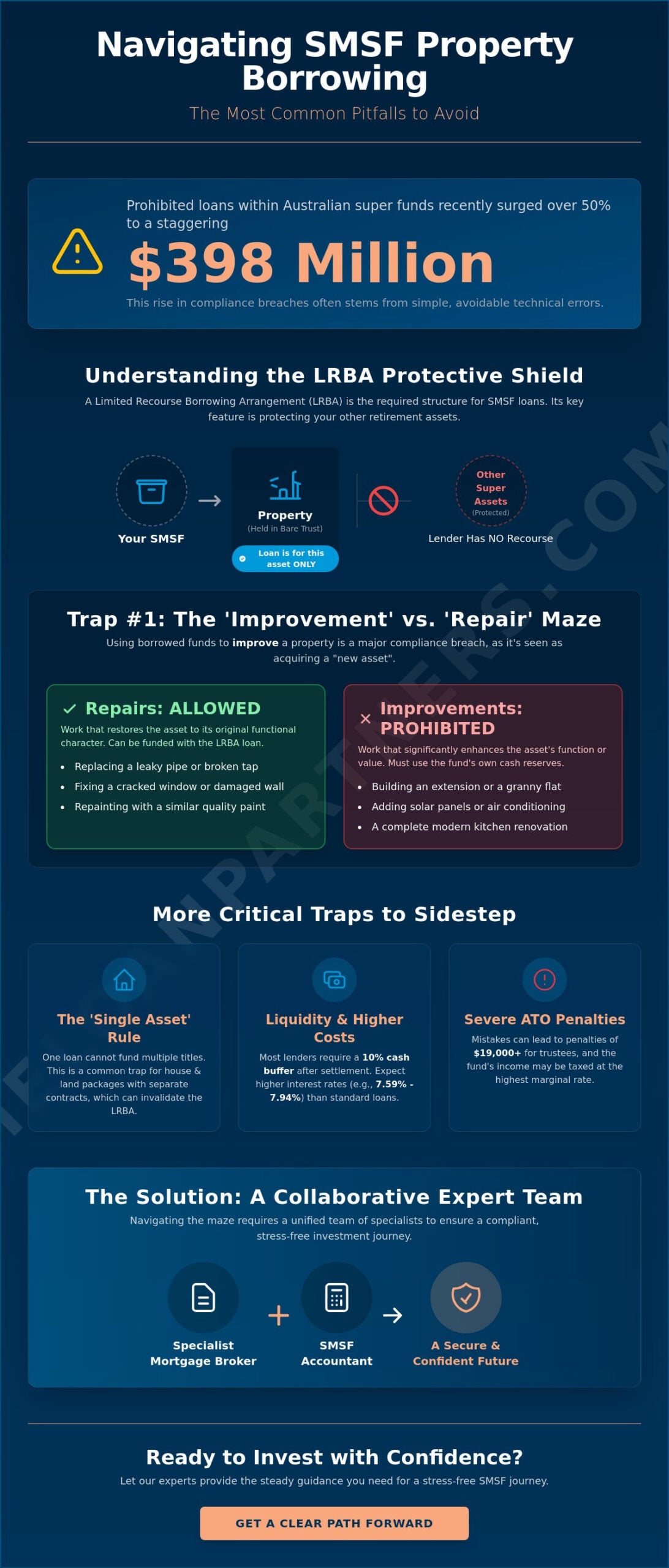

Did you know that the value of prohibited loans within Australian super funds recently surged by over 50% to a staggering $398 million? This sharp rise highlights how easily even the most diligent trustees can stumble into compliance traps when managing debt. We understand that using your super to invest in property is a significant life milestone, but the fear of accidental ATO breaches can make the process feel overwhelming. By identifying the most common borrowing within your SMSF pitfalls, you can navigate these complexities with a sense of calm and expert, steady guidance.

