Did you know the average Australian household now carries debt that is approximately 180% greater than its annual income? With the RBA cash rate held at 4.35% as of May 2026, managing multiple credit cards and personal loans alongside a mortgage has become an exhausting balancing act for many families. If you’re feeling the squeeze of high interest rates and scattered due dates, a debt consolidation home loan australia could offer the structural financial reset you need to regain control of your future.

It’s completely understandable to feel anxious about how these compounding debts impact your credit score and monthly disposable income. We believe you deserve a clear, steady path toward financial security rather than just another temporary fix. This guide teaches you how to leverage your home equity to roll expensive debts into a single, lower-rate mortgage repayment while avoiding long-term interest traps. We’ll explore the latest APRA lending standards and show you how to streamline your finances into one manageable monthly commitment that actually leads to being debt-free.

Key Takeaways

- Understand how to transform multiple high-interest debts into a single, structured mortgage repayment to simplify your monthly cash flow.

- Learn how to calculate your usable equity using the 80% LVR rule to determine if a debt consolidation home loan australia is the right strategic move for your property.

- Discover how to avoid the common “interest trap” by structuring your refinancing to ensure short-term relief doesn’t lead to higher total costs over the life of your loan.

- Follow a clear, step-by-step roadmap to prepare your documentation and collaborate with a professional to compare options across dozens of lenders.

- See how a tailored financial reset through expert refinancing can provide a predictable path toward becoming debt-free without the stress of managing multiple creditors.

What is a Debt Consolidation Home Loan in Australia?

At its core, a debt consolidation home loan australia is a strategic financial tool that allows you to roll various high-interest debts into your existing mortgage. Instead of juggling multiple repayments to different creditors, you use the equity in your home to pay off those balances in full. This leaves you with one single, monthly commitment at a significantly lower interest rate than most personal loans or credit cards. Understanding What is debt consolidation? is the first step toward reclaiming your financial peace of mind and simplifying your life.

The reason this strategy is so effective lies in the fundamental difference between “secured” and “unsecured” debt. Because your home serves as collateral, lenders view the mortgage as a lower risk, which translates to a much lower interest rate for you. In contrast, credit cards and many personal loans are unsecured, often carrying interest rates that exceed 20% p.a. in the current market. By shifting these balances onto your mortgage, you’re effectively swapping high-cost debt for low-cost debt, which can save you thousands of dollars in annual interest charges.

In the current 2026 environment, where the RBA cash rate sits at 4.35% and the average owner-occupier variable rate is approximately 6.26% p.a., many Australian homeowners are finding that traditional personal loans are becoming prohibitively expensive. With household debt levels remaining high, a debt consolidation home loan australia acts as a protective buffer. It allows you to manage the heavy lifting of debt repayment through a single, predictable channel that aligns with your long-term property goals.

Common Debts You Can Consolidate

Most Australians use this path to clear high-interest credit card balances, which can otherwise take decades to pay off if you’re only making minimum payments. You can also include personal loans and high-interest car finance into the arrangement. Depending on the specific lender’s criteria, it’s often possible to include outstanding tax debts or medical bills. The goal is to clear your financial slate and focus on one clear, steady path forward with a lender that values your stability.

Refinancing vs. Home Loan Top-Ups

You generally have two paths to achieve this financial reset. Refinancing involves moving your entire mortgage to a new lender who offers a more competitive rate or a structure better suited to your 2026 goals. A top-up, however, means increasing your limit with your current bank. While a top-up might feel faster, refinancing often unlocks deeper long-term savings. By comparing options across 36+ lenders, you can ensure you’re not just getting a quick fix, but a sustainable foundation for your future security.

