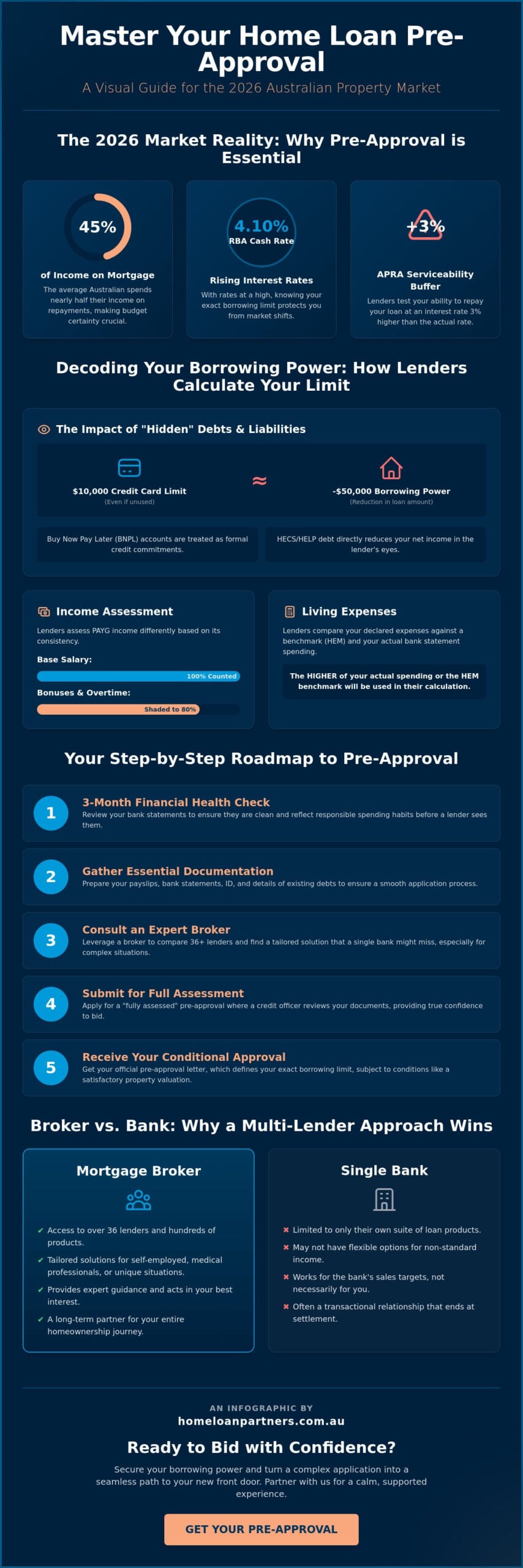

Did you know that as of March 2026, the average Australian now spends 45% of their income on mortgage repayments? With the RBA cash rate sitting at 4.10% and new APRA lending caps limiting high debt-to-income loans since February 1, understanding how to get a home loan pre-approval is the most critical step in your property journey. It’s natural to feel overwhelmed by the piles of paperwork or the fear that multiple applications might bruise your credit score. You want a clear green light to bid at auction without the nagging worry that your budget is based on guesswork.

We believe that securing your home should be a calm, supported experience rather than a stressful transaction. This guide provides you with an expert roadmap to master the pre-approval process and secure your borrowing power in the 2026 Australian property market. We’ll walk you through the essential documentation, explain how to navigate the latest lending regulations, and show you how a tailored approach can turn a complex application into a seamless path toward your new front door.

Key Takeaways

- Define your exact borrowing limit with a formal pre-approval to avoid the risk of searching in a shifting market without a clear financial boundary.

- Learn how lenders use a 3% serviceability buffer and evaluate hidden debts like Buy Now Pay Later accounts to determine your final loan amount.

- Explore why comparing over 36 lenders through a broker offers tailored solutions that single banks often miss, especially for self-employed buyers or medical professionals.

- Follow our step-by-step roadmap on how to get a home loan pre-approval, which includes a three-month financial health check to ensure your documents are bank-ready.

- Understand the value of a long-term partnership that provides a steady hand through the application process and continues to support your homeownership journey after settlement.

What is Home Loan Pre-Approval and Why is it Essential in 2026?

A home loan pre-approval is your lender’s written commitment to lend you a specific amount, subject to certain conditions. Think of it as a financial “green light” that defines your boundaries before you start visiting open homes. By understanding mortgage loans and the pre-approval process, you transform from a casual browser into a serious contender in a competitive market.

