What if the size of your salary isn’t the primary factor standing between you and your first set of keys? It’s a common fear that with the RBA cash rate sitting at 4.35% as of May 2026, lenders will simply overlook anyone without a high-flying corporate income. You might feel that the strict 3% serviceability buffer makes it impossible to figure out how to get a home loan with a low income in australia, especially when the median dwelling price in capital cities has hit $987,000. We understand it’s frustrating to watch the cost of living eat into your savings while banks seem to raise the bar higher every month.

The truth is that homeownership in 2026 is less about the numbers on your payslip and more about which partner you choose to guide you. While major banks often have rigid floor rates, specialized lenders and new government initiatives offer a steady path forward. This guide reveals the strategies we use to help clients secure approval, from leveraging the Help to Buy scheme’s 2% deposit to utilizing the First Home Guarantee, which now has no income caps. We’ll provide a clear roadmap to show you which lenders are truly low-income friendly and how to turn alternative income sources into a “yes” from the credit department.

Key Takeaways

- Understand how lenders use the HEM benchmark and serviceability floor rates to assess your application, and learn how to position your finances to meet these tests.

- Discover how to get a home loan with a low income in australia by leveraging the 2026 First Home Guarantee to secure a property with a 5% deposit and no Lenders Mortgage Insurance.

- Follow a clear action plan to conduct a personal ‘Shadow Audit’ of your spending, helping you eliminate high-interest debt and boost your borrowing capacity.

- Learn why partnering with an expert broker provides access to a wider range of lenders whose criteria are specifically tailored for modest budgets.

- Identify the key differences between regional and metro support schemes to ensure you’re accessing every grant and shared equity program available for your location.

What Counts as ‘Low Income’ for an Australian Home Loan in 2026?

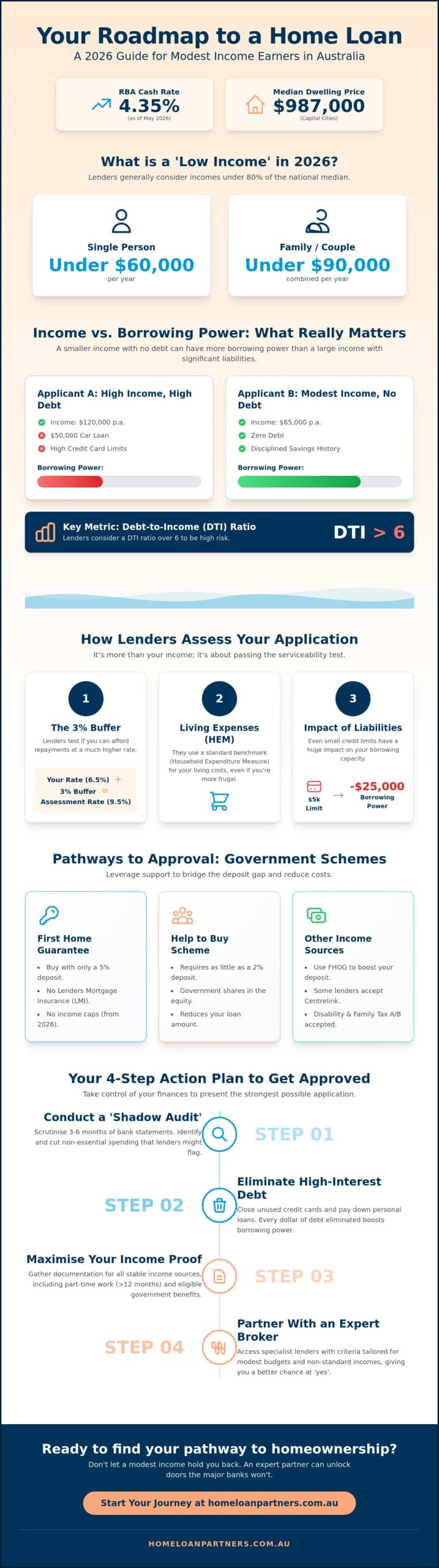

In the Australian housing market of May 2026, the definition of “low income” is relative to the rising cost of living and property values. Generally, lenders consider a household to be on a low income if they earn less than 80% of the national median income. For a single person, this usually means an annual income under $60,000; for a family, it’s typically under $90,000. While these figures might seem modest compared to the capital city median dwelling price of $987,000 recorded in December 2025, they don’t automatically disqualify you from homeownership. Understanding how to get a home loan with a low income in australia begins with a shift in perspective. Your gross salary matters, but your net “borrowing power” is the figure that actually secures the keys.

