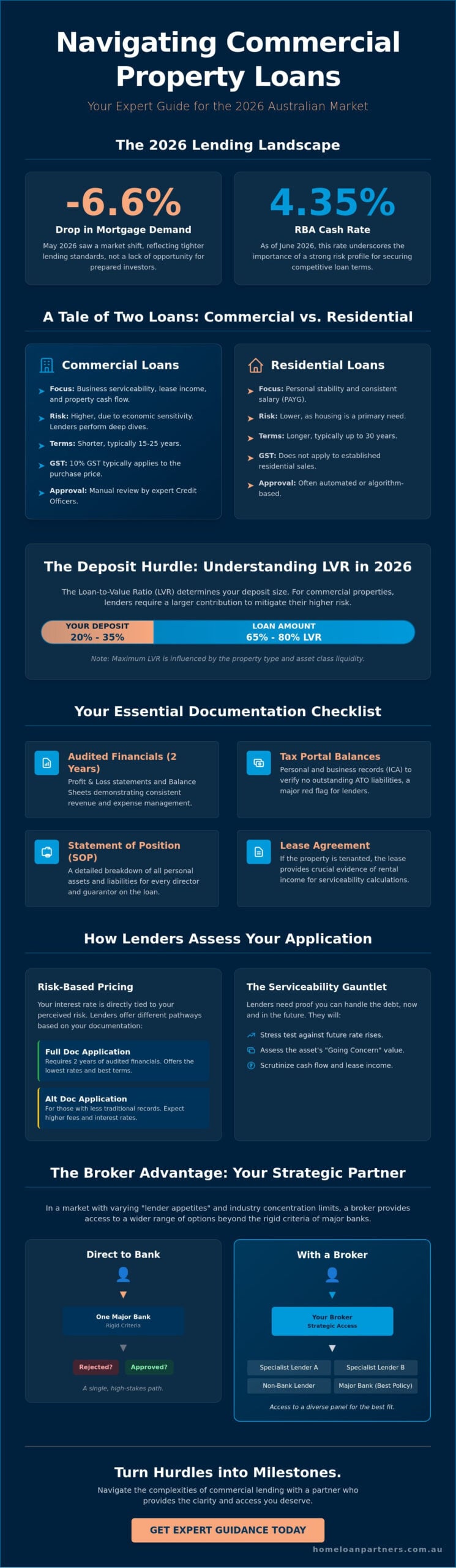

Did you know that overall mortgage demand across Australia dropped by 6.6% in May 2026? While that figure might sound discouraging, it actually reflects a major shift in how banks assess risk rather than a lack of opportunity. Lenders have tightened their standards, making it more important than ever to understand that commercial property loan requirements australia wide are no longer just a box-ticking exercise; they’re about building a compelling case for your business.

It’s understandable if you feel overwhelmed by the higher deposit demands and the dense financial reporting required in today’s market. You’re likely facing Loan-to-Value Ratios that require a 20% to 35% deposit, along with a rigorous focus on your business’s cash flow and serviceability. We know this process can feel opaque and stressful, but we’re here to act as your steady guide through the complexity and provide the clarity you deserve.

This guide provides a clear, expert breakdown of exactly what you need to master the lending environment in 2026. You’ll find a comprehensive checklist of required documents, a detailed look at LVRs for various property types, and the insights needed to choose a lender that aligns with your long-term goals. Let’s turn these hurdles into a clear path toward your next major investment milestone.

Key Takeaways

- Discover why commercial lenders focus on business serviceability and lease income rather than just your personal salary when assessing risk.

- Gain a clear checklist of the essential documentation, such as audited financials and tax portal balances, needed to satisfy commercial property loan requirements australia wide.

- Learn how the liquidity of different asset classes influences your maximum LVR and the specific deposit size you’ll need to provide in 2026.

- Understand how banks stress test your application against future rate rises and the impact of “Going Concern” versus “Vacant Possession” status.

- Explore how partnering with a broker provides access to a diverse panel of specialist lenders that often look beyond the rigid criteria of major banks.

Commercial vs. Residential: Why the Requirements Differ

If you’ve only ever applied for a home loan, the shift to commercial lending can feel like entering a different country with its own language. Residential lending focuses on your personal stability and consistent salary. Commercial lending, however, treats the property as a standalone business venture. Lenders view these as higher-risk assets because commercial tenants are more sensitive to economic shifts than families needing a roof over their heads. This fundamental difference in risk is why a commercial mortgage involves a much deeper dive into the asset’s performance rather than just your individual wealth.

