluating Risks and the Essential ‘Guarantor Exit Strategy’

The most common concern we hear from families is the fear of the “worst-case scenario.” You’re likely asking: what happens if life takes an unexpected turn and I can’t make my repayments? It’s a valid worry, but the legal framework in Australia provides a specific hierarchy of recourse to protect all parties. Lenders don’t immediately look to the guarantor’s home. Instead, they must first sell the borrower’s property to recover the debt. The guarantor’s liability is only triggered if the sale of your home doesn’t cover the full loan amount. Understanding these protections and the guarantor home loan requirements nsw lenders enforce helps provide peace of mind for everyone involved.

We view the ‘Exit Strategy’ as a mandatory component of a healthy loan structure, not an optional extra. This strategy is a pre-defined plan to remove the guarantor from the mortgage as soon as it’s financially viable. Beyond the numbers, we recognize the emotional weight these arrangements carry. Transparency is your best tool to mitigate stress. We encourage our clients to hold open family meetings where every “what if” is discussed openly. This proactive approach ensures your property journey strengthens family bonds rather than straining them.

How to Release a Guarantor from the Loan

The 20% equity threshold is the magic number for most Australian banks. Once your loan-to-value ratio (LVR) drops to 80%, you can apply to have the guarantee removed. Meeting the guarantor home loan requirements nsw institutions set involves a clear plan to reach this milestone. You can accelerate this process by making principal top-ups or completing strategic property renovations that add immediate value. In the 2026 NSW market cycle, property re-valuations are essential. If your suburb sees a price increase of 7% or 10%, your equity grows naturally, potentially allowing you to release your parents from the loan years ahead of schedule.

Refinancing as an Exit Path

Refinancing is the most effective way to transition to a standalone loan. When your property value has increased or your loan balance has decreased enough to hit that 80% LVR mark, you can move the debt to a new product entirely in your name. You can rely on natural capital growth, which remains a strong driver in Sydney and regional hubs, or “forced equity” through home improvements. When you’re ready to take full control, refinancing a home loan allows you to restructure your finances and officially release your family’s assets. It’s a significant milestone that marks your full financial independence and protects your guarantor’s long-term security.

The Step-by-Step Application Process in NSW

The journey to homeownership begins with a clear understanding of your financial landscape. We start with a detailed consultation to measure your borrowing power and evaluate your guarantor’s capacity. This ensures the proposed security, often a family home in Sydney or regional NSW, holds enough equity to meet the guarantor home loan requirements nsw. Meeting the guarantor home loan requirements nsw involves more than just having a willing family member; it requires a precise calculation of their remaining mortgage versus their current property value.

By 2026, lenders have streamlined this by ordering upfront valuations on both your potential new home and the guarantor’s property. This proactive step prevents surprises during the final approval stage. We then structure your loan into two parts: a standard 80% portion and a separate portion covered by the guarantee. This specific setup allows you to track the guaranteed amount easily, making it simpler to release the guarantor once your equity reaches 20% through property growth or extra repayments.

Navigating the 2026 ‘First Home Buyer Choice’ is a vital part of this process. In NSW, eligible buyers can choose between a smaller annual property tax or a one-off stamp duty payment on homes up to A$1.5 million. We help you calculate which option saves you more over the first five years of your loan. This decision is integrated directly into your application to ensure your total loan amount accounts for any upfront costs or ongoing liabilities.

The Importance of Independent Legal Advice

Lenders require every guarantor to seek independent legal advice before any documents are signed. This isn’t just a formality. A solicitor will explain the “worst-case scenarios,” such as what happens if the primary borrower defaults. They ensure the guarantor understands their liability is limited to the specific portion agreed upon. In the 2026 lending environment, expect this legal sign-off to take between 3 to 7 business days. It provides a necessary layer of protection for your family members.

From Pre-Approval to Settlement

A guarantor loan approval usually takes 2 to 4 days longer than a standard 20% deposit loan because the bank must assess two different properties. If your guarantor is also refinancing their own mortgage to unlock equity, we manage a “Simultaneous Settlement” to ensure both loans close on the same day. This requires precision. We coordinate with both sets of legal teams to align the dates perfectly. Before the final keys are handed over, we perform a final audit to confirm all NSW-specific grants, like the First Home Owner Grant for new builds, are applied to your balance correctly.

How The Home Loan Partners Secure Your Future

Choosing the right lender is the most critical step in meeting guarantor home loan requirements nsw. While a local branch might offer one or two products, our panel of over 36 lenders provides access to dozens of different guarantor “appetites.” This variety is vital because every bank views risk differently. Some institutions prefer a conservative 20% equity pledge, while others are more flexible with regional NSW property valuations or specific employment types. We filter these options to find the one that treats your family’s security as a priority rather than just a transaction.

Our “Partner” approach means we’re looking out for both the borrower and the guarantor. We recognize that parents are often putting their most valuable asset on the line to help their children. We provide clear, steady guidance to ensure everyone understands the scope of the guarantee. By acting as a buffer between your family and the bank, we translate complex jargon like “limited liability” and “cross-collateralisation” into a clear, stress-free plan that protects your family’s interests.

