Spending A$100,000 on a kitchen and bathroom update in 2026 could actually decrease your net wealth if you choose the wrong financing structure. You’ve likely spent hours scrolling through design inspiration while worrying if construction costs, which rose by 11.9% according to 2024 Cordell data, will turn your dream home into a financial burden. It’s completely natural to feel anxious about overcapitalising when interest rates remain a moving target. We understand that you want to improve your lifestyle without compromising your future security. That’s why finding the right renovation loans is about more than just a bank transfer; it’s about protecting your biggest asset.

We’re here to partner with you to ensure your home upgrade is a savvy investment rather than a source of stress. You’ll discover how to secure financing with interest rates that are often 4.5% lower than standard personal loans by using your home’s equity or a construction loan. We’ll provide a clear finance plan to help you achieve a seamless transition from your current floorplan to your future sanctuary. This guide breaks down exactly how to choose between equity top-ups and specialized lending to increase your property value by a targeted 15% or more.

Key Takeaways

- Identify the most cost-effective way to fund your project by understanding the key differences between secured equity options and unsecured finance.

- Learn how to accurately calculate your usable equity and gather the specific documentation required to ensure a seamless approval process.

- Explore how to align your project’s scale with the right renovation loans to secure the most competitive interest rates for your home upgrade.

- Discover the strategic advantage of valuation-based lending to help you maximise your renovation budget and increase your property’s future value.

- See how partnering with a mortgage broker provides access to over 36 lenders, ensuring your finance is tailored to your unique long-term financial goals.

What Are Renovation Loans and How Do They Work in 2026?

Renovation finance is a specialized credit category designed specifically for property improvements. It allows you to access the funds needed to transform your current house into a dream home without the upheaval of moving. You can typically access these funds through a home equity loan or by restructuring your existing mortgage to include a construction facility. Our team at The Home Loan Partners sees these products as a bridge between your current reality and your future lifestyle goals.

