Saving a 20% deposit in 2026 feels less like a financial goal and more like a moving target that’s always just out of reach. With property prices continuing to climb, a guarantor home loan australia offers a legitimate shortcut, yet it’s often misunderstood as a risky, lifelong burden for your family. You likely feel the weight of this decision; you want your own home, but you don’t want to jeopardize your parents’ financial security or get tangled in confusing legal liabilities.

We understand that family comes first, which is why we’ve designed this guide to help you leverage equity safely and professionally. You’ll learn how to secure your dream home sooner by using a limited guarantee to avoid Lenders Mortgage Insurance and potentially buy with a 0% deposit. We’ll walk through the latest 2026 market conditions, including the RBA’s 4.35% cash rate, and provide a clear exit strategy to ensure your guarantor is released as your property value grows. By treating this as a temporary strategic bridge rather than a permanent debt, you can protect your family’s future while finally claiming a piece of the Australian property market.

Key Takeaways

- Discover how a guarantor home loan australia can help you secure a property with a 0% deposit and even cover costs like stamp duty by borrowing up to 105% of the purchase price.

- Learn how to protect your family’s assets by utilizing limited guarantees that cap liability at a specific dollar amount, providing peace of mind for everyone involved.

- Understand the eligibility requirements for income stability and property equity to ensure both you and your guarantor meet current 2026 lending standards.

- Follow a structured path to financial independence with a clear exit strategy designed to release the guarantor as soon as your loan-to-value ratio hits 80%.

What is a Guarantor Home Loan in Australia?

In the current 2026 property market, the traditional path of saving a 20% deposit has become a significant hurdle for many Australians. A guarantor home loan australia serves as a collaborative security agreement that bridges the gap between your savings and the purchase price of your first home. Unlike a standard mortgage where the property you buy is the only security, this arrangement brings in a third party to provide additional support. To understand the foundational mechanics of this structure, it helps to look at What is a Loan Guarantee in a broader financial context.

There is a distinct difference between the roles in this agreement. You remain the primary “Borrower,” responsible for all monthly repayments and the overall loan balance. Your family member, usually a parent, acts as the “Security Provider.” They aren’t giving you cash; instead, they allow the bank to use a specific portion of the equity in their own home as a secondary backup. This is fundamentally different from a gifted deposit. While a gift requires your parents to have hundreds of thousands of dollars in liquid cash, a guarantee utilizes the “paper wealth” they’ve built up in their property over time.

How the Guarantee Works

Modern banking has moved away from the old model where a guarantor was liable for the entire loan amount. Today, we focus on “Limited Guarantees.” This means your family member only secures a specific dollar amount, typically the 20% needed to avoid insurance costs plus any extra for stamp duty. Banks prefer immediate family members because the relationship implies a long-term commitment to your success. By using a portion of their equity, the lender views your application as a lower-risk 80% Loan-to-Value Ratio (LVR) deal, even if you’ve only saved a small deposit yourself.

The Immediate Benefits for Borrowers

The primary advantage is speed. You can stop chasing the market and enter your home years earlier than if you were saving alone. The benefits include:

- Zero or Low Deposit: You can often buy with a 0% to 5% deposit, as the guarantee covers the remainder of the bank’s security requirements.

- Wiping Out LMI: Lenders Mortgage Insurance can cost upwards of A$30,000 on a typical suburban home. A guarantee eliminates this cost entirely.

- Premium Interest Rates: Because the loan is technically secured at an 80% LVR, you often qualify for the lower interest rates usually reserved for buyers with massive cash deposits.

This structure turns your family’s historical property success into a launchpad for your own. It’s a strategic move that acknowledges the reality of 2026 property prices while keeping your family’s long-term financial security at the forefront of the arrangement.