There’s a significant difference between having a low income and having low borrowing power. A person earning $120,000 with a $50,000 car loan and high credit card limits may actually have less borrowing capacity than someone earning $65,000 with zero debt and a disciplined savings history. Lenders start categorizing applicants as “high risk” when their Debt-to-Income (DTI) ratio exceeds six. This threshold became even more critical after APRA implemented stricter DTI rules in February 2026. To be a successful applicant, you need to show that your modest income isn’t being stretched thin by existing liabilities.

Standard vs. Non-Standard Income Types

Lenders view the stability of your paycheck as a primary safety metric. Full-time employees usually have the easiest path, but part-time and casual workers can find success if they’ve been in their role for at least 12 months. Secondary income like overtime, bonuses, or commissions is often “shaded,” meaning the bank might only count 80% of those earnings toward your application. Assessable income for 2026 lending standards is defined as the verified, gross annual earnings that a lender considers stable enough to support long-term loan repayments.

Centrelink and Government Payments as Valid Income

Many Australians don’t realize that certain government benefits can be included in a loan application. While some payments are ignored entirely, others like the Disability Support Pension or Family Tax Benefits (Part A & B) are often accepted at 80% to 100% of their value by specific lenders. The key is proving the “stability” of these payments; most banks want to see that you’ve received the benefit for at least 6 to 12 months and that it will continue for at least another five years. When combined with the First Home Owner Grant (FHOG) scheme, these benefits can help bridge the gap between a “no” and a “yes” from a credit assessor. We act as your expert partner to identify which lenders in 2026 are most supportive of these diverse income profiles.

How Lenders Assess Your Borrowing Power (The Serviceability Test)

Securing a mortgage isn’t just about showing you have a deposit. It’s about passing the bank’s “serviceability test.” When you’re looking at how to get a home loan with a low income in australia, you’ll encounter the Household Expenditure Measure (HEM). This is a standard benchmark lenders use to estimate your cost of living based on your family size and location. Even if you live frugally, most banks will default to this benchmark if your actual spending is lower. They want to ensure that after you pay for groceries, transport, and utilities, you still have enough left to cover a mortgage.

The most significant hurdle in 2026 is the serviceability “floor rate.” APRA requires lenders to add a 3% buffer to the actual interest rate. If your variable rate is 6.5%, the bank tests your ability to make repayments as if the rate were 9.5%. This safety margin is designed to protect you if rates rise, but it can significantly lower the amount you’re allowed to borrow. We act as your expert partner to help you identify lenders with more flexible assessment criteria that might suit your specific budget better than the big banks.

The Impact of Existing Liabilities

Small debts have a surprisingly large impact on your borrowing capacity. A credit card with a $5,000 limit can reduce your total borrowing power by as much as $25,000. This is because banks assess the full limit of the card as if it were fully drawn, not just the balance you owe. Student debt like HECS or HELP also plays a role. While it’s a “cheap” debt, the compulsory repayments reduce your take-home pay, which directly lowers your serviceability score. Modern lenders also scrutinize Buy Now Pay Later (BNPL) services. Frequent use of these platforms can be a red flag, signaling a reliance on credit for everyday purchases.

Optimizing Your Financial ‘Passport’ Before Applying

Preparation is your greatest tool. We recommend a “clean-up” period of three to six months before you submit an application. During this time, you should aim to minimize discretionary spending on things like multiple streaming subscriptions or frequent delivery meals. Lenders look for “genuine savings,” which usually means having at least 5% of the property value saved in a bank account for at least 90 days. This proves you have the financial discipline to manage a long-term commitment. Reducing your total credit card limits is the fastest way to boost your borrowing power before you apply.

Many clients find success by combining these personal improvements with the Australian Government 5% Deposit Scheme. This program allows eligible buyers to enter the market with a smaller deposit while avoiding the cost of Lenders Mortgage Insurance. If you’re feeling overwhelmed by these requirements, you can speak with a mortgage partner to get a clear picture of your current standing and a tailored plan to improve it.

Pathways to Approval: Government Schemes and Support Structures

The Australian lending environment in 2026 has shifted its focus from simple cash grants to more sophisticated support structures. While interest rates remain a challenge, these programs act as a bridge for those wondering how to get a home loan with a low income in australia. The most significant evolution is the broad availability of the First Home Guarantee (FHG). As of late 2025, the government removed the limit on the number of available places and scrapped income caps for this specific scheme. This allows you to purchase a home with a deposit as low as 5% without the added cost of Lenders Mortgage Insurance, which saved participants an average of $12,800 in 2025.

For those living outside major metropolitan areas, the Regional First Home Buyer Guarantee provides similar support tailored to local price caps. However, the real game changer for 2026 is the Help to Buy scheme, which officially launched in December 2025. This is a shared equity program where the government contributes up to 40% of the purchase price for a new home or 30% for an existing property. With a minimum deposit requirement of just 2% and a limit of 10,000 places per year, it significantly reduces the mortgage amount you need to service. As of April 2026, over 2,300 places had already been approved, showing strong uptake among modest-income earners.

