Could your current lender be charging you a “loyalty tax” simply because you’re worried about the paperwork or hidden exit fees? You’ve likely felt the squeeze on your monthly cash flow as interest rates shifted throughout 2025. It’s common to feel overwhelmed by the choice between offset accounts and redraw facilities, especially when you’re searching for a home loan refinance Port Macquarie residents can actually understand. We know that the fear of making the wrong move often keeps homeowners stuck in outdated contracts, even though switching could save the average household over A$3,800 in annual interest charges.

This 2026 buyer’s guide will show you how to secure a more competitive rate and a structure that grows with your family. We’ll explore how to access your equity for renovations and eliminate the stress of hidden costs by partnering with an expert who puts your security first. We’ll break down the exact steps to transition into a flexible loan that supports your long-term Australian dream without the usual banking jargon.

Key Takeaways

- Identify how to avoid the “loyalty tax” by replacing your current mortgage with a structure that prioritises your long-term financial security.

- Learn to evaluate the total cost of ownership beyond just interest rates, focusing on lender features and digital capabilities that offer real flexibility.

- Discover how to calculate a clear return on investment by weighing switching costs, such as discharge fees, against your potential long-term savings.

- Prepare for a seamless home loan refinance Port Macquarie by understanding the latest serviceability buffers and documentation required for a stress-free approval.

- Understand how the Best Interests Duty (BID) ensures your broker acts as a dedicated partner, doing the heavy lifting to secure a loan that fits your unique goals.

Why Consider a Home Loan Refinance in Port Macquarie and Across Australia?

