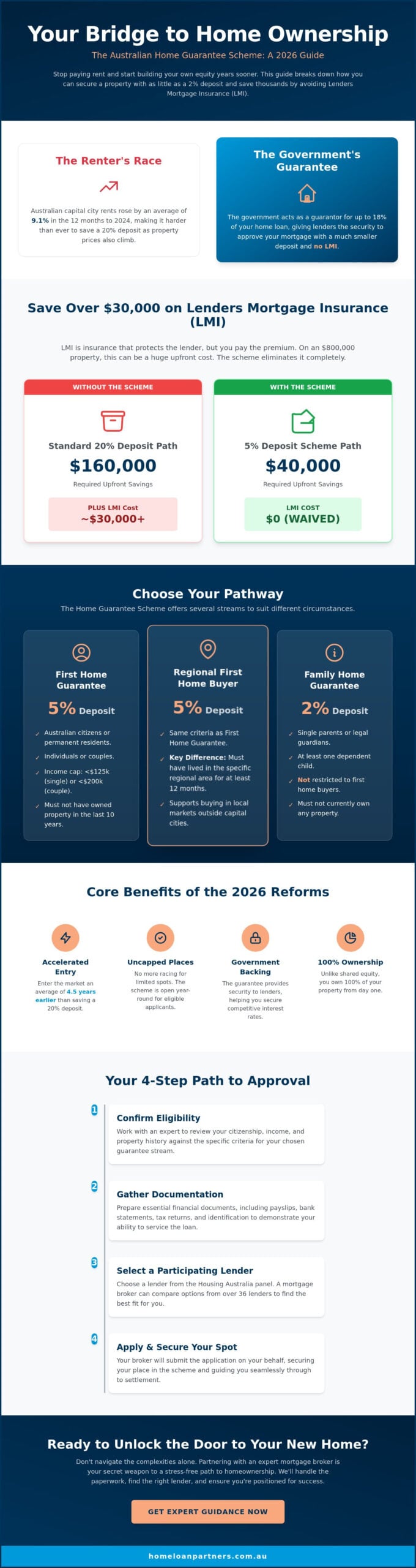

What if you could stop paying your landlord’s mortgage and start building your own equity years earlier than you planned? We understand that saving a traditional 20% deposit feels like a losing race, especially since Australian capital city rents rose by an average of 9.1% in the 12 months leading into 2024. It’s frustrating to watch property prices climb while your savings account struggles to keep pace with the market. The 5 percent deposit home loan scheme offers a genuine bridge to homeownership, allowing you to bypass the massive upfront cost of Lenders Mortgage Insurance and move into your own home sooner.

As your dedicated partner, we’ve designed this guide to help you navigate the expanded 2026 government home guarantee rules with confidence. You’ll learn exactly how to confirm your eligibility for the 5% or 2% deposit streams, ensuring you don’t miss out on the limited annual spots. We provide a clear roadmap that simplifies complex lending criteria and helps you identify a participating lender that fits your specific needs. By the end of this article, you’ll have a stress-free path forward to securing your piece of the Australian dream.

Key Takeaways

- Learn how to secure your first property with just a 5% deposit and save thousands of dollars by completely avoiding Lenders Mortgage Insurance (LMI).

- Identify which government stream fits your needs, including the 5 percent deposit home loan scheme for individuals or the 2% deposit option for single parents.

- Compare the benefits of 100% home ownership under the guarantee model against shared equity programs to determine the best long-term fit for your goals.

- Master the step-by-step application process, from gathering essential financial documentation to selecting the right participating lender from the Housing Australia panel.

- Discover how partnering with an expert mortgage broker can help you navigate 2026 regulations and access over 36 lenders for a seamless path to settlement.

What is the Australian 5 Percent Deposit Home Loan Scheme?

The 5 percent deposit home loan scheme is a federal initiative designed to bridge the gap between renting and owning. By January 2026, the Australian Government expanded this program to address rising property values and the evolving needs of modern buyers. It allows eligible Australians to purchase a property with as little as a 5% deposit. Usually, banks require a 20% deposit to avoid extra fees, but under this scheme, the government acts as a guarantor for the remaining 15%. This support helps you secure a home loan years sooner without the burden of a massive upfront saving goal. We act as your partner throughout this process, ensuring you understand how this guarantee functions as a stepping stone toward your future security.

The History and Evolution of the Home Guarantee

The program began as the First Home Loan Deposit Scheme and has since transitioned into the more inclusive 2026 model. In previous years, limited annual places and strict income caps meant many deserving Australians missed out. The 2026 reforms removed these waitlists and income limits entirely to better support the long-standing tradition of home ownership in Australia. Property price caps were also adjusted on January 1, 2026, to reflect current market conditions. These changes ensure your buying power remains relevant in your local suburb, whether you’re looking at a regional cottage or a city apartment.

