Financing a new home isn’t a single transaction; it’s a synchronized financial dance where timing every step is the only way to protect your cash flow. If you’re currently exploring buying land and building a house package finance, you’ve likely discovered that the rules are different from a standard mortgage. It’s natural to feel some tension when faced with dual contracts or the uncertainty of interest-only payments while your home is still a construction site. You aren’t alone in wanting the benefits of a custom build and lower stamp duty without the stress of hidden site costs.

This guide provides the steady hand you need to master these complexities with confidence. We’ll break down exactly how construction loans function in 2026, from managing the current 4.35% RBA cash rate to handling progressive payment schedules. You will gain a clear financial roadmap that explains how to utilize state-specific benefits, such as the $30,000 First Home Owner Grant in Queensland or the stamp duty abolishment starting July 2026 in the ACT. Let’s turn that initial confusion into a precise plan for your brand-new home.

Key Takeaways

- Understand the structural differences between turnkey and standard build contracts to select the arrangement that best protects your future security.

- Navigate the complexities of buying land and building a house package finance with a clear breakdown of how progressive drawdowns work to lower your initial interest payments.

- Uncover the essential site costs and finishing expenses that often fall outside “fixed price” quotes, ensuring your budget remains precise and transparent.

- Discover a step-by-step financial timeline for 2026 that prioritizes early pre-approval to streamline the coordination between land settlement and construction milestones.

- Learn how partnering with a mortgage broker provides access to specialized construction policies while alleviating the stress of managing multiple industry stakeholders.

What is a House and Land Package and How Does Finance Work?

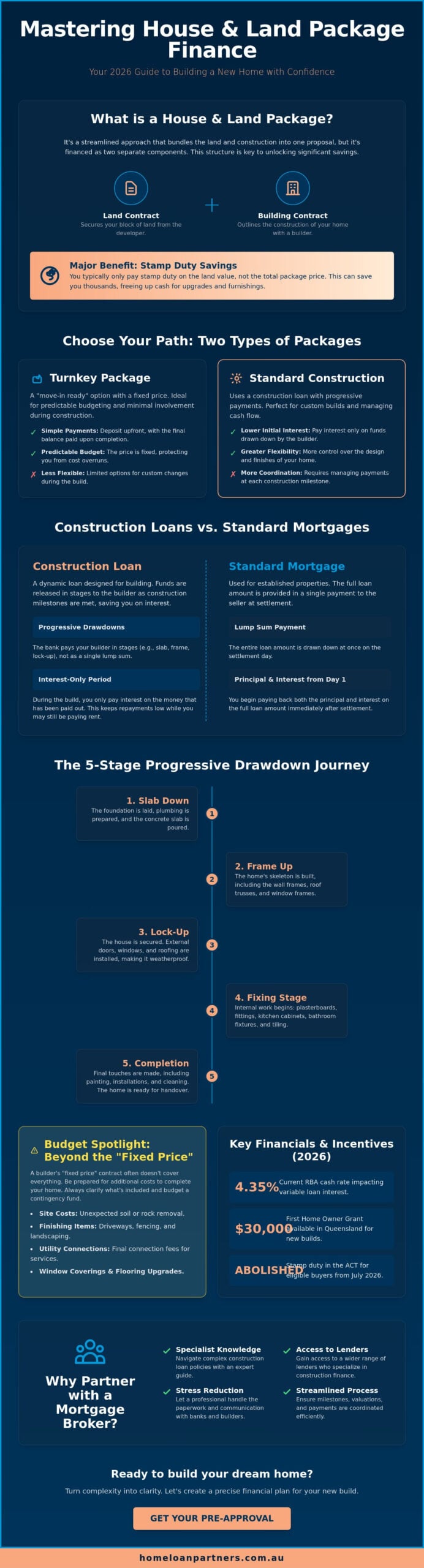

A house and land package simplifies the journey to homeownership by bundling your block of land and your future dwelling into one cohesive proposal. It’s a popular choice for those who want a brand-new home without the stress of sourcing land and a builder independently. For those who value professional insight into residential and commercial property acquisition, teams like Steve Kooner & Associates demonstrate the importance of expert guidance in securing the right foundation for a project. While it feels like a single purchase, the financial engine under the hood operates with two distinct parts: the land purchase and the construction contract. Mastering buying land and building a house package finance requires understanding how these two pieces fit together to protect your long-term security.

One of the most significant benefits of this arrangement is the potential for substantial stamp duty savings. When you buy an established property, you pay stamp duty on the total value of the land and the house. With a house and land package, you typically only pay stamp duty on the land value, provided the building hasn’t started yet. This can result in thousands of dollars in savings, giving you more breathing room in your budget for high-quality finishes or landscaping. While standard mortgages for existing properties involve a single lump-sum payment at settlement, this path uses a more specialized structure to ensure your funds are used efficiently throughout the build.