How a Guarantee Impacts Your Borrowing Power and Savings

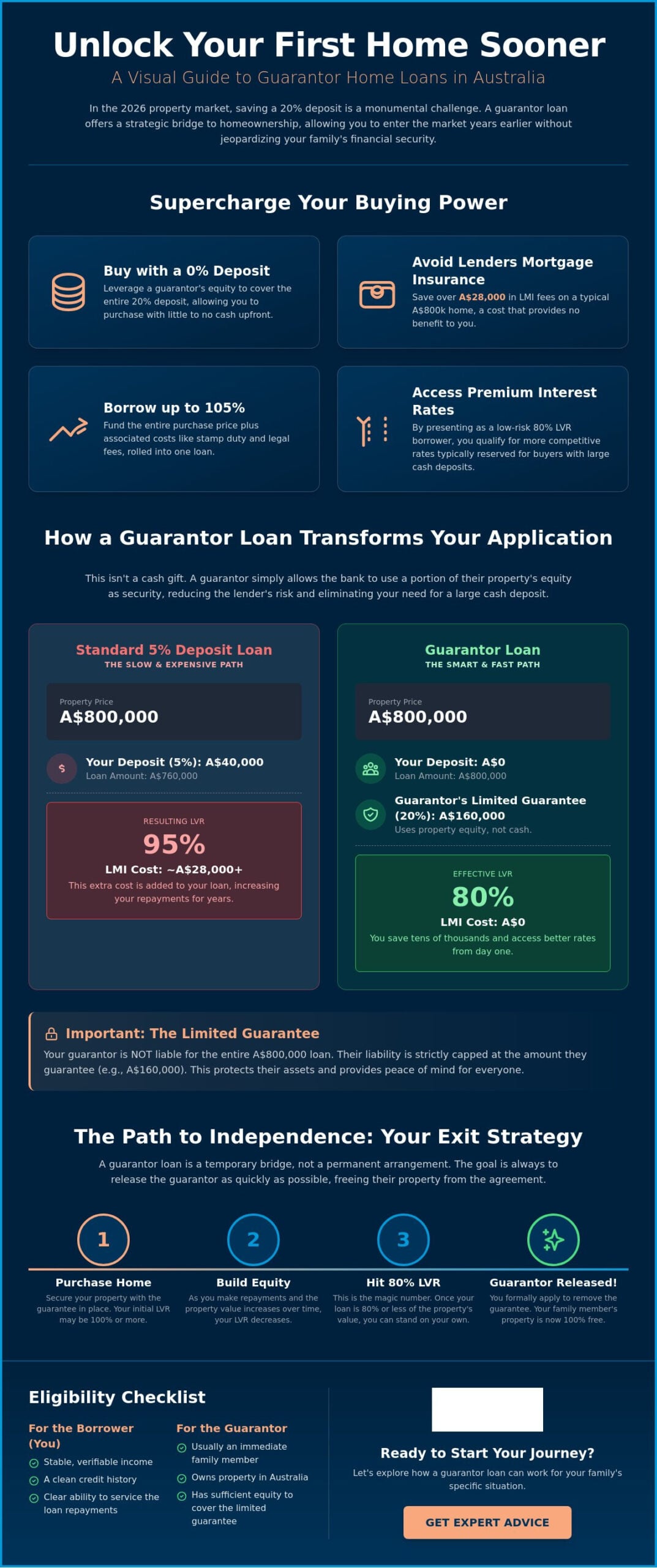

A guarantee transforms the mathematical foundation of your mortgage application by changing how the bank perceives risk. Equity leverage is the strategic use of existing property value to secure additional debt without requiring a cash deposit. By tapping into this existing value, a guarantor home loan australia allows you to bypass the traditional 20% deposit requirement entirely. Instead of looking at your new home in isolation, the lender calculates a “Composite LVR” (Loan-to-Value Ratio). This calculation combines the value of your new property and the portion of equity pledged by your guarantor to create a total security pool, often bringing the technical LVR down to a safe 80% in the eyes of the bank.

This shift in the LVR doesn’t just help you get a “yes” from the credit department; it fundamentally increases your borrowing capacity. When you don’t have to capitalize a massive insurance premium into your loan, your total debt levels stay lower, and your serviceability improves. It’s a proactive way to manage the heavy lifting of a first home purchase while keeping your monthly repayments more manageable. If you’re curious about how these numbers look for your specific situation, a specialist mortgage broker can help model different scenarios for your family.

The LMI Saving Breakdown

Lenders Mortgage Insurance (LMI) is often described as a “sunk cost” because it provides no benefit to the borrower; it only protects the lender if you default. On a standard Australian home purchase of A$800,000 with a 5% deposit, the LMI premium can easily exceed A$28,000. By using a guarantee to reach a technical 80% LVR, you save this entire amount upfront. Rather than paying interest on an extra A$28,000 for the next 30 years, you can redirect those potential savings into an offset account, effectively reducing your interest costs from day one.

Borrowing for Upfront Costs

One of the most significant hurdles for young professionals isn’t just the deposit, but the “hidden” costs like stamp duty and legal fees. A guarantor structure can allow for a 105% loan, where the bank provides the full purchase price plus an extra 5% to cover these transaction costs. This can shave years off your savings timeline, though it’s vital for your family to understand the risks of going guarantor before committing. Even with a 105% loan, most lenders still require you to show a “genuine savings” history, typically 5% of the purchase price held in a bank account for three months, to prove you have the financial discipline to manage the debt.

Protecting the Guarantor: Limited Guarantees and Liability

The most common anxiety surrounding a guarantor home loan australia is the fear that a family member could lose their entire home if the borrower misses a payment. This concern usually stems from the myth of “Joint and Several Liability,” which suggests the guarantor is responsible for the full mortgage balance. In reality, modern Australian lending has shifted toward a more precise and protective model. A Limited Guarantee is a safety cap for the family member. Rather than signing over their entire property as security, your parents or family members only secure a specific, predetermined portion of the loan.

