Why is it that finding clear interest rates for commercial loans feels like trying to solve a puzzle with half the pieces missing? You’ve likely noticed that unlike residential mortgages, business lending rarely comes with a simple “shelf price” you can find on a billboard. It’s a common frustration for Australian business owners who are ready to expand but find themselves blocked by opaque pricing and complex application requirements. We understand that this lack of transparency makes it difficult to project your cash flow with confidence, especially when you’re also managing high upfront valuation costs and legal fees.

This guide is here to provide the clarity you deserve. We’ll show you exactly how lenders calculate your quote and how you can position your business to secure a more competitive rate. We will walk you through the nuances of risk-based pricing in the current 2026 environment, where the RBA cash rate sits at 4.35%. You’ll also learn how to weigh fixed versus variable options and find a lender that values your specific security type. By the end of this article, you’ll have a clear, stress-free path toward financing that supports your long-term goals.

Key Takeaways

- Understand why interest rates for commercial loans vary between businesses based on risk-priced models and specific asset classes.

- Discover how your choice of security, such as retail or industrial property, and your deposit size impact the final interest rate you receive.

- Learn to balance the flexibility of variable rates with the long-term cash flow certainty provided by fixed-rate terms.

- Identify practical steps to strengthen your financial position and reduce liabilities before submitting your application to lenders.

- See how partnering with The Home Loan Partners grants you access to a diverse panel of over 36 lenders to find a policy that fits your unique needs.

