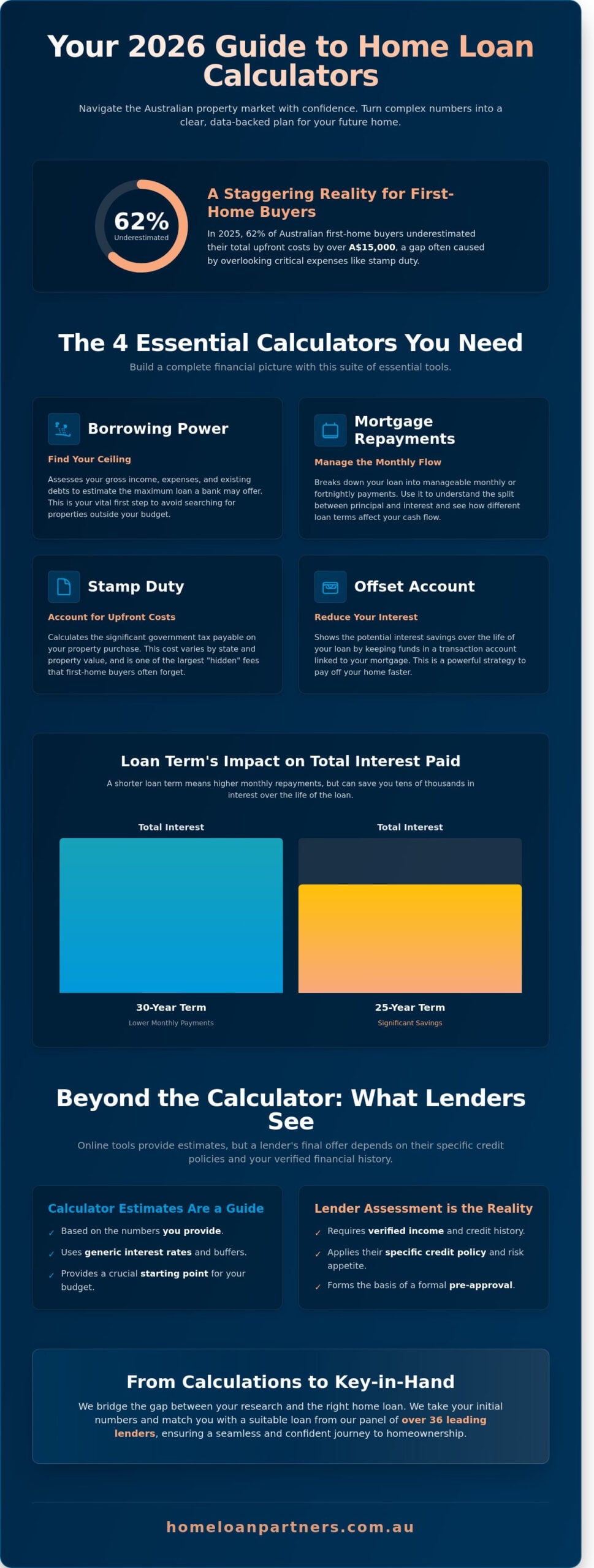

Did you know that 62% of Australian first-home buyers in 2025 underestimated their total upfront costs by more than A$15,000? It’s a staggering figure that highlights how quickly hidden fees like stamp duty can derail a property dream. You likely feel the weight of these numbers already, especially when trying to find a reliable home loan calculator that actually accounts for every variable. It’s completely normal to feel confused by shifting interest rates or the sheer volume of different tools available online. We believe that your journey toward homeownership should be defined by confidence, not guesswork.

We’ve designed this guide to help you master these digital tools so you can step into the 2026 market with a clear, data-backed plan. You’ll learn how to accurately estimate your borrowing power, calculate true entry costs, and discover specific strategies to reduce your interest payments over time. By the time you finish reading, you’ll have a professional’s understanding of your budget and the steady hand of an expert partner to guide your next move. We’ll show you exactly which calculators matter most and how to use them to secure your financial future.

Key Takeaways

- Use a home loan calculator as your essential first step to stress-test your finances and gain a realistic view of your borrowing capacity.

- Discover the four essential tools required to build a complete financial picture, from upfront costs like stamp duty to long-term interest savings.

- Understand the impact of “Lender Policy” and why your final bank offer might differ from generic online results.

- Learn how to turn your raw data into a conservative, future-proof property strategy tailored to the 2026 Australian market.

- Explore how to transition from DIY calculations to a professional partnership that provides access to over 36 leading lenders for a seamless experience.

