What if your construction loan wasn’t just a pool of debt, but actually a protective shield that kept your builder accountable at every stage of the project? Building a home is likely the biggest investment you’ll ever make, so it’s completely natural to feel a bit anxious about those large invoices landing in your inbox. You want to ensure every dollar is spent wisely and that you aren’t paying for work that hasn’t actually happened yet. Understanding your construction loan progress payments schedule is the most effective way to protect your investment and maintain a healthy partnership with your builder.

We know that the financial side of a build can feel overwhelming, especially with construction costs now accounting for a record 64.4% of a new home’s sales price in 2026. This guide will help you master the financial roadmap of your build, giving you total confidence in how your funds are disbursed and how to manage your cash flow. We will provide a clear timeline of when money leaves your loan, explain the bank’s inspection requirements, and show you how interest-only payments keep your monthly costs manageable while your home is under construction.

Key Takeaways

- Master the financial roadmap of your build by understanding how funds are released in increments only after specific milestones are met.

- Learn how to navigate your construction loan progress payments schedule to ensure you only pay interest on the funds drawn down, rather than the full loan amount.

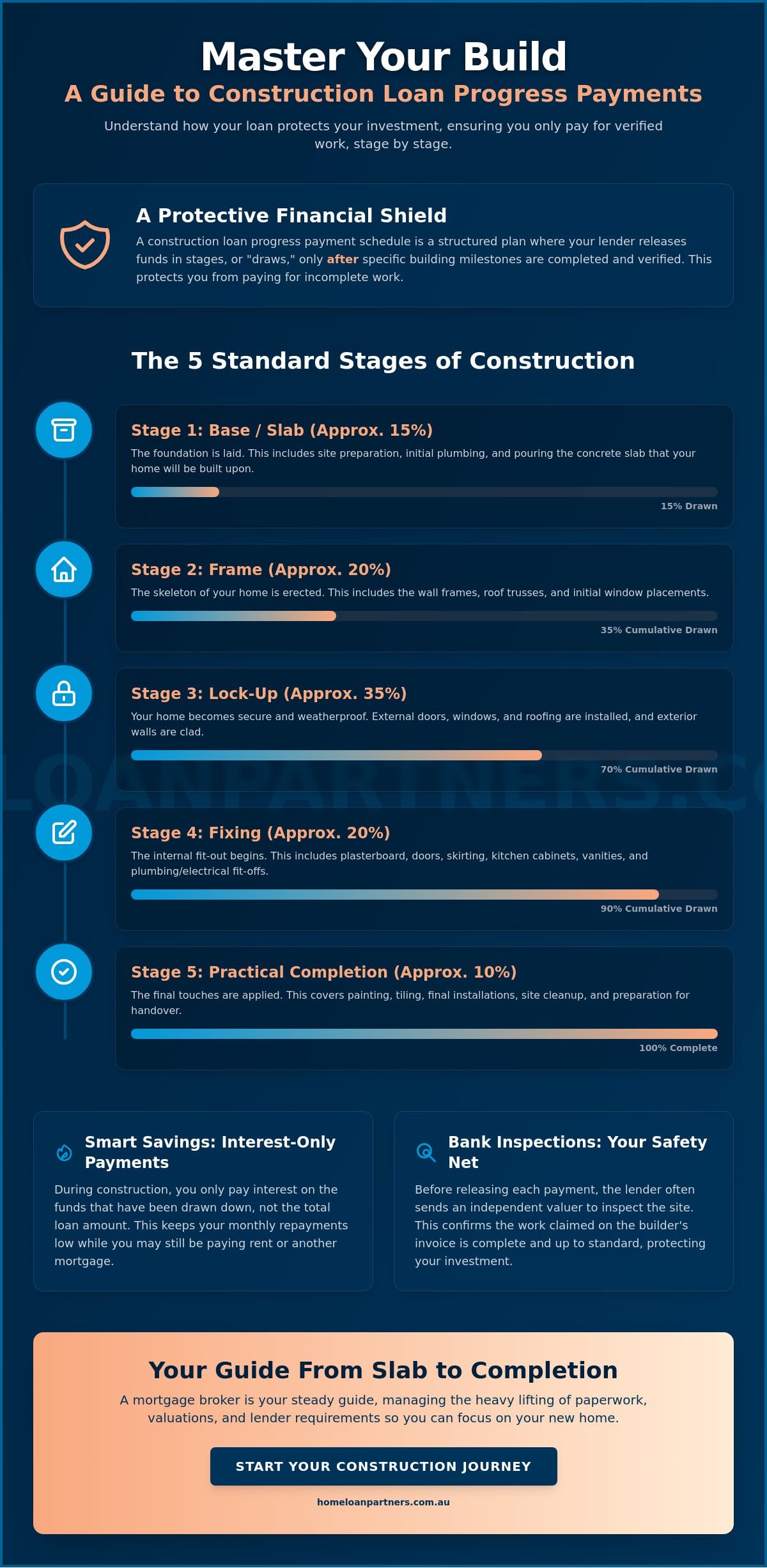

- Gain clarity on the bank inspection process and how independent valuations protect your investment by confirming work is complete before invoices are paid.

- Discover how to manage build variations and provisional sums to avoid unexpected out-of-pocket expenses and keep your project moving forward.

- Understand the vital role of a mortgage broker as your steady guide, managing the heavy lifting of paperwork and lender requirements from slab to completion.

What is a Construction Loan Progress Payment Schedule?

A construction loan progress payments schedule is a structured financial roadmap that governs how your lender releases funds to your builder throughout the project. Unlike a standard mortgage where you receive the entire loan amount in one lump sum at settlement, a construction loan works in stages. Your lender holds the total approved amount and pays it out in increments, known as “draws,” only after specific construction milestones have been completed and verified. This ensures your money is always working in direct proportion to the physical progress of your new home.