You can also utilize the First Home Super Saver Scheme (FHSSS) to build your deposit faster. This scheme allows you to make voluntary contributions to your superannuation, which are taxed at a lower rate, and later withdraw up to $50,000 for your home purchase. By combining these tax savings with government guarantees, your path to homeownership becomes much steadier.

The Family Guarantee (Guarantor) Option

If you don’t have a 5% deposit saved, a guarantor loan remains a powerful shortcut. This is where a family member uses the equity in their own home to provide additional security for your loan. It effectively replaces the need for a cash deposit and allows you to avoid LMI entirely. While this is an excellent strategy for low-income earners, it’s vital that your guarantor understands the legal risks. In 2026, most lenders allow the guarantee to be limited to just a portion of the loan, which protects your family member’s long-term security while helping you get a foot in the door.

Joint Ventures and ‘Buying with Friends’

Co-borrowing is an increasingly popular way to navigate the 2026 property market. By combining two modest incomes into a single application, you can significantly boost your total borrowing power. Banks assess your joint serviceability, which often makes it easier to pass the 3% interest rate buffer test. To protect your relationship and your investment, we always recommend a formal Co-ownership Agreement. This legal document outlines what happens if one person wants to sell or if financial circumstances change, ensuring your journey as partners remains transparent and secure.

A Step-by-Step Action Plan to Secure a Low-Income Home Loan

Securing a mortgage on a modest budget requires more than just hope; it requires a tactical approach to your financial history. Learning how to get a home loan with a low income in australia is a process of elimination. You must eliminate the reasons a bank might say “no” before you ever submit an application. By treating your finances with the same scrutiny as a credit assessor, you can build a case for approval that stands up to the 3% serviceability buffer currently required by APRA as of May 2026.

- Step 1: Conduct a ‘Shadow Audit’. Download your last 90 to 180 days of bank statements. Look for patterns of discretionary spending that might suggest financial stress, such as frequent “buy now pay later” payments or late fees.

- Step 2: Consolidate or eliminate high-interest debt. Every dollar you owe to a credit card or personal loan provider reduces your borrowing power by approximately five dollars. Closing a $5,000 credit card can instantly boost your capacity.

- Step 3: Secure your ‘Genuine Savings’ history. Lenders want to see that you’ve held at least 5% of the property value (roughly $49,350 for the median capital city dwelling) in a savings account for a minimum of 3 months.

- Step 4: Research ‘Low-Income Friendly’ lenders. While major banks are often rigid, Tier 2 and Tier 3 lenders, including non-bank providers, frequently have more flexible algorithms for assessing casual or secondary income.

- Step 5: Obtain a realistic Pre-Approval. Don’t rely on a basic online calculator. A formal pre-approval involves a credit check and a verified assessment of your payslips, giving you the confidence to bid in a competitive market.

Choosing the Right Property Type

The type of home you choose is just as important as your income. Entry-level properties like studio apartments or small units often come with stricter lending rules; many banks require a 20% deposit for properties under 40 square meters. You should also be aware of postcode restrictions. Some lenders limit their exposure in high-density areas, which can lead to a sudden rejection even if your income is sufficient. Finding the “LMI sweet spot” is also vital. Sometimes paying a small amount of Lenders Mortgage Insurance is better than waiting another year while prices rise, provided your serviceability remains strong.

Preparing the Paperwork for a Complex Income

If your income comes from multiple part-time jobs or includes government benefits, your documentation must be flawless. You’ll need to provide at least two years of group certificates and your most recent three months of payslips for every employer. For those receiving Centrelink, a current statement showing the longevity and type of benefit is essential. Providing a clear letter of explanation for any past income gaps or career changes helps the credit assessor understand your journey and build trust in your stability. If you’re ready to start this process, contact our expert brokers for a tailored review of your situation.

Why Partnering with a Mortgage Broker is Essential for Low Income

Securing a “yes” from a credit assessor is often about choosing the right gatekeeper. When researching how to get a home loan with a low income in australia, many applicants find that the major banks have a “one size fits all” approach that doesn’t account for unique financial strengths. We provide access to a panel of over 36 lenders, ranging from traditional banks to boutique non-bank providers. This variety is essential because different lenders use different algorithms; some may be more conservative with discretionary spending, while others prioritize your long-term employment stability and “genuine savings” history.

Our role as your expert partner is to act as an advocate against conservative credit teams. We understand the specific nuances of every lender’s policy, allowing us to package your application in a way that highlights your financial discipline. Instead of a cold, transactional encounter at a bank branch, you receive a tailored strategy designed to maximize every dollar of your assessable income. We do the heavy lifting of comparing rates and features, ensuring your path to property ownership is both steady and predictable.

