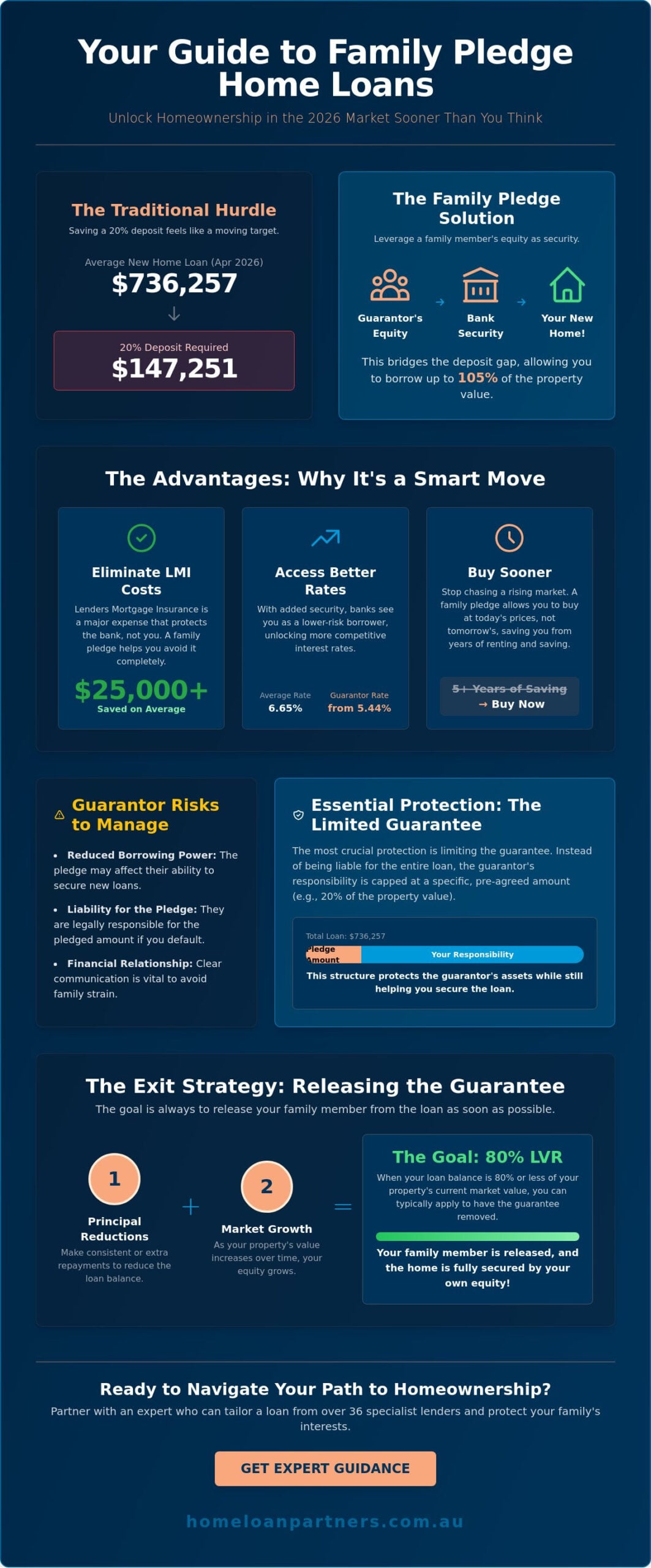

What if the traditional 20% deposit isn’t a mandatory requirement, but an outdated hurdle that’s keeping you stuck in the rental cycle? In a market where the average new home loan has reached $736,257 as of April 2026, saving a six figure sum often feels like a moving target. You likely feel the pressure of rising prices and the stress of Lenders Mortgage Insurance (LMI) costs eating into your future security. Understanding the family pledge home loan pros and cons is the first step toward realizing that your property journey can begin much sooner than you expected with the right partner by your side.

We’re here to act as your steady guide through this significant financial decision to ensure your family’s interests are protected. This guide provides a balanced look at how a guarantor can help you secure variable rates starting from 5.44% while potentially borrowing up to 105% of the purchase price to cover costs like stamp duty. You’ll discover how to navigate the legal responsibilities involved and, most importantly, how to structure a seamless exit strategy to release your family members from the loan as soon as your equity grows. Our goal is to help you move forward with the confidence and clarity you deserve.

Key Takeaways

- Understand how a family pledge bridges the 20% deposit gap by using a portion of a family member’s equity as additional security.

- Weigh the family pledge home loan pros and cons to see how you can save tens of thousands in Lenders Mortgage Insurance (LMI) costs.

- Identify the specific risks to a guarantor’s borrowing power and learn the essential steps to protect their financial future.

- Master the exit strategy by focusing on principal reductions and market growth to release the guarantee as quickly as possible.