When you look at commercial property loan requirements australia wide, the biggest shift occurs in how you prove you can afford the debt. Instead of just looking at your pay slips, banks scrutinize “business serviceability” and “lease income.” They want to see that the rent coming in from the property, or the cash flow from your business if you’re an owner-occupier, can comfortably cover the interest and principal. Because the risk is higher, loan terms are usually shorter, often capped between 15 and 25 years. This faster repayment schedule ensures the bank’s exposure reduces quickly as the building’s specific utility changes over time.

Don’t forget the impact of Goods and Services Tax (GST). Unlike residential sales, commercial transactions usually attract a 10% GST on the purchase price. While you can often claim this back as an Input Tax Credit, you still need the capital to cover it upfront. This can significantly impact your initial borrowing power and the amount of “clear” cash you need to bring to the settlement table.

The Concept of Lender Appetite

Lending isn’t a one-size-fits-all process. Every Australian bank has “concentration limits,” which are essentially caps on how much they’ll lend to specific industries or property types. If a bank already has too many retail shops in its portfolio for 2026, they might reject your application regardless of your financial strength. This is where the Credit Officer plays a vital role. Unlike residential loans that are often approved by algorithms, commercial deals are manually reviewed by these experts who judge the “story” and the viability of your specific investment.

Risk-Based Pricing in 2026

With the RBA cash rate sitting at 4.35% as of June 2026, your “risk profile” is the primary driver of your interest rate. Lenders offer different paths depending on your paperwork. A “Full Doc” application requires two years of audited financials and offers the lowest rates. If your records are less traditional, an “Alt Doc” path might be available, though it usually comes with higher fees. In this environment, your business plan is just as vital as your bank statements; it proves to the lender that you have a proactive strategy to manage the investment through changing market conditions.

Essential Documentation for Commercial Loan Applications

Preparing your application is essentially building a legal and financial story for the bank. To meet commercial property loan requirements australia wide, you’ll need a much more robust folder of evidence than a standard residential application. Lenders in 2026 are looking for deep transparency to offset the inherent risks of the commercial sector. By organizing these documents early, you present yourself as a low-risk, professional borrower, which can often lead to faster approvals and more competitive terms.

A standard application package generally requires the following items:

- Two years of audited financial statements: Lenders want to see your profit and loss statements and balance sheets. They aren’t just looking for a high number; they’re looking for consistent revenue and how you’ve managed operational expenses over a full business cycle.

- Tax portal balances: You’ll need to provide records from your personal and business tax portals. Lenders check your Integrated Client Account (ICA) balances to ensure you don’t have undisclosed tax debt, as any outstanding ATO liabilities are a major red flag in the current market.

- Statement of Position (SOP): Every director and guarantor must provide a detailed SOP. This document lists all personal assets and liabilities, giving the bank a clear picture of your overall financial health and your ability to support the loan if needed.

- Lease agreements and Rent Roll: If the property is tenanted, you must provide current lease agreements and a verified Rent Roll. The bank will scrutinize the “weighted average lease expiry” (WALE) to determine how long the income stream is guaranteed.

- Executive Summary: This is a brief business plan that explains the logic of the transaction. It should outline your experience in the industry, the property’s utility, and your long-term strategy for the asset.

Financial Ratios Lenders Scrutinise

Lenders focus heavily on the Interest Cover Ratio (ICR) to ensure your cash flow can comfortably handle interest payments even if market conditions shift. However, the true gold standard for commercial serviceability is the Debt Service Cover Ratio (DSCR). The DSCR is the ratio of operating income to total debt servicing. If this ratio falls below the lender’s threshold, they may reduce the loan amount to ensure you aren’t overleveraged.

The Alt-Doc Alternative

If your tax returns aren’t yet finalized or your business structure is particularly complex, you might consider an “Alt-Doc” loan path. These products allow you to prove income using accountant letters or recent Business Activity Statements (BAS) instead of full audited financials. While this path involves less paperwork, the trade-off is usually a higher interest rate and more significant upfront fees. If you’re unsure which documentation path fits your current situation, discussing commercial and business loans with a specialist can help you weigh the costs against the benefits of a faster approval.

LVR Requirements and Property Asset Classes

When you’re looking at commercial property loan requirements australia wide, the Loan-to-Value Ratio (LVR) is the most critical number you’ll encounter. It isn’t just a random percentage; it’s a direct reflection of how “liquid” a lender believes your property is. In simple terms, liquidity is the speed at which a bank could sell the asset if you were no longer able to service the debt. A standard office in a capital city is highly liquid, whereas a specialized cold-storage facility in a remote area is much harder to offload. This perceived risk dictates how much of a deposit you’ll need to bring to the table.