It’s vital to protect your retirement nest egg from the heavy $19,000 plus penalties that often follow simple technical errors. We’re here to provide a clear path through the regulatory minefield, helping you distinguish between necessary repairs and prohibited improvements while keeping your fund’s liquidity secure. This article explores the seven most critical mistakes to avoid in 2026, including the impacts of the new Division 296 tax and the latest safe harbour interest rate requirements, so you can focus on your future with absolute confidence.

Key Takeaways

- Understand how the Limited Recourse Borrowing Arrangement (LRBA) acts as a protective shield for your existing retirement assets.

- Learn the critical legal distinction between property repairs and improvements to prevent your loan from being declared non-compliant.

- Identify and prepare for borrowing within your SMSF pitfalls such as mandatory liquidity buffers and specialized setup fees.

- Discover how to navigate the strict rules surrounding related party loans to avoid the highest marginal tax rates on your fund’s income.

- See how a collaborative partnership between your mortgage broker and accountant provides the steady expertise needed for a stress-free investment journey.

The Mechanics of SMSF Borrowing: Why LRBAs Are Different

Investing in property through your super is a cornerstone of the Australian superannuation system. However, unlike a standard home loan, super fund borrowing requires a specific structure known as a Limited Recourse Borrowing Arrangement (LRBA). In 2026, this arrangement remains the only legal pathway for your fund to take on debt. The term “limited recourse” is actually your fund’s greatest protection. It ensures the lender’s rights are restricted solely to the specific property purchased with the loan. If the investment underperforms, the rest of your retirement savings stay safe and untouchable by the bank.

To facilitate this, a Bare Trust is established to hold the legal title of the property on behalf of your fund. The bank doesn’t hold the title directly, and neither does your super fund until the debt is fully extinguished. This layer of legal complexity, combined with the limited recourse nature of the debt, is why SMSF loans typically carry higher interest rates. Lenders take on more risk because they cannot pursue your other fund assets, so they price their products to reflect that exposure. It is a trade-off between higher costs and the security of your broader nest egg.

The ‘Single Acquirable Asset’ Rule

One of the most common borrowing within your SMSF pitfalls involves misunderstanding the “single acquirable asset” rule. You cannot use one loan to buy multiple titles, even if they are adjacent or part of the same complex. This becomes a significant trap for house and land packages. If the land is purchased first and a separate contract is signed for the build, the ATO often views this as two different assets. This can void your LRBA and lead to severe compliance issues. To qualify, the property must be a single legal entity under one contract at the time of purchase.

The 2026 Interest Rate Environment for Super Funds

As of June 2026, interest rates for commercial SMSF loans from non-related party lenders generally range between 7.59% and 7.94%. These are notably higher than standard investment loans. Understanding these borrowing within your SMSF pitfalls helps you prepare for the stricter liquidity requirements seen this year. Most lenders now look for a cash buffer of at least 10% of the property value remaining in the fund after settlement. This 10% rule ensures your fund can cover ongoing costs, such as the annual supervisory levy and property maintenance, without risking the fund’s overall stability.

Structural Pitfalls: The ‘Improvement’ vs. ‘Repair’ Trap

One of the most complex borrowing within your SMSF pitfalls involves the physical evolution of your investment property. The ATO maintains a rigid distinction between maintaining an asset and enhancing it. While it’s perfectly legal to use borrowed funds for repairs and maintenance, using that same money to improve the property is a direct breach of superannuation law. If an upgrade is deemed an “improvement,” it can legally create a “new asset.” This simple change effectively kills your LRBA, as the loan no longer applies to the original single acquirable asset you purchased.

To understand the difference, consider the “functional character” of the property. Replacing a leaky pipe or fixing a broken window restores the asset to its original condition; this is a repair. Conversely, replacing a functional, dated kitchen with a luxury modern equivalent is an improvement. You can use your fund’s own accumulated cash for these upgrades, but you must be careful. If the improvement is so significant that the property’s character changes, such as converting a residential home into a commercial office, you’ve once again created a new asset and breached the rules.

If you’re planning a property strategy and want to ensure your structure remains compliant, speaking with an expert about SMSF loans can provide the steady hand you need to move forward safely.

