Imagine finding your dream home in a leafy suburb before you’ve even listed your current property for sale. While the excitement is real, it’s often shadowed by the fear of being forced to sell your current home at a discount just to make the dates align. You’re probably wondering, how do bridging loans work in australia, and can they actually protect your equity in a market where the RBA cash rate sits at 4.35%?

We understand that the idea of “peak debt” feels overwhelming, especially when standard variable rates are hovering around 5.83% p.a. and bridging rates can reach higher. It’s natural to feel anxious about servicing two loans at once. This guide is designed to be your steady hand, showing you how to buy your next home before selling your current one with total clarity.

You’ll discover the mechanics of interest capitalisation, which allows you to focus on your move rather than monthly repayments. We’ll also walk through the Peak versus End debt math and the 12-month timeline, giving you the confidence to manage your transition without the typical financial hurdles.

Key Takeaways

- Learn how bridging finance removes the need for “subject to sale” clauses, allowing you to secure your next home with confidence and speed.

- Understand the critical difference between Peak Debt and End Debt to accurately calculate your total borrowing power and long-term equity.

- Discover how interest capitalisation works to protect your monthly cash flow by deferring interest payments until your current property sells.

- Gain clarity on how do bridging loans work in australia through the lens of lender servicing tests and the essential 20% equity requirement.

- See why professional broker support is the key to navigating varying lender policies and managing the heavy lifting of dual loan applications.

What is a Bridging Loan and How Does it Work in Australia?

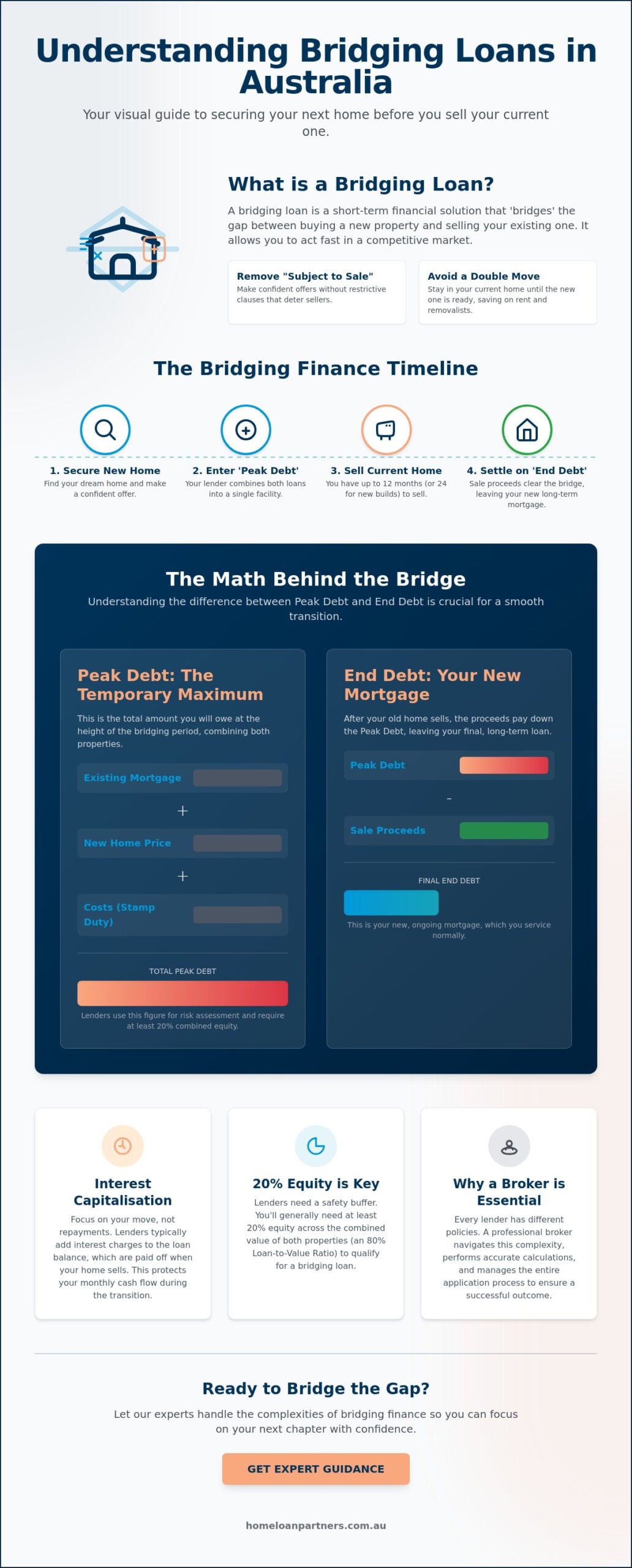

A bridging loan acts as a vital financial link that connects the purchase of your new property with the sale of your current one. This short-term finance solution is specifically designed to “bridge” the gap between two settlements. If you are looking for a global perspective, you can read more about What is a Bridging Loan? and its general applications. In the Australian market of 2026, where speed and certainty are paramount, this facility allows you to secure a new home without the restrictive “subject to sale” condition that often deters sellers in competitive suburbs.