Understanding Lenders Mortgage Insurance (LMI) Savings

Lenders Mortgage Insurance (LMI) is a protection for the lender, paid for by the borrower, that the scheme effectively eliminates. When you have less than a 20% deposit, banks typically charge this one-off insurance fee to protect themselves against default. On a A$800,000 property, LMI can often exceed A$30,000. By using the 5 percent deposit home loan scheme, you keep that money in your pocket. This saving doesn’t just reduce your total loan amount; it provides a financial buffer for your first few months of mortgage repayments or helps cover essential moving costs. Our experts guide you through these calculations so you can see the exact impact on your household budget.

The core benefits of the 2026 scheme include:

- Uncapped Places: No more racing against other buyers for a limited number of spots each financial year.

- No Income Limits: Access the scheme regardless of your annual salary, focusing instead on your ability to service the loan.

- Government Backing: The 15% guarantee provides the bank with the security they need to offer you competitive interest rates.

- Accelerated Entry: Most participants enter the market 4.5 years earlier than those saving a full 20% deposit.

Eligibility Criteria: Who Can Access the 2% and 5% Streams?

The path to owning your first home became significantly more accessible in 2026 as the government expanded support through the Housing Australia Home Guarantee Scheme. To qualify for the 5 percent deposit home loan scheme, you must be an Australian citizen or a permanent resident at least 18 years of age. For the First Home Guarantee, individual applicants need an annual taxable income below A$125,000, while couples are capped at a combined A$200,000. These income thresholds ensure the support reaches those who need it most.

Regional buyers have a dedicated pathway too. If you’ve lived in a specific regional area for at least 12 months, the Regional First Home Buyer Guarantee allows you to purchase with the same 5% deposit. This initiative recognizes the unique challenges of local markets outside major capital cities like Sydney and Melbourne. The definition of a first home buyer in 2026 includes anyone who hasn’t owned or had an interest in a property in Australia in the last 10 years. This reset clause helps those who’ve been out of the market for a decade to re-enter with confidence.

The Single Parent and Guardian Stream (2% Deposit)

The Family Home Guarantee is a specialized stream for single parents or legal guardians with at least one dependent child. This program is unique because you don’t necessarily have to be a first-time buyer to qualify. You can access the 2% deposit pathway if you’ve owned property before, provided you don’t currently hold any interest in a home. This property interest divestment rule allows parents to restart their lives after a separation or major life change. It’s a compassionate approach that prioritizes family stability over rigid historical ownership rules.

Property Types and Price Caps in 2026

Your choice of home can range from existing houses and townhouses to apartments and house-and-land packages. However, the property must fall under specific price caps that vary by state. In 2026, the cap for NSW capital cities and regional centers remains at A$900,000, while Victorian urban areas are capped at A$800,000. Queensland’s major centers carry a cap of A$700,000, reflecting the local market conditions across the Sunshine State.

Because these limits can change based on your specific local government area, we recommend using the tool on the official Housing Australia website to check your postcode. Understanding these limits early prevents disappointment during your search. If you’re feeling overwhelmed by the technical requirements, our expert team can help you identify which stream fits your financial profile. We act as your partner throughout this process, ensuring you meet every criteria before you start your property search.

- Eligible Properties: Existing dwellings, off-the-plan apartments, and land with a contract to build.

- Income Verification: Based on the previous financial year’s Notice of Assessment from the ATO.

- Ownership Status: Must intend to be owner-occupiers; investment properties aren’t eligible under this scheme.

5% Deposit Scheme vs. Help to Buy: Which is Right for You?

Choosing between these two paths defines your financial journey for the next 30 years. The 5 percent deposit home loan scheme, technically known as the Home Guarantee Scheme, focuses on 100% ownership. You provide a 5% deposit, and the government guarantees the remaining 15% to your lender. This structure removes the cost of Lenders Mortgage Insurance (LMI), which often saves buyers over A$15,000 on a A$600,000 property. You own the entire home from day one, but you’re also responsible for the full mortgage amount.

Help to Buy operates as a shared equity program rather than a guarantee. It’s a co-purchase arrangement where the government pays for a portion of the home. While your monthly repayments drop because the loan is smaller, you’ll share any future capital growth with the state. Deciding which is right for you depends on whether you value lower monthly costs today or maximum wealth creation tomorrow.