When a Repair Becomes an Improvement

In 2026, the ATO continues to apply strict scrutiny to common upgrades. Adding solar panels, building an extension, or constructing a granny flat are all classified as improvements because they add new features that weren’t there before. Even if these additions increase the property’s value, they cannot be funded with your loan. We recommend keeping meticulous records of every maintenance invoice. You need to prove that any work performed was strictly to restore the property to its previous state, rather than adding new functionality.

Subdividing and Developing Within an LRBA

Subdivision is a major trap for many trustees. You cannot subdivide a block of land while it’s secured by an SMSF loan. The act of subdivision fundamentally changes the asset by turning one title into two, which violates the “single acquirable asset” rule. Similarly, you cannot buy a block of land with an LRBA and then build a house on it using borrowed funds. Most successful trustees wait until the loan is fully repaid before pursuing development or subdivision. This ensures the property is held directly by the fund, removing the restrictive LRBA requirements and allowing for greater flexibility in your investment journey.

Financial Pitfalls: Liquidity Crises and Hidden Costs

While the tax benefits of property investment are attractive, many trustees overlook the immediate cash flow demands. One of the most significant borrowing within your SMSF pitfalls is the “Liquidity Trap.” The ATO generally expects your fund to maintain a cash buffer, often around 10% of the property value, after the purchase is complete. This isn’t just a suggestion; it’s a safeguard to ensure your fund can meet its ongoing obligations like the annual supervisory levy and insurance premiums. If your fund is asset rich but cash poor, you might find yourself unable to pay for essential maintenance or required audits, leading to compliance red flags.

Hidden costs can also erode your retirement balance quickly. Setting up a Bare Trust and obtaining the necessary legal opinions isn’t a standard mortgage expense. These are specialized requirements that carry their own professional fees. Additionally, because the tax rate inside a super fund is a flat 15%, the benefits of negative gearing are far less impactful than they are for individual investors. If the property’s expenses exceed the rent, your fund must have enough contributions or other investment income to cover the shortfall. Refinancing an SMSF loan is also significantly harder than a standard mortgage. Fewer lenders operate in this space, and the strict compliance requirements mean you can’t simply “shop around” as easily if interest rates shift.

Serviceability and the ‘Super Guarantee’ Pitfall

Lenders calculate your ability to pay by looking at your current rental income and future Super Guarantee (SG) contributions. This creates a major vulnerability if the fund relies heavily on a single member’s income. If that person stops working, faces a redundancy, or decides to retire earlier than planned, the fund’s ability to meet loan repayments could vanish overnight. We’ve seen how stressful this can be for families. It’s why we advocate for a conservative approach to serviceability that accounts for life’s unpredictable turns, ensuring your loan remains a tool for growth rather than a source of anxiety.

The Exit Strategy Nightmare

Selling a property within an SMSF isn’t a quick or simple process. You need a long-term outlook, typically at least 10 years, before committing to an LRBA. If you’re forced to sell during a market downturn to fund a member’s pension, you might lock in losses or face high Capital Gains Tax (CGT) if the timing is poor. Transferring the property “in-specie” to members at the end of the loan is legally complex and often more expensive than trustees anticipate. Planning your exit before you even enter the loan is the only way to ensure a smooth, stress-free transition into your retirement years.

Compliance Pitfalls: Related Parties and Prohibited Loans

The ATO has signaled a significantly tougher stance for 2026. They’re focusing specifically on prohibited loans, which increased from $252 million to $398 million in recent years. The most common of all borrowing within your SMSF pitfalls is the temptation to treat your super fund like a personal bank account. You cannot loan money from the fund back to yourself, your business, or a relative. This is a strict prohibition with no room for error. Even a short term loan to cover a personal cash flow gap can lead to your fund being declared non compliant, which risks losing half your assets to tax.

