What if your Juris Doctorate was the most powerful tool in your property portfolio? You’ve dedicated years to building a prestigious legal career, yet when it’s time to secure a mortgage, you’re often met with generic bank hurdles and high entry costs that don’t reflect your professional standing. At The Home Loan Partners, we understand that your time is your most precious commodity and your career stability is a significant asset that lenders should reward, not ignore.

This guide shows you how to unlock elite home loans for lawyers special offers that are specifically designed for your high-earning trajectory. You’ll discover how to bypass Lenders Mortgage Insurance (LMI) entirely, even with a smaller deposit, and negotiate interest rates well below the May 5, 2026, market average of 6.56%. With industry economists predicting rates to settle between 6.1% and 6.3% for the remainder of the year, we’ll partner with you to leverage your position for a more competitive deal. We’ll preview the path to securing up to 100% financing for properties up to A$1,500,000, ensuring a seamless, low-touch application process that respects your demanding schedule and long-term security.

Key Takeaways

- Learn why Australian lenders classify you as a low-risk borrower, allowing you to waive Lenders Mortgage Insurance and save thousands on your upfront property costs.

- Explore the specific home loans for lawyers special offers available in 2026, including negotiated interest rates that sit well below standard advertised products.

- Understand the essential eligibility criteria, such as holding a current Australian Practising Certificate, required to unlock these professional banking benefits.

- Identify why premium features like offset accounts are vital for your tax strategy and long-term wealth building, rather than just chasing the lowest headline rate.

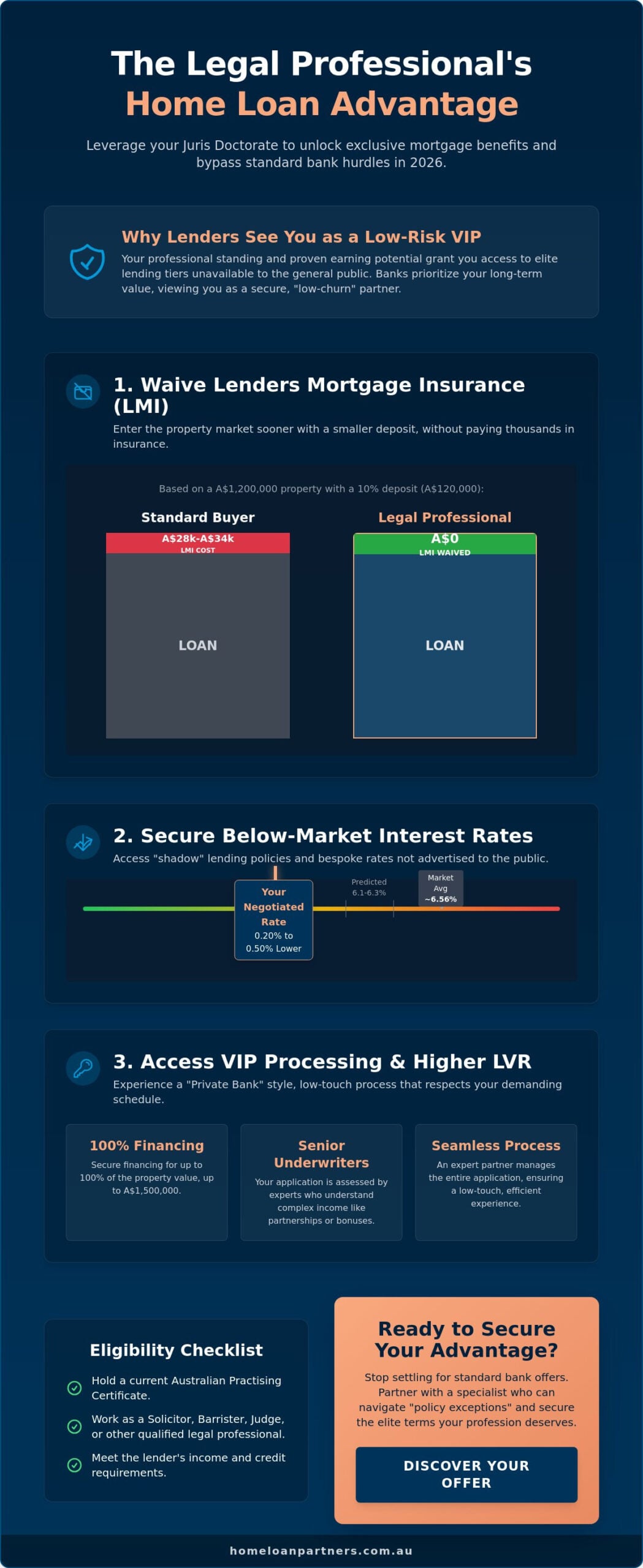

- Discover how an expert partner accesses “shadow” lending policies to secure a seamless, low-touch application process that respects your demanding schedule.