The Pros and Cons of Shared Equity

Shared equity is a powerful tool for those who can’t meet standard borrowing requirements. By reducing the loan size by up to 40% for new builds, it makes homeownership possible in high-cost markets. The trade-off is your equity. You don’t own the whole title. If property values jump by 25% over five years, the government’s share increases in value alongside yours. Many clients prefer the 5 percent deposit home loan scheme because it protects their long-term profit. You keep every cent of the capital gains when you eventually sell or refinance.

Assessing Your Borrowing Power

Your borrowing capacity depends heavily on your debt-to-income (DTI) ratio. Lenders typically look for a DTI below 6 to ensure you can manage repayments safely. Help to Buy significantly lowers your DTI because you’re borrowing a much smaller percentage of the property value. This might be the only viable path if your individual income is below A$90,000 or your household income is under A$120,000. Use our borrowing power calculator to see how these different loan sizes affect your eligibility. A higher deposit usually unlocks better interest rates, but the government guarantee acts as a steady bridge for those who haven’t saved a full 20% yet. We’ll help you compare these options to find the most secure fit for your budget.

How to Apply: The Step-by-Step Path to Approval

Securing your home through the 5 percent deposit home loan scheme is a structured process that rewards preparation. We act as your steady partner, handling the technical heavy lifting so you can focus on finding the right property. The journey begins with a deep dive into your financial health to ensure your application is bank-ready before it reaches the lender’s desk. Our goal is to make the transition from renter to owner as seamless as possible.

- Document Collection: You’ll need your two most recent payslips, three months of bank statements, and your latest Notice of Assessment from the ATO to verify your income.

- Lender Selection: We identify a suitable lender from the official Housing Australia panel that aligns with your specific financial profile.

- Reserving Your Place: Once your lender assesses your basic eligibility, they reserve a place in the scheme for you. These spots are limited each financial year, so timing is a critical factor.

- Securing Pre-approval: This step gives you a clear budget and the confidence to attend auctions or make offers. It’s a protective measure that prevents you from falling in love with a home that sits outside your borrowing capacity.

- Settlement: At the time of your loan settlement, the government guarantee officially activates. This allows you to bypass Lenders Mortgage Insurance (LMI) entirely.

Navigating the 36+ Participating Lenders

The Australian government partners with a specific panel of 36 lenders to deliver this initiative. This panel includes major institutions like Commonwealth Bank and NAB, alongside smaller, community-focused credit unions. While big banks offer high-volume processing, smaller non-bank lenders often provide more tailored solutions for borrowers with unique credit profiles. We help you compare these options to ensure you find a partner that offers both a competitive rate and a policy that fits your lifestyle.

Common Pitfalls to Avoid During Application

Many buyers believe the 5% deposit is the only hurdle, but lenders still look for genuine savings. This usually means showing the bank you’ve held those funds in a personal account for at least 90 days. Additionally, having an income under the A$125,000 individual cap doesn’t guarantee a loan approval. You must still pass serviceability tests. Lenders currently assess your ability to manage repayments at a rate roughly 3% higher than the actual product rate. Finally, be mindful of property price caps. If you bid even A$500 over a regional limit, you will lose your eligibility for the 5 percent deposit home loan scheme instantly.

Our experts are here to guide you through every document and deadline to ensure a stress-free experience. Book a consultation with our team to start your application with a partner you can trust.

Why Partnering with a Mortgage Broker is Your Secret Weapon

The 2026 property market moves fast. While the 5 percent deposit home loan scheme offers a life-changing entry point, the paperwork and government criteria can feel like a maze. This is where we step in. At The Home Loan Partners, we don’t just process applications; we manage the entire bureaucracy so you don’t have to. Our team stays updated on the latest policy shifts to ensure your application meets every requirement the first time.

Choosing the right lender is about more than just the lowest interest rate. We provide you with direct access to a panel of over 36 lenders. This variety allows us to find a loan structure that aligns with your specific financial goals, whether that’s maximizing your offset account or securing the most flexible repayment terms. We take care of the heavy lifting, from the initial document collection to the final negotiations with credit assessors. You stay focused on finding the right property while we handle the back-end logistics.

Our relationship doesn’t end when you get the keys. We view ourselves as your partner for the life of your loan. As your equity grows or market conditions shift, we’ll be there to help you review and refine your strategy. This long-term commitment ensures your mortgage continues to serve your lifestyle as your family or career evolves. We’re here to provide a steady hand, navigating you through a sea of options with patience and precision.

Expert Guidance for First Home Buyers

Banks often use complex jargon that makes the mortgage process feel intimidating. We translate that “bank-speak” into plain English, ensuring you feel confident at every step. Having a professional advocate means you aren’t just another number in a queue. We represent your interests to participating lenders, highlighting the strengths of your application to secure an approval. For more localized advice, read our First Home Buyer’s Guide for more NSW-specific tips.