Conversely, you can lend your own personal money to your super fund to help it purchase property. This is known as a related party loan. To stay safe, you must ensure the loan is an “arm’s length” transaction. The ATO provides “Safe Harbour” terms to help trustees stay compliant. For the 2025-2026 financial year, the safe harbour interest rate for real property is 8.95%. If you fail to meet these specific rates or exceed the recommended 70% LVR for commercial assets, the fund’s income could be taxed at 45% as non arm’s length income (NALI). We recommend seeking professional guidance to ensure your loan documentation is watertight.

If you’re ready to secure a property with a structure that prioritizes your long term security, our specialists can guide you through compliant SMSF loans tailored to your goals.

The Residential Property Trap

The Sole Purpose Test is the bedrock of SMSF law. This rule dictates that your fund must be maintained for the single purpose of providing retirement benefits to members. Because of this, you and your family members cannot live in a residential property owned by your SMSF. You can’t even stay there for a single weekend. A breach of this rule can trigger an administrative penalty of over $19,000 per trustee. There’s a vital exception for “business real property.” Your own business can lease a commercial office or warehouse from your SMSF, provided the lease is at market rates and professionally documented.

Personal Liability for Fines

Many trustees are surprised to learn that the SMSF cannot pay ATO fines on your behalf. These administrative penalties are designed to be a personal deterrent, so they must come from your own pocket. If your fund has multiple trustees, the ATO can apply these penalties to each person individually. With over 93,000 SMSFs having overdue annual returns as of December 2025, the regulator is increasingly using these fines to encourage better management. Protecting your retirement nest egg starts with understanding that you are personally responsible for the fund’s compliance journey.

Navigating the Maze: The Value of a Collaborative Expert

Building an SMSF property portfolio is a team sport that requires the right partners. While your accountant ensures your strategy aligns with tax laws, a mortgage broker acts as the essential bridge to the financial institutions. We take a proactive “Steady Hand” approach to coordinate the legal, tax, and lending requirements, ensuring no detail is overlooked. By filtering through over 36 lenders, we identify those with SMSF friendly policies that specifically address the borrowing within your SMSF pitfalls we have explored. This precision reduces the emotional weight of your investment, allowing you to move forward with a sense of calm expertise and a clear understanding of your options.

We act as your expert collaborator, translating complex bank jargon into practical language you can use to make informed decisions. Many lenders have withdrawn from the SMSF space or tightened their criteria significantly in 2026. Our role is to stay rooted in the current market, identifying the lenders who still value super fund borrowers and offer competitive terms. By managing the communication between all parties, we ensure a rhythmic and logical flow toward your settlement date, avoiding the jarring transitions that often cause stress in complex financial arrangements.

Structuring Your Loan for Longevity

It is essential to establish your Bare Trust and Corporate Trustee correctly from the very beginning. Banks are notoriously strict; even a minor naming error on a trust deed can trigger thousands of dollars in re-documentation fees and significant settlement delays. We manage the heavy lifting by reviewing these structures alongside your legal team to ensure they meet specific lender criteria. Our goal is to ensure your loan remains robust as you transition from the accumulation phase into the pension phase. This long term focus protects your retirement nest egg and ensures your fund remains a source of security throughout your life milestones.

Your Next Steps Toward SMSF Property

The 2026 property market remains highly competitive, making a formal pre-approval your most valuable asset when dealing with real estate agents. This gives you the confidence to bid or negotiate, knowing your fund’s borrowing capacity is already verified. To start correctly, your first conversation should be with your accountant to confirm your investment strategy. Your second call should be to our team. We will help you avoid common borrowing within your SMSF pitfalls and provide a clear, stress free path to settlement. You can book a collaborative consultation with The Home Loan Partners to begin your journey today.

Securing Your Retirement with Confidence

Navigating the landscape of property investment through superannuation requires a steady hand and a clear vision. By understanding the distinction between property repairs and improvements, maintaining essential liquidity buffers, and adhering to strict ATO safe harbour rules, you protect your retirement nest egg from unnecessary risk. Awareness of these borrowing within your SMSF pitfalls is the first step toward building a legacy that provides lasting security for you and your family.