Why a Home Loan Calculator is Your Vital First Step in 2026

Starting your property journey in 2026 requires more than just a wishlist of suburbs and floor plans. A home loan calculator serves as a sophisticated financial modelling tool designed specifically for the Australian market. It translates complex interest rates, bank fees, and loan terms into a clear monthly figure. By running your own numbers first, you perform a personal stress-test. This happens well before a credit provider scrutinizes your bank statements. It gives you the confidence to walk into an open home in Melbourne or Perth knowing exactly where your financial limit lies.

Knowledge is your greatest asset when negotiating with real estate agents. When you understand how loan calculators work to determine your principal and interest split, you move from a place of hope to a position of power. You aren’t just guessing what you can afford; you’re following a mathematical map. At Home Loan Partners, we view these tools as the first step in our collaborative journey. While the math provides the map, your broker acts as the navigator, ensuring you don’t miss the hidden turns in the lending landscape.

The Psychology of the Property Search

Property hunting often feels like an emotional rollercoaster. Seeing hard data in black and white reduces the fear of the unknown that often paralyzes first-time buyers. Using a home loan calculator helps household members align their goals early. It shifts the conversation from a vague “Can we afford this?” to a strategic “How should we structure this?”. This clarity is essential in 2026, as buyers manage the balance between lifestyle aspirations and the reality of a 3% serviceability buffer required by APRA regulations.

Calculators vs. Pre-Approval: Knowing the Difference

It’s easy to mistake a positive result on a digital screen for a guaranteed loan. A calculator provides a helpful estimate based on the data you input, but it doesn’t account for a bank’s specific credit policies or your living expense benchmarks. Pre-approval is a formal, conditional commitment from a lender after they’ve verified your A$100,000 salary and credit history. We bridge this gap by taking your initial calculations and matching them with a lender whose policy fits your unique profile. This ensures your property journey remains seamless and stress-free from the first click to the final settlement.

The 4 Essential Calculators Every Australian Home Buyer Needs

Planning a property purchase in Australia involves more than just looking at a sticker price. To build a clear financial roadmap, you need a suite of tools that talk to each other. Using a single home loan calculator provides one piece of the puzzle, but combining four specific tools creates a full picture of your future. The Home Loan Partners provide these resources to simplify your journey and ensure you’re making decisions based on Australian tax laws and current lending criteria.

1. Borrowing Power Calculator: Finding Your Ceiling

This tool assesses your gross income, regular expenses, and existing debts to estimate what a bank will lend you. It accounts for the 3.00% serviceability buffer required by regulators as of 2026. Borrowing Power is the maximum amount a lender is likely to offer based on current 2026 serviceability buffers. Knowing this number prevents you from falling in love with a property that’s financially out of reach. Check our guide on how to use a borrowing power calculator accurately to get a realistic figure before you start inspecting homes.

2. Mortgage Repayment Calculator: Managing the Monthly Flow

While borrowing power tells you the total amount, this tool focuses on your recurring budget. It breaks down the difference between principal and interest payments versus interest-only options. You’ll see how a 30-year term keeps monthly costs lower but results in significantly higher interest over time compared to a 25-year term. For an independent perspective, Moneysmart’s Mortgage Calculator offers a reliable way to verify these figures. You can also use our mortgage repayment calculator to estimate your costs based on 2026 interest rates.

3. Stamp Duty and Offset Calculators

Stamp duty is the largest hidden cost in a property transaction. Because these taxes vary by state, using a localized home loan calculator for your specific region, like our NSW stamp duty calculator, is vital for accuracy. Once you’ve secured your home, an offset calculator becomes your most powerful tool. It demonstrates how keeping cash in a linked account reduces the interest charged on your loan balance. This strategy can shave years off your mortgage and save you thousands in the long run. If you’re feeling overwhelmed by the numbers, our team can help you find a tailored loan structure that fits your lifestyle.

The Limitations of DIY Math: What Your Online Calculator Won’t Tell You

Many clients feel a sense of confusion when their formal bank offer arrives with a lower figure than their initial home loan calculator results suggested. This gap exists because a generic tool can’t account for the unique “Lender Policy” guidelines that vary across Australia’s 100+ mortgage providers. While an Australian Government mortgage calculator provides a reliable baseline for repayments, it doesn’t see your credit report or employment contract. A credit score below 620 or a high volume of recent credit inquiries can lead a bank to increase your interest rate or reduce your loan-to-value ratio, regardless of what the DIY math says.

Lenders look at the quality of your income with a critical eye. If you’re a casual worker or a freelancer with 18 months of history, some banks might discount your income by 20% to account for potential volatility. In contrast, a permanent employee with a 3-month tenure is often viewed as lower risk. Most online tools also ignore Lenders Mortgage Insurance (LMI). If your deposit is under 20%, LMI can add between A$12,000 and A$35,000 to your total loan cost. This isn’t just a fee; it’s a structural change to your loan that alters your monthly commitment and your total debt level. Working with a qualified finance broker helps you navigate these hidden variables and find lenders whose policies align with your unique financial profile.