- Partner with an expert to navigate the legal complexities and access a tailored loan structure from over 36 specialist lenders.

What is a Family Pledge Home Loan in the 2026 Market?

A family pledge home loan is a strategic financial partnership where a family member, typically a parent, offers a portion of their home equity as additional security for your mortgage. In the April 2026 property market, where the average new home loan has climbed to $736,257, this arrangement has become a vital tool for first-time buyers. It essentially bridges the gap between the small deposit you’ve saved and the 20% threshold required by lenders to avoid costly Lenders Mortgage Insurance (LMI). By using this structure, you’re effectively leveraging the “Bank of Mum and Dad” without requiring them to provide a large lump sum of cash up front.

The 2026 landscape has seen a significant shift in how these loans are used. With variable interest rates for guarantor loans starting as low as 5.44% as of April 28, 2026, many families find this a more sustainable path than watching their children struggle in the rental market. When weighing the family pledge home loan pros and cons, it’s important to distinguish between a full guarantee and a limited pledge. A limited pledge is often the preferred choice for our clients because it restricts the guarantor’s liability to a specific dollar amount, rather than the entire loan balance. This limits the risk to the family member’s assets while still providing you with the boost needed to secure a home.

The Core Mechanics: Equity vs. Cash

One of the most reassuring aspects of this arrangement is that your guarantor doesn’t need to hand over physical cash. Instead, the bank uses the equity in their existing property as a “pledge.” Lenders calculate this amount based on a strict Loan-to-Value Ratio (LVR), ensuring that the combined security of your new home and the pledged equity meets their internal safety margins. As the mortgagee, the bank holds a registered interest in both properties. This doesn’t mean your parents lose control of their home; it simply means their equity acts as a safety net that allows you to borrow up to 105% of the property value to cover purchase costs like stamp duty.

Who Can Be a Guarantor?

To understand what is a guarantor in a legal sense, it’s helpful to view them as a secondary layer of security for the lender. Most Australian banks prefer immediate family members, such as parents or siblings, though some specialist lenders may consider grandparents or even adult children. Each lender has unique rules regarding how much equity the guarantor must own. Crucially, the bank will also assess the guarantor’s serviceability. They need to ensure that the family member can comfortably manage their own financial obligations alongside the potential liability of the pledge. This protective measure ensures the arrangement is sustainable for everyone involved in the long-term journey.

The Pros: Why Thousands of Australians Choose Family Pledges

Choosing a path to homeownership often feels like a race against time. By evaluating the family pledge home loan pros and cons, you’ll see why many Australians are skipping the years of saving and jumping straight into the market. The primary advantage is the ability to bypass the traditional 20% deposit requirement. In April 2026, where the average new home loan has reached $736,257, saving a full deposit while paying rent is a monumental task. A family pledge allows you to enter the market with a minimal deposit, or even $0 in some cases, by leveraging the equity your parents have already built.

Speed is your greatest ally in a rising market. While you might spend five years saving an extra $100,000, property prices often climb faster than your savings rate. By using a guarantor, you can buy at today’s prices rather than tomorrow’s. Additionally, these loans often unlock more competitive interest rates. While the average variable rate is 6.65%, guarantor loans can start from as low as 5.44%. This lower rate applies because the bank views the loan as a lower risk when it’s backed by additional security. You can even borrow up to 105% of the property value to cover essential costs like stamp duty and legal fees, which keeps your liquid cash available for renovations or an emergency fund.

Financial Benefits for the Borrower

The most immediate win is the total removal of Lenders Mortgage Insurance (LMI). For a loan of $736,257 with a small deposit, LMI could easily cost you upwards of $25,000. This is a non-refundable fee that protects the bank, not you. By avoiding it, you keep that wealth in your pocket. You’ll also find that your monthly repayments are more manageable because of the tiered interest rates usually reserved for those with 20% equity. This financial breathing room makes the transition from renting to owning far less stressful. If you’re ready to see how these numbers look for your specific situation, our team can help you compare tailored options from our panel of 36 lenders.

Benefits for the Family Unit

A family pledge is often a more practical way for parents to help their children than providing a cash gift. It allows parents to support your homeownership goals without depleting their own retirement savings or liquidating investments. This keeps family wealth working within the property market across generations. While it’s a generous act, it’s vital that everyone understands the risks for the guarantor before signing. Once you’ve built up 20% equity through a combination of repayments and capital growth, the guarantee can be released. At that point, the “pledge” effectively becomes a gift of independence, allowing your parents to step back while you hold full ownership of your home.

