What if you could acquire the latest machinery without touching your cash reserves or risking your family home? Many business owners feel trapped between the need to modernize and the fear of cash flow volatility or complex tax jargon. It’s a common concern, and we understand that protecting your hard-earned stability is your top priority. Mastering asset finance for small business is about more than just securing equipment; it’s about finding a steady partner to help you manage the 4.35% RBA cash rate environment with confidence.

You likely believe that maintaining a healthy cash buffer is the safest way to grow, and we agree that liquidity provides vital peace of mind. This guide promises to unlock the capital you need to scale by teaching you how to maximize tax deductions, such as the $20,000 instant asset write-off, while avoiding the stress of multiple bank negotiations. We’ll walk through the strategic advantages of different finance structures and show you how to secure your future growth with precision and clarity.

Key Takeaways

- Learn why asset finance for small business uses the equipment itself as security, keeping your personal property and family home protected.

- Discover how to match your finance term to the useful life of your equipment to ensure your repayments remain sustainable.

- Understand the strategic timing of GST claims and tax deductions to keep your cash flow steady throughout the financial year.

- Explore the streamlined “Low Doc” application process that allows established businesses to secure funding with minimal paperwork.

- Find out why a broker’s panel of over 36 lenders offers more flexible and competitive solutions than a single bank can provide.

What is Asset Finance for Small Business?

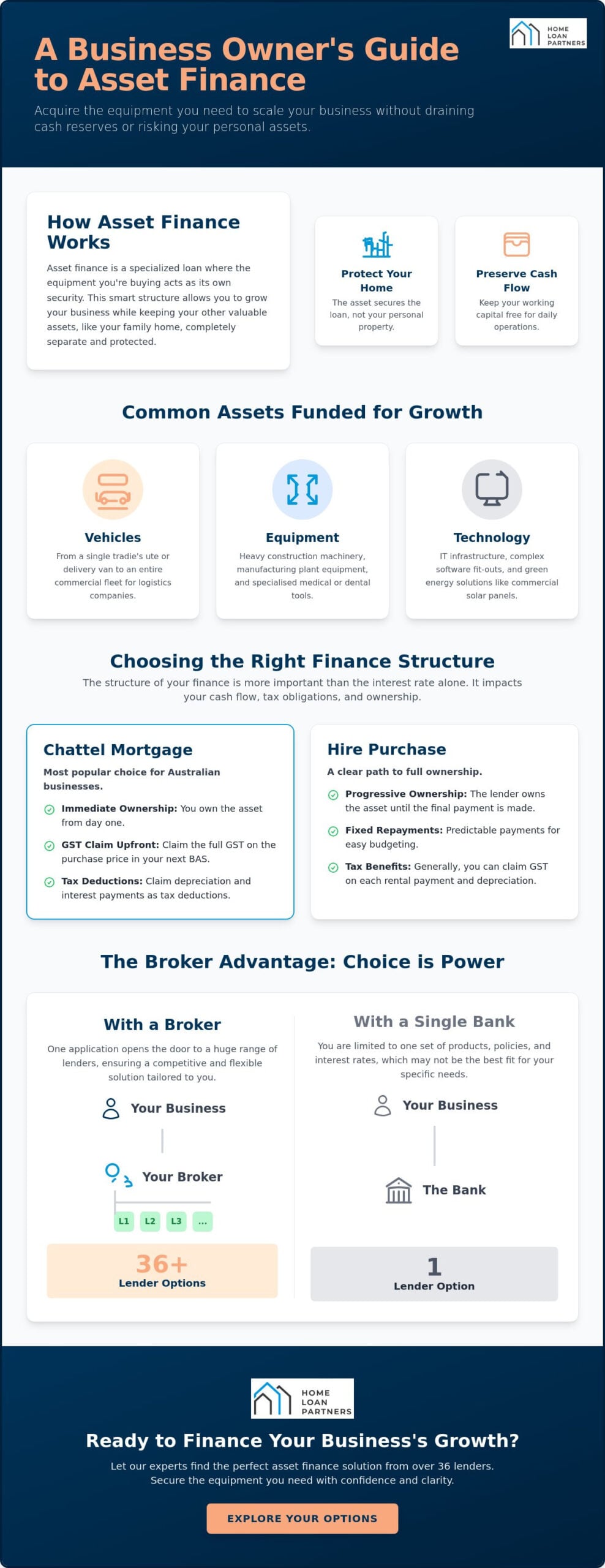

Asset finance for small business is essentially the engine room of Australian enterprise. It allows you to acquire the physical tools your company needs to thrive without exhausting your available cash. Instead of a traditional loan that might look at your entire business history or personal assets, this specialised lending category focuses on the item you’re actually buying. Whether it’s a new delivery van or a high-tech medical scanner, the equipment itself serves as the primary security. We see it as the “workhorse” of growth because it bridges the gap between where your business is now and where you want it to be.