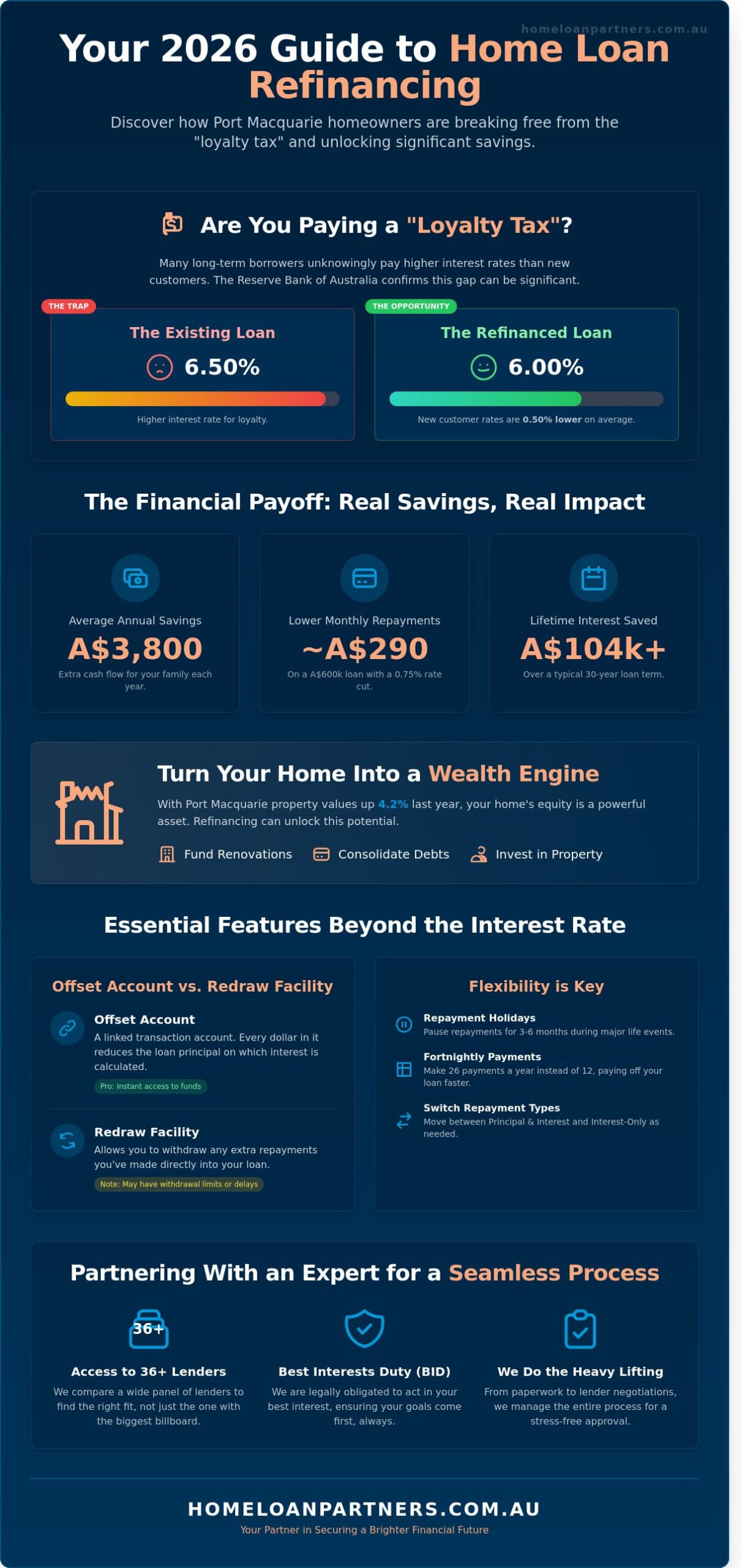

Choosing a home loan refinance Port Macquarie involves replacing your current mortgage with a new one, either through your existing bank or a different lender. To understand the basics, what is refinancing? It’s a strategic move to secure better terms and lower your costs. Many Australians stay with the same bank for years, unknowingly paying a “loyalty tax.” Reserve Bank of Australia data indicates that long-term borrowers often pay interest rates 0.50% higher than those offered to new customers. In 2026, the primary triggers for this shift include changes in market interest rates, growth in property equity, or shifts in your personal life stages. Your goal is simple: reduce interest costs while making your loan work harder for your family.

The Financial Benefits of Moving Your Mortgage

A lower interest rate creates immediate breathing room in your household budget. For a typical A$600,000 mortgage, a rate reduction of just 0.75% can lower your monthly repayments by approximately A$290. This adds up to over A$104,000 in saved interest over a 30-year loan term. You can also use this process to consolidate high-interest debts. Rolling a A$30,000 car loan with a 9% interest rate into a 6% mortgage reduces your total monthly commitments. It simplifies your finances into one single, manageable payment while clearing expensive debt faster.

Refinancing as a Wealth Creation Tool

Equity is the difference between current market value and the remaining loan balance. As Port Macquarie property values rose by an average of 4.2% over the last 12 months, many locals have found themselves sitting on a goldmine of untapped potential. You can use this equity as a deposit for an investment property or to fund a major home renovation. It’s a cornerstone of a long-term property portfolio strategy. We act as your partner to ensure your loan structure supports these big-picture goals. A well-timed refinance transforms your home from a simple residence into a powerful engine for building future security and long-term wealth.

Essential Features to Evaluate for Your New Mortgage

When you consider a home loan refinance Port Macquarie, the headline interest rate is only one piece of the puzzle. You need to look at the total cost of ownership. This includes annual service fees, discharge costs from your current bank, and any upfront application charges. In 2026, the speed of technology matters just as much as the rate. Some lenders now offer 48-hour approval turnarounds and sophisticated mobile apps, while legacy banks might still take 22 days to process a simple application. We believe a tailored loan structure provides more long-term security than a generic, one-size-fits-all product. By accessing our panel of 36+ lenders, we help you identify the specific features that actually save you money over the life of your debt.

Offset Accounts vs. Redraw Facilities

An offset account is a standard transaction account linked directly to your mortgage. Every dollar you keep in this account reduces the interest charged on your loan balance. For example, if you have a A$600,000 mortgage and A$40,000 in your offset, the bank only charges interest on A$560,000. This is a powerful tool for those who want instant access to their cash for daily expenses. A redraw facility allows you to pull back any extra payments you’ve made into the loan itself. While often cheaper in terms of annual fees, redraw facilities can sometimes have restrictions on how quickly you can move the money. Before switching home loans, it’s vital to decide which mechanism fits your monthly cash flow habits.

Flexible Repayment Options

Your financial situation won’t stay the same for 30 years. That’s why flexibility is a core requirement for any modern mortgage. Look for lenders that allow you to switch between principal-and-interest and interest-only repayments if your circumstances change. Many of our clients value “repayment holidays,” which provide a 3 to 6-month buffer during major life events like career changes or parental leave. Small adjustments, such as switching from monthly to fortnightly payments, can also shave years off your loan term because interest is calculated daily. We can partner with you to model these different scenarios, ensuring your home loan refinance Port Macquarie acts as a safety net rather than a source of stress. These structural choices often provide more financial freedom than a minor 0.10% difference in the interest rate.

Calculating the Real Cost of a Home Loan Refinance

Switching your mortgage isn’t a free process. To ensure a home loan refinance Port Macquarie actually puts money back in your pocket, we need to perform a precise return on investment analysis. While a lower interest rate looks attractive on a billboard, the upfront exit and entry fees determine whether the move is truly beneficial for your family’s future security. We look past the headline rates to find the genuine value in every offer.