The Cons and Risks: Protecting the Guarantor’s Future

While the benefits of entering the property market sooner are compelling, a balanced view of the family pledge home loan pros and cons requires a serious discussion about the risks involved. A family pledge isn’t just a paperwork formality; it’s a legal commitment that ties your guarantor’s financial security to your mortgage. If you fall behind on repayments and default, the bank has the right to look to your guarantor to satisfy the pledged portion of the debt. In extreme scenarios, this could lead to the forced sale of the guarantor’s home to cover the shortfall. This reality can place an immense emotional burden on family relationships if expectations aren’t clearly managed from the start.

Beyond the risk of default, there’s the immediate impact on the guarantor’s credit profile. Banks view a guarantee as a contingent liability. This means if your parents decide to take out a loan for a new car or a renovation in late 2026, their borrowing capacity is reduced by the specific dollar amount they’ve pledged for your home. It’s a weight on their financial freedom that remains until the guarantee is formally released. For a parent nearing retirement, this reduction in flexibility is a significant factor to weigh against the desire to help their children buy a home.

The Impact on the Guarantor’s Lifestyle

Acting as a guarantor can complicate a parent’s plans to downsize or refinance their own mortgage. Because the bank holds a registered interest in their property as security, any major change to their title requires lender approval. This is why we facilitate a process where every guarantor must seek independent legal and financial advice. Most lenders won’t proceed without a signed Statutory Declaration confirming this advice was received. It protects the family dynamic by ensuring everyone understands the guarantor home loan pros and cons from a neutral, professional perspective before any documents are signed.

Borrower Risks: The ‘Negative Equity’ Trap

You also face specific risks as the borrower. In the April 2026 market, where the average loan is $736,257, a slight dip in property prices could lead to a negative equity trap. If your home’s value falls shortly after purchase, your Loan-to-Value Ratio (LVR) increases. This makes it much harder to refinance or remove the guarantee as planned. You might find yourself locked in to your current lender because other banks may not accept a pledge loan transfer when the equity is low. Even with a guarantor, your serviceability remains the primary hurdle. The bank still needs to see that you can comfortably afford the 6.65% average variable rate on your own income, regardless of the extra security provided by your family.

Building a Release Strategy: How to Exit the Guarantee

A family pledge is designed to be a strategic bridge to homeownership, not a lifelong financial obligation for your parents. While weighing the family pledge home loan pros and cons, the most vital consideration is how and when you’ll release the guarantor from the loan. This transition doesn’t happen automatically; it requires a proactive plan and regular monitoring of your property’s performance. Our role as your expert partner is to help you navigate this exit strategy so your family can regain their full financial independence as quickly as possible.

The journey to releasing a guarantee follows a logical path of equity building. You can accelerate this process through four key steps:

- Focus on principal reductions: Every extra dollar you pay into your loan increases your equity share and reduces the bank’s reliance on the pledge.

- Monitor market value: In the April 2026 market, capital growth is often the fastest way to reach the required equity threshold. Even modest price increases can significantly shift your position.

- Formal valuation: Once you believe your equity has grown, we’ll help you request a formal bank valuation to confirm the property’s current worth.

- The Application for Release: When the numbers align, you must submit a formal application to the lender to remove the guarantor’s name from the title.

The 80% LVR Milestone

In the Australian lending landscape, 80% Loan-to-Value Ratio (LVR) is the magic number. Once your loan balance represents 80% or less of your property’s value, most banks will release a guarantor without charging you Lenders Mortgage Insurance. You can reach this milestone faster by using an offset account to lower your interest costs or by making consistent additional repayments. It’s vital to remember that a release is not automatic; you must actively manage this process with your lender to ensure the guarantee is removed the moment you’re eligible. If you’re unsure where your equity stands, you can book a strategy session with our team to review your current LVR.

Alternative Exit Routes

There are several ways to speed up the release if market growth is slower than expected. You might use a lump sum, such as a work bonus or an inheritance, to pay down the pledged portion of the debt immediately. Another common route is refinancing to a different lender. If your current bank’s valuation feels conservative, moving to a new lender can often unlock a more favorable valuation and a cleaner exit for your family. We recommend reviewing your loan every 12 months to ensure you’re on the most efficient path toward full independence. This regular check-in ensures that the family pledge home loan pros and cons stay balanced in your favor throughout the life of the guarantee.

How Home Loan Partners Guide Your Family Through the Process

Buying a home with family support is a deeply personal journey, and we treat it as such. While you focus on the excitement of your new property, we manage the intricate details of the lending process to ensure a seamless experience. Our team provides access to over 36 specialist lenders, each with vastly different rules for family pledges. This is a critical advantage because big banks often only offer a one size fits all approach. By comparing the family pledge home loan pros and cons across multiple institutions, we find the specific structure that aligns with your family’s unique financial goals and risk tolerance.