You don’t have to manage these complexities alone. Our team acts as your dedicated collaborator, offering access to 36 plus specialized lenders and deep expertise in complex Australian property structures. We prioritize your peace of mind by providing personalized, stress-free guidance at every stage of the process. Let our expert brokers guide your SMSF loan journey and help you achieve your most significant life milestones with precision. Your future is a long term journey, and we’re here to support you every step of the way.

Frequently Asked Questions

Can I use my SMSF to buy a holiday home for my family?

No, you cannot use your super fund to purchase a holiday home for personal use. This violates the Sole Purpose Test, which requires the fund to be maintained strictly for providing retirement benefits. Family members are prohibited from staying in the property, even for a single night. Such an arrangement would be classified as an in-house asset breach, potentially leading to severe tax consequences and personal fines for the trustees involved.

How much deposit do I need for an SMSF property loan in 2026?

For residential property loans in 2026, you generally need a deposit of at least 20% as lenders cap LVRs at 80%. For commercial properties, the deposit requirement often increases to 30% or 40%. You must also account for settlement costs and the mandatory liquidity buffer, which is typically 10% of the property’s value. Having these funds ready helps you avoid common borrowing within your SMSF pitfalls during the application process.

What are the penalties for breaching SMSF borrowing rules?

Penalties for non-compliance are significant and can be applied personally to each trustee. The ATO can issue administrative penalties exceeding $19,000 per person, which cannot be paid using fund assets. In extreme cases, your fund could be declared non-compliant, resulting in a tax rate of 47% on the total value of the fund’s assets. This highlights why professional guidance is vital for your long term security and the protection of your nest egg.

Can I renovate a property owned by my SMSF using borrowed money?

You cannot use borrowed funds to renovate or improve a property; you may only use them for repairs and maintenance. While you can use the fund’s own accumulated cash for improvements, you must ensure the work doesn’t fundamentally change the asset’s character. Misunderstanding this distinction is one of the major borrowing within your SMSF pitfalls that can void your entire Limited Recourse Borrowing Arrangement and trigger a compliance audit.

Is it possible to refinance an existing SMSF loan to a lower rate?

Yes, it’s possible to refinance your SMSF loan, but the process is more specialized than a standard residential refinance. The new loan must strictly maintain the limited recourse structure and cannot be used to increase the debt for property improvements. Because the lender pool is smaller, we recommend a collaborative approach to compare the current 2026 rates, which typically range from 7.59% to 7.94% for commercial SMSF products.

What is a ‘Bare Trust’ and why is it required for SMSF borrowing?

A Bare Trust is a specific legal entity created to hold the property title until the loan is fully repaid. It acts as a protective layer, ensuring that the lender’s recourse is limited only to that specific asset. This structure is a mandatory requirement for an LRBA because Australian law prohibits super funds from directly charging their assets. It ensures that the rest of your retirement savings remain safe and untouchable by the bank.

Can I buy my own business premises through my SMSF?

You can certainly purchase your own business premises through your super fund under the “Business Real Property” exception. This allows your business to lease the property from the SMSF, provided the lease is conducted on strictly commercial, arm’s length terms. Your business must pay market-rate rent directly into the fund. This strategy is a popular way for business owners to build wealth while securing their professional future in their own regional market.

For example, a specialized logistics and vehicle recovery service like Done Wright Towing & Transport can benefit from this arrangement by securing a permanent depot while ensuring the rental payments contribute directly to the business owners’ retirement savings.

For business owners in the Australian horticulture industry, managing these investments often goes hand-in-hand with maintaining high operational and ethical standards, and you can discover Fair Farms to see how they support growers with specialized HR services and memberships.

What happens to the SMSF loan if I lose my job?

If a member loses their job, the SMSF must still meet its loan repayments using existing cash reserves or other investment income. If the fund can no longer service the debt, the lender’s rights are limited only to the property held within the Bare Trust. They cannot pursue other fund assets or your personal wealth. This limited recourse feature provides a steady sense of security during unpredictable life transitions or changes in employment.