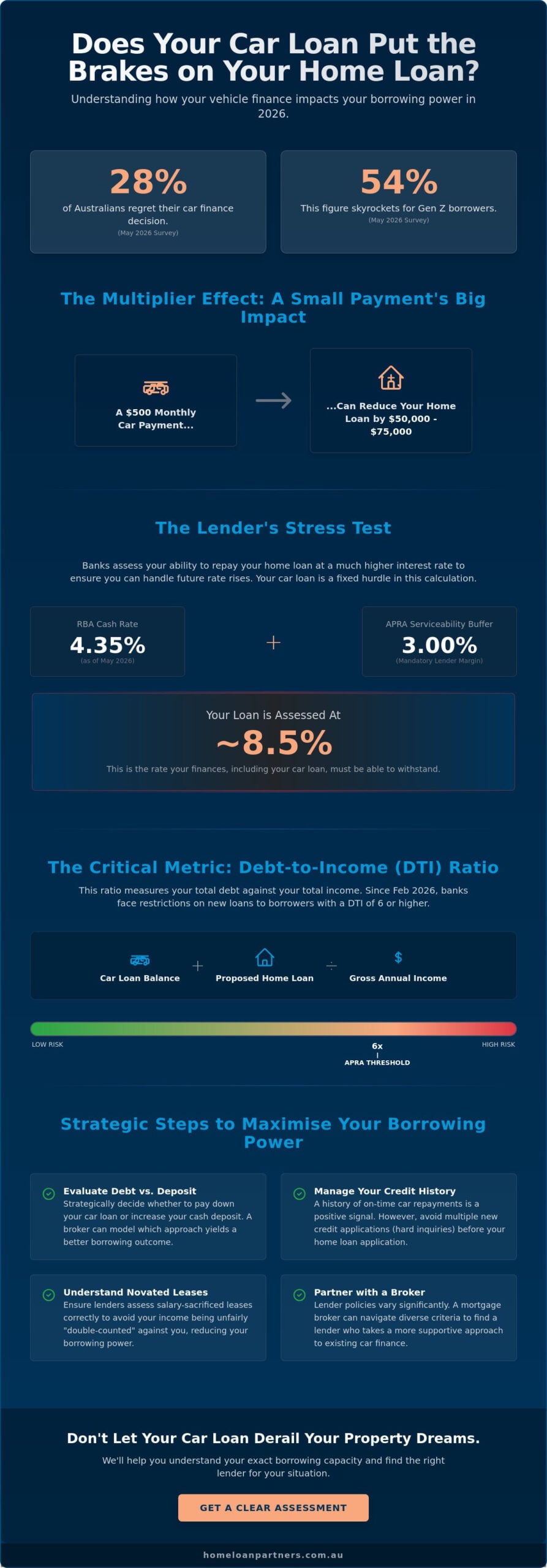

A May 2026 survey found that 28% of Australians regret their car finance, a figure that climbs to 54% for Gen Z borrowers. If you’re planning to buy a house, you’re likely asking: does a car loan affect home loan application? The answer is a clear yes. With the RBA cash rate sitting at 4.35% and APRA’s 3% serviceability buffer in full effect, every dollar you commit to a vehicle repayment directly reduces the surplus income lenders use to calculate your mortgage limit.

It’s natural to feel uneasy about how a novated lease or a standard car loan might impact your chances of approval, especially with the new debt-to-income caps introduced in February. We understand that these financial layers can feel complex and stressful. You want to move forward with confidence, knowing your vehicle choice hasn’t stalled your home-buying dreams. This guide will show you exactly how lenders run their stress tests and provide actionable steps to improve your serviceability. We’ll explore the math behind your borrowing power and help you identify lenders that take a more supportive approach to existing car finance.

Key Takeaways

- Understand how lenders view car finance as a fixed commitment that reduces the surplus income available for your mortgage repayments.

- Learn why the debt-to-income ratio is a critical 2026 benchmark and how it determines your eligibility for high-leverage home loans.