This structure acts as a vital safeguard for your equity and financial security. By releasing funds in stages, the lender prevents the risk of over-capitalization, ensuring you don’t pay for work that hasn’t been finished or materials that aren’t yet on site. These payment stages are typically based on a Schedule of Values or a payment schedule clearly outlined in your Fixed Price Building Contract. It creates a transparent environment where you, your builder, and your lender are all aligned on what constitutes a completed stage before any money changes hands.

One of the most significant benefits for your monthly budget is the interest-only repayment structure. During the build, you only pay interest on the amount of money that has been drawn down from your loan. If your total loan is $500,000 but you’ve only used $100,000 for the initial stages, your monthly repayments are calculated only on that $100,000. This keeps your cash flow manageable while you might still be paying rent or a mortgage on your current residence.

The Difference Between Drawdowns and Lump Sums

Lenders refuse to pay the full loan amount upfront because a house that is only partially built doesn’t provide enough security for the full debt. If a builder were to stop work unexpectedly, a lump sum payment would leave both you and the bank at a significant financial loss. Progress payments manage this risk by keeping the loan balance in sync with the actual value on the ground. Most lenders provide an interest-only period for the duration of the build, which typically lasts between 12 and 24 months or until the home is ready for you to move in.

Key Documents You Will Need

To establish your construction loan progress payments schedule, your lender will need several specific documents to verify the project’s legitimacy and protect your investment. These include:

- Council-approved plans and specifications: These confirm that your build is legal and adheres to all local building regulations.

- Builder’s insurance and licence: Your lender will verify that these are current to protect against structural defects or the rare event of builder insolvency.

- The Schedule of Payments: Found within your building contract, this document outlines the exact percentage of the total cost due at each milestone, from the initial deposit to the final handover.

The 5 Standard Stages of Construction Progress Payments

Your construction loan progress payments schedule is typically divided into five distinct milestones. Each stage represents a significant physical advancement in the build. Understanding these stages helps you visualize where your money is going and ensures you only pay for tangible results. This structure is a standard feature in many financial products, as highlighted in this consumer guide to construction loans. By following this roadmap, you maintain control over the project’s financial health from the first shovel in the ground to the final coat of paint.