Why Legal Professionals Get Exclusive Home Loan Offers in 2026

Banks don’t just look at your current bank balance; they look at your future. In 2026, actuarial data confirms that legal professionals remain the lowest-risk borrowing cohort in Australia. This data isn’t just a statistic. It’s the foundation for why lenders are eager to provide home loans for lawyers special offers. Because you’re statistically less likely to default, banks view you as a safe harbour, even when the broader economy feels uncertain.

Lenders also value “low-churn” relationships. They know that a lawyer’s career often involves high-balance offset accounts and a steady increase in income over decades. By offering you a superior deal now, they’re securing a long-term partnership with a high-net-worth individual. They want to be there for your first home, your first investment, and eventually, your commercial ventures. This long-term value makes you a priority for their most competitive products.

The “Low-Risk” Premium Explained

Your Australian Practising Certificate is more than a license to practice law; it’s a financial passport that grants you access to elite lending tiers. Banks focus on the longevity and predictable upward trajectory of your career. They’ve shifted their focus in 2026 to prioritize this professional stability over the size of your raw deposit. Essentially, your professional status acts as a form of social equity that allows banks to waive traditional requirements. Because of your proven earning potential, many lenders will waive Lenders Mortgage Insurance (LMI) even if you have less than a 20% deposit.

VIP Treatment in a Competitive Market

You won’t find the best home loans for lawyers special offers on standard comparison websites. Those platforms are built for the general public, where “one size fits all” is the rule. For legal professionals, credit departments often apply “policy exceptions” that exist outside the standard retail framework. This shifts you into Private Bank style service, where your application is assessed by senior underwriters who understand complex partnership structures or variable bonus cycles. It’s a bespoke approach where we act as your partner to ensure the bank sees the full value of your professional profile. This level of service ensures a seamless experience that matches the high standards you set in your own practice.

The Big Three: Waived LMI, Discounted Rates, and Cashbacks

Your legal expertise doesn’t just win cases; it wins financial concessions that the general public rarely sees. In the 2026 market, the most powerful home loans for lawyers special offers revolve around three core pillars. By stacking these benefits, you can effectively bypass the standard entry barriers to premium Australian real estate. It’s not about choosing one incentive over another. It’s about leveraging your professional standing to secure all three simultaneously.

The financial impact of this “triple-stack” strategy is substantial. When you combine a waived insurance premium with a bespoke interest rate and a refinance incentive, the total benefit often exceeds A$20,000 in the first year alone. This isn’t just a marketing claim; it’s a reflection of the low-risk profile you bring to a lender’s portfolio.

Waived LMI: Buying with a 10% Deposit

Borrowing 90% or even 95% of a property’s value typically triggers a massive insurance premium known as Lenders Mortgage Insurance. For a standard buyer purchasing a A$1,200,000 home with a 10% deposit, LMI could easily cost between A$28,000 and A$34,000. As a legal professional, this cost is frequently waived. This isn’t just a small discount. It’s a significant injection of liquidity back into your portfolio. Instead of that money disappearing into a bank’s insurance policy, it stays in your offset account to reduce interest from day one. This waiver dramatically increases your immediate borrowing power, allowing you to secure a superior property without waiting years to save a full 20% deposit.

Negotiated Interest Rates vs. Retail Rates

Retail interest rates are just a starting point for negotiation. While a bank might advertise its “best” rate, we often secure bespoke discounts sitting 0.20% to 0.50% lower for our legal clients. These aren’t standard “packaged” products available to the general public. They are individual price points negotiated based on your specific income level and career trajectory. A lower rate on a A$1,000,000 loan can save you thousands in interest annually. This compounding effect creates a massive wealth-building advantage over the life of your loan. If you’re curious about how your current rate compares to these professional tiers, you can explore our tailored refinancing options to see the potential savings.

Cashback offers in 2026 have also become increasingly sophisticated. Rather than generic “switch” bonuses, lenders are targeting professional refinancers with incentives designed to cover the costs of moving and provide an immediate cash buffer. When these cashbacks are layered on top of a negotiated rate, the long-term journey toward homeownership becomes significantly more affordable and stress-free.

Eligibility Checklist: Who Qualifies for Legal Professional Loans?

Qualifying for home loans for lawyers special offers is more straightforward than many busy professionals realize. While standard lending relies heavily on deposit size, professional policies prioritize your credentials. The core requirement is holding a current Australian Practising Certificate. This document proves to the bank that you belong to a low-risk, high-earning cohort, regardless of whether you’re a junior solicitor or a senior partner. It signals to the credit assessor that your career follows a stable, upward trajectory.