- Discover the specific assessment techniques for novated leases to prevent your salary sacrifice from being unfairly double-counted by banks.

- Evaluate the strategic choice between paying down car debt or increasing your cash deposit to maximize your borrowing capacity.

- Find out how a broker helps you navigate diverse lender criteria to see exactly how does a car loan affect home loan application results across the market.

How a Car Loan Impacts Your Home Loan Eligibility

When you sit down with a lender in 2026, they look far beyond your savings account. They focus on your future cash flow and your ability to manage multiple commitments. You might be asking, does a car loan affect home loan application? The answer is a definitive yes. Lenders view any existing debt as a prior claim on your income. Every dollar you send to a car financier is a dollar that cannot be used to service a mortgage. Under current responsible lending obligations, banks must “stress test” your finances. With the RBA cash rate at 4.35% as of May 2026, lenders apply a 3% serviceability buffer. This means they assess your ability to pay your home loan at roughly 8.5% or higher, and your car loan is a fixed hurdle in that calculation.

Even a relatively small car loan can trigger a deeper review of your living expenses. Banks are now more granular in their assessments, often comparing your declared spending against your actual bank statements. If a car loan payment pushes your total monthly commitments too high, it might suggest that your lifestyle relies heavily on credit, which can lead to a more conservative borrowing offer.

Liabilities vs. Assets in your Application

It’s vital to distinguish between what you own and what you owe. Your car is technically an asset, but for a mortgage application, its market value takes a backseat to the loan attached to it. While a high-value vehicle might look good on a “net worth” statement, lenders care much more about the repayment amount than the total debt figure. A $30,000 loan with a five-year term has a much heavier impact on your daily cash flow than the same debt spread over seven years.

Lenders use your Debt-to-Income (DTI) ratio to measure your total financial risk. Since February 2026, APRA has restricted banks from issuing more than 20% of new loans to those with a DTI of six or higher. Your car loan balance is added to your potential mortgage to reach this figure. We work with you to understand these ratios before you apply, ensuring your total debt profile fits within these strict regulatory limits.

The Role of Credit History and Repayment Behavior

Your car loan also leaves a digital footprint that can work in your favor. Every on-time repayment is recorded in your Comprehensive Credit Reporting (CCR) data. This builds a profile of reliability and proves you can manage a structured debt facility over the long term. If you’ve managed your car finance perfectly, it sends a positive signal to the bank that you are a dependable borrower.

However, be cautious with “hard inquiries.” If you applied for several car loans recently to compare rates, each application appears on your credit file. Too many inquiries in a short period can suggest financial distress or a lack of stability. We help our clients navigate these nuances, positioning your history of consistent car loan management as a strength rather than a liability during the home loan process.

Calculating the Impact: Borrowing Power and Debt-to-Income Ratios

Understanding the math behind your application is the first step toward a successful home purchase. While many buyers focus solely on their deposit, lenders are deeply focused on your Debt-to-Income (DTI) ratio. As of February 1, 2026, APRA has tightened these standards. Banks are now restricted to issuing no more than 20% of new home loans to borrowers with a DTI of six or higher. When calculating your debt-to-income ratio, the lender adds your total car loan balance to your proposed mortgage amount. If that combined total exceeds six times your gross annual income, your application enters a high-risk category that many banks now avoid.

The impact of car finance is often more significant than borrowers expect because of the multiplier effect. A car loan doesn’t just reduce your borrowing capacity by the amount of the debt; it eats into the surplus income used to service a 30-year mortgage. For every $100 you spend on monthly car repayments, your potential home loan amount could drop by approximately $10,000 to $15,000. This means a $500 monthly car payment might effectively slice $50,000 to $75,000 off your maximum mortgage limit. This is a primary reason why asking “does a car loan affect home loan application” results in such a high level of concern for modern buyers.