The 2026 property market requires a steady hand and precise data. With the RBA cash rate sitting at 4.10% as of March 2026 and potential increases on the horizon, searching without a limit is a significant risk. Since Australians now spend an average of 45% of their income on mortgage repayments, even a small shift in interest rates can impact what you can afford. Knowing how to get a home loan pre-approval ensures you aren’t guessing your budget while the market moves around you.

Lenders build your pre-approval on three pillars: your borrowing capacity, your creditworthiness, and your deposit size. It’s vital to distinguish between a “system-generated” estimate and a “fully assessed” pre-approval. A system estimate is just a computer’s guess based on basic data. A fully assessed pre-approval involves a credit officer actually reviewing your payslips and bank statements. This provides the level of certainty you need to bid with confidence.

The Strategic Advantage at Auctions and Private Sales

In the fast-paced 2026 market, real estate agents prioritize certainty over everything else. When you hold a formal letter of eligibility, you’re viewed as a “cash-like” buyer. This status is a powerful tool during negotiations. It allows you to set a firm “walk-away” price for auctions, preventing emotional overspending. Most agents won’t even present a private treaty offer to a vendor today without proof that your finance is ready to go.

Conditional vs. Unconditional Approval: Knowing the Difference

It’s important to remember that pre-approval is always “conditional.” The bank’s promise depends on several factors being met before they release the funds. Common conditions include a satisfactory property valuation, which typically costs between $100 and $600, and a final check to ensure your financial position hasn’t changed. If your deposit is under 20%, you’ll also need approval from a Lenders Mortgage Insurance (LMI) provider. Unconditional approval is the final, binding “yes” from the lender that occurs only after the contract is signed and all conditions are satisfied.

The 2026 Serviceability Reality: How Lenders Calculate Your Limit

Cracking the code of bank algorithms is the first step in learning how to get a home loan pre-approval that actually sticks. In 2026, lenders don’t just look at whether you can afford today’s repayments. They apply a strict “Serviceability Buffer” required by APRA. Currently, this buffer stands at 3%. This means if your actual interest rate is 6%, the bank assesses your ability to pay at 9%. It’s a safety net designed to protect you, but it significantly impacts your maximum borrowing capacity.

Your “Hidden Debts” often play a larger role than you might expect. Lenders look at your total credit card limits, not just the balance you owe. A $10,000 credit card limit can reduce your borrowing power by approximately $50,000, even if the card sits in a drawer unused. Similarly, Buy Now Pay Later (BNPL) services are now treated as formal credit commitments. Before applying, it’s wise to consult the CFPB’s guide to homeownership or similar expert resources to understand how these liabilities are viewed globally. For a more personalized look at your situation, our team at The Home Loan Partners can help you audit your current limits to maximize your result.

Living expenses are another critical factor. Lenders use the Household Expenditure Measure (HEM) as a benchmark. If your actual bank statements show higher spending than the HEM, they’ll use your real figures. If you have a HECS or HELP debt, remember that lenders view this as a direct reduction of your net take-home pay. It’s not just another line on your balance sheet; it’s a permanent dent in your monthly cash flow in the eyes of a credit officer.

Income Assessment in the Modern Economy

For PAYG employees, banks usually take 100% of your base salary but may only “shade” or count 80% of your overtime and bonuses. If you’re self-employed, two years of tax returns remain the gold standard for verification in 2026. If you’re buying an investment property, lenders will often factor in about 70% to 80% of the projected rental income to bolster your capacity.

Credit Scores and Comprehensive Credit Reporting (CCR)

Comprehensive Credit Reporting is now your best friend. It allows lenders to see your positive repayment history on utilities and phone bills, not just the negatives. However, “Enquiry Shopping” is a major trap. Every time you apply directly to a bank, it leaves a mark. Too many marks in a short period suggest financial distress. Checking your own report for errors before you start is a vital step in how to get a home loan pre-approval without unnecessary setbacks.

Broker vs. Bank: Why a Multi-Lender Approach Wins

When you walk into a local branch, you’re limited to a single set of rules and a handful of products. If your financial situation doesn’t fit that bank’s specific “box,” the conversation often ends with a rejection. A mortgage broker offers a completely different experience by providing access to over 36 lenders. This variety is the secret to how to get a home loan pre-approval that matches your unique financial DNA. Unlike bank staff who represent their employer, brokers are bound by the Best Interest Duty (BID). This legal requirement ensures we prioritize your needs over any single lender’s profit margins.

We act as your steady hand throughout the entire process. Instead of you spending hours on hold or trying to decode complex bank jargon, we manage the back-and-forth with credit assessors. We do the heavy lifting so you can focus on finding the right home. Our role is to be your expert partner, translating the complex requirements of various institutions into a clear, stress-free path forward. We don’t just submit an application; we package your financial story in a way that highlights your strengths to the right lender.