The journey begins with the Base or Slab stage. This covers the foundation work, including initial plumbing and the pouring of the concrete floor. Once the slab has cured, we move to the Frame stage. This is where you see the skeleton of your home take shape, with internal and external walls being erected. The Enclosed or Lock-up stage follows, which is a major relief for many homeowners. At this point, the roof, windows, and external doors are installed, making the house weatherproof and secure.

The final two steps bring the home to life. The Fixing stage involves the installation of internal linings, cabinetry, and plumbing fixtures. Finally, Practical Completion covers the final touches like painting and site clean-up. At this stage, the home is ready for a final inspection before you receive the keys. Each milestone is a collaborative victory for you and your builder.

Typical Percentage Breakdowns for Each Stage

While every contract is unique, industry standards often follow a specific percentage of the total contract price. For example, the slab stage might represent 10% to 15% of the total cost, while the frame stage often sits around 15% to 20%. Lock-up is usually the largest draw, often ranging from 25% to 35%. These percentages can vary based on state regulations and the specific policies of your lender. In Australia, the initial deposit is legally capped in most states at 5% for contracts over a certain value. If you’re unsure if your builder’s requested percentages align with current market standards, talking to a construction loan specialist can provide the clarity you need.

What Triggers a Payment Request?

A payment request is triggered when your builder issues a progress claim. This is a formal invoice stating that a specific stage of the construction loan progress payments schedule has been reached. You shouldn’t simply pay this invoice immediately. Instead, you should visit the site or receive a report to verify that the work described in the claim is actually complete. You are the first line of defense in ensuring the build matches the invoice. For the final stage, the builder will issue a ‘Notice of Completion,’ which signifies that the home is ready for the final bank valuation and handover.

How to Manage the Drawdown Process and Valuations

Once you have established your construction loan progress payments schedule, the actual mechanics of moving money from the bank to your builder begins. This process, often called the drawdown, is designed to be a collaborative effort between you, your lender, and your construction team. It starts when your builder reaches a milestone and sends you an invoice. Your role is to act as the project’s steady hand, verifying that the work matches the claim before you sign the “Authority to Pay” form. This document is your formal instruction to the bank to release the funds. Generally, you can expect the funds to reach your builder within three to five business days, though this timeline can shift if a physical inspection is required.

Lenders prioritize security, which is why they don’t release funds without verification. For most projects, the bank will charge specific fees for this oversight. As of 2026, a typical draw inspection fee is about $125 per visit, while a draw processing fee is around $195 per draw. These costs are a small price to pay for the peace of mind that comes from knowing an expert has verified the structural integrity and progress of your future home before any payment is made.

The Role of the Bank Valuer

Lenders don’t just take your word for it; they often send an independent valuer to the site to ensure the bank’s security is protected. While policies vary, inspections typically occur at the slab, lock-up, and final completion stages. The valuer’s job is to confirm that the value added to the land matches the amount being requested in the progress claim. If a valuer’s estimate comes in lower than the builder’s invoice, it can create a temporary funding gap. To ensure a smooth inspection, make sure the site is easily accessible and that all work for that specific stage is visibly finished. A clean, well-managed site projects professionalism and helps the valuer complete their report without delays.

Dealing with Shortfalls in Funding

It’s a standard industry practice known as the “first-in” rule: you must contribute your own funds before the lender starts drawing from the loan. This means your deposit and any additional savings you’ve committed to the project are paid to the builder for the initial invoices. Only once your equity is fully utilized will the bank begin making payments from the construction loan. If your build costs increase due to unexpected site issues or premium material choices, you may face a shortfall. In these cases, you’ll need to cover the difference with your own cash or apply for a loan top-up, which requires a new assessment of your borrowing capacity. Managing these expectations early prevents stress and keeps the build on track.

