The most expensive mistake you can make in the 2026 property market isn’t buying the wrong house; it’s entering a thirty year commitment without a clear exit strategy. We understand that staring at a mortgage repayment calculator can feel overwhelming when interest rates shift and banks hide fees in the fine print. It’s natural to feel uncertain about whether a fixed or variable rate actually serves your long term goals or if you’re borrowing more than is truly safe for your family’s future.

We’ll show you how to turn those basic numbers into a professional property strategy that accounts for A$15 monthly service fees and potential rate fluctuations. You’ll gain the confidence to set a monthly budget that protects your lifestyle while discovering how an extra A$100 per month could shave four years off your loan term. You deserve clarity. This guide breaks down the essential steps to mastering your home loan costs and securing your financial future with a plan tailored specifically to your needs.

Key Takeaways

- Understand why 2026 is the year of the ‘informed borrower’ and how to set a firm foundation for your Australian property goals.

- Master our mortgage repayment calculator to project accurate monthly costs based on current Australian market interest rates and your specific loan amount.

- Discover how your deposit size and Loan-to-Value Ratio (LVR) directly influence the interest rate you are offered and the overall cost of your loan.

- Learn the crucial difference between simple repayment estimates and bank serviceability to ensure your home ownership journey remains seamless and stress-free.

- Transform a basic calculation into a tailored home loan strategy by partnering with experts who navigate over 30 lenders to find your ‘true’ best rate.

Navigating Your Home Ownership Journey with a Mortgage Repayment Calculator

A mortgage repayment calculator is a digital compass designed to guide you through the complexities of home finance. It functions as a specialized financial tool that estimates your weekly, fortnightly, or monthly loan costs by processing your total principal amount alongside current interest rates. As we approach 2026, the Australian property market demands a new level of precision. The era of the “Informed Borrower” has arrived, where success depends on data rather than guesswork. By using these tools, you transform vague aspirations into a concrete financial blueprint.

Seeing your financial future in black and white provides a powerful psychological anchor. It replaces the “what-ifs” of lending with hard numbers, allowing you to breathe easier as you plan your next move. Whether you’re a first-time buyer or looking to refinance an existing property, this data serves as the bedrock of your strategy. We view ourselves as your partner in this process, ensuring you have the steady expertise needed to make decisions with absolute confidence.

Why Estimating Your Repayments is Step One

Validating your budget is the most critical task before you step foot into an open home. It’s easy to fall in love with a property, but it’s much harder to manage a budget that doesn’t fit your lifestyle. Consider the impact of a 0.25% interest rate change; on a A$600,000 loan over 30 years, this small shift can add roughly A$100 to your monthly commitment. Using a mortgage repayment calculator allows you to stress-test your finances against these fluctuations. This proactive approach ensures your property search remains grounded in reality, helping you target homes that align with your long-term security.

Beyond the Numbers: The Psychology of Budgeting

Mortgage stress often stems from a lack of clarity. When you engage in proactive planning, you significantly reduce the anxiety associated with large-scale debt. Clarity empowers you during intense price negotiations or auctions. You won’t be swayed by the heat of the moment because you already know your limit. This shift in mindset is profound; you move from asking “Can I afford this?” to “How do I optimize this?”. By focusing on optimization, you can explore how offset accounts or extra repayments might shave years off your loan term. This sense of control turns the home-buying process from a stressful transaction into a rewarding personal milestone.

How to Use a Mortgage Calculator for Accurate 2026 Projections

Using a mortgage repayment calculator effectively isn’t just about finding a single number; it’s about stress-testing your financial future. To get a clear picture of your 2026 commitments, you should follow a structured approach that mirrors how Australian banks assess your application.