Turnkey vs. Standard Construction Packages

Choosing the right package type depends on your cash flow needs and how much involvement you want in the process. Turnkey packages are often the simplest option; they’re “move-in ready” and usually require a deposit upfront with the balance paid only upon completion. This makes budgeting predictable because you don’t have to manage multiple payments during the construction phase.

Standard construction packages utilize a progressive build model. This requires a construction loan where the lender releases funds in stages, known as progressive drawdowns, as the builder reaches specific milestones. While this requires more coordination, it offers greater flexibility for those who want a home tailored specifically to their lifestyle. In 2026, many clients prefer this model to keep interest costs lower, as you only pay interest on the funds that have been actually released to the builder.

The Dual-Contract Structure Explained

The legal foundation of your new home rests on two separate documents. The first is the Land Contract, which you sign with the developer to secure your block. The second is the Building Contract, signed with a registered builder for the construction of the dwelling. Even if you purchase a package through a single developer, these contracts remain legally distinct. Your lender will review both documents during the application for buying land and building a house package finance to ensure the project is viable and the costs are fixed. This separation protects you by ensuring that your land is secured even if there are adjustments to the building timeline.

Construction Loans vs. Standard Mortgages: Key Differences

When you buy an established home, your lender provides a lump sum at settlement to cover the purchase price. However, buying land and building a house package finance requires a more dynamic approach. Instead of a single payment, the bank uses a progressive drawdown system. This ensures that funds are only released as the builder hits specific milestones. Before the first sod is turned, lenders perform an “as if complete” valuation. This assessment estimates the future value of your finished home and land to determine your total borrowing power, providing a sense of security that the project is financially viable.

The primary difference you’ll notice is how your repayments are calculated during the build. While standard mortgages usually require principal and interest payments from day one, construction finance typically begins with an interest-only period. This structure is designed to support your cash flow while you’re still paying rent or managing your current mortgage. You only pay interest on the portion of the loan that has been paid to the builder, keeping your monthly costs manageable until you’re ready to move in. Understanding these nuances is a key part of mastering Freddie Mac’s loan options and similar construction-to-permanent products available in the market.

The Progressive Drawdown Mechanism

Your loan is divided into stages that mirror the physical progress of your home. This protective structure ensures that the builder is paid for work completed, rather than work promised. The typical sequence includes:

- Stage 1: Deposit and Slab. This initial release covers the building deposit and the completion of the foundation and ground works.

- Stages 2-4: Frame, Lock-up, and Fixing. These stages involve the home’s skeleton, exterior cladding, roofing, and internal fittings like plastering and cabinetry.

- Final Stage: Practical Completion. The final payment is released once the home is finished and a final inspection ensures everything meets the agreed standards.

Managing Interest-Only Payments

The interest-only phase is a powerful tool for maintaining financial stability during the 6 to 12 months of construction. Since you aren’t paying down the principal yet, your outgoings remain lower while the house is a work in progress. It’s vital to maintain a small financial buffer during this time. Even with a fixed-price contract, unexpected weather delays or minor site adjustments can extend the interest-only period. By planning for these costs early, you can navigate the build with a steady hand. If you’d like to see how these payments fit into your specific budget, you can speak with an expert to model your potential monthly costs. Once the keys are in your hand, the loan usually transitions into a standard principal and interest arrangement, starting your long-term path to full ownership.

Key Financial Considerations and Hidden Build Costs

Securing the right buying land and building a house package finance requires a sharp eye for detail that looks far beyond the initial sticker price. While the RBA cash rate has stabilized at 4.35% as of June 2026, lenders are applying stricter scrutiny to construction budgets than in previous years. Most banks traditionally look for a 10% deposit, but many eligible buyers now leverage the Home Guarantee Scheme to enter the market with just a 5% deposit while avoiding the added cost of Lenders Mortgage Insurance. Understanding your Loan to Value Ratio (LVR) is vital; the bank’s “as if complete” valuation must align with your total project costs to ensure you aren’t left with a funding gap at the final stage.

One of the most frequent hurdles involves site costs, which are the expenses required to prepare your specific block for construction. You should be aware that a “fixed price” contract might not automatically account for significant rock removal, complex drainage, or specific soil classifications. Industry data indicates that site works can range from $10,000 to over $50,000 depending on the terrain and soil quality. If these expenses aren’t accurately captured in your initial finance application, you may need to cover the difference with personal savings. We aim to help you identify these variables early so your financial path remains steady and predictable.