Navigating Variations and Delays in Your Build

Even with the most meticulous planning, your building journey will likely encounter a few turns in the road. These are known as variations. A variation occurs whenever there is a change to the original plans or specifications of your contract. Whether you decide to upgrade your kitchen cabinetry or need to account for unexpected soil conditions, these changes can impact your construction loan progress payments schedule. It’s vital to handle these adjustments formally. If a variation increases the total cost, your lender will need to see a signed variation document. In many cases, you may need to pay for these additions from your own savings if they exceed the original loan approval.

You should also keep a close eye on Prime Cost (PC) items and Provisional Sums (PS). PC items are allowances for specific materials, like light fixtures or tiles, while PS items are estimates for work where the final cost is uncertain, such as site excavation. If the actual cost ends up higher than the estimate in your contract, the builder will invoice you for the difference. To protect your financial security, we recommend maintaining a contingency reserve of at least 5% of the total construction cost. This buffer helps you manage these fluctuations without the stress of scrambling for extra funds mid-build.

One rule remains absolute: never pay for a stage in advance. A builder might ask for an early payment to “secure materials” or “keep the momentum going,” but doing so breaks the protection of your progress payment schedule. Your lender will not reimburse you for work that hasn’t been completed, and paying early leaves you with zero leverage if the work isn’t finished to a high standard. Keeping the payments strictly tied to the physical milestones ensures that the builder remains accountable and your equity stays protected.

Managing Cost Overruns and Variations

Lenders are generally supportive of mid-build changes, but they require a clear paper trail. Small variations can occasionally cause a pause in your progress payments if the bank needs to re-evaluate the property’s future value. To keep things moving, always communicate with your lender before signing off on a major change. This proactive approach ensures that your funding remains aligned with the builder’s expectations and prevents any awkward delays when the next invoice arrives. If you’re concerned about how variations might affect your borrowing capacity, speak with our construction loan experts today for a personalized review of your project.

What Happens if the Builder Goes Bust?

The thought of a builder facing financial difficulty is a major source of anxiety for many homeowners. This is where your construction loan progress payments schedule serves as your ultimate safety net. Because you only pay for work that has been physically completed and verified, your financial exposure is strictly limited. If work stops, you still have the remaining loan funds to engage a new contractor. Additionally, Domestic Building Insurance (DBI) provides a layer of protection to help cover costs if a builder cannot complete the project. If you notice work has stopped for an extended period, contact your lender and legal representative immediately to assess your options.

How a Mortgage Broker Simplifies Your Construction Journey

While a construction loan provides the necessary funds, a mortgage broker provides the expertise to navigate the complex administrative requirements that come with building from scratch. We act as your primary intermediary, managing the dense paperwork and communication between you and the lender. This partnership is especially valuable when setting up your construction loan progress payments schedule. Different lenders have varying degrees of flexibility regarding stage percentages and inspection triggers; we help you find the one that aligns best with your builder’s contract.

We offer access to a panel of over 36 lenders, including many specialized construction products that traditional big banks rarely advertise to the public. This wide-reaching access allows us to tailor your loan structure to match your specific cash flow needs. We don’t just settle the loan and walk away. Our team remains by your side throughout the entire build, helping you manage the drawdowns and ensuring the lender receives exactly what they need to release funds at every milestone.

Alleviating the Stress of Progress Claims

Managing the relationship between your builder and your bank is often the most stressful part of the build. If a payment is delayed, it can stall work on site and strain your relationship with your contractor. We help ensure invoices are processed efficiently to keep your builder happy and the project moving forward. When valuation issues arise or the bank’s bureaucracy feels overwhelming, we act as your professional advocate. We troubleshoot these hurdles directly with the lender to find a resolution that keeps your funding on track and your site active.

Planning for the Long-Term Journey

Our commitment to your financial security continues long after you receive the keys. Once your home reaches practical completion, we guide you through the transition from interest-only payments to a standard principal and interest structure. This is a critical moment to review your financial strategy. Since your home is now a completed asset, you may qualify for more competitive rates that weren’t available during the construction phase. We’ll help you review your options to ensure your mortgage remains as efficient as possible for the years ahead.

Let us manage the heavy lifting of your construction loan so you can focus on the excitement of watching your dream home take shape.