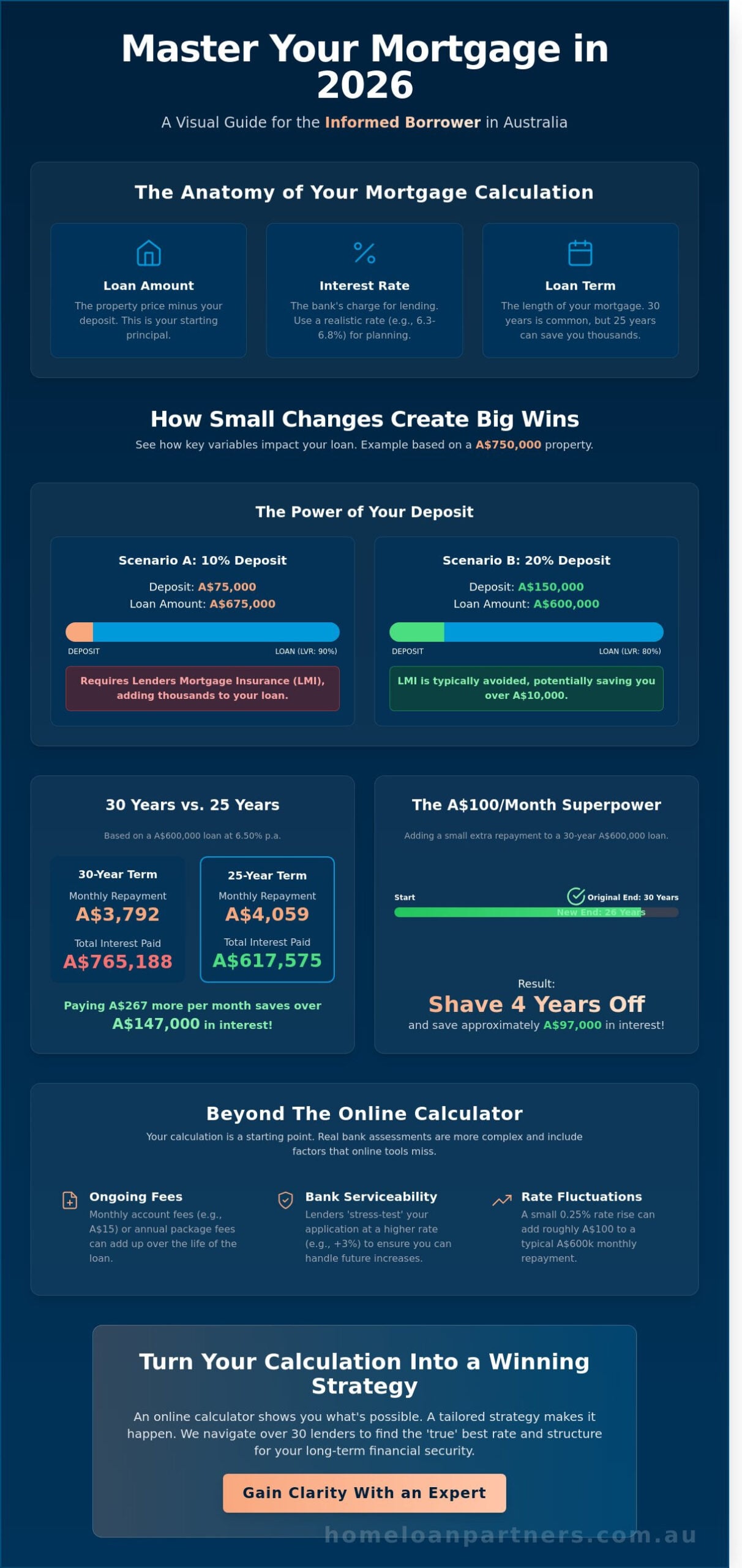

- Step 1: Input your total loan amount. Ensure you subtract your deposit from the total purchase price first. If your deposit is less than 20%, remember to include any capitalized Lenders Mortgage Insurance (LMI) in this total.

- Step 2: Select a realistic interest rate. While you might see “headline” rates around 5.99%, using the current market average for variable loans, which sits between 6.30% and 6.80% as of late 2024, provides a safer baseline for your 2026 planning.

- Step 3: Choose your loan term. Most Australian borrowers opt for a 30-year term to maximize cash flow, but you should also test a 25-year term to see how much interest you could save.

- Step 4: Adjust your repayment frequency. You can choose between weekly, fortnightly, or monthly cycles. Matching this to your salary schedule helps you stay organized without feeling the pinch.