For most established homes, you’ll have a 12-month window to sell your previous property. If you are building a new home, this timeframe often extends to 24 months to account for construction stages. This flexibility is why bridging finance has become the preferred strategy for Australian families looking to upgrade. Instead of waiting for a buyer to appear, you can act immediately when your dream home hits the market. Success in this area relies heavily on the equity you’ve built in your current home, which serves as the foundation for the entire loan structure.

The Core Mechanics of Bridging Finance

When you enter a bridging arrangement, the lender typically takes security over both your current home and your future property. They look at your existing mortgage and the purchase price of the new home to create a single, combined facility. So, how do bridging loans work in australia during this transition? The lender calculates your total debt before your first house sells. The bridging period is the specific timeframe between the purchase of your new property and the sale of your current one. During this time, your lender manages the heavy lifting, often allowing interest to accumulate so you don’t have to worry about dual repayments while you’re packing boxes.

When is Bridging the Right Strategic Move?

Choosing a bridging loan is often about lifestyle preservation as much as it is about finance. It allows you to avoid the dreaded “double move”. Moving twice means paying for removalists twice, finding short-term storage, and often losing thousands of dollars in rent. By staying in your current home until your new one is ready, you maintain a sense of calm for your family. This approach is particularly effective for downsizers who want to take their time finding the perfect smaller property without the ticking clock of a fixed sale date. When exploring how do bridging loans work in australia, it becomes clear that this tool provides the leverage needed to stay competitive in a fast-paced market while keeping your long-term equity intact.

Peak Debt vs. End Debt: The Math Behind the Bridge

To master the transition between homes, you need to look past the sticker price of your new property. The math of bridging finance is a two-stage journey that starts with your current position and ends with your long-term mortgage. Understanding How Bridging Loans Work in Australia requires a clear view of your total liability during the crossover period. This period represents the time when you are technically responsible for the debt on two houses at once.

Peak debt is the most critical figure for any lender’s assessment. It represents the absolute maximum you will owe at the height of the bridging process. Lenders use this figure to determine if you meet their internal risk profiles and equity requirements. Because this number is often significantly higher than a standard mortgage, having an expert team like The Home Loan Partners to calculate these figures accurately before you commit can save you from unexpected surprises during the application phase.

Understanding Your Peak Debt

Your Peak Debt is the sum of your existing mortgage, the purchase price of your new home, and all associated buying costs such as A$ stamp duty and legal fees. Lenders evaluate this total amount against the combined value of both properties to determine your Loan to Value Ratio (LVR). While you might have plenty of equity in your current home, the lender needs to ensure that the total debt doesn’t exceed their safety margins, typically requiring you to hold at least 20% equity across the combined portfolio. They aren’t just looking at the total; they are assessing your ability to eventually transition to a sustainable long-term position.

The End Debt: Your New Long-Term Mortgage

The accuracy of your “End Debt” calculation depends entirely on a realistic valuation of your current property. Once your first home sells, the net sale proceeds, which is the sale price minus agent fees and remaining mortgage, are applied directly to the facility. This reduces the Peak Debt down to your final, long-term mortgage. The End Debt must remain within your long-term borrowing power to ensure you can comfortably manage the mortgage once the bridge concludes.

When you look at how do bridging loans work in australia, you’ll see that the end debt is what you will be left with for the next 20 or 30 years. It’s essentially your new standard principal and interest loan. Ensuring this figure aligns with your lifestyle goals is just as important as securing the bridge itself. By focusing on the math now, you can enjoy your new home with the peace of mind that your financial foundation is secure.

The Costs of Bridging: Interest Rates and Capitalisation

Understanding how do bridging loans work in australia requires a deep dive into the interest structure. Unlike a standard mortgage where you pay interest on your current balance, bridging interest is typically calculated on the entire Peak Debt. In May 2026, with the RBA cash rate holding at 4.35%, the cost of carrying this debt is a significant consideration. While standard variable rates for owner-occupiers sit between 5.74% and 5.83% p.a., bridging rates are usually 1% to 2% higher. You will find bank bridging products ranging from 6.70% p.a. to 10.65% p.a., while private lenders may charge upwards of 12.95% p.a. for the same facility.