One of the most significant advantages we help our clients understand is the preservation of working capital. You shouldn’t have to choose between upgrading your technology and having enough cash to cover operational expenses or unexpected hurdles. By using asset finance, you keep your cash buffer intact for day-to-day needs while the new asset starts producing income immediately. Most importantly, it creates a clear line between your business ambitions and your personal life. You can scale your operations without the anxiety of using your family home as collateral.

The Asset as Security: A Game Changer

This structure is often called “self-securing” because the lender’s interest is tied directly to the asset. To understand the broader context, it’s helpful to look at what asset-based lending is on a global scale. Unlike general business loans that often require a General Security Agreement (GSA) over all your company’s assets, asset finance is more surgical. It’s a precise way to borrow that keeps your other assets unencumbered. Asset-backed lending serves as a practical tool for risk mitigation by ensuring the debt is supported by the value of the equipment itself.

Common Assets Funded in 2026

- Vehicles: This remains a core part of the market. We assist with everything from a single tradie’s ute or delivery van to entire commercial fleets for logistics companies.

- Equipment: This category is broad. It includes heavy construction machinery like excavators, manufacturing plant equipment, and specialized tools for dental or medical practices.

- Technology: In 2026, we’re seeing a massive shift toward financing IT infrastructure, complex software fit-outs, and green energy solutions like solar panels. These assets are vital for staying competitive but often carry high upfront costs that are better managed through structured finance.

The Six Core Asset Finance Structures in Australia

Choosing the right way to pay for your equipment is just as important as the equipment itself. We often see business owners get caught up in finding the lowest interest rate, but the structure of your loan often has a bigger impact on your long-term success. One size definitely does not fit all. A structure that works for a sole trader with a single van might be completely wrong for a company upgrading its entire IT network. Matching the finance term to the useful life of the asset ensures you aren’t still paying for a machine that has already become obsolete.

Your business structure also dictates which path is most efficient. Sole traders and large companies face different tax obligations and reporting requirements. This is why we focus on the “why” behind the numbers. We also look at the role of balloon payments, sometimes called residuals. By setting a larger final payment at the end of the term, you can significantly lower your monthly repayments and keep your cash flow steady for daily operations. If you’re unsure which path fits your specific goals, our team can help you explore asset and equipment finance options tailored to your needs.

Chattel Mortgage vs. Hire Purchase

The chattel mortgage is currently the most popular choice for asset finance for small business in Australia. With this structure, you take ownership of the asset from the day of purchase, and the lender secures the loan against it. The primary benefit is the immediate impact on your balance sheet. Under 2026 rules, you can typically claim the full GST amount on the purchase price in your next BAS, which provides a welcome cash injection. In contrast, a hire purchase involves the lender owning the asset until you make the final payment. It’s a progressive ownership model that suits businesses looking for a clear path to full ownership without the immediate tax complexities of a mortgage.

Finance Leases and Operating Leases

Leasing offers a different kind of flexibility. In a finance lease, the lender buys the asset and leases it to you for a fixed term. You take on the risk regarding the residual value at the end of the lease, but you gain the use of the equipment without a large upfront cost. Operating leases are more like a long-term rental. The lender retains ownership and carries the risk of the asset’s value dropping. This is a strategic choice for fast-obsolescence technology like servers or specialized software. We recommend operating leases for any assets that you plan to upgrade every two or three years to stay competitive.

Novated Leases and Sale-and-Leaseback

A novated lease is a unique three-way agreement between you, your employee, and the lender. It’s an excellent tool for providing vehicle benefits as part of a salary package while managing your business costs. For established businesses looking to grow quickly, sale-and-leaseback can be a game changer. You sell an asset you already own to a lender and then lease it back from them. This acts as a liquidity injection for established businesses, allowing you to unlock the equity tied up in your machinery to fund new projects or manage seasonal dips.

Strategic Analysis: Balancing Cash Flow and Tax Benefits

While most business owners naturally look for the lowest interest rate, the “cheapest” loan isn’t always the most profitable choice for your bottom line. We view asset finance for small business as a sophisticated cash flow strategy rather than just a way to buy equipment. A slightly higher rate on a loan that offers flexible repayments or better tax alignment can actually save you thousands over the life of the asset. It’s about looking at the total financial outcome and ensuring your debt serves as an investment in your company’s capacity to generate revenue.