In 2026, standard LVR benchmarks for most commercial properties range between 65% and 80%. This means you’ll typically need a deposit of 20% to 35% of the property’s value. However, the type of security you offer changes the math. “Non-specialized” properties, like standard warehouses or retail shops, are the easiest to finance because they can be used by almost any business. “Specialized” assets, such as petrol stations, hotels, or childcare centers, often see LVRs capped at 60% or lower. Location remains a heavy hitter too. Even in our national market, lenders might reduce your borrowing power by 5% to 10% if the property is in a regional area with a smaller pool of potential buyers.

Industrial and Warehouse Requirements

Industrial property remains the preferred asset class for many Australian lenders in 2026. Because these buildings are versatile, they often command the highest LVRs, frequently reaching 75% or even 80% for prime locations. Lenders prioritize “clear span” designs and excellent truck access, as these features attract the widest range of tenants. You’ll also need to provide evidence of a “clean site,” as environmental contamination is a significant deal-breaker for commercial credit teams. If the site has a history of heavy manufacturing, expect a request for a detailed environmental audit early in the process.

Retail and Office Space Criteria

For retail and office investments, the Weighted Average Lease Expiry (WALE) is the metric that carries the most weight. A long WALE provides the steady, predictable income that lenders love to see. Following the shifts in work culture over the last few years, banks are still scrutinizing office occupancy rates with a cautious eye. They prefer buildings with diverse tenant mixes rather than a single large tenant whose departure could leave the building empty. In retail, foot traffic data and the presence of “anchor tenants,” like major supermarkets, can significantly improve your chances of securing a higher LVR and better interest rates.

The Serviceability Test: Proving You Can Pay

Passing the serviceability test is about more than showing a profit on your last tax return. Meeting commercial property loan requirements australia involves passing a rigorous “stress test” where lenders assess your ability to pay if interest rates rise. Even with the RBA cash rate sitting at 4.35% as of June 2026, banks typically add a buffer of 2% to 3% to your current rate. They want to ensure that your business or the property’s rental income can withstand a shift in the economic climate without putting the investment at risk.

Lenders look at serviceability through two distinct lenses: “Going Concern” and “Vacant Possession.” If you’re purchasing a property with a strong tenant already in place, the bank focuses on the “Going Concern” serviceability, primarily relying on the existing lease income. If you’re buying an empty building to move your own business into, they assess “Vacant Possession” serviceability. This requires a deep dive into your business’s historical cash flow to prove you can afford the mortgage as if you were your own tenant.

If the higher deposit requirements discussed earlier are a hurdle, you can often use existing residential equity to strengthen your application. By providing a residential property as additional security, you can sometimes reduce the cash deposit needed for the commercial purchase. However, be wary of common pitfalls in your cash flow projections. Overestimating future rent increases or failing to account for GST and ongoing maintenance costs can lead to an immediate rejection. Lenders prefer conservative, data-backed projections that acknowledge the reality of the 2026 market.

Lease Covenants and Tenant Quality

The quality of your tenant directly impacts your loan’s risk profile. A “Blue Chip” tenant, such as a government department or a national franchise, provides a level of security that can actually lower your interest rate. Conversely, month-to-month leases are viewed as high-risk because the income could vanish with 30 days’ notice. Banks also look closely at “incentives” or “rent-free periods” offered to tenants. These are often stripped out of the bank’s valuation to find the “true” net rent, which might be lower than the headline figure on the lease.

Director Guarantees and Security

In the Australian commercial market, “Joint and Several” director guarantees are a standard requirement. This means every director is personally responsible for the entire loan amount, not just their percentage of ownership. You can often limit your personal exposure through smart loan structuring or by offering a General Security Agreement (GSA) over business assets. This allows the bank to take a charge over the business’s equipment or accounts receivable as secondary security. If you want to explore how these structures can work for your specific goals, you can apply for commercial and business loans with our expert team to find the right fit for your portfolio.

How a Mortgage Broker Navigates the 2026 Lending Landscape

Accessing the right lender is half the battle in today’s market. Many investors head straight to their primary bank, only to find that the Big Four often have a limited appetite for specific commercial sectors or regional locations. A broker changes this dynamic by providing access to a panel of over 36 lenders. This includes non-bank specialists who often view specific asset classes with more optimism than a traditional institution. By understanding the full spectrum of commercial property loan requirements australia wide, a broker identifies which lender’s current “caps” actually work in your favor.

Success isn’t just about finding a lender; it’s about how you present your case. We act as your expert collaborator to “package” your application. This process involves more than just gathering documents; it’s about strategic presentation. We highlight your business strengths and proactively mitigate risks, such as the “Vacant Possession” serviceability hurdles we explored earlier. We translate your complex financial statements and BAS records into a clear narrative that credit officers can approve with confidence. Our partnership continues long after the keys are in your hand. We regularly review your commercial loan as your business grows, ensuring your debt structure evolves alongside your success.