- Step 5: Factor in extra repayments. Even small, consistent additions of A$50 or A$100 can drastically alter your loan’s trajectory.

Small adjustments to these inputs today can prevent significant financial hurdles tomorrow. If you’re unsure which figures apply to your specific situation, our team can help you build a tailored home loan strategy that fits your goals.

Inputting the Right Data: Loan Amount and Terms

Accuracy starts with your loan principal, not the property’s sticker price. For example, on a A$750,000 home with a A$150,000 deposit, your mortgage repayment calculator inputs should reflect the A$600,000 balance. The term you choose also dictates your total interest cost. On a A$600,000 loan at 6.5%, a 30-year term results in approximately A$765,000 in total interest. Shaving that term down to 20 years increases monthly payments but slashes that interest bill by nearly A$300,000. Always include a 3% “buffer” rate in your calculations to mirror the serviceability standards set by APRA, ensuring you can still afford the home if rates rise by 2026.

Understanding Frequency: Weekly vs Fortnightly vs Monthly

Aligning your mortgage with your income stream creates a seamless cash flow that reduces the manual stress of budgeting. While monthly payments are the standard, switching to fortnightly payments is a proven strategy for paying off a loan faster. By paying half the monthly amount every two weeks, you effectively make an extra month’s payment every year without noticing the difference in your pocket. This works because 26 fortnights equals 13 months of repayments. Over a standard 30-year term, this simple shift can shave four to five years off your mortgage and save you tens of thousands in interest charges.

The Anatomy of a Repayment: Principal, Interest, and Fees

Every dollar you send to your lender has a specific job to do. When you look at your monthly statement, the total figure can feel like a single, large expense, but it’s actually a combination of three distinct parts. Your payment covers the interest charged by the bank, a portion of the original amount you borrowed, and any ongoing service fees. Understanding this breakdown helps you take control of your financial future and ensures you aren’t caught off guard by changing costs.

Most Australian home loans use a structured schedule where interest is calculated on the remaining balance every day. Because your debt is highest at the start of your 30 year journey, your initial payments are heavily weighted toward interest. A mortgage repayment calculator is a vital tool here. It allows you to see exactly how much of your A$3,500 monthly payment is actually reducing your debt versus simply paying the bank for the privilege of the loan.

Principal vs. Interest: How Your Debt Shrinks Over Time

Progress often feels slow during the first five to seven years of a mortgage. This is due to the amortization curve. On a A$600,000 loan at a 6.25% interest rate, roughly 80% of your repayments in the first year go toward interest. We want to help you shift that balance sooner. By making small, consistent extra payments of just A$150 a month, you can shave years off your loan term and save tens of thousands in interest costs.

If you start with an interest-only period, which is common for investors, remember that your principal doesn’t move. Once that period ends, usually after 5 years, your repayments will jump significantly because you must now pay back the full principal over a shorter remaining timeframe. Using a mortgage repayment calculator helps you model these future “repayment shocks” so you can transition smoothly without stress.

Factoring in the ‘Hidden’ Costs of Borrowing

The interest rate isn’t the only number that matters for your budget. Many Australians forget to include Lenders Mortgage Insurance (LMI) if their deposit is less than 20%. For a A$700,000 property with a 10% deposit, LMI can add over A$12,000 to your total loan cost. While this is often capitalized into the loan, it increases your monthly commitment.

- Annual Package Fees: Many “pro-pack” loans charge between A$350 and A$395 annually for features like offset accounts.

- Monthly Service Fees: Some no-frills loans charge A$10 to A$15 a month just to maintain the account.

- The Comparison Rate: This is your most honest guide. It’s a legal requirement in Australia for lenders to show this rate, which includes the interest plus most fees.

We always recommend looking at the comparison rate rather than the advertised “headline” rate. If a bank offers a 5.99% rate but the comparison rate is 6.30%, those hidden fees are costing you significantly over the life of the loan. Our goal as your partner is to ensure the loan structure we choose together aligns with your actual cash flow, keeping your path to homeownership clear and predictable.