Understanding Fixed-Price Build Contracts

Lenders prefer fixed-price contracts because they minimize the risk of cost overruns. However, you must look closely for Provisional Sums (PS) and Prime Cost (PC) items. A PS is an estimate for work that cannot be fully costed yet, such as earthworks, while a PC is an allowance for specific items like fixtures or cabinetry. If the actual cost exceeds these allowances, you’ll be responsible for the difference. Lenders often view large PS or PC amounts as a red flag; they prefer contracts where these variables are kept to a minimum to ensure the loan amount remains sufficient.

Budgeting for Post-Settlement Essentials

Many standard packages focus purely on the structure, leaving “finishing” items as the owner’s responsibility. This often includes essentials like floor coverings, air conditioning, driveways, fences, and window blinds. It’s a wise strategy to maintain a 5% to 10% contingency fund to manage these post-settlement needs or any minor variations that arise during the build. If you already own property, you might consider using existing equity to cover these gaps. This proactive approach ensures your new home is truly move-in ready without a last-minute financial scramble. Mastering buying land and building a house package finance means accounting for the day you turn the key, not just the day the slab is poured; for those planning premium finishes, Horns Construction offers a great example of high-quality building services and renovations.

The Step-by-Step Finance Timeline for 2026

Timing is the most powerful tool in your arsenal when managing buying land and building a house package finance. Unlike a standard purchase, you’re coordinating two distinct legal events that must align perfectly to avoid costly delays. In 2026, the process typically follows a five-step path designed to protect your interests and maintain a steady financial flow. It begins with a comprehensive pre-approval that accounts for your total project budget, including both the land price and the fixed-price build contract. This proactive step ensures you can shop with confidence, knowing exactly what your borrowing ceiling is in the current 4.35% cash rate environment.

- Step 1: Obtain Pre-Approval. Secure a figure based on your total project budget before committing to a specific block.

- Step 2: Secure Land and Sign Build Contract. Sign your dual contracts, ensuring the build contract is “fixed-price” to satisfy lender requirements.

- Step 3: “On Completion” Valuation. Your lender assesses the plans to ensure the finished home’s value supports the loan amount.

- Step 4: Land Settlement. The land loan is established, and you take legal ownership of the block.

- Step 5: Construction Start. Work begins, and the first progressive drawdown is released to the builder.

Preparing Your Application

Success starts with a complete documentation pack. Lenders require detailed plans, specifications, and a copy of the builder’s insurance before they’ll issue a formal offer. You’ll also need to demonstrate your deposit clearly. Whether you’re using genuine savings, equity from an existing property, or a government incentive like the $30,000 First Home Owner Grant in Queensland or Tasmania, the bank needs to see how the total project is funded. A common hurdle is the land title; if the developer hasn’t “titled” the land yet, your settlement might be delayed. We monitor these timelines closely to ensure your finance remains valid throughout any developer delays.

From Slab to Keys: The Payment Flow

Once construction starts, the bank manages the payment flow through the progressive drawdown system. At each milestone, the builder will issue an invoice. You’ll need to sign a claim form to authorize the bank to pay the builder directly. This protective measure ensures you only pay for work that has been physically completed to the agreed standard. If weather or material shortages cause delays, your interest-only period simply extends. The final step is the handover, which occurs after a practical completion inspection and the release of the final payment. To ensure your timeline remains on track, get started with a specialized construction loan assessment today. This allows us to manage the heavy lifting while you focus on the design of your new home.

Why Partner with a Mortgage Broker for Your Build?

Managing the intricacies of buying land and building a house package finance requires more than just a loan approval; it demands a dedicated partner who understands the rhythm of construction. While a single bank can only offer you their own internal products, a mortgage broker provides a gateway to over 36 different lenders. This diversity is essential because every lender views construction risk differently. Some may offer lower variable rates starting from 5.84% for investors or 5.89% for owner-occupiers, while others might be more flexible with deposit requirements for first-time builders. By comparing the entire market, we ensure you aren’t just getting a loan, but the specific construction policy that aligns with your 2026 financial goals.

The true value of a broker lies in the coordination of the “synchronized dance” between the developer, the builder, and the bank. When you’re dealing with dual contracts, a minor delay in land titling or a small variation in the build specifications can stall your progress. We act as your central point of contact, managing the heavy lifting of communication so you don’t have to. This proactive management prevents the stress of missed deadlines and ensures that your progressive payments are released on time, keeping your builder on-site and your project moving forward.

Comparing Construction Policies Across 36+ Lenders

Lender appetite for new builds varies significantly. Some institutions are “construction-friendly,” offering streamlined approvals and higher Loan to Value Ratios (LVRs) that allow you to start with a smaller capital contribution. Others may have strict limits on the types of materials or locations they will finance. We help you navigate these nuances, identifying lenders who accept the Home Guarantee Scheme or those who offer more competitive fixed rates, currently starting around 6.20% for one-year terms. Our expertise allows us to structure your application to maximize your borrowing power while minimizing costs like Lenders Mortgage Insurance, even in a cautious lending environment.