The Serviceability Math

Lenders don’t just look at your raw salary. They often “shade” your income, meaning they might only recognize 80% of your bonuses, commissions, or rental income to create a safety margin. Once they have this adjusted figure, they subtract your car repayments and apply the mandatory 3% interest rate buffer. This stress test ensures you can still manage repayments if home loan rates, currently in the mid-5% to low-6% range, were to climb higher. If your car loan includes a “balloon payment” at the end of the term, lenders may view this as an additional risk, as it represents a large, looming cash requirement that could threaten your mortgage stability.

DTI Thresholds and Lender Appetite

Lender appetite for debt varies significantly across the market. Some major banks may automatically decline an application if the DTI exceeds their internal benchmarks, while others are more flexible if you have a high “net worth” or significant savings. The way you documented your car loan also matters. A “full-doc” car loan with clear tax records is generally viewed more favorably than “low-doc” finance. Accurate living expense reporting is essential here. If your car loan repayments are high, you must demonstrate that your other discretionary spending is disciplined to maintain a healthy surplus. If you are unsure where you stand, we can help you analyze your serviceability before you approach a lender.

Novated Leases and Salary Sacrifice: The Hidden Effect

For many professionals, a novated lease seems like the ultimate financial win. It allows you to pay for a vehicle and its running costs using pre-tax income, which reduces your overall tax bill. However, when you pivot toward a property purchase, this arrangement often becomes a double-edged sword. While you enjoy more take-home pay, a lender sees your gross income as artificially lowered. If you’ve ever wondered, does a car loan affect home loan application differently when it’s part of a salary sacrifice, the answer lies in the nuances of lender assessment. Banks view the lease as a fixed, non-discretionary commitment that must be subtracted from your borrowing capacity, regardless of the tax benefits you receive.

In 2026, the assessment of these leases has become even more complex due to the rising popularity of Electric Vehicles (EVs). While EV fringe benefit tax exemptions remain a powerful incentive for employees, they create a unique footprint on your financial profile. Even if the car is exempt from Fringe Benefits Tax, the value is still recorded on your income statement. This figure can inadvertently push you into a higher bracket for other obligations, such as HECS or HELP repayments, which further tightens the surplus income available for a mortgage.

Assessment of Pre-Tax Commitments

Lenders handle novated leases with a high level of scrutiny. When they review your payslip, they see a significant portion of your salary being diverted before it even hits your bank account. To ensure you aren’t unfairly penalized, we often use the “add-back” method during the application process. This involves showing the lender that the lease payment is actually part of your total compensation package, effectively “adding back” the lease amount to your income for the purpose of the serviceability test.

Despite this, a novated lease can sometimes be more restrictive than a standard car loan. Some lenders may “double-count” the expense by viewing the reduced net income on your payslip while also listing the lease as a separate liability. This is where professional guidance becomes essential. We help lenders see your true earning potential by providing clear reconciliations of your pre-tax and post-tax positions.

Fringe Benefits and Your Borrowing Capacity

The Reportable Fringe Benefits Amount (RFBA) on your tax return is a critical figure that many buyers overlook. Even if you don’t pay tax on the benefit, the RFBA is used by the government and lenders to determine your eligibility for various schemes and your capacity to repay debt. A high RFBA can increase your mandatory debt repayments elsewhere, which directly answers the question: does a car loan affect home loan application? Yes, it does, often through these indirect tax-related channels.

If you are considering a new lease before a property purchase, timing is everything. Entering into a long-term salary sacrifice arrangement just months before applying for a mortgage can significantly reduce your options. We recommend reviewing your current lease terms and how they align with the 2026 DTI caps before making any new vehicle commitments. Our goal is to ensure your transport choices support, rather than hinder, your journey toward home ownership.

Strategic Steps: Should You Pay Off Your Car Loan Early?