The most reassuring feature for many families is “Capitalised Interest”. This arrangement allows you to defer interest payments during the bridging period, adding them to your loan balance instead of paying them monthly. While this protects your immediate cash flow, it means your debt grows every month you wait for a sale. Some lenders mandate interest-only repayments to keep the debt stable, while others offer the flexibility to choose the path that best suits your current income. Beyond the interest, you should also account for setup costs. These often include establishment fees, which can be around A$595, along with valuation fees and mortgage discharge fees of approximately A$275 when you eventually close the bridge.

How Capitalised Interest Affects Your Equity

Capitalisation creates a snowball effect on your loan balance. Every month the interest remains unpaid, it’s added to the principal, and you then pay interest on that new, higher amount. This can quickly erode the equity you expect to take from your current home sale. If your property takes the full 12 months to sell, the final End Debt could be significantly higher than your initial projections. We often suggest making partial repayments during the bridge if your budget allows. Even small, inconsistent contributions can help dampen the compounding effect and protect your long-term wealth.

Comparing Lender Fees and Charges

Lenders vary widely in how they structure their fees. Some non-bank lenders might charge a risk fee, often around 0.75% of the loan amount, in exchange for more flexible servicing requirements. You should also be aware of potential “default” or “expired” rates. If your home doesn’t sell within the agreed 12-month term, some lenders may increase your interest rate as a penalty. A professional broker identifies the lenders with the lowest total cost of entry, looking past the headline rate to find the most protective terms for your specific timeline.

Qualifying for a Bridging Loan: What Lenders Look For

Securing a bridging loan in 2026 requires more than just a high income; it demands a clear exit strategy. Lenders focus primarily on the “End Debt Servicing” test. This assessment determines whether you can comfortably afford the final mortgage once your current property is sold and the proceeds are applied. Even if you have a significant salary, the bank needs to see that your long-term position is sustainable under current APRA standards. Because bridging loans are temporary facilities, many lenders are willing to overlook your ability to pay the Peak Debt during the transition, provided the interest is capitalised and the final debt is manageable.

Equity is the second pillar of your application. You typically need to hold at least 20% equity across the combined value of both properties. If you are moving from a A$1,200,000 home to a A$1,800,000 property, the lender will look at the total A$3,000,000 portfolio to ensure their risk is covered. Your credit history and income stability remain vital, especially with the 2026 shift toward payday superannuation payments, which gives lenders a more real-time view of your financial health. If you’re unsure where you stand, you can speak with our team to assess your eligibility before you start house hunting.

Closed vs. Open Bridging Finance

Lenders distinguish between “Closed” and “Open” bridging based on your current sale status. Closed bridging occurs when you already have a signed, unconditional contract for the sale of your existing home. This is the gold standard for banks because the “bridge” has a confirmed end date, making approval much faster and often resulting in lower interest rates. Open bridging is available if your house isn’t on the market yet or hasn’t sold. While this offers maximum flexibility, it is considered higher risk. In the 2026 market, many Australian lenders are shifting toward “Closed” structures to ensure settlements align perfectly.

The Servicing Buffer in 2026

When you ask how do bridging loans work in australia regarding affordability, you have to consider the interest rate stress test. Lenders apply a serviceability buffer, usually 3% above the current product rate, to your future End Debt. This ensures you can still manage the mortgage if rates rise further from the May 2026 cash rate of 4.35%. A major advantage of bridging is that if your interest is being capitalised, the lender won’t usually test your ability to service the Peak Debt. This nuance is exactly why professional guidance is vital for complex servicing scenarios, as it can be the difference between a rejection and an approval.

Navigating the Bridge: Why Professional Broker Guidance is Essential

The “Lender Lottery” is a significant hurdle for many Australian property upgraders. You might find that your current bank has a rigid policy on “Open” bridging, while a smaller lender is perfectly comfortable with your 12-month sale plan. Understanding how do bridging loans work in australia involves knowing that every institution views risk, equity, and servicing through a different lens. At The Home Loan Partners, we manage the heavy lifting of dual applications, ensuring your transition from one mortgage to a combined facility is seamless and professional. We also help you structure the loan to maximise offset benefits, which can significantly reduce your interest costs during the peak debt phase.

Our role is to act as your steady collaborator, navigating the technical jargon and complex lender requirements on your behalf. We focus on the long-term journey, ensuring that once your current property sells, your remaining mortgage transitions into a competitive rate that supports your future security. This protective approach allows you to focus on the logistics of your move while we handle the precision-oriented math behind your finance. If you are ready to take the next step, Book a consultation with The Home Loan Partners to explore your options.

Accessing a Panel of 36+ Lenders

Sticking with your current lender might feel like the path of least resistance, but it often limits your strategic options. Some banks have strict LVR caps or won’t allow capitalised interest for certain property types. By accessing our panel of 36+ lenders, we can identify specialists who offer more generous limits or longer bridging periods. This is especially helpful if you are building a new home and need the full 24-month window to complete construction. Comparing non-bank specialists alongside the major banks ensures you aren’t just getting an approval; you’re securing a facility that aligns with your specific financial goals.

