Why are you still paying rent when some Australian lenders now require only six months remaining on your TSS 482 visa to approve a mortgage? You’ve likely felt the weight of uncertainty, worrying that your temporary residency status might lead to an automatic rejection, or that foreign buyer surcharges of 8% in states like Victoria and New South Wales make homeownership an impossible dream. We understand that the path to your own front door often feels more like a maze of regulations than a simple financial transaction.

We’re here to be your partner in this journey, showing you exactly how to get a home loan on a 482 visa in australia while managing FIRB requirements and finding a lender that values your specific visa stream. You’ll discover how to navigate the May 2026 lending landscape, including FIRB fees starting at A$14,700 for properties under A$1 million and competitive interest rates from 5.08% p.a. This guide provides a clear, step by step roadmap to help you secure pre-approval and move closer to the Australian dream with total confidence.

Key Takeaways

- Understand why an 80% Loan-to-Value Ratio (LVR) is the “sweet spot” for securing competitive terms and avoiding complex lending hurdles.

- Learn exactly how to calculate the total cost of entry, including mandatory FIRB application fees and state-specific stamp duty surcharges.

- Discover the specific steps for how to get a home loan on a 482 visa in australia by following our proven 6-step roadmap to pre-approval.

- Gain access to a panel of over 36 lenders through a specialist partner who understands the nuances of the TSS visa stream.

- Shift your perspective from “temporary resident” to “high-quality borrower” by aligning your application with specific lender policies.

Understanding the 482 Visa Home Loan Landscape in 2026

The Temporary Skill Shortage (TSS) 482 visa is more than just a work permit; for many skilled professionals, it’s the foundation for a new life in Australia. While your residency status is technically temporary, lenders often view you as a high-quality borrower because your presence in the country is backed by stable, skilled employment in sectors that drive the economy. Understanding how to get a home loan on a 482 visa in australia starts with recognizing that the path is open to you, provided you have the right partner to guide you through the additional layers of criteria.

Applying for a mortgage as a temporary resident involves two distinct hurdles that Australian citizens don’t encounter. First, you must satisfy the internal credit policies of the bank, which focus heavily on your job stability and the time remaining on your visa. Second, you must comply with federal government regulations regarding foreign investment. These requirements aren’t meant to stop your progress. Instead, they serve as a framework that requires a more tailored approach to your application. We specialize in translating these complex rules into a clear, manageable plan for your homeownership journey.