Deciding whether to clear your car finance before applying for a mortgage is a common crossroads. It often comes down to a choice between boosting your borrowing power or protecting your deposit. If you’re asking, does a car loan affect home loan application success, the answer often hinges on which of these two pillars is weaker in your specific profile. If your income is high but your deposit is small, keeping the cash might be the smarter play to avoid costly Lenders Mortgage Insurance (LMI). Conversely, if you have plenty of savings but your income is stretched, wiping out the debt could be the key to unlocking the loan amount you need. Timing is everything.

Refinancing your car loan is another strategic path. With average car loan rates for good credit sitting around 7.58% p.a. in May 2026, switching to a more competitive rate or a different structure can lower your monthly commitment. This lower repayment directly increases your uncommitted monthly income, which lenders view favorably during their serviceability assessment. We can help you analyze your options to ensure your cash is working as hard as possible for your future home.

Scenario A: Paying Off the Loan

Clearing a $20,000 car loan today can have a dramatic impact on your mortgage limit. If that loan required a $450 monthly repayment, removing it could potentially increase your borrowing capacity by $45,000 to $65,000. This follows the logic we explored earlier, where small monthly debts have a massive multiplier effect on your total loan potential. A “clean” credit file with zero active liabilities often results in a faster approval process and a wider choice of lenders. However, there is a potential catch. Lenders typically want to see “genuine savings” held for at least three months. If paying off your car loan depletes your bank balance, you must ensure you still have enough liquid cash to satisfy the lender’s deposit requirements and cover closing costs.

Scenario B: Consolidating Debt

Rolling your car debt into your new home loan, known as debt consolidation, can simplify your finances by creating a single monthly payment. This often lowers your immediate outgoings because home loan interest rates, currently starting from 5.64% p.a. in May 2026, are typically lower than car finance rates. You must proceed with caution here. It’s vital to remember that paying for a car over a 30-year mortgage term instead of a 5-year car loan term can cost you significantly more in total interest over the long run. Additionally, adding your car debt to your mortgage increases your Loan-to-Value Ratio (LVR). If this push takes your LVR above 80%, you may find yourself paying LMI, which could outweigh the benefits of the consolidation itself. We’ll work with you to model these scenarios so you can make a choice that protects your long-term wealth.

Navigating Lender Criteria with a Mortgage Broker

Hearing a “no” from your primary bank can feel like a major setback, but it’s rarely the end of the road. The Australian mortgage market consists of over 36 lenders, each with their own unique appetite for risk and different ways of assessing liabilities. Many borrowers assume that because one lender was strict about their vehicle debt, the answer to “does a car loan affect home loan application” is always a negative one. In reality, while every bank must follow APRA’s core safety guidelines, the way they interpret your “surplus income” can vary significantly from one institution to the next.

We act as your expert collaborator, looking beyond the raw numbers to package your application in a way that highlights your underlying strengths. If you have a high savings rate or a long history of stable employment, we ensure the lender sees these positive signals. Our goal is to move the conversation away from a cold, transactional rejection and toward a professional assessment of your true financial reliability. We don’t just look for a loan; we look for a partnership that aligns with your long-term life milestones.

The Power of Choice and Lender Variance

The “Big 4” banks often use highly automated, rigid systems to flag debt-to-income ratios. If your car loan pushes you even slightly over their internal threshold, you might face an automatic decline. Conversely, many second-tier lenders and non-bank institutions employ manual underwriting. This means a human credit officer actually reviews your file, allowing for a more nuanced understanding of your complex debt profile. They might be more “car-loan friendly” if they can see that your vehicle is essential for work or that your repayment history is flawless. Understanding Why Use a Mortgage Broker in Australia? becomes clear when you realize we can filter through these 36+ lenders to find the one whose serviceability model best fits your specific situation.

Pre-Approval and Debt Management

Getting a professional set of eyes on your file before you submit a formal application is critical. Every “hard inquiry” on your credit report can impact your score, so we aim for precision from the start. If your current car debt is too high to achieve the home loan amount you want, we don’t just walk away. We help you craft a “pathway to purchase,” which might involve a six-month plan to reduce certain liabilities or wait for a lease to expire. This steady, logical approach ensures that when you do apply, you do so with a high level of confidence and security. If you’re ready to see how your current commitments fit into the 2026 lending environment, Book a strategy session with The Home Loan Partners today. We’ll help you navigate the math and find a clear, stress-free path to your new front door.