The ‘Serviceability Buffer’ Reality

Banks don’t test your ability to pay at the current market rate. Under APRA’s October 2021 guidelines, lenders apply a minimum 3% serviceability buffer. If your actual interest rate is 6.15%, the bank calculates your repayments at 9.15%. This safety net ensures you can handle future economic shifts. It’s the primary reason a home loan calculator might suggest a borrowing capacity of A$1,000,000, while a bank’s formal assessment caps you at A$840,000. We guide you toward lenders whose internal math is more generous toward your specific financial profile.

Living Expenses: The HEM vs. Reality

The Household Expenditure Measure (HEM) is the benchmark banks use to estimate your cost of living based on your family size and location. However, lenders now scrutinize three to six months of actual bank statements. If your spending on discretionary items like A$120 monthly gym memberships or frequent A$60 food delivery orders exceeds the HEM, the bank uses your higher “actual” figure. This reduces your borrowing power. A calculator’s default expense setting is often an optimistic estimate that doesn’t reflect the A$2,800 monthly reality for many Australian families. We act as your expert partner to ensure your application reflects a realistic and bank-friendly view of your lifestyle.

How to Use Calculator Results to Build Your 2026 Property Strategy

Once you’ve used a home loan calculator to see your potential borrowing power, the real work begins. Your goal isn’t just to find the biggest number a bank might lend you. It’s about crafting a plan that protects your lifestyle while securing your future. Think of these results as the foundation of your “Property Brief,” the document we use to match you with the right lender and product for your specific needs.

Step 1: Determine Your ‘Comfort Zone’ Repayment

Banks often approve loans that stretch your budget to its absolute limit. In the 2026 market, we recommend a more conservative approach. Don’t just calculate what you can pay; decide what you want to pay. A common benchmark for financial health is the 30% rule. This suggests keeping your total housing costs below 30% of your gross household income to avoid mortgage stress.

For a couple earning a combined A$165,000 per year, this means aiming for repayments around A$4,125 per month. Keeping your target within this zone ensures you still have funds for A$5,000 annual holidays, unexpected car repairs, or rising grocery bills. We want you to enjoy your new home, not feel trapped by it. By setting a “comfort zone” repayment figure, you maintain control over your quality of life from day one.

Step 2: Factor in the ‘Entry’ and ‘Exit’ Costs

Your home loan calculator results usually focus on the loan amount, but your “Cash to Complete” is the figure that actually gets you the keys. This total includes your deposit, stamp duty, and legal fees. In 2026, savvy buyers are adding a mandatory A$10,000 buffer to their initial savings goal. This extra cushion covers hidden costs like building inspections, moving expenses, or immediate minor repairs after settlement.

You also need a clear exit strategy for different economic cycles. If interest rates were to climb by another 1.5% in the future, could your budget handle the shift? We help you stress-test these numbers now so you aren’t forced into a difficult sale later. When you bring your calculator results to us, we treat them as a starting point. We’ll help you refine these figures into a professional brief that shows lenders you’re a prepared, low-risk borrower.

Ready to turn these numbers into a reality? Partner with our expert team to refine your 2026 property strategy today.

From Calculations to Key-in-Hand: How The Home Loan Partners Step In

A home loan calculator offers a vital starting point for your “what if” scenarios. It helps you visualize the impact of an extra A$250 monthly repayment or a 0.5% interest rate shift. However, a digital tool cannot negotiate with a credit assessor or interpret the nuances of your specific career path. We take those initial numbers and stress-test them against our panel of 36+ Australian lenders, ranging from major institutions like ANZ and NAB to boutique credit unions. Our role is to bridge the gap between a digital estimate and a formal approval letter.

We view ourselves as your long-term partner rather than a one-time service provider. We don’t just look for a loan that fits today; we structure your debt to support where you want to be in five or ten years. This collaborative approach ensures that your mortgage remains a tool for wealth creation rather than a source of financial stress. We take the heavy lifting out of the process, providing a steady hand as you move from research to reality. Understanding how to choose the right finance broker in Australia can make the difference between a loan that merely fits and one that actively builds your long-term wealth.

The Value of a Tailored Loan Structure

Interest rates often dominate the headlines, but they’re only one part of a successful strategy. A loan with the lowest advertised rate might lack an offset account, which could potentially cost you A$45,000 or more in interest over a 30-year term if you hold significant savings. We look beyond the surface to find features like redraw facilities and flexible repayment structures that align with your lifestyle. The “cheapest” loan on a screen often becomes the most expensive if it doesn’t allow for the flexibility you need as your family or career grows. Our ongoing support includes:

- Annual Health Checks: we review your interest rate every 12 months to ensure it remains competitive against new market offers.