Assessing Your Equity and Eligibility in 2026

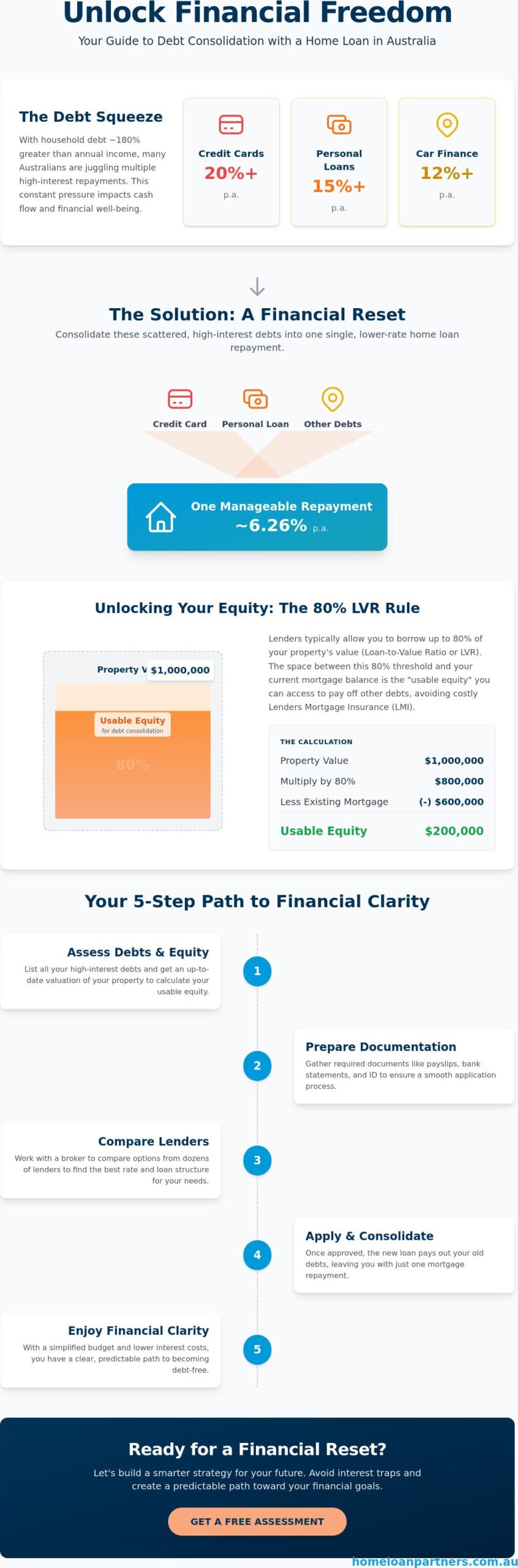

Before you can roll your high-interest debts into your mortgage, you need to understand how Australian lenders view your eligibility in the current market. Since February 1, 2026, APRA has enforced tighter restrictions on high debt-to-income (DTI) lending. Lenders are now limited to a 20% share of new home loans where the DTI ratio is six times or more. This means your income needs to support the combined weight of your mortgage and consolidated debts more robustly than in previous years. It’s not just about what you owe; it’s about your total financial capacity to manage the new arrangement.

Your usable equity serves as the foundation for this strategy. Most lenders follow the 80% Loan to Value Ratio (LVR) rule, which allows you to borrow up to 80% of your property’s current value minus your existing mortgage balance. For a deeper look at the risks and benefits of this approach, you can consult this Australian government guide to debt consolidation. Understanding these boundaries early helps ensure that your debt consolidation home loan australia application is built on realistic expectations rather than guesswork.

The 80% LVR Threshold

Staying under 80% LVR is crucial because it helps you avoid Lenders Mortgage Insurance (LMI), which can be a significant upfront cost. In 2026, property valuations have been influenced by the 4.35% cash rate, making an accurate appraisal more important than ever. If your consolidation push takes you over that 80% mark, the cost of LMI might outweigh the interest savings you hope to achieve. We often help clients look at refinancing options that keep them within this “sweet spot” to maximize their long-term benefit.

Credit Score and Repayment History

Lenders now have a very clear window into your financial habits. Thanks to Comprehensive Credit Reporting (CCR), your repayment history for the last six to twenty-four months is visible. A “clean” history, showing no missed payments or overdrawn accounts in the last six months, is vital for securing the most competitive rates. Before you apply for a debt consolidation home loan australia, it’s wise to tidy up your bank statements and ensure all your current bills are paid on time to present the strongest possible case to a new lender.

Finally, be prepared for the “Credit Limit” trap. Lenders assess your serviceability based on your total credit limits, not just your current balances. If you have a $15,000 credit card limit but a $0 balance, they still factor in the potential repayment of that full $15,000. Gathering your payslips, bank statements, and debt payout letters ahead of time will make the entire process feel far more manageable and predictable.

The Financial Math: Savings vs. Long-Term Interest Costs

Lowering your interest rate is only half the battle. If you move a $30,000 credit card debt from a 20% interest rate to a 6% mortgage rate, your monthly stress will drop instantly. However, if you let that debt sit for the full 30 year term of your home loan, you could end up paying more in total interest than you would have on the original high interest card. This is the “Interest Trap” that many homeowners overlook. As noted in the government advice on debt consolidation, it’s vital to ensure the restructuring actually saves you money in the long run.

To put this into perspective, paying off $30,000 at a 20% interest rate over three years costs roughly $10,100 in interest. If you roll that same amount into a 30 year mortgage at 6%, your monthly payment drops from about $1,115 to just $180. While this provides massive immediate relief, the total interest paid over 30 years balloons to approximately $34,750. When considering a debt consolidation home loan australia, the math must extend beyond the monthly repayment amount to protect your future wealth.