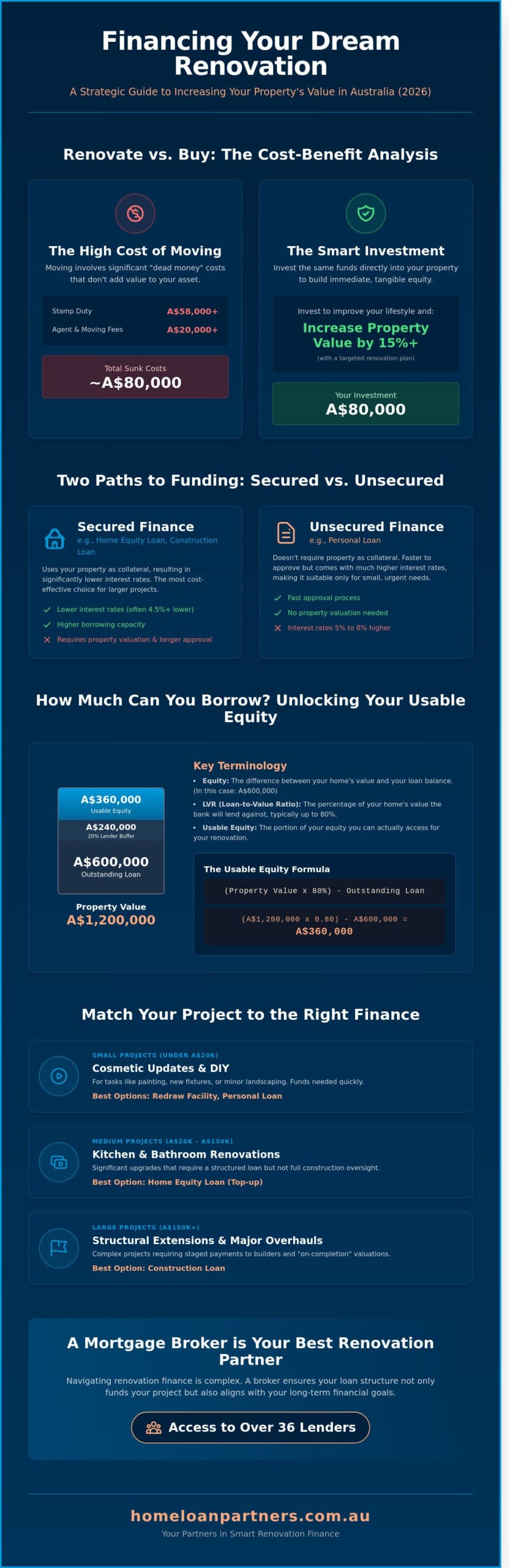

There’s a clear distinction between secured and unsecured renovation debt that you should understand. A secured loan uses your property as collateral. This usually results in lower interest rates because the lender has more security. Unsecured personal loans for renovations are faster to approve and don’t require property valuations, but they often carry interest rates 5% to 8% higher than home-linked options. For larger projects like kitchen remodels or structural extensions, secured renovation loans are almost always the more cost-effective choice.

By mid-2026, market conditions in Australia have shifted significantly. The cost of moving house has reached a point where many families prefer to stay put. High transactional costs, including agent fees and government taxes, make upgrading your current space a much smarter financial move. When you apply for finance, your property valuation plays a vital role in determining your borrowing capacity. Some lenders look at the current “as-is” value of your home. Others use an “on-completion” valuation, which estimates what the property will be worth once your specific upgrades are finished. This expert approach can often unlock more funds than you might expect.

Renovating vs. Buying: The Cost-Benefit Analysis

Choosing to renovate rather than buy a new property is often a decision based on preserving your hard-earned wealth. In 2026, the stamp duty on a median-priced home in Sydney or Melbourne can easily exceed A$58,000. When you add A$20,000 in selling commissions and moving costs, you’ve spent nearly A$80,000 before even stepping into a new front door. Investing that same A$80,000 into your current home builds immediate equity and avoids “dead money” payments to the government. Overcapitalisation occurs when the total cost of improvements exceeds the actual market value added to a property within its specific Australian suburb. For homeowners who do decide to upsize after renovating, using a bridging loan calculator Australia tool can help you accurately estimate the costs of managing two properties during the transition period.

Key Terminology Every Homeowner Should Know

Understanding the technical side of renovation loans helps you feel more in control of your financial journey. We believe in keeping things simple and transparent so you can make informed decisions.

- LVR (Loan to Value Ratio): This is the percentage of your home’s value that the bank is willing to lend against. Most Australian lenders prefer an LVR of 80% or less to avoid additional insurance costs.

- Equity: This is the straightforward difference between what your home is worth today and what you currently owe the bank.

- Usable Equity: This is the portion of your equity you can actually borrow against. Banks don’t let you borrow your full equity amount; they usually require you to leave a 20% buffer in the property. If your home is worth A$1,200,000 and your loan is A$600,000, your total equity is A$600,000, but your usable equity is A$360,000.

Our role as your partner is to guide you through these calculations. We’ll help you determine exactly how much you can afford to spend on your upgrade while keeping your long-term financial security as the top priority.

The 5 Main Ways to Finance a Renovation in Australia

Choosing how to fund your home improvement is just as important as selecting the right builder or floor plan. In the Australian market, homeowners generally rely on five distinct paths to secure renovation loans. Each method carries its own set of requirements, interest structures, and approval timelines. Whether you’re planning a minor cosmetic refresh or a total structural overhaul, we’re here to help you identify the most cost-effective way to bring your vision to life.

Leveraging Your Current Mortgage

If you’ve been diligently making extra repayments, a redraw facility offers the most immediate path to funding. You can typically access these funds instantly through your banking app to cover DIY costs or smaller trades. It’s your own money, so there’s no new approval process or additional interest beyond your current mortgage rate. For mid-sized projects like a A$40,000 kitchen upgrade, a home loan top-up is a common choice. This involves applying to your existing lender to increase your total loan amount based on the equity you’ve built. Most banks allow you to borrow up to 80% of your property’s value without incurring Lenders Mortgage Insurance. If your property was valued at A$900,000 in early 2024 and your balance is A$600,000, you have a healthy buffer to work with. If your current bank isn’t offering the flexibility you need, you might find better terms by following our Home Loan Refinancing guide to unlock equity with a new lender.