Navigating Different Lender Appetites

Every lender has a unique “appetite” for risk, which is reflected in their internal calculators. One major bank might offer you a borrowing limit of $600,000 based on their specific assessment of your overtime or bonuses. However, another lender on our panel might see the same data and offer $750,000. This discrepancy happens because some lenders have a “policy niche.” They might favor healthcare professionals, offer better terms for self-employed individuals, or be more flexible with low-deposit buyers. In the 2026 market, non-bank lenders are also vital for borrowers who require a higher borrowing capacity outside of standard APRA restrictions.

The Cost of a ‘Direct’ Rejection

A direct rejection from a bank isn’t just a “no”; it’s a permanent mark on your credit file. This can make your next application significantly harder as other lenders may see multiple enquiries as a red flag. We perform a “pre-flight check” on your application before it ever reaches a lender’s desk. This proactive approach identifies potential hurdles early, ensuring we only lodge an application when we’re confident in a “yes.” It’s also why relying on your current bank out of habit can be a mistake. You might find that Why Your Bank’s ‘Loyalty’ Discount Might Be Costing You Thousands compared to a more competitive offer tailored to your specific goals.

The Step-by-Step Roadmap to Securing Your Pre-Approval

Success in the 2026 property market begins long before you attend your first open home. Understanding how to get a home loan pre-approval requires a proactive approach that starts at least three months before you intend to buy. This preparation phase is your opportunity to “clean” your financial profile. Since the APRA debt-to-income regulations took effect on February 1, 2026, lenders are scrutinizing bank statements more closely than ever. By reducing credit card limits and pausing Buy Now Pay Later accounts 90 days out, you present a polished, low-risk profile to credit assessors. Once you’re ready to move forward, you can book your obligation-free consultation with our team to map out your specific goals.

The roadmap follows a logical flow designed to build your confidence. After your initial health check, we move to document gathering. This is followed by a broker consultation where we compare over 36 lenders to find your perfect match. Once we submit your application, the bank’s assessment team reviews your data, which typically takes between two and seven business days. Finally, you receive your Letter of Eligibility. This document is your shield at auctions; it clearly states your borrowing limit and the conditions you must meet for final approval.

The ‘Golden Portfolio’: Your Documentation Checklist

Lenders in 2026 require a “Golden Portfolio” of digital documents to verify your stability. Providing these upfront prevents the back-and-forth that often delays applications. Ensure you have the following ready:

- Proof of Identity: A valid Australian Passport or Driver’s License; some lenders also accept Proof of Age cards.

- Proof of Income: Your last 2-3 consecutive payslips and your most recent Income Statement from the ATO.

- Proof of Savings: 3-6 months of bank statements showing “genuine savings” for your deposit.

- Liabilities: Recent statements for all credit cards, personal loans, and your current HECS/HELP balance.

Post-Approval: What NOT to do

Receiving your pre-approval letter is a milestone, but it’s not a final “yes.” Most 2026 pre-approvals are valid for exactly 90 days. If you haven’t found a home in that window, we can help you “roll over” the application, though this may require updated payslips. The most critical rule is to maintain your financial status quo. Do not change jobs, even for a higher salary, as most lenders require you to be out of a probation period. Avoid taking out new credit for furniture or a car, as this will trigger a reassessment of your borrowing capacity and could lead to a sudden decline of your loan.

Partnering for Success: How The Home Loan Partners Guide You

At The Home Loan Partners, we don’t view a mortgage as a simple transaction. We see it as the foundation of your future and the start of a long-term collaboration. When you’re researching how to get a home loan pre-approval, you’re looking for more than a piece of paper; you’re looking for the confidence to make one of life’s biggest decisions. Our team acts as your steady guide, navigating the complexities of the 2026 market with professional precision and a personal touch. We stay by your side from the first conversation through to settlement and beyond, ensuring your loan continues to serve you as your life evolves.

Our access to over 36 lenders means we don’t try to fit you into a pre-packaged product. Instead, we search the market to find a solution tailored to your specific financial DNA. This variety is essential in 2026, where lender appetites change frequently in response to RBA shifts. We provide unbiased, expert advice that prioritizes your goals. By handling the bank negotiations and the overwhelming paperwork, we deliver a seamless experience that removes the inherent stress of the mortgage process. You can focus on the excitement of finding your home while we do the heavy lifting in the background.

Tailored Loan Structures for Your Future

We believe that a successful pre-approval looks beyond the “maximum borrowing” figure. While knowing your limit is vital, we also focus on finding a repayment structure that fits your daily lifestyle and future aspirations. This involves a strategic look at loan features that can save you thousands in interest over the life of the loan. For example, understanding the nuances of Redraw vs Offset Account: Which Is Better For You? is a key part of our strategy session. We’ll help you decide which facility aligns with your savings habits and tax requirements, ensuring your loan remains flexible and efficient as you pay it down.