Understanding Commercial Interest Rates in Australia

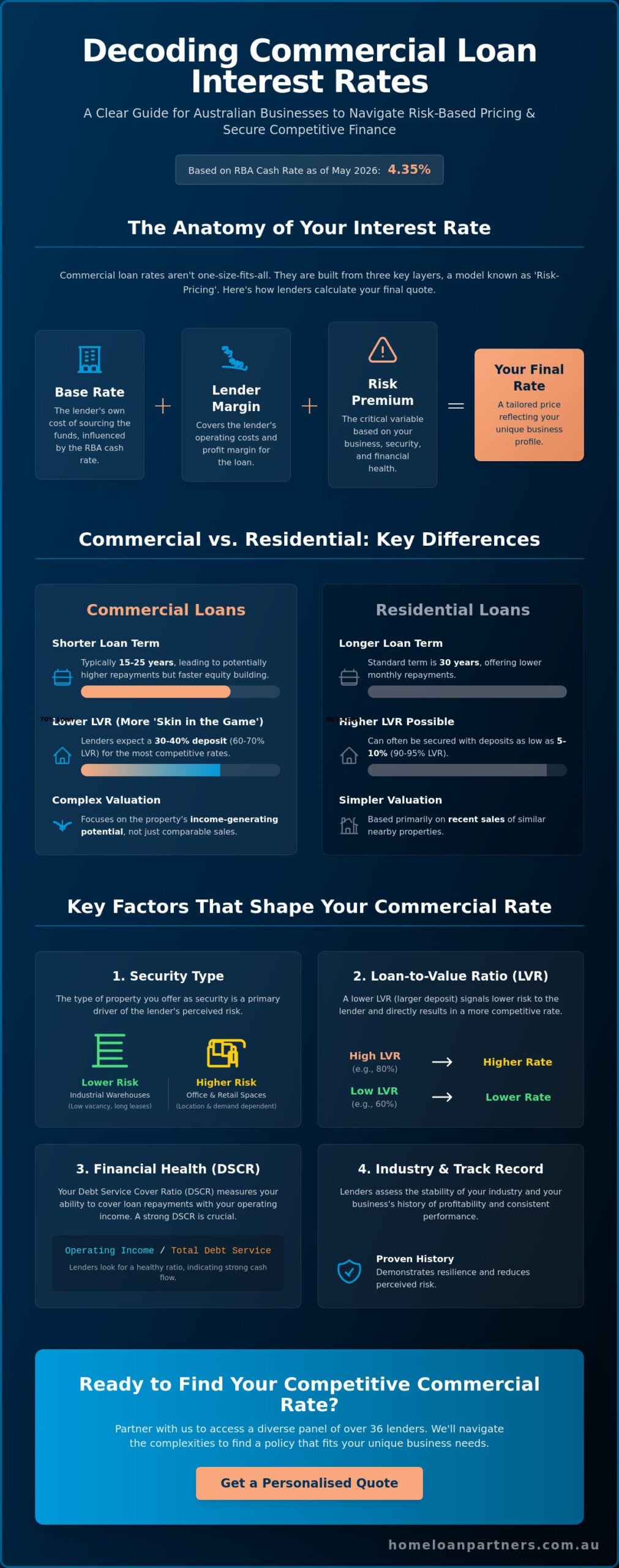

Commercial interest rates represent the cost your business pays to access capital, typically secured by commercial property or business assets. Unlike the relatively uniform world of home loans, interest rates for commercial loans operate on a principle called risk-pricing. This means that two different businesses could apply for the exact same loan amount but receive significantly different rate offers. Lenders look at your specific situation to determine the price of your debt, moving away from the “one size fits all” approach seen in residential lending.

To understand your quote, it helps to look at the three layers that make up the final number. First, there’s the base rate, which is the lender’s own cost of sourcing the funds. On top of this, they add a lender margin to cover their operating costs and profit. Finally, they apply a risk premium based on your business’s financial health and the security you offer. Many factors that influence interest rates come into play here, including your industry’s stability and your historical cash flow. Because commercial markets are less liquid and carry higher default risks than residential markets, these rates are generally higher than what you would see for a standard home mortgage. We act as your guide through this complexity, ensuring you understand why each component exists.

Commercial vs. Residential: Key Differences

When you transition from a home loan to a commercial product, the rules of the game shift. Most residential mortgages offer 30-year terms, but commercial loan terms are usually shorter, often ranging between 15 and 25 years. This shorter timeframe means your monthly repayments might be higher even if the loan amount is the same. Lenders also require more “skin in the game” through lower Loan-to-Value Ratios (LVR). While you might get a home loan with a small deposit, commercial lenders typically expect 30% to 40% equity to offer their best interest rates for commercial loans. Additionally, commercial valuations are far more complex. They focus on the income-generating potential of the property rather than just recent sales nearby, which directly impacts the risk profile the lender assigns to you.

The Role of the Cash Rate in 2026

The Reserve Bank of Australia (RBA) plays a pivotal role in the commercial landscape. With the cash rate sitting at 4.35% as of May 2026, banks use this as a benchmark for their own indicator rates. It’s important to distinguish between these public indicator rates and the actual rate you receive. The indicator rate is the starting point, but your final offer is tailored through the risk premium mentioned earlier. Market volatility throughout 2026 has made long-term fixed commercial rates more sensitive to global economic shifts than in previous years. This environment requires a steady hand and a clear understanding of how these macro factors filter down to your specific business goals.

Factors Influencing Your Commercial Loan Interest Rate

Your final quote isn’t just a number pulled from a hat. It’s a calculated response to the level of risk a lender perceives in your application. While the RBA provides official lending rate statistics that highlight broad market movements, your personal rate is shaped by several distinct levers. Understanding these factors allows you to present your business in the best possible light and potentially lower your borrowing costs.

Security type is a primary driver of risk-based pricing. Industrial warehouses are currently viewed as highly stable due to consistently low vacancy rates and long lease terms. In contrast, office spaces or retail shops might attract a higher risk premium depending on their location and current market demand. Lenders also look closely at your Loan-to-Value Ratio (LVR). A lower LVR is one of the most effective ways to drive down your interest rates for commercial loans. If you can provide a 30% or 40% deposit, you’re signaling to the lender that you have significant “skin in the game,” which reduces their potential loss and earns you a more competitive offer.