- Feature Optimization: we match you with accounts that include multiple sub-offsets if that suits your budgeting style.

- Future-Proofing: we select lenders that offer easy pathways for future equity release or property portfolio expansion.

Your Next Step: A Seamless Strategy Session

Your journey continues with a low-pressure strategy session. This is a 15-minute verification call where we review your DIY math from the home loan calculator and ensure it stands up to the latest bank servicing criteria. It’s not a sales pitch; it’s a professional sanity check to give you confidence before you start bidding at auctions. We take the weight of the paperwork off your shoulders, managing every interaction with the lender so you can stay focused on finding the right property. Our goal is to make the transition from calculation to settlement feel steady, logical, and entirely within your control. You’ve done the hard work of planning; now let us provide the expert hand to guide you home.

Take the Next Step Toward Your 2026 Property Goals

Navigating the Australian property market in 2026 requires more than just a rough estimate of your borrowing power. While a home loan calculator provides a vital baseline for your budget, it’s only the beginning of a secure financial strategy. Real success comes from understanding how variables like interest rate shifts and specific lender policies impact your long term goals. You shouldn’t have to navigate these complexities alone.

At Home Loan Partners, we bridge the gap between digital estimates and a settled mortgage. We provide access to over 36 Australian lenders to ensure your loan structure is both professional and stress free. Whether you’re a first home buyer looking for your first set of keys or an investor expanding a portfolio, our expert guidance turns raw data into a tailored roadmap. We handle the heavy lifting so you can focus on finding the right home.

Book a Seamless Strategy Session with Your Home Loan Partners

We’re ready to help you turn your 2026 property dreams into a reality with confidence and clarity.

Frequently Asked Questions

Are home loan calculators accurate for Australian borrowers in 2026?

Home loan calculators provide a reliable estimate based on current 2026 market data, but they serve as a starting point rather than a final approval. Banks apply a 3% serviceability buffer as mandated by APRA to ensure you can manage repayments if interest rates rise. While these tools offer a clear snapshot of your potential monthly commitments, your actual interest rate depends on your specific credit profile and the A$600,000 or A$900,000 loan amount you seek.

Do I need to include my partner’s income in the borrowing power calculator?

You should include your partner’s income if you plan to apply for a joint mortgage to maximize your borrowing capacity. Combining two salaries, such as A$85,000 and A$95,000, significantly increases the total loan amount a lender will consider. Our home loan calculator allows you to input multiple income streams to give you a realistic view of your combined household purchasing power for your 2026 property search.

How much deposit do I really need according to the calculators?

You generally need a 20% deposit to avoid Lenders Mortgage Insurance (LMI), which equals A$160,000 on an A$800,000 property. However, many 2026 first home buyers use government schemes to enter the market with as little as a 5% deposit. While a smaller deposit gets you into a home sooner, a larger down payment reduces your total interest costs over the standard 30 year loan term.

Does using an online mortgage calculator affect my credit score?

Using an online mortgage calculator has zero impact on your credit score because it doesn’t involve a hard credit inquiry. You can test different scenarios and loan amounts as often as you like without leaving a footprint on your Equifax or Experian credit report. It’s a safe, private way to explore your options before you decide to move forward with a formal application in the 2026 market.

Why do different bank calculators give me different results?

Different banks use unique internal algorithms and varying expense benchmarks, such as the Household Expenditure Measure (HEM), to calculate your borrowing limit. One lender might offer you A$750,000 while another limits you to A$710,000 based on how they weight your discretionary spending or bonuses. These variations highlight why it’s helpful to have a partner who compares multiple products to find the most generous terms for your situation.

Should I use a repayment calculator for principal and interest or interest-only?

You should use a principal and interest calculation if you’re buying a home to live in, as this is the standard path to full ownership. Interest-only calculations are typically reserved for investors looking to maximize tax deductions or maintain cash flow for a set period, often 1 to 5 years. Selecting the right repayment type in your home loan calculator ensures your budget reflects the actual monthly costs you’ll face after settlement.

Can a home loan calculator account for my specific tax situation?

Standard calculators don’t account for individual tax nuances like negative gearing benefits or specific 2026 income tax brackets. They focus on gross figures and standard bank lending criteria to provide a baseline for your journey. For a tailored view that includes your A$5,000 annual tax refund or complex corporate structures, we recommend a personal consultation to refine those numbers.

What is the most important number to look at on a mortgage calculator?

The most critical figure to watch is the total interest paid over the life of the loan, which can often exceed A$450,000 on a standard mortgage. While monthly repayments matter for your weekly budget, the total cost shows you the long-term impact of your interest rate and loan term. Focusing on this number helps you understand how small changes, like an extra A$150 monthly payment, can save you thousands of dollars over 30 years.