Specialised Construction and Personal Finance

When your plans involve moving walls, adding a bedroom, or any work requiring council approval, a construction loan becomes necessary. Unlike a standard lump-sum loan, these are managed through progressive drawdowns where the bank pays your builder directly at specific stages, such as the frame or lock-up phase. Progressive drawdowns save you significant money because you only pay interest on the portion of the loan that’s been paid out to the builder so far. This keeps your monthly costs lower during the months your home is a construction site.

For homeowners focused on sustainability and reducing long-term bills, the Australian Government’s Household Energy Upgrades Fund provides a strategic framework for financing energy-efficient installations like high-grade insulation or solar systems. This initiative reflects a growing shift toward greener homes in the 2024 property market. If speed is your priority for a smaller project under A$35,000, an unsecured personal loan is a viable alternative. These loans offer several benefits and a few trade-offs:

- Fast Approval: Many lenders provide funds within 24 to 48 hours of application.

- No Collateral: You don’t need to use your home as security, which protects your equity.

- Fixed Terms: You’ll have a clear end date for the debt, usually between three and seven years.

- Higher Rates: Expect interest rates between 8% and 13% in the current market, which is higher than mortgage-based renovation loans.

Our team acts as your expert partner throughout this decision, ensuring you don’t over-capitalise or take on a debt structure that doesn’t fit your long-term goals. We’ll handle the heavy lifting of comparing rates and terms so you can focus on choosing your finishes. If you’re ready to see which option fits your budget, reach out for a tailored assessment of your borrowing power today.

Project Matching: Which Loan Suits Your Renovation Scale?

Matching your finance to your project’s scope is the most critical step in the planning phase. A small bathroom refresh doesn’t require the same complex paperwork as a second-story extension. We help you identify the most cost-effective path so your budget goes into your home, not into unnecessary bank fees. Your choice of renovation loans should align with the total cost, the time it takes to build, and your long-term goals for the property.

Interest rates vary significantly across different finance paths. While a mortgage top-up might sit around 6.2%, a personal loan can climb to 15% depending on your credit profile. Short projects that wrap up in three months might justify a higher rate for the sake of speed. Conversely, a structural overhaul lasting 12 months requires a loan that offers interest-only periods during the build to manage your cash flow effectively.

Cosmetic Upgrades (Under $50,000)

For minor updates like landscaping, painting, or a kitchen face-lift, simplicity is key. Personal loans provide fast approval, often within 24 to 48 hours, but they carry interest rates that are often double those of a mortgage. If you’ve been diligent with your mortgage, using an offset account is usually the smartest move. By drawing from your offset, you effectively borrow at your home loan rate, which currently averages around 6.15% for many Australian homeowners. For those focusing on sustainability, the Household Energy Upgrades Fund provides a pathway to cheaper finance for energy-efficient improvements. It’s a great way to lower your bills while increasing your home’s value without the stress of a high-interest credit card debt.

Major Structural Renovations ($150,000+)

Large-scale projects demand a more rigorous lending structure. When you change the footprint of a house, banks require a fixed-price building contract to protect their investment. They won’t just hand over a lump sum; they release money in “drawdowns” at specific stages like slab, frame, and lock-up. A key benefit here is the “subject to completion” valuation. The lender assesses the future value of your home based on the architectural plans. If your home is worth A$850,000 now but will be worth A$1.3 million after the build, you can often borrow against that future equity. This is where Construction Loans become essential, as they provide the oversight and staged payments required for high-value builds.

Your future plans for the property dictate the final loan structure. If you intend to sell the property within 18 months, avoid products with high exit fees or complex break costs. If this is your “forever home,” focus on a structure that allows for redraws or additional repayments so you can clear the debt faster once the dust settles. We act as your partner throughout this decision, ensuring the financial foundation of your renovation loans is as solid as the new walls you’re building. We take the weight of the paperwork off your shoulders so you can focus on choosing tiles and paint colours.

Step-by-Step: How to Prepare for a Renovation Loan Application

Securing renovation loans doesn’t have to be a source of stress. By following a structured preparation path, you position yourself as a low-risk borrower. This preparation begins with a clear understanding of your current financial standing and the future value of your property. We’ve seen that clients who prepare their paperwork early often shave three weeks off the standard approval timeline.