Why Your Online Calculator Result Might Not Be the Whole Story

A mortgage repayment calculator is a fantastic starting point for your property journey. It helps you visualize your future budget and provides a sense of control. However, these digital tools often rely on “perfect world” assumptions. In the actual 2026 lending market, your final approval involves human variables and complex bank policies that a simple algorithm can’t capture. It’s the difference between a rough sketch and a finished architectural plan.

The Difference Between Advertised and Actual Rates

Most lenders in Australia use tiered pricing models. This means the headline rate you see online is usually reserved for the lowest-risk borrowers. Your deposit size is the biggest factor here. If you have a 20% deposit, you’ll likely unlock “gold-tier” rates. For instance, a borrower with a 20% deposit might be offered a rate of 5.74%, while a buyer with a 5% deposit could face 6.19% plus the added cost of Lenders Mortgage Insurance (LMI). As of late 2024, data showed that the gap between “advertised” and “negotiated” rates could be as wide as 0.50%. We take the guesswork out of this by shopping your specific profile across multiple lenders to find the actual floor rate available to you.

Why Serviceability and LVR Change Everything

The Loan-to-Value Ratio (LVR) is how banks measure their risk. If your LVR is high, your interest rate usually follows suit. But even with a great deposit, you must pass the serviceability test. APRA currently requires banks to apply a 3% “serviceability buffer” on top of the actual interest rate. If your loan rate is 6%, the bank tests if you can still pay at 9%. They also use the Household Expenditure Measure (HEM) to estimate your living costs. Even if you live a frugal lifestyle, the bank might benchmark your monthly expenses at A$3,800 for a family of four, regardless of your actual bank statements.

Your credit score will also play a more significant role in 2026. With Comprehensive Credit Reporting (CCR) now standard, lenders see every late phone bill or high credit card limit. For self-employed borrowers or those with commission-based income, generic calculators fail to account for how different banks “shade” or discount certain income types. One bank might take 100% of your overtime, while another only takes 80%. This is where having a partner to guide you makes the difference between a “no” and a “yes.”

Don’t rely on generic estimates when planning your future. Speak with a Home Loan Partners expert to get a tailored assessment of your true borrowing capacity.

Turning Your Calculation into a Tailored Home Loan Strategy

Using a mortgage repayment calculator provides a vital baseline for your property journey. It helps you visualize your monthly commitments and understand how interest rate changes might impact your cash flow. However, a digital tool cannot account for the nuanced lending criteria of 2026 or the individual complexities of your financial profile. Moving from a DIY calculation to a professional strategy is the most effective way to ensure your home loan remains an asset rather than a burden.

The Australian lending market is dynamic. While a bank might offer an attractive headline rate, the true cost of a loan involves annual fees, valuation costs, and discharge charges. We look beyond the surface to find a loan that fits your life. Our team analyzes 36+ different lenders to identify products that align with your specific risk profile and long-term wealth goals. This professional oversight often uncovers opportunities that a simple online search would miss.

A strategic loan structure often relies on smart features like offset accounts and redraw facilities. These are not just administrative add-ons; they are powerful interest-saving tools. For example, keeping A$30,000 in an offset account against a A$550,000 mortgage can potentially save you over A$95,000 in interest over the life of a 30-year loan. We help you use these facilities to maximize your liquidity while minimizing your interest bill.

The biggest mistake homeowners will make in 2026 is the “set and forget” approach. Data from the 2024-2025 financial year indicated that borrowers who failed to review their loans every 18 months paid an average of 0.85% more in interest than those who proactively refinanced. We ensure you don’t pay a “loyalty tax” to your bank by conducting regular health checks on your mortgage.

How The Home Loan Partners Bridge the Gap

We do the heavy lifting by comparing 36+ lenders on your behalf. This saves you dozens of hours of research and prevents unnecessary credit enquiries that could damage your credit score. Our experts tailor loan structures to your specific goals, whether you’re a first-home buyer seeking a low-deposit entry or an investor looking to maximize tax benefits. We act as your Trusted Guide, providing a steady hand from the moment you receive pre-approval until the day you pick up your keys and beyond.

Your Next Steps Toward Settlement

The results from your mortgage repayment calculator are the perfect starting point for a formal borrowing power assessment. This assessment provides a concrete figure of what Australian banks will actually lend you based on current 2026 serviceability buffers. To ensure a seamless application experience, start gathering your two most recent payslips and your most recent group certificate. Having these documents ready allows us to move quickly when you find the right property.