A Stress-Free Path to Your New Home

A successful transition depends on a clear “Exit Strategy” established before you sign a purchase contract. We coordinate with your real estate agent and conveyancer to ensure settlement dates align as closely as possible, reducing the time you spend in the peak debt phase. Having a dependable guide to explain how do bridging loans work in australia provides the reassurance you need during a high-stakes move. We take pride in our regional expertise, helping you manage the logistics of downsizing or upgrading with patience and precision. Our involvement continues throughout the life of your loan, ensuring your home remains a milestone you can celebrate without the weight of financial stress.

Take the Next Step Toward Your New Home

Mastering the transition between properties doesn’t have to be a source of anxiety. By understanding the core mechanics of interest capitalisation and the vital math behind your Peak Debt, you’ve already taken a significant step toward securing your future. Gaining a clear perspective on how do bridging loans work in australia is the foundation of a successful move. You now have the knowledge to act with speed in a competitive market while protecting your hard-earned equity.

Our team is here to provide the steady hand you need during this high-stakes journey. We offer personalised, national guidance and access to a panel of 36+ lenders, ensuring we find a tailored structure that fits your specific goals. We specialize in the complex calculations required to manage Peak Debt safely, taking the heavy lifting off your shoulders so you can focus on the excitement of your new property. We believe that every client deserves a partner who values their long-term security as much as their immediate milestones.

Ready to secure your next home? Let our experts structure your bridging loan for a stress-free move.

Your dream home is within reach, and we’re ready to help you bridge the gap with precision and care.

Frequently Asked Questions

Can I get a bridging loan if I haven’t sold my house yet?

Yes, you can certainly secure finance before your current home is sold through what is known as “Open” bridging. This facility is specifically designed for buyers who find their next property before they’ve even listed their current one. Lenders will evaluate the equity in your existing home and your projected “End Debt” to ensure the transition is viable. It’s a popular choice for those who want to act quickly in a competitive market without the restriction of a “subject to sale” condition.

What is the maximum term for a bridging loan in Australia?

The standard maximum term for a bridging loan is 12 months for established properties. If you’re using the facility for a construction project, many Australian lenders extend this timeframe to 24 months to account for building stages and potential delays. It’s vital to have a clear sale strategy in place, as these loans are strictly short-term instruments intended to be repaid in full once your first property settlement is finalised.

How much deposit do I need for a bridging loan?

You typically don’t need a cash deposit for a bridging loan because the lender uses the equity built up in your current home as security. Most lenders require you to hold at least 20% equity across the combined value of both your existing property and the new one you’re purchasing. This “equity-as-deposit” model is a key part of how do bridging loans work in australia, allowing you to buy your next home without liquidating other assets first.

Are bridging loan interest rates higher than normal home loans?

Yes, bridging loan interest rates generally carry a premium of 1% to 2% above standard variable home loan rates. In May 2026, with the RBA cash rate at 4.35%, you’ll find bridging rates starting from approximately 6.70% p.a. and reaching over 10% p.a. depending on the lender’s risk assessment. While the rate is higher, the short-term nature of the loan means the total interest cost is often manageable when compared to the expense of a double move.

What happens if my house doesn’t sell within the 12-month bridging period?

If your property remains unsold as the term expires, you must communicate with your lender immediately to explore an extension. Lenders may grant additional time, but they might also increase your interest rate or require you to start making principal and interest repayments on the full Peak Debt. In extreme cases, a lender could require a forced sale to recover the funds. This is why a realistic valuation and a steady marketing plan for your current home are essential from day one.

Can I use a bridging loan for a construction project?

You can use specialized construction bridging loans to fund the build of your new home while staying in your current one. These facilities are structured with longer terms, often up to 24 months, to provide a buffer for the construction timeline. This approach is highly effective for families who want to avoid the stress of moving into a rental while their new home is being built, providing a much smoother transition once the final occupation certificate is issued.

Do I need to make repayments during the bridging period?

Most bridging loans offer the flexibility of “capitalised interest”, meaning you don’t have to make monthly repayments during the bridging period. Instead, the interest is added to your loan balance and paid out from the proceeds of your home sale. This protects your monthly cash flow during a time when you might be managing moving costs. However, some lenders may still require you to service the interest on your original mortgage amount if your equity position is tighter.

Is it better to sell first or use a bridging loan?

The choice depends on your financial buffer and the current speed of the property market. Selling first is safer because you’ll know exactly how much you have to spend, but it often involves the high cost and hassle of moving twice and paying rent. Using a bridging loan is often the better strategic move if you find your dream home and need to act fast. It simplifies the logistics and removes the pressure of a forced sale, provided you’ve calculated your Peak Debt accurately.