Beyond the Initial Approval

The journey doesn’t end when you settle on your property. As your income grows and you build equity in your first home, your financial needs will evolve. We maintain a long-term partnership with you, reviewing your mortgage regularly to ensure it still serves your future security. This might involve looking at How to refinance your home loan to take advantage of lower interest rates or better features as your loan-to-value ratio improves. This focus on longevity is a core part of how we support your Australian dream.

Navigating the 2026 Market with Confidence

The complexity of the 2026 lending market requires more than just a basic online estimate. Professional, unbiased advice helps to alleviate the inherent stress of the application process, providing a sense of calm expertise. By choosing a guide who understands the local landscape, you gain the clarity needed to make informed decisions without the high-pressure sales tactics common in the finance industry. If you are ready to explore your options, Speak with an expert from The Home Loan Partners today to begin your stress-free path forward.

Take Your First Step Toward Homeownership Today

The path to owning your own home in 2026 remains open, even if your income feels modest. By combining government support like the Help to Buy scheme’s 2% deposit with a disciplined “shadow audit” of your spending, you can overcome the challenges of the current 4.35% cash rate. You’ve learned that borrowing power is more about managing debt and serviceability than just the size of your payslip. Understanding how to get a home loan with a low income in australia is the first step; the next is finding a partner who can navigate the specific lending criteria of over 36 Australian lenders on your behalf.

We specialize in complex income situations and low-deposit solutions, acting as your steady guide through the entire mortgage process. Whether you’re aiming for the $12,800 average savings provided by the Home Guarantee Scheme or using a family guarantor, we handle the heavy lifting for you. Book a free strategy session with The Home Loan Partners to see how we can turn your homeownership goals into a clear, manageable roadmap. Your Australian dream is achievable, and we’re here to help you reach it with confidence.

Frequently Asked Questions

Can I get a home loan if I’m on a single low income?

Yes, you can secure a mortgage on a single income by utilizing government shared equity programs. The Help to Buy scheme, which has 10,000 places available annually as of 2026, is specifically designed for individuals earning under $100,000. It allows the government to co-purchase up to 40% of the property; this significantly lowers your monthly repayments and makes a single-income application much stronger in the eyes of a lender.

What is the minimum income required for a home loan in Australia?

There’s no official minimum salary required by law, but lenders generally look for a stable income that covers the 3% serviceability buffer. In the 2026 market, “low income” usually refers to individuals earning under $60,000. Your success depends more on your debt-to-income ratio than the raw number on your payslip. Keeping this ratio below six is a key factor in figuring out how to get a home loan with a low income in australia.

Does Centrelink count as income for a mortgage?

Many lenders accept specific Centrelink payments as valid income, including the Disability Support Pension and Family Tax Benefit Parts A and B. While some banks “shade” these payments by only counting 80% of the value, others will accept 100% if the benefit is stable. You typically need to show you’ve received these payments for at least 12 months and that they’ll continue for at least five years to satisfy credit assessors.

How much deposit do I really need if I have a low income?

You can enter the market with as little as a 2% deposit if you qualify for the Family Home Guarantee or the Help to Buy scheme. For the standard First Home Guarantee, a 5% deposit is required to waive Lenders Mortgage Insurance. Having a smaller deposit is a viable path, provided you can demonstrate “genuine savings” over a 90 day period to prove your financial discipline to the bank.

Can I use a guarantor if I have a low income but a good deposit?

Yes, a guarantor can be a vital asset even if you have a healthy deposit. A guarantor doesn’t just replace a deposit; they provide additional security that can help you pass strict serviceability tests. This is a common strategy for low-income earners to access better interest rates or borrow a slightly higher amount than their salary alone would allow. It acts as a safety net for the lender and your partner in finance.

What happens if interest rates rise after I get my loan?

Lenders already account for potential rate rises by testing your application at 3% above the current market rate. This APRA-mandated buffer ensures you can still manage repayments even if the RBA raises the cash rate beyond the May 2026 level of 4.35%. We also help you explore fixed-rate options or offset accounts to provide a sense of security and control over your long-term financial journey as a homeowner.

Are there specific lenders that specialize in low-income home loans?

While no lender exclusively serves low-income earners, many Tier 2 and Tier 3 providers have more flexible policies for non-standard income. These smaller lenders often use manual underwriting rather than the rigid automated systems found at major banks. We provide access to 36+ lenders to find those who specialize in low-deposit solutions and complex income profiles. This is often the best way to learn how to get a home loan with a low income in australia.

Can I get a home loan while on a casual or probation work contract?

You can certainly get a loan while on a casual contract, provided you have a consistent 12 month work history in the same industry. Probation periods are more challenging, but some lenders will consider your application if you’ve moved between similar roles with no significant gaps. We focus on documenting your professional stability to show lenders that your income is reliable, even if your current contract is technically temporary or still in its early stages.