Beyond the asset itself, your business’s financial health is under the microscope. Lenders prioritise the Debt Service Cover Ratio (DSCR), which measures your ability to cover debt obligations with your current operating income. A strong DSCR, paired with a proven track record in your industry, builds confidence. If you’re wondering how your business’s credit score or asset type might influence your quote, a quick chat with The Home Loan Partners can provide the clarity you need.

Asset Quality and Security

Specialised assets like childcare centres, petrol stations, or car washes often carry higher rates because they are harder to sell quickly if a borrower defaults. Because of this limited secondary market, lenders apply a premium to offset the risk. One effective strategy to lower your rate is using residential property as cross-collateral. Residential real estate is a highly liquid asset in Australia, and using it as security can often unlock much more favourable interest rates for commercial loans than using a specialised commercial asset alone. The location of your asset also matters; a property in a major capital city usually attracts better terms than one in a remote regional area.

Financial Health and Servicing

The documentation you provide significantly impacts your pricing. Full Doc loans, which require comprehensive tax returns and financial statements, offer the lowest rates. Low Doc options are available for business owners with less traditional paperwork, but these come with a rate premium to account for the reduced transparency. In 2026 lending standards, the Interest Cover Ratio (ICR) has become a critical benchmark. This ensures your earnings can comfortably handle interest payments even if market conditions shift. Your personal credit score and the trading history of your business are also weighted heavily, as they demonstrate your reliability as a long-term partner.

Fixed vs. Variable vs. Split Commercial Rates

Choosing the right structure is just as important as the rate itself. It’s about aligning your finance with your business’s unique rhythm. When you’re comparing interest rates for commercial loans, you’ll find that the decision between fixed and variable options isn’t just a matter of price. It’s a strategic choice that affects your cash flow, your ability to make extra repayments, and your protection against future market shifts. We act as your expert collaborator to help you weigh these options with precision.

Agility is the hallmark of variable rates. They allow you to make extra repayments or clear the debt entirely without the sting of exit penalties. This structure is particularly beneficial if you plan to sell the asset or refinance in the short term. Unlike most fixed products, variable options often include redraw facilities, giving you a safety net to access surplus funds if your business needs a sudden injection of liquidity. Because these rates react instantly to RBA cash rate changes, you’ll feel the benefit of any rate cuts immediately.

When to Choose a Variable Commercial Rate

A variable structure suits businesses that prioritise liquidity and freedom over long-term predictability. If your strategy involves a quick turnaround or you expect your cash flow to fluctuate, the ability to pay down debt faster is invaluable. In the current 2026 environment, variable rates remain a popular choice for those who want to avoid being locked into a specific pricing tier while maintaining the option to refinance if a better opportunity arises.

The Strategy Behind Fixed Rates in 2026

Fixed rates act as a protective shield for your business projects, typically available for terms between one and five years. By locking in your rate, you remove the guesswork from your monthly overheads, which is essential for accurate long-term budgeting. In 2026, lenders price these rates based on the “yield curve,” which reflects market expectations for future economic shifts. Fixed rates are often higher than variable rates at the start of the term due to the “certainty premium” you pay for that peace of mind. However, if you’re managing a project with tight margins, this premium is often a small price to pay for financial security.

For many of our clients, a split loan offers the most balanced path forward. This hybrid approach allows you to hedge your bets and manage risk effectively. Consider these key points when deciding:

- Split Loans: You can nominate a portion of your debt to be fixed while leaving the remainder variable. This provides a blend of protection and flexibility.

- Break Costs: Be cautious. Exiting a fixed-rate commercial loan early can trigger substantial break costs. These fees are often much higher than those found in residential lending.

We’re here to ensure your fixed term aligns perfectly with your business timeline. By looking at the long-term journey, we help you avoid the traps of early exit fees and find the structure that supports your major milestones. Our goal is to make the process steady and predictable, giving you the confidence to grow.

How to Secure the Most Competitive Commercial Rate

Securing a favourable quote isn’t about luck. It’s the result of a deliberate, well-prepared strategy. Lenders are effectively looking for reasons to say “no,” so your job is to give them every reason to say “yes” at a lower price point. By taking a proactive approach to your application, you can directly influence the interest rates for commercial loans offered to you. We’ve distilled this process into five actionable steps to help you take control of your financial future.