Short-Term vs. Medium-Term Streams

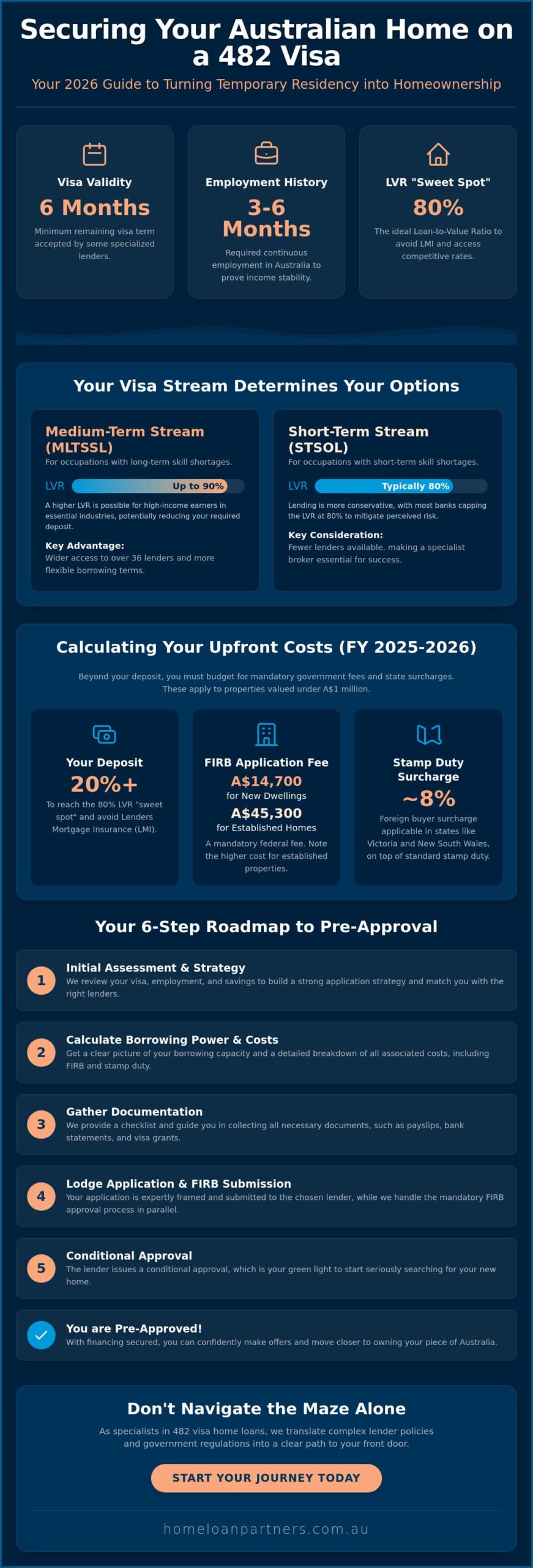

The specific stream of your 482 visa plays a significant role in determining which lenders will work with you. If you’re on the Medium-Term (MLTSSL) stream, you’ll generally find a wider variety of bank options and more flexible borrowing limits, often reaching up to 90% of the property value. Short-Term (STSOL) stream holders typically face more conservative limits, with most lenders capping the Loan-to-Value Ratio (LVR) at 80% to mitigate the perceived risk of a shorter stay.

Most banks expect you to have at least 12 months remaining on your visa when you apply. However, as of May 2026, some specialized lenders have adjusted their policies to accept as little as 6 months for professionals in high-demand fields like healthcare, education, or engineering. Your occupation acts as a signal of your future stability, and we help you present this strength to the right lender to maximize your chances of approval.

The Role of the Foreign Investment Review Board (FIRB)

Before you can finalize your property purchase, you must engage with the Foreign Investment Review Board (FIRB). This government body monitors residential real estate purchases by non-citizens to ensure they align with national interests. For a 482 visa holder, this is a mandatory step that involves a formal application and a fee. As of the 2025 to 2026 financial year, the fee for a new dwelling under A$1 million is A$14,700.

If you choose to purchase an established home rather than a new build, the cost increases significantly to A$45,300 for properties up to A$1 million, following the government’s 2026 focus on increasing housing supply. FIRB approval is a prerequisite for settlement for non-residents and must be secured before you can legally take ownership of your home. We’ll help you factor these timelines and costs into your budget so there are no surprises on your way to settlement.

Lender Eligibility: How Much Can You Borrow on a 482 Visa?

Determining your borrowing capacity is the first step toward moving into your own Australian home. For most 482 visa holders, the standard benchmark is an 80% Loan-to-Value Ratio (LVR). This means you’ll typically need a 20% deposit plus enough to cover transaction costs like stamp duty and FIRB fees. Banks view the 80% mark as a “sweet spot” because it significantly reduces their risk and, most importantly, removes the requirement for Lenders Mortgage Insurance (LMI). While LMI is common for local buyers with small deposits, many insurers are traditionally conservative when it comes to temporary residents, making an 80% loan the most seamless path to approval.

Lenders also look closely at your stability within the Australian workforce. While you may have decades of experience abroad, most banks want to see a minimum of 3 to 6 months of continuous employment history here in Australia. This confirms you’ve successfully transitioned into your role and have a steady income to meet your monthly repayments. Understanding how to get a home loan on a 482 visa in australia involves presenting a clean financial profile that proves your long term commitment to staying and working in the country.