By capping the guarantee at a specific dollar amount, usually around 20% of the property value plus transaction costs, the risk is contained. For example, on an A$800,000 purchase, the guarantee might be limited to A$160,000. This ensures the guarantor’s exposure doesn’t grow even if the total loan balance fluctuates. Beyond this cap, guarantors are protected by the “Right of Indemnity.” This legal principle ensures that if a guarantor is ever required to pay the bank, they have a formal legal right to be reimbursed by the borrower from their assets or future income.

Risks Every Guarantor Must Consider

While liability is limited, the commitment still carries weight in the financial world. A guarantee is recorded as a contingent liability, which can impact the guarantor’s own borrowing capacity if they plan to apply for an investment loan or downsize their own home in the near future. If the borrower encounters financial hardship, the bank will prioritize selling the primary property first, but the guarantor remains the secondary safety net for the capped amount. To ensure everyone is fully informed, lenders require guarantors to seek independent legal and financial advice to confirm they understand the specific terms of the contract.

Mitigation Strategies

We believe in a proactive approach to safeguard the family partnership. One of the most effective tools is ensuring the borrower has comprehensive income protection insurance. This ensures that if the borrower can’t work due to illness or injury, the mortgage repayments are covered, keeping the guarantor’s equity safe. We also focus on building equity quickly through the use of an offset account. Every dollar saved in that account effectively reduces the loan balance, bringing you closer to the day the guarantee can be removed. Finally, setting clear expectations through an informal family agreement can help manage the emotional side of the investment, outlining exactly how and when the exit strategy will be executed.

Eligibility and the Step-by-Step Application Process

Applying for a guarantor home loan australia requires a dual assessment process where the bank evaluates both your financial character and your family member’s asset strength. For you, the borrower, the primary focus is on “serviceability.” Lenders need to see a stable employment history and a healthy credit score, as you’re the one responsible for the monthly repayments. They want to ensure you can comfortably manage the debt at the current RBA cash rate of 4.35% plus the lender’s standard interest rate buffer. Unlike a standard loan, the bank is looking for a partnership that is sustainable for the long term.

The role of a mortgage broker is vital during this phase. We act as the central point of contact, managing the communication between you, your family, and the lender’s credit team. This coordination is essential because these loans often involve two separate property valuations and two sets of legal documents. To get started on your own journey, you can speak with an expert advisor who understands how to package these complex family applications for a smooth approval.

Lenders are generally specific about the types of security they’ll accept. The primary property you’re buying and the guarantor’s property should ideally be standard residential homes in metropolitan or major regional areas. Banks are often hesitant with hobby farms, “tiny homes,” or properties in very remote postcodes. They want to know that if the worst happens, the properties can be sold quickly in a liquid market. We’ll help you verify the eligibility of both properties before you pay for any valuations.

Who Can Be a Guarantor?

Most Australian lenders stick to the “Immediate Family” rule, which includes parents, siblings, and sometimes grandparents. While it’s rare for a friend to be accepted, some niche lenders may consider it if a long-standing financial relationship exists. If your parents are nearing retirement, lenders will assess their “working life” but primarily focus on whether the guarantee would force them to sell their home in a worst-case scenario. As long as they have ample equity and a clear path forward, their age is often secondary to their asset position. We also look for a documented exit strategy at this stage, ensuring there’s a plan to release the guarantor within a few years.

The Application Timeline

- Preliminary assessment: We review the finances of both the borrower and the guarantor to ensure the structure is viable and the “Composite LVR” is within safe limits.

- Policy selection: We select a lender whose specific guarantor policies match your family’s unique situation, such as allowing for guarantors who are already retired.

- Legal review: The guarantor must seek independent legal advice to ensure they fully understand their obligations before signing the contract.

- Valuations and approval: The bank orders valuations on both properties. Once the equity is confirmed and the legal documents are signed, the loan proceeds to final approval and settlement.

The Exit Strategy: When and How to Release the Guarantor

A guarantor home loan australia is a powerful tool, but it’s never intended to be a lifelong commitment. We view the guarantee as a strategic, temporary bridge designed to help you cross the initial deposit gap. For most of our clients, this arrangement typically lasts between two and five years. The ultimate goal is to reach the “magic number” of an 80% Loan-to-Value Ratio (LVR) on your primary property. Once your debt represents 80% or less of your home’s current market value, the bank no longer requires the additional security, and your family member can be formally released from the mortgage.

Our approach is built on proactive partnership. We don’t just set up your loan and walk away; we conduct regular reviews to monitor your property’s value and your loan balance. When market conditions are favorable, property price growth can accelerate this timeline significantly. If your home’s value increases while you’re making steady repayments, you’re suddenly much closer to that 80% threshold. We manage the heavy lifting of the valuation and paperwork to ensure your parents’ equity is freed up as soon as the numbers align, providing everyone with financial independence.