First, calculate your usable equity. Lenders generally allow you to access up to 80% of your property’s value minus your existing mortgage. For instance, if your home is valued at A$950,000 and you owe A$550,000, your usable equity is A$210,000. This calculation provides the foundation for your project scope. Next, gather your documentation. You’ll need itemised quotes from licensed builders, council-approved architectural plans, and proof of income, such as your two most recent group certificates or three months of payslips. In the current 2026 market, property values fluctuate. You must obtain an “as-if-complete” valuation. This specific report estimates what your home will be worth once the hammers stop swinging; this often allows you to borrow more than your current equity suggests.

Consulting a mortgage broker is your next logical step. Different lenders have varying appetites for construction risk. Some banks offer better rates for structural changes, while others prefer cosmetic updates. Finally, ensure your budget includes a 15% contingency buffer. Building costs in Australia shifted significantly between 2023 and 2025, and material prices remain volatile. Having this cash reserve prevents your project from stalling if you encounter unexpected site issues like old wiring or plumbing complications. If your renovation plans are part of a broader strategy to sell and upgrade your property, you may also want to use a bridging loan calculator Australia lenders recommend to map out the financial gap between your sale and purchase settlements.

Calculating Your Borrowing Power

Your Debt-to-Income (DTI) ratio is a primary metric lenders use to assess your application. Most Australian banks prefer a DTI ratio below 6.0 to ensure you can comfortably manage repayments alongside your existing lifestyle. A clean credit history, ideally with a score above 750, often leads to fast-tracked approvals. Maintaining a 20% equity buffer is the sweet spot for lenders because it eliminates the need for Lenders Mortgage Insurance and signals a lower risk profile for your renovation project.

Working with Builders and Contracts

Banks require a fixed-price building contract from a licensed professional before they release funds. This contract must include a progress payment schedule that aligns with standard industry stages like base, frame, and lock-up. If you’re considering an owner-builder path, be aware that many lenders limit your borrowing to 60% of the total property value. To manage variations in the build price, keep your contingency fund separate from your primary loan. This ensures you can cover unexpected costs without needing to renegotiate your mortgage terms during the middle of construction.

Ready to start your home transformation? Our team of experts can help you compare the best renovation loans tailored to your specific project goals.

Why a Mortgage Broker is Your Best Renovation Partner

Choosing the right financing for your project feels overwhelming when you’re staring at a stack of builder quotes and architectural plans. While your current bank might offer a simple “top-up,” they only provide access to their own limited products. We give you a distinct advantage by providing access to over 36 different lenders across the Australian market. This variety ensures you aren’t forced into a rigid policy that doesn’t align with your specific renovation goals.

Our expertise lies in “valuation-based” lending, a strategy that can significantly expand your project scope. Instead of just looking at what your home is worth today, we work with lenders who assess the “as-if-complete” value. For instance, if your current property is valued at A$900,000 but will be worth A$1.25 million after a major extension, we help you unlock equity based on that future valuation. This approach often increases a client’s available budget by 25% or more compared to a standard equity release. It’s about making your money work harder for you from day one.

We take the heavy lifting off your shoulders by managing the complex paperwork and lender negotiations. Renovation finance involves more than a single lump sum; it requires a structured drawdown process where funds are released as your builder hits specific milestones. We act as the intermediary between you, the bank, and the contractor to ensure payments flow smoothly. Our focus remains on ensuring your loan structure supports long-term wealth creation. We don’t just look at the build; we look at how this debt fits into your life over the next decade.

Beyond the Interest Rate

A low headline rate often masks expensive traps. We’ve identified hidden fees in many renovation “top-up” offers, such as A$500 valuation charges or ongoing monthly administration costs that erode your savings. Our team provides dedicated support throughout the five-stage drawdown process, ensuring you only pay interest on the funds you’ve actually used. As we look toward the 2026 lending landscape, where APRA regulations continue to evolve, we provide the steady hand needed to navigate shifting serviceability requirements. We keep your project on track even when the broader market feels uncertain.

Getting Started with Home Loan Partners

Your journey begins with a comprehensive renovation strategy session. During this meeting, we’ll analyze your current equity, your borrowing capacity, and the projected value of your finished home. We bring deep local expertise to the table, whether you are renovating a heritage home in Greenwich or a modern coastal property in Port Macquarie. We understand the local market nuances that big banks often miss. We’re here to be your partner in every sense of the word, turning your vision into a tangible reality through expert guidance. Book a consultation to find your ideal renovation loan and take the first step toward your home upgrade today.