The 90% LVR Exception

If saving a 20% deposit feels like a distant goal, there are exceptions. Some specialized lenders are willing to offer a 90% LVR to borrowers on the Medium-Term (MLTSSL) stream, provided they meet high income thresholds or work in essential industries like healthcare or engineering. These “90% loans” are subject to much stricter credit scoring and often require a flawless savings history. Because policies change frequently, partnering with an expert broker is the best way to identify which lenders are currently offering these higher leverage options for your specific visa type.

Applying with an Australian Citizen or PR Partner

Your borrowing potential changes dramatically if you’re purchasing a home with a partner who is an Australian citizen or Permanent Resident (PR). In this scenario, many lenders will treat the application as a “domestic” loan. This can unlock 95% LVR options, meaning you only need a 5% deposit to get started. Beyond the lower deposit, applying as a couple can sometimes help you avoid the foreign buyer stamp duty surcharges that apply to individual temporary residents.

It’s vital to consult the Official FIRB Guidance to see how your joint application affects your legal obligations. Generally, for the bank to grant these favorable terms, your Australian partner must be a co-borrower on the loan and a co-owner on the property title. This collaborative approach doesn’t just increase your borrowing power; it provides a more secure foundation for your future together in Australia.

Navigating Extra Costs: FIRB Fees and Stamp Duty Surcharges

Budgeting for your new home involves more than just the purchase price and your deposit. As a temporary resident, you’ll need to account for government costs that local buyers simply don’t face. These additional expenses often catch applicants by surprise, but they don’t have to be a deal breaker if you plan for them from the start. Understanding how to get a home loan on a 482 visa in australia requires a clear view of your total “entry cost,” which includes both lender requirements and state-based taxes. Resources like this guide on Home Loans for Temporary Residents highlight the importance of factoring in these specific financial obligations before you start your property search.

One common misconception is that the Foreign Investment Review Board (FIRB) process is only for wealthy international investors. In reality, it’s a standard procedural step for almost anyone on a 482 visa looking to buy a home. To avoid certain investment taxes and higher vacancy fees, you must generally purchase the property as your Principal Place of Residence. This means you intend to live in the home rather than rent it out. We’ll help you navigate these definitions to ensure your application remains compliant with both your visa conditions and Australian tax law.

Calculating the Foreign Buyer Surcharge

Most Australian states apply a Surcharge Purchaser Duty on top of the standard stamp duty. As of January 2026, if you’re buying in New South Wales, Victoria, or Queensland, you’ll face an 8% surcharge. In Western Australia and South Australia, the rate is 7%. It’s vital to remember that lenders rarely allow you to capitalise these costs into your mortgage. You’ll need to pay this amount from your savings at the time of settlement. We always advise our clients to use a specialized stamp duty calculator that includes non-resident fields to get an accurate figure for their specific state.

FIRB Application Fees and Timelines

The cost of your FIRB application depends heavily on the type of property you choose. For the 2025 to 2026 period, the fee for a new dwelling or vacant land under A$1 million is A$14,700. If you’re looking at an established dwelling, the fee jumps significantly to A$45,300 for properties up to A$1 million. This pricing structure is a deliberate move by the government to encourage the purchase of new housing stock. Once you’ve paid the fee, the Australian Taxation Office generally takes up to 30 days to process the application. Because of this window, it’s standard practice to include a “conditional on FIRB approval” clause in your purchase contract to protect your interests while the paperwork is finalized.

Roadmap: 6 Steps to Secure Your 482 Visa Home Loan

Moving from the dream of homeownership to holding the keys requires a tactical plan that aligns with both banking policies and government regulations. Because your situation involves additional layers of compliance, following a structured path ensures you don’t waste time on unsuitable lenders or risk your credit score with rejected applications. This roadmap simplifies how to get a home loan on a 482 visa in australia into six manageable milestones.

- Step 1: Financial Health Check. Review your savings to ensure you have the 20% deposit “sweet spot” plus an additional 10% to 15% for FIRB fees and stamp duty surcharges.

- Step 2: Broker Consultation. Connect with a specialist who understands which of our 36+ lenders currently favor your specific visa stream and occupation.