Tailoring the Loan Structure

Choosing between “Principal and Interest” and “Interest Only” repayments is a vital decision for your tax efficiency and cash flow. While interest-only periods can maximize your immediate liquidity, P&I structures build equity faster and satisfy lenders seeking lower-risk profiles. We also explore the availability of offset accounts. These are rare in the commercial world, but certain non-bank specialists offer them to help you manage tax liabilities and surplus cash. We ensure your loan is structured with the flexibility to support future growth, including potential equipment finance needs or your next property acquisition.

Ready to Secure Your Commercial Future?

The first step toward your investment milestone is a no-obligation strategy session. We’ll assess your current position against the 2026 lending criteria and map out a clear path forward. Our team manages the heavy lifting from the initial application through to settlement, ensuring a smooth and stress-free experience. If you’re ready to take the next step, speak with a Commercial Loan Specialist at The Home Loan Partners to discuss your options today.

Securing Your Commercial Investment Milestone

Achieving your property goals in the current market requires more than just a strong balance sheet. It’s about presenting a clear, professional case that aligns with a lender’s specific risk profile. We’ve explored how commercial property loan requirements australia wide depend on factors like asset liquidity, lease quality, and rigorous serviceability stress tests. Whether you’re targeting a high-yield warehouse or a specialized retail space, the right preparation turns a complex process into a manageable path forward.

You don’t have to navigate these intricate financial waters alone. Our team provides personalized, stress-free guidance from the initial application right through to settlement. With access to over 36 Australian lenders and deep expertise in complex commercial and SMSF structures, we’re here to do the heavy lifting for you. We focus on the details so you can focus on growing your business and securing your future.

Take the first step toward your next major acquisition today. Book a Commercial Strategy Session with The Home Loan Partners and let’s build your success together. We’re ready to act as your steady guide and expert collaborator every step of the way.

Frequently Asked Questions

What is the minimum deposit for a commercial property loan in Australia?

The minimum deposit for a commercial property loan typically ranges between 20% and 35% of the property’s purchase price. This requirement corresponds to a Loan-to-Value Ratio (LVR) of 65% to 80%. For specialized properties that are harder to sell, such as childcare centers or petrol stations, lenders may require a larger deposit of 40% or more to offset the higher risk.

Can I use my home as security for a commercial property loan?

You can certainly use the equity in your residential property as additional security to strengthen your application. This strategy allows you to tap into the value of your home to cover part of the commercial deposit, which reduces the amount of “clear” cash you need upfront. It’s a proactive way to leverage your existing assets to reach a new investment milestone.

How is a commercial loan different from a residential home loan?

Commercial loans focus on business cash flow and rental income rather than just your personal salary. Unlike residential mortgages, commercial property loan requirements australia wide usually involve shorter loan terms of 15 to 25 years and do not offer Lenders Mortgage Insurance (LMI). The assessment is a manual process where a credit officer judges the specific utility and “liquidity” of the building you’re buying.

What is a “Low Doc” commercial loan and do I qualify?

A “Low Doc” commercial loan is an alternative for business owners who don’t have finalized tax returns or audited financial statements. You can often qualify by providing Business Activity Statements (BAS) or an accountant’s letter to verify your income. While these loans offer a faster path to approval with less paperwork, they typically come with higher interest rates and require a larger deposit to mitigate the lender’s risk.

Do I need a business plan to get a commercial loan approved?

A business plan or executive summary is highly recommended, especially for owner-occupiers or complex investment structures. This document acts as your “case” to the bank, proving that you have a steady strategy to manage the property and service the debt. It helps the lender understand your industry experience and your plan for managing potential vacancies or interest rate shifts.

How long does the commercial loan approval process usually take?

The approval process generally takes between four and eight weeks from the time you submit your application to the final settlement. This timeline is longer than residential lending because it requires a manual credit assessment and a specialized commercial valuation of the property. We work as your expert collaborator to manage the heavy lifting and keep the process moving steadily toward completion.

What are the typical fees associated with commercial property loans?

You should expect to pay several standard costs, including lender application fees, specialized valuation fees, and legal fees for the bank’s solicitors. These fees cover the rigorous due diligence required for commercial assets. We’ll provide a clear, transparent breakdown of these costs during our strategy session so you can plan your capital requirements with total confidence.

Is GST included in the loan amount for a commercial property?

GST is usually not included in the loan amount, so you’ll need to account for an additional 10% of the purchase price at settlement. Most commercial transactions are “plus GST,” and while you can often claim this back as an input tax credit later, you must have the funds available to pay it upfront. This is a critical detail in your cash flow planning that we’ll help you navigate before you sign a contract.