Ready to Start Your Journey?

The 5 percent deposit home loan scheme remains one of the most effective tools for Australians to bypass the traditional 20% deposit hurdle in 2026. Because these places are often allocated on a first-come, first-served basis, acting while the scheme is accessible is vital. We’re here to provide the steady hand and expert precision you need to secure your future. Book a consultation with The Home Loan Partners today to check your eligibility and take the first step toward your new front door.

Take the Next Step Toward Your Australian Home

Navigating the 2026 property landscape doesn’t have to feel like an uphill battle. By utilizing the 5 percent deposit home loan scheme, you can bypass the years spent saving for a traditional 20% deposit and avoid the costly burden of Lenders Mortgage Insurance. Whether you qualify for the 2% or 5% stream, success relies on understanding your specific eligibility and choosing the right path between government guarantees and shared equity programs.

You don’t need to navigate these complex financial waters alone. Our team provides national service coverage and expert guidance for first home buyers, offering you direct access to a panel of 36+ lenders. We act as your steady partner, translating bank jargon into clear steps so you can focus on finding the right keys. Start your stress-free home ownership journey with The Home Loan Partners. We’re here to help you turn the Australian dream into your daily reality.

Frequently Asked Questions

Is the 5% deposit scheme still available in 2026?

Yes, the 5 percent deposit home loan scheme remains active in 2026 with 35,000 places available through the First Home Guarantee. The Australian Government committed to these annual allocations to help more people enter the market sooner. We’ll help you check the current availability of places, as these spots are often claimed quickly by eager buyers across the country. Our team ensures your application is ready to go the moment you find your home.

Can I use the First Home Super Saver Scheme (FHSS) alongside the 5% deposit scheme?

Yes, you can combine the First Home Super Saver Scheme with the 5 percent deposit home loan scheme to maximize your benefits. The FHSS helps you build your savings faster through tax-effective super contributions, while the guarantee removes the burden of Lenders Mortgage Insurance. Using these together can shave years off your savings timeline, letting you move into your new home much earlier than planned. It’s a powerful combination for any first-time buyer.

What happens if the property I want to buy is over the price cap?

You’ll lose eligibility for the scheme if the property purchase price exceeds the specific caps set by Housing Australia for your region. In 2026, the cap for Sydney is A$900,000 while Brisbane sits at A$700,000. If your chosen property is over the limit, we’ll look at alternative strategies. This might include different loan products or lenders who specialize in low-deposit options for professionals. We’ll guide you through every available path to home ownership.

Do I have to pay back the government’s 15% guarantee later?

You don’t have to pay back the 15% guarantee because it isn’t a cash payment or a second loan. The government simply acts as a guarantor to protect the lender if you default. This support remains until your equity reaches 20% through regular repayments or property value growth. Once you hit that 80% loan-to-value ratio, the guarantee ends without any cost or debt to you. It’s a seamless way to avoid Lenders Mortgage Insurance.

Can permanent residents apply for the 5% deposit home loan scheme?

Yes, permanent residents are eligible for the scheme following the legislative changes that took effect in July 2023. This expansion means you no longer need to be an Australian citizen to access the 5% deposit benefits. You’ll still need to meet the income thresholds of A$125,000 for individuals or A$200,000 for couples. We’ll review your residency documents to ensure your application meets all current criteria. It’s our job to make the process simple and stress-free.

What is the difference between the 5% scheme and the Family Home Guarantee?

The main difference is the required deposit and who the program targets. The standard 5% scheme is for first home buyers or those who haven’t owned property in 10 years. Conversely, the Family Home Guarantee allows eligible single parents to buy with just a 2% deposit. Both options eliminate Lenders Mortgage Insurance, but we’ll help you determine which specific pathway offers the most protection for your family. We’re here to be your expert partner throughout the journey.

Will I get a higher interest rate if I only have a 5% deposit?

You won’t typically pay a higher interest rate when using the government guarantee. Participating lenders generally offer the same competitive products to scheme users as they do to customers with a 20% deposit. This is a significant advantage, as it saves you money on both LMI and monthly interest. As your partner, we’ll compare 32 different lenders to find the most cost-effective rate for your situation. We prioritize your long-term financial security above all else.

How long does it take to get approval for the scheme?

Approval usually takes between 2 to 10 business days once we submit your completed application to a participating lender. Because there are only 35,000 places available each year, timing is everything. We prioritize getting your documents organized early so your application is seamless. This proactive approach helps you secure a place in the scheme and gives you the confidence to bid at auction. We’ll be by your side until you get the keys.