- Step 3: Pre-approval. Obtain a conditional “yes” from a lender, giving you a clear price range and the confidence to start your search.

- Step 4: Property Search & FIRB. Once you find a suitable home, you’ll lodge your application with the Foreign Investment Review Board while negotiating the purchase.

- Step 5: Formal Approval. After signing a contract “subject to FIRB approval,” your lender will perform a property valuation to finalize the mortgage.

- Step 6: Settlement. Your legal representative coordinates with the bank and the ATO to transfer funds and officially register you as the owner.

To start this journey with an expert by your side, you can book a consultation with our specialist team today.

Documents You Will Need

Lenders require a more comprehensive document trail for temporary residents than they do for citizens. You’ll need your Visa Grant Notice to prove your stream and expiry date, along with your passport. While standard bank statements and Australian payslips are mandatory, the “Letter of Employment” is the most critical piece of the puzzle. This letter must confirm your role, salary, and the employer’s intention to continue your sponsorship. If you’ve recently arrived, providing foreign tax returns from your previous country can also help demonstrate a consistent earning history to conservative credit assessors.

The Importance of Pre-Approval

You should never bid at an auction or sign an unconditional contract without a firm pre-approval in place. For 482 visa holders, the stakes are higher; if a loan falls through because of a visa-related policy quirk, you could lose your entire 10% deposit. A pre-approval typically remains valid for 90 days and acts as your shield in a competitive market. It tells real estate agents that you’re a serious buyer who has already cleared the major hurdles of how to get a home loan on a 482 visa in australia. This allows you to negotiate with the same authority as a local buyer, knowing your financial foundation is secure.

Partnering for Success: How The Home Loan Partners Guide You

We believe that securing a mortgage shouldn’t be a solitary struggle. Our “Partner” philosophy means we take on the heavy lifting, acting as your dedicated advocate throughout the entire application process. When you’re learning how to get a home loan on a 482 visa in australia, you aren’t just looking for a bank; you’re looking for a strategy that accounts for your unique residency status. We provide that bridge by managing the technical details, from initial borrowing assessments to final settlement coordination. Our goal is to replace the stress of the unknown with the confidence of expert guidance.

Access to a wide panel of over 36 lenders is a core part of our service. This extensive network includes major Australian banks and specialized “broker-only” non-bank lenders who often have more flexible policies for temporary residents. We don’t just stop at finding the lender; we work closely with your legal representatives and the FIRB to ensure every document is aligned. This collaborative approach minimizes the risk of delays or rejections, keeping your path to homeownership steady and predictable. We’re here to ensure the transition from applicant to homeowner is as seamless as possible.

Tailored Loan Structures for Temporary Residents

We understand that a doctor on a Medium-Term visa has different needs and options than a tech specialist on a Short-Term stream. Our team matches your specific occupation and visa conditions to the lender most likely to offer favorable terms. Whether you’re in Sydney, Perth, or a regional hub, our national service scope ensures you receive expert guidance regardless of where you choose to settle. By leveraging niche policies, we can often find solutions that standard retail banks might overlook, ensuring your loan structure fits your personal goals and financial capacity perfectly.

The Journey to Permanent Residency (PR)

Your home loan journey doesn’t end when you get your keys. We view our relationship as a long-term collaboration that evolves as your residency status changes. Once you transition from a 482 visa to Permanent Residency, new financial doors open. We’ll be there to help you refinance your loan, potentially removing the high foreign buyer surcharges or accessing the lower interest rates reserved for domestic borrowers. This proactive management ensures your mortgage remains a tool for your future security, not just a current expense. We’re committed to supporting you at every milestone of your Australian dream.

Speak with a 482 Visa Home Loan Expert today to begin your journey with a partner who understands your path.