In 2026, membership in an industry body like the Law Society or the Bar Association has become a critical benchmark for premium lending. Lenders use this membership as a secondary layer of verification to justify waiving Lenders Mortgage Insurance (LMI). Providing evidence of your current industry membership is the golden key for LMI waivers, as it confirms your professional standing and unlocks the most aggressive interest rate discounts available in the Australian market.

Eligible Legal Roles in Australia

Many assume these offers are exclusive to private practice partners, but that isn’t the case in the current market. Solicitors and Barristers are the primary beneficiaries, yet the scope has widened significantly. Judges, Magistrates, and even Clerks of Court are now frequently included in specialized professional policies. We also see corporate counsel and government lawyers accessing these benefits, provided their role requires a legal qualification and they meet the bank’s specific income thresholds. Typically, a minimum individual income of A$120,000 to A$150,000 is required; however, some lenders allow household income to be considered if both parties are professionals, even if only one is a lawyer.

Documentation and Evidence Requirements

Proving your status requires specific evidence that goes beyond a standard payslip. For PAYG employees, a current employment contract and your Practising Certificate are usually sufficient to trigger a professional discount. However, for self-employed Barristers or law firm Partners, the requirements are more nuanced. In 2026, many lenders have moved away from requiring two years of full tax returns for top-tier professionals. We can often secure approvals using Business Activity Statements (BAS) or a simple letter from your firm’s accountant. This streamlined approach minimizes the paperwork burden, allowing you to focus on your practice while we handle the heavy lifting with the credit assessors. Our goal is to ensure your application is “bank-ready” without you needing to spend hours hunting for historical financial data.

Strategic Comparison: Negotiated Rates vs. Standard Bank Products

Many lawyers make the mistake of choosing a mortgage based solely on the lowest headline interest rate. While a low rate is attractive, standard “Basic” or “No Frills” products often lack the structural flexibility required for a sophisticated tax strategy. These entry-level loans typically exclude offset accounts or limit redraw facilities. For a high-earning professional, missing out on these features can be far more expensive than a slightly higher rate. We focus on securing home loans for lawyers special offers that balance competitive pricing with the high-end features your career demands.

When we evaluate the “true cost” of debt, we look beyond the interest. Standard professional packages in Australia often carry an annual fee, frequently around A$395. However, many exclusive offers we negotiate for our clients include a permanent waiver of these fees. Over a 30-year loan term, this waiver alone saves you nearly A$12,000. We also compare the established “medico-legal” packages of the Big 4 banks against nimble boutique lenders. These smaller institutions often use more flexible “shadow” policies to win your business, providing bespoke terms that standard bank comparison sites never display.

The Power of Offset Accounts for High Earners

An offset account is one of the most effective tools for a lawyer’s long-term wealth journey. Unlike standard bank products that might limit you to a single offset, professional-tier loans often allow multiple accounts to be linked to the same loan. This allows you to partition funds for specific purposes, such as GST reserves for barristers or deposit savings for future investment properties. Every dollar sitting in these accounts works to reduce your mortgage interest daily. There is a powerful synergy between a high legal salary and an active offset strategy, allowing you to maintain liquidity while aggressively paying down your principal.

Refinancing Strategy for 2026

The lending environment in 2026 is highly dynamic. If you haven’t had a professional review of your loan structure in the last 18 months, you’re likely missing out on new market concessions. We perform a detailed cost-benefit analysis to determine if moving for a cashback incentive outweighs staying with your current lender for a negotiated rate discount. If a move is the right choice, Home Loan Partners manages the entire transition to ensure zero downtime and a stress-free experience. If you’re ready to see how your current mortgage stacks up against the latest market offers, request a professional loan review today.

Securing Your Special Offer with a Dedicated Mortgage Partner

Accessing the highest tier of the Australian mortgage market requires more than a simple application. It requires an advocate who understands the “shadow” policies that lenders keep off their public websites. These discretionary rules often allow for higher borrowing limits or deeper rate discounts that aren’t available to the general public. We specialize in identifying these opportunities, ensuring you receive the full benefit of your professional status from the outset.

By representing your professional profile to the specific credit teams most hungry for legal clients, we maintain a 98% approval rate. This success comes from knowing how to frame your income, partnership distributions, and career trajectory in a language that bank underwriters respect. Our promise is to do the heavy lifting while you manage your practice. We take over the administrative burden, managing the paperwork and lender follow-ups so you can focus on your billable hours and your clients.

The Partnership Advantage

We view our role as a long-term advisory relationship rather than a one-off transaction. Home Loan Partners provides you with direct access to more than 36 lenders, including niche institutions and specialist professional credit teams. This broad market reach ensures we find the perfect fit for your unique financial structure. Our commitment to your long-term journey means we stay with you long after settlement. We proactively monitor interest rate movements and bank policy changes, acting as your steady hand in a shifting market to ensure your loan continues to serve your future security. This collaborative approach ensures that as your career grows, your financial structures evolve with you.