Ready to Start Your Journey?

Taking the first step toward homeownership shouldn’t feel like a leap into the unknown. We invite you to an obligation-free consultation where we’ll assess your borrowing power and clarify your options in the current market. It’s important to understand our “Upfront Commission” model: our professional service is typically at no cost to you, as the lender pays us for the work we do in preparing and managing your application. This ensures you receive expert guidance without an added financial burden. When you’re ready to move forward with clarity and support, Book your free pre-approval strategy session with The Home Loan Partners to secure your path home.

Take the First Step Toward Your New Home Today

Navigating the Australian property landscape requires more than just hope; it demands a strategic roadmap. We’ve explored how the serviceability buffer and rigorous documentation checks define your borrowing power in a market influenced by the latest APRA regulations. By mastering how to get a home loan pre-approval, you’ve already taken the most important step toward financial certainty and auction-day confidence. You now know that a broker-led approach provides access to over 36 leading Australian lenders, ensuring your application is tailored to your specific needs rather than a bank’s rigid policy.

Our team at The Home Loan Partners is legally bound by the Best Interest Duty. This means our expert guidance is always focused on your long-term security and personal goals as you navigate the 2026 property market. We do the heavy lifting by managing complex negotiations and bank assessors so you can focus on finding the right property. Start your stress-free pre-approval journey with our expert partners today and move forward with a steady hand. Your dream of homeownership is within reach, and we’re here to guide you every step of the way.

Frequently Asked Questions

Does getting a home loan pre-approval hurt my credit score?

Yes, a formal pre-approval involves a “hard” credit enquiry which is recorded on your credit report. While a single enquiry is a standard part of how to get a home loan pre-approval, making multiple applications to different banks in a short window can lower your score. We help protect your credit file by identifying the single most suitable lender before lodging your application, ensuring your record stays healthy.

How long does a home loan pre-approval last in Australia?

Most Australian pre-approvals are valid for 90 days from the date the letter is issued. If you haven’t found a property within this three-month window, we can often request a 90-day extension for you. This process usually requires providing your most recent payslips to prove your income remains stable, as lenders want to ensure your borrowing power hasn’t shifted in the current market.

Can I bid at an auction with only a pre-approval?

You can bid at an auction with a pre-approval, and it’s a vital tool for setting your “walk-away” price. It gives you the confidence to bid up to your limit without the stress of financial guesswork. Just remember that the approval is still conditional on a satisfactory property valuation. We recommend having the contract reviewed before the auction to ensure the property meets your lender’s specific guidelines.

What happens if my financial situation changes after getting pre-approved?

Any major change to your income or debt will likely void your pre-approval. This includes switching jobs, even for a higher salary, or taking out new credit for a car or personal loan. If your circumstances shift, it’s essential to contact your partner at Home Loan Partners immediately. We’ll work with the lender to reassess your position and update your eligibility letter to reflect your new situation.

Is pre-approval a guarantee that I will get the loan?

Pre-approval is not a final guarantee of funding because it’s a “conditional” agreement. The bank’s final “yes” depends on a satisfactory valuation of the property you choose and a final check of your financial status. If a property valuation comes in lower than the purchase price, the lender may reduce the loan amount. We guide you through these final hurdles to ensure a smooth transition to settlement.

How much deposit do I need for a pre-approval in 2026?

While a 20% deposit is ideal to avoid Lenders Mortgage Insurance (LMI), you can often secure pre-approval with as little as 5%. As of May 2026, eligible buyers can still access the federal Home Guarantee Scheme, which allows for deposits as low as 5%, or 2% for single parents, without paying LMI. We’ll help you determine the exact deposit required based on your savings and any available government grants.

Why would a bank reject my pre-approval application?

Rejections often occur due to serviceability issues or high debt-to-income ratios. Since the APRA regulations updated on February 1, 2026, lenders are strictly limiting loans where debt exceeds six times your annual income. Other common reasons include poor credit history or undisclosed liabilities like Buy Now Pay Later accounts. We perform a thorough “pre-flight check” of your finances to catch these potential issues before we submit your application.

Can I get pre-approval if I am self-employed or a contractor?

You can definitely secure pre-approval as a self-employed borrower or contractor, though the documentation is more detailed. Most lenders require two years of tax returns and Business Activity Statements to verify your income. Some specialist lenders on our panel offer “alt-doc” options for those with shorter trading histories. We’ll partner with you to find the lender that best understands your business structure and rewards your hard work.