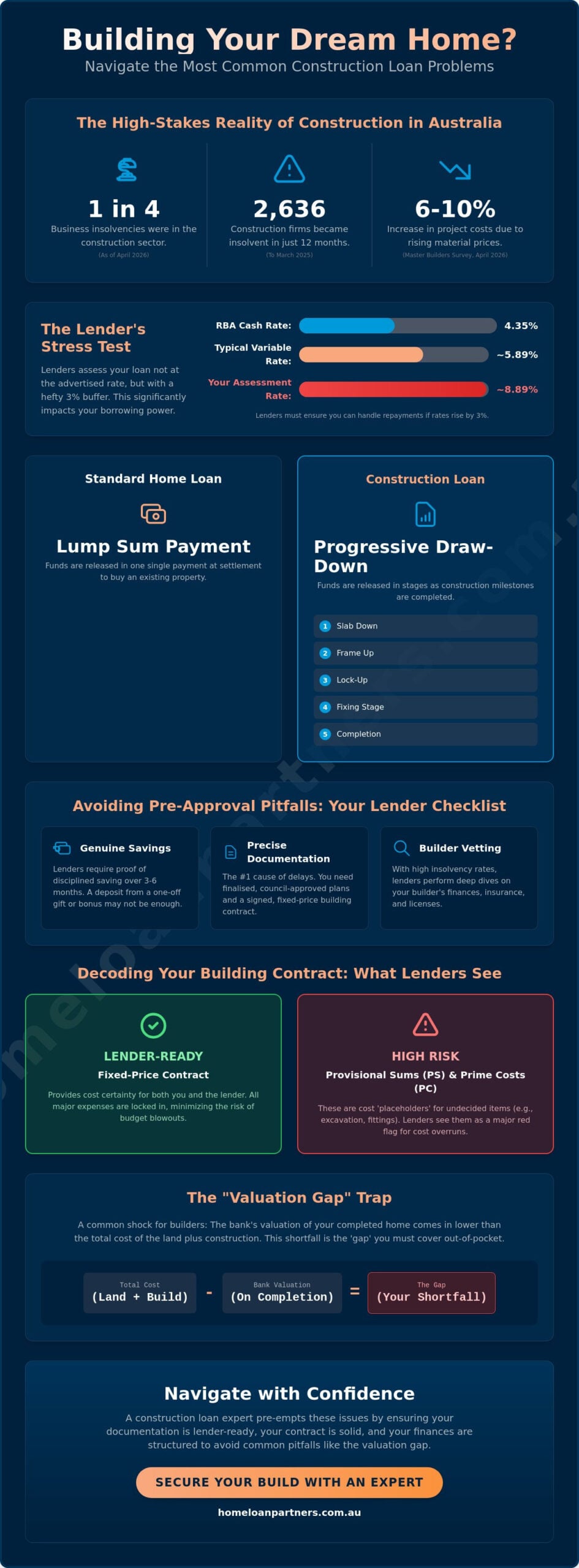

Did you know that the construction sector accounted for a quarter of all business insolvencies in Australia as of April 2026? It’s a sobering figure that explains why securing your dream build often feels more like a high-stakes balancing act than a simple financial transaction. You’ve likely felt the weight of rising material costs and the pressure of the RBA’s 4.35% cash rate, which can make common construction loan problems feel like insurmountable barriers to your family’s future security.

We understand that the complexity of progress payment schedules and the fear of valuation shortfalls can be exhausting. Our goal is to act as your steady guide, helping you pre-empt these hurdles so you can focus on the excitement of your new home. This guide will show you exactly how to solve frequent lending issues, from managing unexpected cost overruns to ensuring your builder’s financial health is robust enough for the journey ahead. We’ll walk through a clear path to approval that prioritizes your peace of mind and keeps your budget firmly under control, ensuring your project remains a source of joy rather than stress.

Key Takeaways

- Learn why lenders test your borrowing capacity with a serviceability buffer and how a progressive draw-down facility differs from a standard loan.

- Understand the critical difference between fixed-price contracts and provisional sums to ensure your project stays lender-ready.

- Discover how to pre-empt common construction loan problems like the “valuation gap” to avoid unexpected out-of-pocket costs.

- Master the documentation needed for smooth progress payments and learn why mid-build variations can impact your funding.

- See how partnering with a steady expert can help you navigate complex lender policies and ensure a smooth journey from first brick to final inspection.

Avoiding Pre-Approval Pitfalls: Why Construction Loans Get Stuck at the Gate

Construction loans are a different breed of finance. Unlike a standard mortgage where the lender hands over a lump sum at settlement, construction finance operates as a progressive draw-down facility. This means your lender releases funds in stages, paying your builder only when specific milestones are achieved. This structure is a fundamental part of understanding project finance and how banks manage the risks involved in creating an asset from the ground up. One of the most common construction loan problems occurs when borrowers treat the application like a standard home loan, only to find the requirements are significantly more complex.