To avoid this, we recommend a split loan strategy. This allows you to isolate the consolidated portion of your debt and set it to a shorter repayment schedule, such as five years. You still benefit from the lower mortgage interest rate; however, you aren’t paying for your 2026 holiday for the next three decades. Before committing, you should calculate the break even point by factoring in any refinancing fees or discharge costs from your current lender.

Short-Term Cash Flow vs. Long-Term Wealth

Consolidation can improve your monthly budget by hundreds of dollars, giving you the breathing room needed to handle rising living costs. There is a significant psychological benefit to seeing a single monthly repayment instead of five different due dates. Consolidation is a tool for liquidity, not a discount on the debt itself. It buys you time and reduces immediate pressure, but the goal remains the same: eliminating the principal balance as quickly as possible.

Strategies to Pay Off Debt Faster

- Use an Offset Account: Keep your savings in an account linked to the consolidated portion of your loan to reduce the daily interest charged.

- Maintain Old Repayment Levels: If you were paying $1,000 a month on various debts, keep paying that same amount toward your new mortgage balance to smash the principal.

- Create a Sub-Account: Ask your lender to set up a separate sub-account for the consolidated debt so you can track your progress independently from your main mortgage.

How to Consolidate Debt into Your Mortgage: A Step-by-Step Guide

Taking the first step toward a financial reset requires a clear plan and a bit of organization. While your current bank might suggest a simple top-up, a truly strategic approach often involves looking beyond your existing lender to find a structure that prioritizes your long-term wealth. Following a structured process ensures that your application for a debt consolidation home loan australia is handled with precision and care.

- Step 1: Document Gathering. Start by collecting your most recent mortgage statement along with current balances and interest rates for every credit card, car loan, or personal debt you wish to include.

- Step 2: Professional Consultation. We compare options across 36+ Australian lenders to find the right fit. This is where we analyze whether a professional refinancing assessment will yield better results than staying with your current bank.

- Step 3: Property Valuation. A formal valuation is conducted to determine your current equity. This confirms your Loan to Value Ratio (LVR) and ensures the new loan amount remains within a safe, sustainable range.

- Step 4: Submission and Payout. Once approved, the new lender typically pays out your high-interest debts directly. This removes the temptation to spend the funds and ensures your financial slate is wiped clean immediately.

- Step 5: Account Closure. This is the most critical psychological step. You must formally close your old credit accounts to prevent “debt creep” and ensure you don’t find yourself back in the same position a year from now.

Why a Broker is Essential for Consolidation

Working with an expert collaborator gives you access to a much broader range of products than any single bank can offer. Many non-bank lenders have more flexible debt-to-income (DTI) frameworks, which can be vital if your current bank has declined a top-up. We specialize in “packaging” your application to highlight your serviceability and repayment history, effectively bypassing the “loyalty tax” that many long-term bank customers unknowingly pay. Before you begin, you can Check out our borrowing power calculator to see your current capacity.

Closing the Loop: Post-Consolidation Habits

The success of a debt consolidation home loan australia depends heavily on what happens after the ink has dried. There is a real danger of “re-loading” credit cards once they show a zero balance. To protect your progress, we recommend setting up automated mortgage repayments that coincide with your pay cycle. This predictable rhythm fosters security and ensures you stay on the clear path to becoming debt-free that we’ve mapped out together.

Partnering with The Home Loan Partners for a Financial Reset

We understand that the path to financial freedom often feels like navigating a maze of paperwork and fine print. At The Home Loan Partners, we act as your expert collaborator, taking the heavy lifting of lender negotiations off your shoulders. Choosing a debt consolidation home loan australia is a significant decision, and our team is here to ensure that your short-term need for cash flow doesn’t compromise your long-term wealth. We don’t just facilitate a transaction; we build a partnership that supports your milestones for years to come.

Our process is built on transparency and precision. We compare products from over 36 Australian lenders to find a structure that fits your specific 2026 goals. Whether you’re looking at refinancing to secure a lower rate or restructuring your current debt, we provide the steady hand you need to make informed choices. By translating complex industry jargon into practical language, we empower you to take control of your financial narrative.

A Steady Hand in a Complex Market

The Australian lending environment changed significantly in early 2026, with the RBA holding the cash rate at 4.35% and APRA tightening debt-to-income limits. Our national expertise allows us to navigate these different lender appetites with ease. We focus on alleviating your stress through clear, benefit-driven communication, ensuring you always know where you stand. For example, we recently helped a family consolidate $40,000 of high-interest personal debt, which was sitting at an average rate of 17.95%. By rolling this into their mortgage at the current average variable rate of 6.26%, they reduced their monthly interest obligations by hundreds of dollars, creating the breathing room they desperately needed.