Your Path to an Australian Home Starts Here

You’ve now seen that while the journey involves specific government fees and lender criteria, homeownership is entirely achievable on a TSS 482 visa. By focusing on an 80% deposit to avoid LMI and factoring in the May 2026 FIRB and surcharge costs early, you can build a financial foundation that banks respect. Understanding how to get a home loan on a 482 visa in australia isn’t just about the numbers; it’s about finding a lender that recognizes your professional value to the country.

We’re ready to act as your expert partner, providing access to over 36 lenders with specialized non-resident policies and guiding you through every complex FIRB requirement. Whether you’re on a Short-term or Medium-term stream, our team handles the heavy lifting so you can focus on finding the perfect property for your future. Book a Free 482 Visa Consultation with The Home Loan Partners to take the first step toward your Australian dream. Your new life in Australia deserves a place to call home, and we’re honored to help you find it.

Frequently Asked Questions

Can I buy an existing house on a 482 visa, or only new builds?

You can buy both, but the government currently prioritizes new builds to increase housing supply. As of May 2026, a temporary ban on foreign persons purchasing established dwellings is in effect until March 2027, though exceptions exist for temporary residents buying a principal place of residence. If you choose an established home, the FIRB fee is A$45,300 for properties up to A$1 million, compared to just A$14,700 for a new dwelling.

How much deposit do I really need for a 482 visa home loan?

A 20% deposit is the standard requirement to avoid Lenders Mortgage Insurance and secure the most competitive interest rates. While some lenders allow 10% deposits for Medium-Term stream holders in high-demand professions, these applications face stricter credit scoring. If you’re purchasing with an Australian citizen partner, you might only need a 5% deposit. We recommend having an additional 15% in savings to cover the mandatory government surcharges and fees.

Do I have to pay the Foreign Citizen Stamp Duty Surcharge if I am on a 482 visa?

Yes, most Australian states require temporary residents to pay a surcharge on top of standard stamp duty. In New South Wales, Victoria, and Queensland, this surcharge is 8% of the property’s value as of 2026. Western Australia and South Australia apply a 7% rate. Because lenders won’t let you add this cost to your mortgage balance, you must pay this entire amount from your own savings before settlement can occur.

What happens to my home loan if my 482 visa expires or is not renewed?

If your visa expires and you must leave Australia, FIRB regulations generally require you to sell the property within three months of your departure. However, if you’re in the process of renewing your visa or transitioning to Permanent Residency, you can keep the home while your application is pending. We focus on how to get a home loan on a 482 visa in australia with a view toward your long term residency goals to avoid these complications.

Can I get the First Home Owners Grant (FHOG) as a 482 visa holder?

Temporary residents on a 482 visa are generally ineligible for state government grants like the FHOG when buying alone. You can usually only access these benefits if you’re purchasing the home jointly with an Australian citizen or Permanent Resident. Even in these cases, the citizen or PR partner must meet specific residency and first-home buyer criteria set by their respective state government to qualify for the grant or stamp duty exemptions.

Is FIRB approval required if I am married to an Australian citizen?

You don’t need FIRB approval if you’re purchasing a residential property as “joint tenants” with an Australian citizen spouse or de facto partner. This exemption applies specifically to the person you are in a committed relationship with, not friends or other family members. If you decide to buy the property as “tenants in common” or in your name only, you must still complete the FIRB application and pay the required fee before settlement.

Are interest rates higher for 482 visa home loans?

Competitive variable interest rates for 482 visa holders currently start from 5.08% p.a., matching the rates offered to Australian citizens. While some smaller lenders might charge a premium for temporary residents, many major banks will offer standard market rates if your financial position is strong. Having a 20% deposit and stable employment in a high-demand industry are the best ways to ensure you don’t pay more for your mortgage than a local buyer.

How long do I need to be in Australia before I can apply for a mortgage?

Lenders typically want to see that you’ve been living and working in Australia for at least 3 to 6 months. This timeframe allows you to provide the necessary Australian payslips and bank statements to prove your local income stability. If you’ve arrived very recently but have a high-income contract in an essential field like medicine or engineering, some specialized lenders may consider your application sooner, provided your 482 visa has a significant remaining term.