Many first-time builders are also caught off guard by the ‘Genuine Savings’ hurdle. Lenders don’t just want to see that you have a deposit; they want proof that you’ve built that capital through disciplined saving over at least three to six months. If your deposit comes entirely from a gift or a one-off bonus, you might find your application stalled. We act as your steady hand during this phase, helping you organize your finances so they meet the specific, often rigid, criteria that construction lenders demand.

The 3% Serviceability Buffer in 2026

As of June 2026, the Reserve Bank of Australia’s cash rate sits at 4.35%. While you might see variable rates starting around 5.89%, lenders won’t assess your application at that level. They apply a 3% serviceability buffer, testing your ability to manage repayments at nearly 9%. This buffer is designed to protect you, but it also means your borrowing capacity for a new build might be lower than for an established home. To strengthen your position, it’s wise to reduce credit card limits and clear minor debts well before you seek pre-approval. This proactive approach shows the lender you’re prepared for the long-term journey.

Documentation: The ‘Death by a Thousand Papercuts’

Lenders require absolute precision before they commit to your project. Incomplete or pending council-approved plans are the leading cause of application delays. You can’t rely on loose estimates; you need a signed, fixed-price building contract that clearly defines the scope of work. Lenders also perform deep dives into your builder’s background. With the construction industry facing a 5.8% insolvency rate as of April 2026, banks are incredibly cautious. They’ll verify that your builder’s insurance, licenses, and financial track record are current and lender-compliant. We help you gather this documentation early, ensuring your project is ready for the green light without unnecessary back-and-forth.

Builder and Contract Red Flags: Ensuring Your Project is Lender-Ready

Choosing your builder is perhaps the most critical decision of your entire project. In the current economic climate, lenders are scrutinizing these choices more than ever. With the Australian construction industry seeing a 5.8% insolvency rate in April 2026, banks are rightfully protective of their investment. They often look for established firms with a proven track record, making it much harder for owner-builders or small, unrated construction firms to secure finance. This heightened scrutiny is one of the common construction loan problems that can derail a project before the first shovel hits the ground.

Lenders essentially want to ensure that the builder you’ve chosen can actually finish the job for the price they’ve quoted. In the 12 months to March 2025, 2,636 construction companies became insolvent; a 23% increase from the previous year. This data drives banks to demand a comprehensive, fixed-price contract. They are looking for stability and transparency to avoid funding a project that might stall halfway through. Understanding how construction loans work from a lender’s perspective helps you see why they demand such rigorous vetting of your contractor and their financial health.

The Danger of Provisional Sums and Prime Cost Items

A contract might look like a fixed-price agreement on the surface, but it’s often riddled with Provisional Sums (PS) and Prime Cost (PC) items. These are essentially “placeholders” for costs that haven’t been finalized, such as excavation or high-end kitchen fittings. Lenders view these as a significant risk because they lead to cost overruns. According to a Master Builders Queensland survey in April 2026, project costs have already increased by 6-10% due to material price rises. If the final price of your foundation work exceeds the estimate, you’ll have to cover the difference out-of-pocket. To keep your loan stable, we recommend limiting these items to ensure your total contract remains truly fixed.

Standard vs. Non-Standard Progress Payment Schedules

Lenders follow a strict rhythm when releasing funds, typically aligned with Housing Industry Association (HIA) or Master Builders standards. A standard schedule usually involves five or six stages: Deposit, Base, Frame, Enclosed, Fixing, and Final. If a builder asks for “front-loaded” payments, such as a 20% deposit instead of the standard 5%, your lender will likely reject the application. They want to ensure the value of the work completed always matches or exceeds the money released. If you’re unsure if your builder’s terms will pass the bank’s test, our team can help you review your construction loan options to find a lender whose policies align with your project’s needs. Navigating these contract nuances early prevents common construction loan problems from stalling your progress later on.

The Valuation Gap: Managing Price Shortfalls and Equity Requirements

The “as-if-complete” valuation is the cornerstone of your construction finance. Unlike buying an existing property where the market value is largely determined by the agreed sale price, a lender assesses your project based on what it will be worth once the final nail is driven. This process is a frequent source of stress because the valuer’s estimate often doesn’t match the actual cost of your land and building contract. When the total cost exceeds the bank’s valuation, you’re faced with a “valuation gap,” which is one of the most frustrating common construction loan problems for Australian families.