Understanding Discharge and Break Costs

Your current lender will charge a discharge fee to close your mortgage and release the property title. Most Australian banks set this fee between A$200 and A$600 per loan account. If you’re currently on a fixed-rate term, you may also face break costs. These are calculated based on how much wholesale interest rates have moved since you signed your contract. If rates have fallen significantly, these costs can reach several thousand dollars. We always recommend requesting an official payout figure from your bank to get exact data. For a clearer picture of these potential hurdles, ASIC’s guide to switching home loans offers tools to help you estimate these expenses accurately.

Upfront Fees vs. Long-term Savings

The new lender will have their own set of requirements. You’ll likely encounter application fees ranging from A$0 to A$600 and property valuation fees that typically cost between A$200 and A$500. There are also government charges, such as the NSW mortgage registration fee, which is currently A$165.40. We help you calculate the “break-even point” to see how quickly your monthly savings cover these costs. Consider this scenario:

- Total switching costs: A$1,200

- Monthly interest savings: A$240

- Break-even point: 5 months

If you plan to stay in your home for several years, a five-month recovery period is an excellent result. Be cautious of large cashback offers, which often range from A$2,000 to A$4,000. While they provide an immediate boost, they shouldn’t distract you from the underlying interest rate. A slightly higher rate can cost you far more than the initial cashback amount over the life of the loan. Our goal is to find a home loan refinance Port Macquarie that prioritizes your long-term wealth. We focus on the total cost of the loan over the next five years to ensure you’re truly moving forward with confidence.

A Practical Checklist for a Seamless Refinancing Process

Preparation pays off. A successful home loan refinance Port Macquarie depends on how well you present your financial story to a new lender. Banks currently apply a 3% serviceability buffer above the offered interest rate to test your repayment capacity. If your new rate sits at 5.75%, the lender evaluates your income as if the rate were 8.75%. This safeguard ensures you remain secure even if market conditions shift.

A clean credit history is your greatest asset. Lenders look for 100% on-time payment records over the last six months. We act as your expert partner to review your credit file and employment stability before any paperwork hits a bank desk. This proactive approach prevents unnecessary rejections that could lower your credit score.

Document Preparation: What You Need

Lenders require a clear snapshot of your current financial health. You should gather your two most recent payslips, your latest Group Certificate, and six months of mortgage statements. If you’re self-employed, have your last two years of ATO tax assessments ready. Modern regulations require “proof of living expenses,” which means banks will look at your digital transaction history to categorize spending. Organizing these files in a secure digital folder can reduce your application processing time by up to 72 hours.

- Income: Recent payslips or ABN-related tax returns.

- Liabilities: Statements for credit cards, car loans, or HECS debts.

- Expenses: A realistic summary of monthly grocery, utility, and leisure costs.

The Application and Valuation Stage

The property valuation is a pivotal moment because it dictates your Loan-to-Value Ratio (LVR). If your LVR is 80% or lower, you avoid the cost of Lenders Mortgage Insurance, which can save you over A$12,000 on a standard A$800,000 Port Macquarie property. The journey from initial application to formal settlement typically takes between 20 and 45 days. To help the process, ensure your home is well-presented for a physical valuation; simple tasks like mowing the lawn or finishing minor repairs can positively influence the valuer’s final report by 1% to 3%.

Our team handles the heavy lifting by coordinating with the banks and valuers on your behalf. We guide you through the fine print so you stay informed without feeling overwhelmed. This collaborative effort ensures your transition to a better rate is steady and predictable.

Ready to secure a better deal? Partner with our Port Macquarie experts to start your seamless refinancing journey today.

Partnering with a Broker for Your Home Loan Refinance

Securing a home loan refinance Port Macquarie doesn’t have to be a stressful administrative burden. Think of a broker as your professional project manager who handles the heavy lifting, from initial research to final settlement. While a single bank can only offer you their own products, a broker provides access to a panel of 36+ lenders. This variety ensures you aren’t just getting a loan, but the specific product that aligns with your financial trajectory. We take the time to understand your lifestyle, ensuring the transition is smooth and tailored to your needs.

Your protection is built into every recommendation through the Best Interests Duty (BID). This legal requirement, which came into effect in 2021, mandates that mortgage brokers must act in your best interests at all times. Unlike bank staff who are incentivized to sell their own specific products, brokers are legally bound to prioritize your financial well-being. It’s a powerful layer of security that provides peace of mind throughout the entire process.

Unbiased Advice and Market Access

Brokers often access “broker-only” specials and discounted interest rates that aren’t advertised on bank websites or public billboards. We compare multiple loan structures side-by-side, showing you exactly how an offset account or a split-rate loan impacts your monthly cash flow. This service typically comes at no cost to you as the borrower. The lenders pay the broker a commission after the loan settles, meaning you receive expert guidance without adding to your personal expenses. It’s a transparent way to ensure you’re getting a competitive deal from a pool of dozens of institutions rather than just one. If you’re currently with Australia’s largest lender, our Commonwealth Bank refinance guide walks you through exactly how to compare your CBA rate against the broader market to uncover potential savings.