Triggers for Removing a Guarantee

There are three primary ways to reach the point where a guarantee is no longer necessary. We’ll help you track these milestones throughout your home ownership journey:

- Principal Repayments: Every standard monthly payment reduces your debt, slowly improving your equity position.

- Capital Gains: In a rising market, the organic growth of your property’s value is often the fastest way to hit your target LVR.

- Refinancing: We can look at moving your loan to a different lender who may have more flexible valuation policies once you’ve built a solid “safety margin.”

Why a Mortgage Broker is Essential

Navigating the exit strategy requires a deep understanding of the 36+ lender landscape in Australia. Each bank has different rules for releasing a guarantor; some are far more supportive than others when it comes to valuation updates or partial releases. We act as a neutral mediator between parents and children, providing the data and expert guidance needed to make these transitions stress-free. It’s about protecting the long-term journey and achieving major life milestones for the whole family. If you’re ready to see how this structure could work for your situation, Book a strategy session with The Home Loan Partners to see if you qualify.

Take the Next Step Toward Home Ownership

Securing a guarantor home loan australia is a sophisticated way to bypass years of saving while keeping your family’s financial security intact. By focusing on a limited guarantee and a clear exit strategy, you turn a complex banking product into a manageable, short-term bridge to independence. You don’t have to wait for the market to cool or for a 20% deposit to materialize. With the right structure, you can protect your parents’ assets while finally stepping onto the property ladder.

Our team provides the steady hand you need to navigate this journey. We offer access to over 36 Australian lenders and specialize in first-home buyer and family guarantee structures that prioritize your long-term goals. We manage the heavy lifting, from coordinating multiple valuations to ensuring your family receives the professional guidance they deserve. When you’re ready to explore what’s possible, talk to an expert about your guarantor loan options. We’re here to help you achieve this major life milestone with precision and peace of mind. Your dream home is closer than you think.

Frequently Asked Questions

Who is eligible to be a home loan guarantor in Australia?

Eligibility is typically restricted to immediate family members, such as parents, siblings, or grandparents. The guarantor must be an Australian citizen or permanent resident and own a property with sufficient equity to secure the required portion of your loan. Lenders also review the guarantor’s credit history and overall financial stability to ensure they can fulfill the commitment if needed.

Does a guarantor need to provide a cash deposit?

No, the guarantor doesn’t provide liquid cash. Instead, they pledge a specific portion of their property’s equity as additional security for your mortgage. This is a primary reason why a guarantor home loan australia is so popular; it allows you to enter the market without your family needing to have tens of thousands of dollars sitting in a bank account.

Can I remove a guarantor from my mortgage later?

You can apply to release the guarantor once your loan-to-value ratio (LVR) reaches 80% or less. This milestone is usually achieved through a combination of your regular principal repayments and the natural increase in your property’s market value. The bank will perform a fresh valuation to confirm you’ve met this threshold before formally discharging the guarantor from their legal obligations.

What happens if I cannot make my mortgage repayments?

The bank will first look to you to resolve the arrears through hardship programs or by selling your property to cover the debt. If the sale of your home doesn’t cover the full loan balance, the guarantor is legally responsible for the capped amount they secured. We strongly recommend borrowers maintain comprehensive income protection insurance to prevent this scenario and keep family assets safe.

Does being a guarantor affect my own ability to get a loan?

Being a guarantor is recorded as a contingent liability, which can reduce your own borrowing capacity in the future. Because you’ve legally committed to backing a portion of someone else’s debt, other banks must factor this into your expenses when you apply for your own investment property loans or personal finance. It’s a key detail to discuss with your broker if you plan to move house or invest soon.

Is there a limit on how much a guarantor can secure?

Most modern lenders use limited guarantees that cap the liability at a specific dollar amount, usually between 20% and 25% of the property’s purchase price. This amount is designed to cover the gap between your small deposit and the 80% LVR required to avoid insurance costs. The guarantee doesn’t cover the entire loan balance, which provides a significant layer of protection for the family member’s estate.

Can I use a guarantor for an investment property loan?

While most guarantor structures are designed for first-home buyers, some specialized lenders allow guarantees for investment property loans. These applications often face stricter scrutiny regarding the borrower’s income and the guarantor’s asset position. If you’re looking to build a portfolio using this method, we can help you identify the specific lenders that still support investment-focused guarantee structures.

Do I still need to save a deposit if I have a guarantor?

It’s possible to borrow up to 105% of the purchase price with a guarantor, effectively requiring a 0% deposit. However, many lenders still prefer to see a “genuine savings” history of at least 5% held in a bank account for three months. This history demonstrates to the credit department that you have the financial discipline required to manage a long-term mortgage commitment.