Next Steps: Your Stress-Free Application

Securing a premium mortgage shouldn’t be a source of stress. We’ve refined our process to be as efficient as possible for busy legal professionals. It starts with a simple 5-minute initial assessment that has zero impact on your credit score. From there, we move into a tailored loan structuring phase where we align your mortgage with your specific tax and investment goals. When you’re ready to unlock the home loans for lawyers special offers your career has earned, Partner with us to secure your exclusive legal home loan offer and experience a truly professional lending journey.

Leverage Your Professional Status for Property Success

Your journey toward homeownership doesn’t have to be slowed down by standard bank requirements. Your career in the Australian legal system provides a unique advantage that allows you to bypass Lenders Mortgage Insurance and secure bespoke interest rates. We’ve explored how home loans for lawyers special offers can save you over A$20,000 in upfront costs, providing a significant boost to your immediate borrowing power. By choosing a mortgage structure with multiple offset accounts, you’re setting yourself up for a more tax-effective future that matches your high-earning potential.

At Home Loan Partners, we act as your steady guide through the complexities of professional lending. With access to 36+ Australian lenders and a deep specialty in LMI waivers, we provide the expert, unbiased guidance your legal career deserves. We manage the heavy lifting of the application process, ensuring a seamless experience that respects your time. Secure Your Exclusive Lawyer Home Loan Offer Today and take the first step toward a property strategy that works as hard as you do. Your dream home is within reach, and we’re here to help you claim it with confidence.

Frequently Asked Questions

Do I need a 20% deposit to avoid LMI as a lawyer?

No, you don’t need a 20% deposit to avoid this cost. Legal professionals can frequently borrow up to 90% of a property’s value without paying any Lenders Mortgage Insurance. In fact, as of April 17, 2026, some specialized programs offer up to 100% financing for purchases up to A$1,500,000. This waiver allows you to enter the market years earlier while keeping your capital for other investment opportunities.

Are government-employed lawyers eligible for these special offers?

Yes, government-employed lawyers are fully eligible for these benefits. As long as you hold a current Australian Practising Certificate and meet the lender’s income requirements, you can access the same home loans for lawyers special offers as those in private practice. Banks highly value the career stability and consistent salary progression associated with government legal roles, often making the approval process even smoother.

Is there a minimum income required for the LMI waiver in 2026?

Most lenders require a minimum individual income between A$120,000 and A$150,000 to grant an LMI waiver. However, some banks have introduced more flexible policies in 2026 that allow for combined household income if your partner is also a qualified professional. This shift ensures that even senior associates or those in specialized niche practices can qualify for premium discounts based on their total financial position.

Can I get a professional discount if I am a self-employed barrister?

You can certainly secure a professional discount as a self-employed barrister. We work with lenders who understand the unique cash flow of the Bar and don’t require the standard two years of tax returns. Many of our partners accept Business Activity Statements (BAS) or a simple accountant’s letter to verify your income. This streamlined documentation process ensures you aren’t held back by the complexities of your business structure.

What is the maximum loan-to-value ratio (LVR) available for lawyers?

The maximum LVR for legal professionals currently reaches 100% with select lenders. While 90% is the standard threshold for waiving LMI, specific professional programs in 2026 offer 0% down options for loan amounts up to A$1,000,000. These high-LVR loans are designed to reward your career stability and high earning potential, allowing you to secure premium real estate with minimal upfront cash.

Do these offers apply to investment properties or just owner-occupied homes?

These offers apply to both investment properties and owner-occupied homes. Lenders recognize that lawyers are often sophisticated investors looking to build long-term wealth through property. Consequently, you can access LMI waivers and negotiated interest rates across your entire portfolio. This flexibility is essential for tax-effective wealth strategies, as it allows you to maintain professional-tier benefits while expanding your investment footprint.

How long does it take to get a formal approval for a professional loan?

Formal approval typically takes 3 to 5 business days when your application is managed through a specialist partner. Because we deal directly with senior underwriters and professional credit teams, we bypass the standard retail banking queues that often cause delays. This accelerated timeline is crucial in competitive Australian property markets, giving you the confidence to make unconditional offers with a quick turnaround.

Will I lose my discount if I move from private practice to a corporate role?

You generally won’t lose your existing interest rate discount if you change roles after your loan has settled. Most loan contracts don’t include clauses that trigger a rate increase based on a change in employer. However, if you decide to refinance or apply for a loan increase in the future, the new lender will re-verify your professional status and current income to ensure you still meet their eligibility criteria.