Start Your Home Transformation Journey Today

Turning your current house into a dream home requires more than just a vision; it demands a strategic financial foundation. As we navigate the 2026 property market, the key to success lies in matching your project’s scale to the right funding method. Whether you need a construction loan for structural changes or an equity release for cosmetic updates, preparation is your greatest asset. Ensure your quotes and plans are ready before you approach a lender to keep the process moving forward.

You don’t need to navigate the complexities of renovation loans alone. Home Loan Partners gives you direct access to over 36 leading Australian lenders, providing the variety and competitive edge your project deserves. Our team brings specialized experience in construction and equity lending to Greenwich and Port Macquarie locals, acting as a steady partner from your first inquiry through to the final settlement. We’ll do the heavy lifting with the banks so you can focus on the design details.

Let our expert brokers find the right renovation loan for your project

We’re ready to help you unlock your property’s full potential and secure your family’s future in a home you truly love.

Frequently Asked Questions

Can I get a renovation loan if I have no equity?

Yes, you can still access funding through an unsecured personal loan or a construction loan based on the property’s “on-completion” value. While traditional equity-based top-ups require a buffer, some Australian lenders allow you to borrow up to 95% of the estimated future value of your home. This approach helps you start your project sooner. We’ll partner with you to determine which path fits your current financial position.

Is it better to refinance or get a personal loan for renovations?

Refinancing is generally better for major structural works because it offers lower interest rates, often between 6.00% and 7.00% in the 2024 market. Personal loans are faster to set up but carry higher rates, sometimes exceeding 10.00%. If your project costs more than A$50,000, refinancing your mortgage is usually the most cost-effective way to secure renovation loans. We’ll guide you through the comparison to ensure you save on interest.

How much can I borrow for a home renovation in Australia?

You can typically borrow up to 80% of your home’s current or future value without paying Lenders Mortgage Insurance (LMI). Some specialized lenders allow borrowing up to 95% of the “on-completion” value for major works. For a A$750,000 home, this could mean accessing A$150,000 or more in funds. Your borrowing capacity depends on your income, existing debt, and the specific scope of your building contract.

Do I need council approval before applying for a renovation loan?

You need formal council approval or a Complying Development Certificate (CDC) if your project involves structural changes or extensions. Lenders require these documents before they’ll finalize a construction loan or release large sums of money. For cosmetic updates like a A$20,000 kitchen refresh, you don’t need council consent to apply. We help you identify exactly which permits your bank will ask for during the application process.

What happens if my renovation goes over budget?

If costs exceed your initial loan, you’ll need to apply for a loan top-up or use your own savings to cover the gap. Most Australian builders recommend keeping a 15% cash contingency buffer to handle unexpected price hikes in materials or labor. Banks won’t automatically increase your limit once the contract is signed. Planning for these extra costs from day one ensures your project stays on track without financial stress.

Can I use a renovation loan for a DIY project?

You can use renovation loans for DIY projects, but banks are often stricter with “owner-builder” arrangements. Most lenders prefer you to use an equity release or a personal loan for DIY work to avoid the complex inspections required for professional builds. If you choose an owner-builder loan, expect to provide a 30% deposit as a security measure. This ensures the bank’s investment remains protected while you manage the site yourself.

How does a construction loan drawdown process work?

The drawdown process involves the bank releasing funds in five distinct stages as your builder reaches specific milestones. These stages typically include the slab, frame, lock-up, fixing, and final completion. After each stage, you’ll submit an invoice to the bank, and they’ll often send a valuer to inspect the progress. This system protects you by ensuring you only pay for work that’s been completed to a professional standard.

Will a renovation loan increase my monthly mortgage repayments?

Your monthly repayments will increase because you’re adding to your total debt balance. For example, adding A$50,000 to your mortgage at a 6.5% interest rate increases your monthly commitment by approximately A$316. However, if you use an interest-only period during construction, your initial costs will be lower until the project is finished. We’ll help you calculate these figures accurately so there are no surprises for your household budget.