Build With Total Financial Confidence

Your journey from a vacant lot to a finished home is a major life milestone. By mastering your construction loan progress payments schedule, you ensure that your financial roadmap remains as solid as your home’s foundation. You now understand how to navigate the five standard stages of construction, manage the bank’s valuation requirements, and protect your equity against unexpected variations. This knowledge transforms the building process from a source of anxiety into a series of manageable, celebrated victories.

You don’t have to manage the heavy lifting alone. As NSW-based specialists with access to a panel of over 36 lenders, we provide the personalized support you need through every stage of your build. We’ll help you find the right loan structure and manage the complex paperwork between you and your builder. Book a free consultation to structure your construction loan today and let’s turn your vision into a reality. We’re here to be your steady guide throughout this entire life-changing journey. Your dream home is closer than you think.

Frequently Asked Questions

Can I change the progress payment schedule in my contract?

You can negotiate the schedule with your builder before signing, but it must ultimately meet your lender’s approval. Banks have strict internal policies regarding how much they are willing to release at each milestone to ensure their security is protected. If your builder requests a 30% deposit or front-loads the payments, the lender will likely reject the contract. We help you review these percentages early to ensure they align with industry standards and bank requirements.

Do I need to pay a deposit to the builder before the loan starts?

Yes, you typically pay the initial 5% deposit using your own savings or equity. This follows the “first-in” principle where your personal contribution is exhausted before the bank begins to draw from the loan facility. This initial payment covers the builder’s costs for insurance, council permits, and site preparation. Paying this directly to the builder is a standard part of starting your building journey and demonstrates your commitment to the project.

What is a ‘Practical Completion’ inspection and why is it vital?

Practical Completion is the final milestone where you and the builder walk through the home to ensure it is finished according to the contract. It’s your opportunity to identify any minor defects or “snag list” items that need fixing before you move in. This inspection is vital because once you sign the final payment authority, you’re confirming the work is complete. The bank will then conduct a final valuation to ensure the property’s value matches their security requirements.

Are interest rates higher on construction loans during the build?

Interest rates for construction loans in June 2026 typically range between 6.5% and 9% for traditional bank lenders. While these rates might be slightly higher than some standard mortgages, the total cost is often lower because you only pay interest on the funds actually drawn down. This interest-only structure during the construction phase keeps your monthly repayments manageable while you’re still paying for your current accommodation. We’ll help you compare rates across 36+ lenders to find the most competitive option.

What happens if the bank valuation comes in lower than the contract price?

If the valuation is lower than your contract price, you’ll need to cover the difference with your own cash. Lenders calculate your borrowing capacity based on the lower of the contract price or the bank’s valuation. This often happens if the land is over-valued or if the build includes luxury features that don’t add equivalent market value. Our team acts as your advocate during this process, helping you understand the valuer’s report and exploring options to bridge any funding gaps.

Can I do some of the work myself and still get progress payments?

Most lenders require a registered builder with a fixed-price contract to manage the construction loan progress payments schedule. Being an owner-builder is seen as a higher risk, which means many standard banks won’t provide a traditional construction loan for DIY work. If you plan to handle specific stages yourself, you’ll usually need to fund those parts with your own savings or seek out specialized niche lenders who accommodate owner-builders under very specific conditions.

How do I pay the builder’s final invoice?

You pay the final invoice only after the home has reached practical completion and you’ve received a Certificate of Occupancy. The bank will send a valuer for one last site visit to confirm the home is 100% finished. Once the valuer gives the green light, you’ll sign the final Authority to Pay form. The lender then releases the remaining funds to the builder, and you can finally collect your keys and celebrate your new home.

Does the First Home Owner Grant (FHOG) count towards my progress payments?

The First Home Owner Grant is typically paid directly into your construction loan progress payments schedule at the slab stage. While the timing can vary slightly depending on your state’s regulations, it generally counts as part of your total contribution. This means the grant funds are used to pay a portion of an early invoice, reducing the amount you need to draw from the bank. We’ll help you coordinate the paperwork so the grant is ready when your builder’s first major claim arrives.