The Home Loan Partners Advantage

Our commitment to your journey doesn’t end when the first slab is poured. We view our role as a long-term partnership that continues from the initial pre-approval through to the final inspection and beyond. Once your home is complete and you’ve moved in, we continue to monitor the market to ensure your post-construction interest rate remains competitive. This steady, expert guidance provides a sense of security during what is often one of life’s most significant investments. If you’re ready to move forward with clarity and confidence, book a stress-free consultation with our team today. We’ll help you navigate the complexities of buying land and building a house package finance with precision and care.

Build Your Vision With Financial Confidence

Navigating the path to a brand-new home is a journey of precision. By understanding how progressive drawdowns protect your cash flow and how to identify hidden site costs early, you’ve already taken the most important step toward a successful build. The dual-contract structure doesn’t have to be a source of anxiety when you have a clear roadmap and a steady hand guiding the timeline. Mastering buying land and building a house package finance is about more than just numbers; it’s about securing the milestones that turn a block of land into your family’s future.

Our team acts as your dedicated collaborator, offering access to a panel of over 36 lenders to find the specific construction policy that fits your needs. As specialists in complex construction and bridging finance, we provide expert guidance through the dual-contract process so you can focus on the design of your new home. We take pride in managing the heavy lifting, ensuring your transition from land settlement to final handover is as smooth as possible.

Start your building journey with a tailored finance strategy from The Home Loan Partners. We look forward to standing beside you from the first brick to the final key handover, helping you achieve this major life milestone with total peace of mind.

Frequently Asked Questions

Can I buy a house and land package with a 5% deposit?

Yes, you can secure a home with a 5% deposit through the Home Guarantee Scheme. As of June 2026, this federal initiative allows eligible buyers to bypass Lenders Mortgage Insurance entirely. This significantly lowers your upfront costs while buying land and building a house package finance. We help you navigate the eligibility criteria to ensure your application meets the specific requirements of participating lenders on our panel.

Do I pay stamp duty on the whole package price or just the land?

You typically only pay stamp duty on the land value. This is a primary financial benefit of a house and land package because the building contract is treated separately. In states like Queensland, first home buyers are exempt from stamp duty on new homes with no price cap. In the ACT, stamp duty is abolished for all first-home buyers from July 1, 2026, regardless of the property price.

What happens if my builder goes into liquidation during the build?

Your project is protected by Domestic Building Insurance if your builder enters liquidation. This mandatory insurance covers the costs to complete the build or fix structural defects if the builder can’t fulfill their contract. We verify that your builder has the correct insurance certificates before your loan is established. This provides a steady safety net so your investment remains secure through any unforeseen industry changes.

Can I use the First Home Owner Grant for a house and land package?

Yes, the First Home Owner Grant is specifically designed for new builds. Depending on your state, you could receive between $10,000 and $30,000 to assist with your project. Most lenders allow you to use these funds toward your final construction stages. We coordinate with your builder to ensure the grant timing aligns with your progressive payment schedule to maintain a smooth cash flow throughout the build.

Are interest rates higher for construction loans than standard mortgages?

Construction loan rates are generally comparable to standard variable rates. As of June 10, 2026, owner-occupier variable rates start from approximately 5.89% p.a. The main advantage is that you only pay interest on the amount actually released to the builder. This keeps your monthly outgoings much lower during the 6 to 12 months it takes to complete your home compared to a fully drawn mortgage.

How long does it typically take to get finance approved for a build?

Finance approval for a build usually takes four to six weeks. This timeline is slightly longer than a standard purchase because the lender must review the building contract, specifications, and the “as if complete” valuation. Having your plans and builder’s insurance ready when you begin buying land and building a house package finance can speed up the process. We manage the communication between all parties to keep this timeline moving.

Can I change my house design after the loan has been approved?

You can make changes, but they require a formal variation process. Any change to the design or price after the loan is approved must be submitted to your lender for re-assessment. If the variation increases the cost, you may need to cover the difference with your own funds if the valuation doesn’t increase proportionally. It’s best to finalize your design before signing the building contract to avoid these complications.

What is a “valuation as if complete” and why does it matter?

This is an expert estimate of what your property will be worth once construction is finished. Lenders use this figure to determine your borrowing power and Loan to Value Ratio (LVR). It’s a critical step because it confirms that the total cost of your land and build is supported by the property’s future market value. This provides security for both you and the bank that the project is a sound investment.