The impact of GST is a perfect example of this strategic thinking. If you choose a structure like a chattel mortgage, you can typically claim the entire GST amount back in your very next Business Activity Statement (BAS). For a $60,000 vehicle, that’s a significant cash injection early in the term. This immediate recovery of funds often outweighs a minor difference in interest rates. Shifting your mindset from “repayment stress” to “capacity building” allows you to see these financial tools as levers for growth rather than burdens on your balance sheet.

The 2026 Tax Environment

For the 2025-2026 financial year, the Australian government has maintained specific incentives for businesses with an aggregated turnover of less than $10 million. You can immediately deduct the full cost of eligible assets costing less than $20,000. If your new equipment exceeds this threshold, it doesn’t mean you lose out. These assets can be placed into a simplified depreciation pool, allowing for a 15% deduction in the first year and 30% in subsequent years. Because the interest component of your repayments is also generally tax-deductible, the net cost of borrowing is often much lower than the headline rate suggests. We always recommend a quick chat with your accountant to ensure your chosen structure aligns perfectly with your specific tax position.

Cash Flow Management Strategies

Smart cash flow management often involves using balloon payments to keep your monthly overheads low during aggressive growth phases. By deferring a portion of the principal to the end of the loan, you keep more cash in your pocket today to fund staff, marketing, or inventory. We also help clients explore seasonal repayment structures. If your business earns most of its income in the summer months, your loan payments can be structured to match that cycle, reducing pressure during quieter periods. Consider the “opportunity cost” of your capital. If your business generates a 15% return on every dollar you reinvest, it makes perfect sense to finance equipment at a rate of 8% or 9% and keep your cash working where it earns the most.

The Application Process: What Australian Lenders Look For

Understanding the mechanics of asset finance for small business is one thing, but knowing how to present your case to a lender is what actually secures the funds. The modern lending environment has changed. Lenders now prioritize speed for established businesses, which has led to the rise of streamlined “Low Doc” options. However, they’ve also become more precise about what they’re willing to fund. They aren’t just looking at your bank balance; they’re looking at the strength of your business’s foundations and the quality of the asset you’re buying.

When choosing asset finance for small business, the asset’s age is a critical factor lenders weigh heavily. Most prefer newer equipment because it holds its value better if they ever need to recover it. If you’re looking at used machinery, it generally needs to be less than 10 to 12 years old by the end of the loan term. Beyond the asset itself, your credit score and ATO portal standing are vital. Lenders want to see that you’re up to date with your tax obligations, as a clean portal often translates to a more competitive interest rate.

Low Doc vs. Full Doc Finance

Low Doc finance is a popular choice for businesses that have been trading for at least 12 months with a valid ABN. It often requires only a simple declaration of affordability and basic identification. This path is built for speed, allowing you to secure equipment quickly when an opportunity arises. Full Doc applications are still necessary for startups, very large-scale machinery purchases, or businesses that don’t meet the standard credit criteria. While Full Doc requires two years of financial statements and tax returns, the trade-off is often a lower interest rate because you’re providing a more detailed picture of your financial strength.

The 5-Step Approval Journey

We aim to make the path to approval as smooth as possible by managing the complex parts for you. The journey typically follows these logical steps:

- 1. Consultation and asset identification: We start by defining exactly what you’re buying and how it will improve your business.

- 2. Structure selection: We align the loan with the tax and cash flow goals we discussed in previous sections.

- 3. Document submission: This is where we gather your “proof of strength,” whether that’s a simple declaration or full financials.

- 4. Lender matching: We navigate our panel of over 36 lenders to find the one that fits your specific profile and asset type.

- 5. Settlement and “Key-in-hand”: Once approved, the lender pays your supplier directly, and you take delivery of your new asset.

If you’re ready to secure the tools your business needs to grow, you can apply for asset and equipment finance with a team that handles the heavy lifting for you.

The Home Loan Partners Advantage: Why a Broker Beats a Bank

Approaching your current bank for asset finance for small business might seem like the easiest path, but it often limits your options to a single set of criteria. The “Big Four” banks are restricted to their own internal products, which may not align with your specific cash flow needs or tax objectives. We act as your expert collaborator, providing a steady hand to navigate the complexities of the market. By looking beyond a single institution, we ensure you aren’t forced into a structure that doesn’t fit your long-term vision.

Our team provides access to a panel of over 36 lenders, ranging from traditional banks to specialized non-bank asset financiers. This variety is crucial because different lenders have different appetites for specific industries or equipment types. Most importantly, we address the common anxiety regarding collateral. While many general business loans might push for a claim on your real estate, we prioritize asset-backed solutions that keep your family home protected. We manage the heavy lifting and the multiple bank negotiations, allowing you to stay focused on running your business without the time-consuming administrative burden.