We don’t just disappear once you get the keys to your new home. Our commitment extends to the long-term journey, specifically focusing on the eventual release of the guarantee. Typically, we aim to remove the guarantor’s liability once your loan-to-value ratio (LVR) drops to 80% through a combination of regular repayments and property capital growth. We monitor your progress and proactively suggest when it’s time to refinance or restructure to give your parents their financial independence back.

Tailored Loan Structures for NSW Families

We design loan structures that work for your specific budget. This includes customising loan splits and setting up offset accounts to maximise your interest savings. For example, placing A$25,000 in an offset account can significantly reduce the interest charged on your balance, helping you pay off the debt years earlier. Our expertise in navigating complex guarantor policies ensures your family remains protected while you build equity at an accelerated pace. We match every structure to your long-term financial goals, whether you plan to renovate or eventually turn the property into an investment.

Start Your Home Ownership Journey Today

First-home buyers often feel overwhelmed by the paperwork and strict criteria of modern lending. You don’t have to manage this process alone. A proactive broker does the heavy lifting by comparing rates, managing the application, and negotiating with credit assessors on your behalf. We take the stress out of the equation so you can focus on finding the right property in the NSW market. Taking that first step with a professional guide ensures your application is right the first time.

Take the Next Step Toward Your NSW Home

Securing a property in the 2026 market demands a clear strategy and a steady hand. By mastering the guarantor home loan requirements nsw lenders expect, you can bypass the hurdle of a 20% deposit and enter the market sooner. We’ve detailed how a professional exit strategy protects your loved ones while leveraging family equity to build your own. It’s about more than just a loan; it’s about creating a safe path to long-term financial security for your entire family.

Home Loan Partners acts as your dedicated expert throughout this journey. We offer access to more than 36 Australian lenders, ensuring you receive a tailored solution rather than a one-size-fits-all product. From the streets of Greenwich to the coast of Port Macquarie, our team understands the nuances of NSW first-home buyer grants and local regulations. We do the heavy lifting by translating complex bank jargon into a clear, manageable plan for your future.

Ready to turn your homeownership goals into a reality? Book a free strategy session with our expert mortgage brokers today. We’re excited to partner with you and help you secure the keys to your new home with confidence and ease.

Frequently Asked Questions

Can my grandparents be my home loan guarantors in NSW?

Yes, most Australian lenders allow grandparents to act as guarantors if they have sufficient equity in their NSW property. While parents are the most common choice, 85% of major banks extend this to grandparents to help family members enter the market sooner. As your partner in this journey, we’ll ensure they understand their obligations before signing any documents to keep the process transparent for everyone.

Does a guarantor need to provide a cash deposit for my home loan?

No, a guarantor doesn’t need to provide a cash deposit or any physical funds. Instead, they use the equity in their own home as security for a portion of your loan. This setup allows you to meet the guarantor home loan requirements nsw without saving a 20% deposit, which can save you A$30,000 or more in upfront costs depending on your purchase price.

What is the maximum LVR allowed on a guarantor home loan in 2026?

In 2026, the maximum Loan-to-Value Ratio (LVR) for a guarantor home loan typically reaches 105%. This covers the full purchase price plus government costs like stamp duty and transfer fees. By borrowing more than the property’s value, you can keep your savings for renovations or an emergency fund. Our experts guide you through the risks to ensure this high LVR remains manageable for your household budget.

What happens to the guarantor if I lose my job and can’t pay the mortgage?

If you can’t make your repayments, the bank first looks to sell your property to recover the debt. If a shortfall remains, the guarantor is legally responsible for the specific amount they guaranteed, which is usually 20% of the original loan. We work closely with you to set up buffers, such as income protection insurance, to protect your family’s assets from these potential risks.

Can I use a guarantor loan if I am buying an investment property?

You can use a guarantor for an investment property, though some lenders limit the maximum loan to 90% or 95% LVR for these scenarios. Approximately 15% of guarantor applications in NSW are currently for investments. It’s a strategic way to build your portfolio faster, but we’ll need to demonstrate a clear repayment strategy to the lender to secure a seamless approval for your investment goals.

How much equity does my guarantor need to have in their own home?

Most lenders require your guarantor to have at least 80% equity in their home after the new guarantee is added. For example, if their home is worth A$1,000,000, their total debt including your guarantee shouldn’t exceed A$800,000. This ensures they have a safe buffer for their own financial security. We’ll perform a quick equity assessment to confirm if your family members meet these specific guarantor home loan requirements nsw.

Are there any extra fees or charges for using a guarantor?

You won’t pay Lenders Mortgage Insurance (LMI), but you should budget for independent legal advice and additional valuation fees. Legal fees for guarantors typically range from A$500 to A$1,500 depending on the solicitor you choose. While these small upfront costs exist, they’re significantly lower than the A$20,000 or more you’d likely pay for LMI on a standard low-deposit loan without a partner’s support.

Can I remove the guarantor from my loan if the property value increases?

You can remove your guarantor once your loan balance drops to 80% of the property’s current market value. This usually happens through a combination of your regular repayments and local property price growth. In NSW, many homeowners reach this milestone within 3 to 5 years of their purchase. We’ll act as your guide during the refinancing process to ensure a smooth transition to a standard loan in your name only.