Securing Your Property Future with Confidence

Understanding the interplay between your vehicle finance and your mortgage is the first step toward a successful purchase. We’ve explored how the current 4.35% cash rate and APRA’s serviceability buffers turn every monthly repayment into a critical variable. While asking does a car loan affect home loan application is a smart starting point, the real value lies in how you strategically position your debt before meeting a lender. You now have the tools to evaluate whether paying off a loan or preserving your deposit is the right move for your specific situation.

Whether you’re a first home buyer or a seasoned investor, you deserve unbiased advice tailored to your 2026 goals. We provide a steady hand through this process, offering access to a panel of over 36 lenders to find the one that values your unique financial profile. We’ll manage the heavy lifting of the calculations so you can focus on finding the right property for your future.

Let’s calculate your true borrowing power together; contact The Home Loan Partners today.

Your journey toward home ownership is a significant life milestone, and we’re here to ensure you move forward with clarity, security, and peace of mind.

Frequently Asked Questions

Can I get a home loan if I have a car loan?

Yes, you can absolutely obtain a home loan while holding a car loan. Lenders don’t require you to be debt-free, but they will subtract your car repayments from your total income to determine what you can afford. This is a central way does a car loan affect home loan application outcomes, as it lowers the maximum amount a bank is willing to lend you for a property.

How much does a $500 monthly car payment reduce my mortgage borrowing power?

A $500 monthly car repayment typically reduces your borrowing power by $50,000 to $75,000. This calculation is based on the general rule that every $100 of monthly debt can slice roughly $10,000 to $15,000 off your total mortgage limit. This multiplier effect happens because that $500 is no longer available to cover the principal and interest on a 30-year home loan.

Is it better to pay off my car loan or save for a house deposit?

The decision depends on whether your application is limited by your deposit size or your annual income. If you have a small deposit, keeping the cash helps you reach the 20% threshold to avoid Lenders Mortgage Insurance. However, if your income is the bottleneck, paying off the car loan removes a liability and can significantly boost your serviceability and borrowing capacity.

Does a novated lease count as debt when applying for a mortgage?

Lenders treat a novated lease as a significant financial commitment during your assessment. Even though it’s paid from your pre-tax salary, banks view it as a fixed monthly expense that reduces your take-home pay. We often help clients by using an “add-back” strategy to ensure lenders see your true earning potential rather than just your reduced net income.

Will a car loan affect my credit score for a home loan application?

Your car loan has a direct impact on your credit score through the Comprehensive Credit Reporting system. On-time repayments build a positive profile and prove you’re a reliable borrower. Conversely, applying for multiple car loans in a short window creates “hard inquiries” that can temporarily lower your score and signal financial instability to a mortgage lender.

Can I consolidate my car loan into my home loan?

You can often consolidate car debt into your mortgage when you apply for refinancing. This can lower your overall monthly outgoings because home loan rates are generally lower than car finance rates. It’s vital to remember that rolling a five-year car debt into a 30-year mortgage will result in paying more total interest over the life of the loan.

Should I wait until my car loan is finished before buying a house?

Waiting isn’t always required, but it can be a strategic move if you need to maximize your serviceability. If your current car debt pushes your Debt-to-Income ratio above six, waiting until the loan is finished could be the difference between an approval and a rejection. We can help you model how does a car loan affect home loan application results based on your specific timeline.

Does a car loan affect a first home buyer’s grant or stamp duty concessions?

A car loan does not directly impact your eligibility for the First Home Owner Grant or stamp duty concessions. These government benefits are based on the value of the property you’re buying and your residency status. However, because a car loan reduces your borrowing power, it may limit the price range of the homes you can afford to purchase using those grants.