A frequent trap for eager builders is over-capitalising. If you choose to build a high-spec, architecturally unique home in a neighborhood where most houses are modest, the valuer might not find enough comparable sales to justify your costs. They’re conservative by nature. They want to ensure that if they had to sell the property tomorrow, they could recover their funds. If your loan-to-value ratio (LVR) exceeds 80% because of this gap, you’ll also need to factor in Lenders Mortgage Insurance (LMI). This can add thousands to your upfront costs, potentially pushing your dream home out of reach if you haven’t prepared for the shortfall.

Why Valuations Come Back ‘Short’

Valuers rely on historical data, but the market moves fast. In the year to March 2026, building material costs rose by 2.5%, the largest annual increase since late 2023. While your builder’s contract reflects these current 2026 prices, a valuer might be looking at sales from six months ago when costs were lower. This lag is a primary reason for shortfalls, especially in new estates where comparable data is scarce. Furthermore, if your design is highly customized, it lacks “comparability.” Valuers prefer standard layouts because they’re easier to sell to the general market, leading to more conservative figures for bespoke projects.

Bridging the Equity Gap

Facing a shortfall doesn’t mean your project is over. It simply requires a strategic pivot. You might choose to increase your cash deposit to cover the difference or work with your builder to reduce the scope of the build, perhaps by opting for standard finishes instead of premium ones. As your expert collaborator, we can also explore using existing equity in other properties you own to secure the loan. If the valuation seems demonstrably wrong, we can initiate a “valuation challenge” by providing more accurate comparable sales data, or we can simply approach a different lender whose valuer may have a more realistic view of the local market. Our role is to find that clear, stress-free path forward, even when the initial numbers don’t align.

Mid-Build Hurdles: Navigating Variations and Progress Payment Delays

Approval is a major milestone, but it’s not the finish line. Once construction begins, the relationship between you, your builder, and your lender enters its most active phase. This is often where common construction loan problems surface, particularly when reality on the ground deviates from the initial plans. Managing these shifts requires a proactive approach and a clear understanding of your lender’s expectations to ensure your budget doesn’t spiral out of control.

The “variation trap” is a frequent source of stress. It’s natural to want to make changes as you see your home take shape. Perhaps you’ve decided to upgrade the kitchen cabinetry or add extra lighting. These changes can quickly complicate your finance because most lenders approve your loan based on the original fixed-price contract. They won’t easily increase the loan amount mid-build, meaning you’ll usually need to fund variations out of your own pocket. If you do need to increase the loan, it involves a full reassessment of your application, which can halt work for weeks.

Handling Contract Variations Mid-Construction

To avoid “payment stops” from the bank, you must document every change with a signed variation order. Lenders are conservative and want to see that the value of the property still supports the loan. If you’re planning significant changes, it’s vital to talk to us first. We can help you determine if your current equity can cover the cost or if a formal loan increase is viable. Having a dedicated cash buffer for these moments is the best way to keep your project on track without stressing over every minor adjustment.

The Progress Payment ‘Dance’

Releasing funds is a structured process. First, your builder issues an invoice for a completed stage. Second, you sign a claim form. Third, the bank may send an inspector to verify the work. Finally, the funds are released. Delays often happen because of missing documentation, such as termite protection certificates or glazing certificates. If the lender’s inspector disagrees with the builder’s progress, it can create significant friction. We help you manage this process by ensuring your paperwork is flawless before it hits the bank’s desk. If you’re worried about payment friction, you can apply for a construction loan review to ensure your current facility is still the right fit for your build’s progress.

In 2026, supply chain issues continue to impact build timelines. With material costs rising 2.5% in the first quarter of the year, projects are often taking longer than anticipated. This is critical because most construction loans have a set “interest-only” period, typically 12 to 24 months. If your build exceeds this timeframe, you might be forced into principal and interest repayments while you’re still paying for your current accommodation. We act as your steady guide, helping you negotiate extensions with your lender to ensure your cash flow remains manageable until the keys are in your hand.

Strategic Solutions: How a Mortgage Broker Pre-empts Construction Loan Issues

The construction journey is complex, but you don’t have to walk it alone. We position ourselves as the steady expert in the three-way partnership between you, your builder, and your lender. By identifying potential common construction loan problems before they reach a bank’s credit team, we save you time and prevent the heartbreak of a late-stage rejection. Our role is to manage the heavy lifting, translating technical lender requirements into a clear, stress-free path forward for your family.

One of the greatest advantages we offer is access to more than 36 lenders. This diversity is crucial because every bank has a different appetite for risk. Some might be wary of high-density estates, while others specialize in bespoke architect-led projects. We perform a rigorous “pre-submission audit” on your application. We look at your builder’s solvency data, review the progress payment schedule against industry standards, and check your serviceability against the current 3% buffer. This proactive approach ensures that when we submit your application, it’s already optimized for success.