Beyond the Transaction

We don’t view our work as a one-off settlement. Instead, we focus on how each new asset fits into your five-year growth plan. Our role is to act as an intermediary, translating technical “bank-speak” into practical, everyday language so you feel confident in every decision. Whether it’s explaining the nuances of a residual payment or helping you understand how a new purchase impacts your future borrowing capacity, we’re here for the long-term journey. This unbiased advice ensures that your finance structure remains a support for your milestones rather than a hurdle.

Ready to Scale Your Business?

Scaling your operations should be an exciting milestone, not a source of stress. We promise a calm, predictable experience from our first strategy chat through to the final settlement. If you’re looking for holistic growth beyond just equipment, we can also assist with broader Commercial & Business Loans to support your wider ambitions. Let us handle the complexities of the lending market while you focus on delivering value to your customers. Book a strategy session with The Home Loan Partners today.

Take the Next Step Toward Sustainable Growth

Mastering asset finance for small business is about more than just buying equipment; it’s about protecting your personal stability while aggressively pursuing your professional goals. We’ve explored how the right structure can preserve your working capital and how the latest tax incentives can work in your favour. By choosing a self-securing loan, you ensure that your family home remains safe while your business gains the capacity it needs to thrive in the current 4.35% RBA cash rate environment. You don’t have to navigate these complex financial choices alone.

Our specialised asset and equipment team is here to act as your steady hand throughout this process. With a national Australian service and access to 36+ lenders, we manage the heavy lifting so you can focus on your customers and your team. We’re committed to your long-term journey and look forward to helping you reach your next major milestone with precision and ease. Our experts are ready to guide you through every option with patience and clarity.

Talk to an Asset Finance Expert at The Home Loan Partners today and let’s build your future together.

Frequently Asked Questions

Do I need to put up my house as security for asset finance?

No, you generally don’t need to use your home as collateral for asset finance for small business. The equipment or vehicle you’re purchasing acts as the primary security for the lender. This structure protects your personal property and ensures that your business growth doesn’t put your family’s security at risk. It’s a surgical way to borrow that keeps your most important personal assets completely unencumbered.

Can a new business or startup get asset finance in Australia?

Startups can certainly access asset finance, though the requirements are often stricter than for companies with a long trading history. You’ll likely need to provide “Full Doc” information, including a detailed business plan and financial projections to demonstrate your ability to service the debt. Some lenders may also require a larger upfront deposit to mitigate the risk associated with a new venture.

What is the difference between a chattel mortgage and a lease?

The main difference lies in ownership and how you handle GST. With a chattel mortgage, you own the asset from day one and can typically claim the full GST back in your next BAS. In a lease, the lender owns the asset and you pay for its use over a fixed term. Leasing is often a strategic choice for technology that you plan to replace every few years to avoid obsolescence.

How long does the asset finance approval process take?

The approval process is remarkably fast, often taking between 24 and 48 hours for a “Low Doc” application. If your business requires a “Full Doc” assessment for complex machinery or a very large loan, it might take a few extra days to review your financials. We manage the communication with our panel of over 36 lenders to keep the timeline as short as possible for you.

Can I get asset finance for used equipment or vehicles?

Yes, you can finance used equipment and vehicles, provided they meet the lender’s age requirements. Generally, the asset shouldn’t be more than 10 to 12 years old at the end of the loan term. This allows you to acquire high-quality, pre-owned machinery while still enjoying the benefits of structured finance and preserving your cash reserves for other operational needs.

What are the tax benefits of asset finance for a small business?

Asset finance for small business offers several tax advantages, including the ability to claim interest and depreciation as deductions. For the 2025-2026 financial year, you can also take advantage of the $20,000 instant asset write-off for eligible items. These benefits effectively reduce the net cost of your investment and help you maintain a healthier bottom line while you scale.

Is there a minimum or maximum amount I can borrow for asset finance?

There is no strict universal limit, as the amount you can borrow depends on your business’s financial strength and the value of the asset. While the average asset finance amount in 2026 is approximately $70,369, we help clients secure funding for everything from single delivery vans to multi-million dollar manufacturing plants. We’ll work with you to find a loan size that fits your specific capacity.

What happens if I want to pay off my asset finance early?

You can pay off your loan early, but it’s important to check your contract for early termination fees. Some lenders may charge a fee equivalent to three months’ worth of repayments if you settle the debt before the term ends. We always review these details with you during the selection process so you can make an informed decision about your future flexibility.