Take the Next Step Toward Your 2026 Home Ownership Goals

A mortgage repayment calculator is a vital starting point to help you visualize your monthly commitments. You’ve seen how principal and interest components shift over time and why basic online estimates often miss local variables like specific bank fees or fluctuating A$ interest rates. While a digital tool provides the raw data, your long-term security depends on a strategy that prepares for the 2026 economic landscape. Moving from a rough estimate to a concrete plan requires professional insight that looks beyond the screen.

At Home Loan Partners, we act as your steady guide through the complex Australian lending market. We provide access to a panel of over 36 lenders to ensure your loan remains truly competitive. Our team offers expert, unbiased advice tailored to your unique financial situation; we provide dedicated support during the application and for the entire life of your loan. We don’t just find you a rate. We build a partnership that protects your home ownership dream.

Get a tailored mortgage strategy from The Home Loan Partners today. We’re ready to help you navigate the journey with confidence and ease.

Frequently Asked Questions

How accurate are mortgage repayment calculators?

A mortgage repayment calculator provides a highly reliable estimate based on the specific interest rate and loan term you enter. While these tools are accurate for principal and interest figures, they don’t account for individual credit scores or specific lender credit policies. You should treat the results as a professional guide that helps you understand your baseline commitments before we dive into the finer details of your application.

Does an offset account reduce my monthly mortgage repayments?

No, an offset account typically reduces the interest you’re charged rather than lowering your required monthly repayment amount. If you hold A$40,000 in an offset account against a A$400,000 loan, the bank only charges interest on A$360,000. While your monthly payment stays the same, a larger portion of that money pays down your actual debt, which can shorten your loan term by several years.

What is the difference between principal and interest and interest-only repayments?

Principal and interest repayments cover both the borrowed amount and the cost of borrowing, ensuring you eventually own your home outright. Interest-only payments only cover the monthly interest charges, meaning your original loan balance of A$550,000 remains exactly the same after five years. Most Australian owner-occupiers choose principal and interest to build equity, while investors often use interest-only periods to manage short-term cash flow.

How much extra should I pay to shave 5 years off my mortgage?

On a A$600,000 loan with a 6.10% interest rate over 30 years, paying an extra A$465 per month will shave exactly five years off your mortgage. This strategy saves you approximately A$152,000 in total interest costs over the life of the loan. Using a mortgage repayment calculator allows you to test different scenarios to see how small, consistent contributions can accelerate your path to total homeownership.

Will my repayments change if interest rates go up in 2026?

Yes, your monthly costs will rise if you’re on a variable rate or if your fixed-rate term expires during 2026. For every 0.25% increase on a A$500,000 loan, your monthly repayment increases by roughly A$82. We help you stress-test your budget against these potential 2026 market shifts so you can feel secure that your lifestyle remains protected even if the economic environment changes.

Can I use a mortgage calculator for investment property loans?

You can certainly use these tools for investment planning, though you must account for the higher interest rates typically applied to non-owner-occupied loans. Investment rates in the current Australian market are often 0.45% higher than standard residential rates. It’s also vital to factor in your expected rental yield, as 75% of your gross rental income is usually considered by lenders when they calculate your borrowing capacity.

What fees should I add to my calculation for a realistic estimate?

You should include a monthly service fee of A$12 to A$15 and an annual package fee, which commonly costs A$395 for most major Australian bank products. Beyond the loan itself, remember to budget for upfront costs like NSW or VIC stamp duty, which can exceed A$35,000 on a A$750,000 property. Including these concrete figures ensures your financial plan is a realistic roadmap rather than a best-case estimate.

Is it better to pay my mortgage weekly or monthly?

Paying weekly or fortnightly is generally better because it aligns with how interest is calculated daily by Australian lenders. By making fortnightly payments that equal half of a monthly payment, you effectively make 13 full monthly payments every year. This simple adjustment can reduce a 30-year mortgage by 4.2 years and save you tens of thousands of dollars without requiring a major change to your lifestyle.