Tailored Loan Structures for Complex Builds

Not every build fits the standard mold. A knockdown-rebuild in an established suburb has different financial requirements than a greenfield project in a new development. We provide unbiased advice to match your specific project to the right financial product. Whether you’re exploring SMSF construction loans to build your retirement wealth or looking for investment-specific finance, we ensure the structure supports your long-term goals. We prioritize your understanding, stripping away the jargon to explain how each option impacts your future security.

Your Partner from Slab to Shingles

Our commitment to your journey doesn’t end when the loan is approved. We act as a reliable intermediary, facilitating communication between your builder’s accounts team and the lender’s draw-down department. This ensures that when an invoice is issued, the progress payment process happens as smoothly as possible. As your home nears completion, we’ll help you manage the transition from an interest-only facility to a standard principal and interest loan, ensuring your cash flow remains stable. You deserve a guide who values your project as much as you do. Start your stress-free building journey with The Home Loan Partners today.

Building Your Future with Confidence and Clarity

Embarking on a new build is a significant life milestone, but the path from slab to shingles requires more than just a great architect. By understanding common construction loan problems, you’ve already taken the first step toward protecting your investment. You now know how to navigate the 3% serviceability buffer, why fixed-price contracts are non-negotiable in 2026, and how to bridge the valuation gap before it stalls your progress.

We’re here to ensure your journey is as smooth as possible. With access to over 36 Australian lenders and specialised expertise in NSW building regulations, we provide the steady hand you need. Our team offers end-to-end support, managing the complex three-way relationship between you, your builder, and your lender until the day you receive your keys. Don’t let financial complexity dim the excitement of your new home. Book a Personalised Construction Loan Strategy Session today and let’s turn your blueprints into a reality together. You’ve got a vision for your future, and we’ve got the expertise to help you reach it.

Frequently Asked Questions

What happens if my builder goes into liquidation during the build?

You must contact your lender immediately and notify your insurance provider to lodge a claim under your Home Building Compensation (HBC) cover. The lender will pause all progress payments until a new, licensed builder is vetted and a replacement contract is signed. This is a complex transition that requires a steady hand to manage, as the new builder’s quote may be higher than the remaining loan funds.

Can I get a construction loan for a DIY or owner-builder project?

Securing finance as an owner-builder is significantly more difficult in 2026 because lenders view these projects as high-risk. Most major banks have moved away from this space, often requiring a 40% deposit and proof of trade qualifications if they consider it at all. It’s generally more straightforward to secure approval by partnering with a registered builder who provides a fixed-price contract.

Why is the bank valuation lower than my building contract price?

Bank valuers use conservative, historical data from past sales, which often lags behind the 2026 reality of rising material costs. If your build includes high-end custom features that don’t exist in nearby “comparable” homes, the valuer may not assign them full market value. This creates a shortfall that you’ll need to cover with extra equity or a larger cash deposit.

How do progress payments work with a construction loan?

Your lender releases funds in five or six distinct stages, such as the slab, frame, and lock-up, rather than providing a lump sum. After your builder completes a stage and issues an invoice, you’ll sign a draw-down request for the bank to pay the builder directly. This system protects you by ensuring the bank only pays for work that has been physically verified on-site.

Can I make extra repayments during the construction phase?

You can typically make extra repayments into your loan, but doing so won’t always reduce your monthly interest-only obligations. Because you’re only charged interest on the amount the builder has actually drawn down, many clients find that using an offset account is a more flexible strategy. This approach helps mitigate common construction loan problems by keeping your capital accessible for unexpected variations.

What is a ‘fixed-price’ building contract and why do I need one?

A fixed-price contract is a legal agreement where the builder commits to completing your home for a set total, barring any specific “provisional sums” for unknown costs like excavation. Lenders insist on these contracts because they provide a ceiling for the project’s cost. Without this certainty, the bank cannot accurately assess your ability to finish the build if material prices spike mid-construction.

What happens if the construction takes longer than the interest-only period?

If your build exceeds the standard 12 to 24-month interest-only period, the loan may automatically revert to principal and interest repayments. This shift can create a significant cash flow squeeze if you’re still paying for temporary accommodation. We can act as your collaborator to negotiate an extension with the lender, especially if the delay is caused by documented supply chain issues.

Do I need a larger deposit for a construction loan than an established home loan?

While you can still access construction finance with a 5% deposit through certain government schemes, you’ll need a larger “genuine savings” buffer than you would for an established home. Lenders want to see that you can handle common construction loan problems, such as a valuation shortfall or a 6% to 10% increase in project costs. Having a clear financial cushion ensures your project stays on track even if the initial estimates move.