Start Your Journey Today

Beginning your financial reset is as simple as reaching out for a confidential conversation. In your first meeting with our expert brokers, we’ll listen to your aspirations and review your current debt structure without any high-pressure tactics. We’ll provide a clear, rhythmic plan that outlines exactly how a debt consolidation home loan australia can work for your unique situation. Our goal is to replace your anxiety with a sense of calm, steady progress toward a debt-free future.

Your financial security is a long-term journey, and we’re committed to being by your side every step of the way. When you’re ready to move forward, we’ll manage the application process from start to finish, letting you focus on what matters most in your life.

Reclaiming Your Financial Future

A debt consolidation home loan australia provides more than just a lower interest rate; it offers a deliberate path to financial clarity. By carefully assessing your usable equity and choosing a structure that avoids long-term interest traps, you can transform scattered liabilities into a single, manageable commitment. This strategic reset allows you to breathe easier today while protecting your hard-earned wealth for the years ahead.

Navigating the 2026 lending environment doesn’t have to be a solo effort. Our team brings deep expertise in complex loan structures and refinancing to help you find the most efficient way forward. With access to over 36 bank and non-bank lenders, we provide the professional, unbiased guidance needed to ensure your home works as hard for you as you do for it. We’re here to manage the heavy lifting so you can focus on achieving your major life milestones with confidence.

Take control of your debt with a tailored home loan strategy from The Home Loan Partners

You have the power to change your financial trajectory starting today. We’re ready to act as your steady hand and expert collaborator throughout this journey, ensuring you feel supported and secure every step of the way.

Frequently Asked Questions

Is it a good idea to consolidate debt into my home loan?

It can be a highly effective strategy if you prioritize reducing interest costs and simplifying your monthly cash flow. By rolling high-interest credit cards or personal loans into a mortgage, you benefit from a lower interest rate, which is currently averaging 6.26% p.a. for owner-occupiers. However, it’s only a beneficial move if you commit to paying off the debt quickly rather than stretching it over the full 30 year term.

Will consolidating debt affect my credit score?

Applying for a debt consolidation home loan australia involves a hard credit inquiry, which might cause a minor, temporary dip in your score. Over the long term, this move often improves your credit health by reducing your total credit utilization and ensuring you make consistent, on-time payments. A single, manageable repayment is much easier to track than multiple due dates across different creditors.

Can I consolidate debt if I have a fixed-rate home loan?

Yes, you can consolidate debt with a fixed-rate loan, but you may face break costs if you choose to refinance the entire amount before the term ends. Alternatively, some lenders allow you to create a separate variable split or top-up for the consolidated portion while keeping your existing fixed rate intact. We can help you weigh the cost of these fees against the potential interest savings to ensure the move makes sense for your 2026 goals.

How much equity do I need to consolidate my debts?

You generally need enough equity to keep your total Loan to Value Ratio (LVR) at or below 80% to avoid Lenders Mortgage Insurance (LMI). This means your total mortgage, including the consolidated debts, shouldn’t exceed 80% of your property’s current value. Under the APRA regulations effective from February 2026, lenders also look closely at your debt-to-income ratio to ensure you can comfortably service the new loan amount.

What are the costs involved in refinancing for debt consolidation?

Refinancing typically involves several administrative costs such as discharge fees from your current lender, application fees for the new loan, and government registration charges. You might also need to pay for a formal property valuation to confirm your usable equity. While these upfront costs exist, they’re often outweighed by the significant interest savings achieved by moving away from double-digit credit card rates.

Can I consolidate my tax debt into my mortgage?

Consolidating ATO tax debt into your home loan is possible, though it’s subject to specific lender policies and your overall serviceability. Some lenders are more flexible with tax obligations than others, provided you have a clear plan to remain compliant in the future. We specialize in finding lenders who understand these complex scenarios and can structure a debt consolidation home loan australia that helps you move forward cleanly.

How long does the debt consolidation process take in Australia?

The process typically takes between two to four weeks from the initial application to the final payout of your debts. This timeframe includes the property valuation, the lender’s credit assessment, and the discharge of your existing mortgage if you’re switching lenders. Gathering your documentation, like payslips and recent debt statements, ahead of time can significantly speed up the approval stage.

Do I have to close my credit card accounts after consolidating?

Most lenders will require you to close your credit card accounts as a condition of the loan approval to ensure you don’t accumulate new debt. Even if they don’t mandate it, closing these accounts is a vital step in preventing debt creep. This helps protect your financial reset and ensures your new, streamlined repayment structure remains effective for the long term.