Your Long-term Financial Partner

Our commitment to your success extends far beyond the day your new loan is approved. The Home Loan Partners provide ongoing annual reviews to ensure your rate remains competitive as market conditions shift. If your goal is to buy an investment property in 2027 or renovate your current home, we’re already preparing the groundwork for those milestones. We don’t just settle a loan; we manage a lifetime of property goals. We act as a steady hand, navigating you through a sea of options with patience and precision. Take the first step toward a smarter mortgage and book a consultation with The Home Loan Partners today.

Take Control of Your Mortgage Journey

Securing a better financial position in 2026 starts with understanding how your current mortgage stacks up against the latest market offerings. A successful home loan refinance Port Macquarie requires a clear look at your equity and a careful comparison of features like redraw facilities. By calculating the real cost of switching, including any discharge fees, you ensure that your new loan provides genuine long-term savings rather than just a temporary fix.

You don’t need to tackle the banks by yourself. We provide access to a panel of over 36 lenders, offering you a range of choices that go far beyond the standard big bank products. Our team delivers expert, unbiased advice tailored to your specific goals, managing the stress-free process from your first enquiry through to settlement. We act as your dedicated partner, doing the heavy lifting so you can focus on enjoying your home.

Partner with an expert to find your better rate today

We’re here to help you navigate the path toward homeownership with confidence and ease.

Frequently Asked Questions

How much equity do I need to refinance my home loan?

You generally need at least 20% equity in your property to avoid paying Lenders Mortgage Insurance (LMI) when you switch. While some Australian lenders accept as little as 5% or 10% equity, having a 20% buffer ensures you access the most competitive rates for your home loan refinance Port Macquarie. If your property value has increased since 2024, you might already have more equity than you realize. We’ll help you calculate your current position to ensure your move is financially sound.

Will refinancing my mortgage hurt my credit score?

Refinancing typically causes a minor, temporary dip of 5 to 10 points in your credit score because the lender performs a hard credit inquiry. This small change is normal and usually recovers within 6 to 12 months as you make regular payments on your new loan. It’s a standard part of the process. We focus on ensuring your application is strong from the start so you don’t need multiple inquiries that could impact your rating further.

How long does the refinancing process typically take in 2026?

The refinancing process in 2026 typically takes between 14 and 28 days from your initial application to settlement. Advanced digital valuation tools and automated document verification now allow many lenders to provide formal approval within 48 hours. Your dedicated partner handles the paperwork and follows up with banks to keep things moving. We aim to make the transition as seamless as possible so you can start saving sooner.

Can I refinance if I have a fixed-rate home loan?

You can refinance a fixed-rate loan, but you’ll likely need to pay a break cost to your current lender. These fees vary based on current market interest rates and the remaining time on your fixed term. In early 2026, many homeowners are weighing these costs against the long-term savings of a lower variable rate. We’ll provide a clear cost-benefit analysis to help you decide if breaking your fixed term makes financial sense for your future security.

What is the “loyalty tax” and how do I know if I am paying it?

The loyalty tax is the higher interest rate banks charge existing customers compared to the discounted rates they offer new borrowers. Data from the Reserve Bank of Australia often shows a gap of 0.5% or more between these two groups. You’ll know you’re paying it if your current rate is higher than the deals advertised on your bank’s website. We’ll audit your current statement to identify exactly how much this tax is costing you each year.

Is it possible to refinance with the same lender?

It’s possible to refinance with your current lender through a process called an internal refinance or a pricing request. This often involves moving to a different loan product or negotiating a lower rate to match what they offer new customers. While this can save on government registration fees, we’ll still compare their best offer against the wider market. This ensures you aren’t missing out on better features or lower rates available elsewhere.

What happens to my offset account when I refinance?

Your existing offset account won’t automatically transfer to a new lender, so you’ll need to set up a new one as part of your home loan refinance Port Macquarie. You’ll move your savings into the new account once the loan settles to continue reducing your interest charges. We’ll guide you through this transition to ensure your funds are working for you from day one. It’s a simple step that protects your long-term financial goals and keeps your interest costs down.

How does a mortgage broker get paid for a refinance?

Mortgage brokers are paid via a commission from the lender you choose, meaning our service typically comes at no direct cost to you. The lender pays an upfront commission of approximately 0.65% of the loan amount at settlement, followed by a small monthly trail commission. These payments are standard across the industry and don’t result in a higher interest rate for you. We remain your partner for the life of the loan to ensure it still fits your needs as the market changes.