We often act as the essential “middle man” during this process. Conversations about money and property can be stressful, even between the closest family members. We facilitate these discussions with a calm, expert hand, ensuring that both the borrower and the guarantor feel heard and protected. Our focus on compliance means we don’t just push paperwork through; we ensure every party has the required legal protections and independent advice in place. This steady guidance alleviates the inherent stress of the mortgage process, allowing you to focus on the long term journey ahead.

Tailored Loan Structures

Not all guarantees are created equal. We help you compare lenders who offer limited guarantees, which cap the guarantor’s liability, versus those that might require more extensive security. We also prioritize lenders with favorable release of guarantee policies, ensuring your parents have a clear path to independence once your equity reaches that 80% threshold. By structuring offset accounts correctly from day one, we help you maximize interest savings. This directly accelerates your principal reductions and brings the release date closer, saving you money while protecting your family’s assets.

Your Partners for the Long Term

Our commitment to your family doesn’t end when you get the keys. We view settlement as the beginning of a partnership that lasts for the life of your loan. We conduct annual reviews to check your property’s value and your loan balance, proactively identifying the moment the guarantor can be released. In the April 2026 market, staying informed is your best defense against rising costs. We provide unbiased advice to help you navigate this environment with confidence and precision. If you’re ready to take the next step toward homeownership, you can Book a consultation with The Home Loan Partners today and let us guide you home.

Securing Your Place in the 2026 Property Market

Navigating the property landscape requires more than just savings; it demands a strategic vision for your family’s future security. By now, you’ve seen how understanding the family pledge home loan pros and cons can transform your approach to homeownership. You don’t have to wait years to save a 20% deposit while prices continue to climb. Instead, you can leverage family equity to bypass Lenders Mortgage Insurance and secure more competitive interest rates today. The key to success lies in having a clear, documented plan to release your guarantor as your property value grows.

At Home Loan Partners, we act as your steady hand throughout this entire process. We provide access to over 36 leading Australian lenders to find the tailored structure that fits your needs perfectly. Our experts guide you and your family through the difficult conversations and ensure every legal protection is in place for the long-term journey. We’re committed to your success well beyond settlement day. Start your home ownership journey with a free expert consultation and let us help you achieve the Australian dream with confidence and clarity. Your new front door is closer than you think.

Frequently Asked Questions

Is a family pledge the same as a guarantor loan?

Yes, a family pledge is simply a branded term used by certain lenders for a guarantor loan. It describes the same legal arrangement where a family member uses their home equity to secure a portion of your mortgage. This structure is a cornerstone of the Australian market, helping many of the 66% of households who are homeowners pass that security down to the next generation.

Can my parents be released from the guarantee early?

Your parents can be released as soon as your loan balance represents 80% or less of your property’s current market value. This milestone can be reached through a combination of your regular principal repayments and natural capital growth in the property market. We recommend requesting a formal valuation every 12 to 24 months to track your progress toward this goal.

Does the guarantor need to have their own home loan with the same bank?

No, your guarantor doesn’t need to move their existing mortgage to your new lender. While having both loans with the same bank can sometimes speed up the internal paperwork, it isn’t a requirement. We work with a panel of 36 lenders, many of whom are comfortable taking a second mortgage over a guarantor’s property while their primary loan remains elsewhere.

What is the maximum amount I can borrow with a family pledge?

You can typically borrow up to 105% of the property’s purchase price when using this structure. This allows you to cover the full cost of the home plus additional expenses like stamp duty and legal fees. When weighing the family pledge home loan pros and cons, the ability to enter the market with no cash deposit is often the most significant advantage for our clients.

What happens if I can’t make my mortgage repayments?

The bank will first look to sell your property to recover the outstanding debt if you default on the loan. If the sale price doesn’t cover the full balance, the guarantor is then legally responsible for paying the specific portion they pledged. This is why we facilitate a process where every guarantor receives independent financial advice to ensure they’re comfortable with this responsibility.

Do my parents need to have a certain amount of equity in their home?

Lenders generally require guarantors to have at least 20% to 30% equity remaining in their home after the pledge is factored in. This buffer ensures that their own financial position remains secure even while they’re supporting your loan. We’ll help you calculate your parents’ usable equity early in the process so you know exactly what your borrowing capacity looks like.

Can I use a family pledge for an investment property or only a home to live in?

Most Australian lenders restrict family pledges to owner-occupied properties where you intend to live. While a small number of specialist lenders may consider investment scenarios, the primary purpose of these loans is to help first-home buyers escape the rental trap. We can help you identify which lenders on our panel currently support investment pledge structures if that’s your goal.

Are there extra fees for setting up a family pledge home loan?

You’ll likely encounter additional costs for things like a second property valuation and independent legal advice for your guarantor. There may also be a small guarantee processing fee charged by the lender. These upfront costs are usually minor when you consider the $25,000 or more you’ll likely save by not having to pay Lenders Mortgage Insurance.