- Clean up your financials: Start by auditing your balance sheet. Clearing small director loans or settling minor tax liabilities makes your business look lean and professional.

- Diversify your security: If you have additional equity in other properties, use it. Lowering the LVR across a broader security pool is one of the fastest ways to trigger a rate reduction.

- Prepare a robust business plan: For owner-occupiers, a clear vision for growth is essential. If you’re an investor, a detailed lease schedule showing tenant stability is your best asset.

- Compare multiple tiers: Don’t limit yourself to your current bank. Different lenders have different appetites for specific industries at different times.

- Engage a broker: A commercial specialist knows which lenders are currently “on sale” and can negotiate on your behalf to find a better deal than you’d get going direct.

If you’re ready to see how these steps apply to your specific situation, you can book a strategy session with our team to explore your options.

The Importance of the Loan Proposal

Your application lives or dies by the “credit memorandum.” This is a professional document that tells the story of your business or investment. A high-quality proposal doesn’t just list numbers; it highlights the strengths of your tenants or your dominant market position. It also addresses potential “weak spots” head-on. If your turnover dipped last year due to a specific project, we help you explain that context clearly so the lender doesn’t just see a red flag. This transparency builds the trust necessary to secure a lower risk premium.

Lender Tiers: Where to Look

The Australian market is divided into three distinct tiers, each serving a different purpose. Tier 1 lenders, the Big 4 banks, offer the sharpest interest rates for commercial loans but maintain the strictest entry criteria. They want “perfect” files with significant history. Tier 2 lenders, including regional and mid-tier banks, are often more flexible with industry types and can offer competitive pricing for medical or agricultural sectors. Finally, Tier 3 lenders, such as private and non-bank firms, provide “outside the box” thinking. While their rates are higher, they offer much faster approvals and are ideal for complex scenarios that don’t fit traditional bank policies.

Navigating Commercial Finance with The Home Loan Partners

You’ve seen how complex interest rates for commercial loans can be. It’s not just about a single number; it’s about a risk-priced outcome tailored to your business’s unique profile. At The Home Loan Partners, we believe you shouldn’t have to navigate this complexity alone. We act as your expert collaborator, translating dense financial jargon into clear, actionable advice that puts you back in control. Our goal is to alleviate the stress of borrowing by projecting a sense of calm, steady expertise throughout your entire journey.

Unlike a single bank that is limited by its own internal policies, we provide access to a diverse panel of over 36 lenders. This breadth ensures your aspirations aren’t sidelined just because one institution doesn’t have an appetite for your specific industry or security type. We manage the heavy lifting of the entire process, from the initial comparison of terms to the final settlement. This proactive approach reduces the friction of commercial borrowing and allows you to focus on what you do best: running your business. We’re here for the long term, ready to help you restructure as your business grows or as the market evolves.

Why a Broker Beats a Bank for Commercial Loans

Banks often change their lending appetite based on their current portfolio balance. A bank that offered great terms last year might be restrictive today. We stay ahead of these shifts, knowing exactly which lenders are currently active and hungry for business in your sector. Beyond just finding a lender, we negotiate on your behalf to reduce lender-paid margins and application fees. Our role also grants you access to non-bank and private lenders. These institutions often think “outside the box” but rarely deal with businesses directly, making a broker your essential gateway to flexible finance that a local branch manager simply cannot offer.

Start Your Commercial Journey Today

Our process is steady, logical, and designed to move you from inquiry to settlement without the usual friction. We don’t just look at the immediate transaction; we focus on a long-term partnership that continues well after the papers are signed. As your business scales or the 2026 market shifts, we’ll be by your side to ensure your debt structure remains efficient. It’s also a perfect time to review your existing commercial debt. Refinancing in the current environment could potentially save your business thousands in interest over the life of the loan.

Take the first step toward a more secure financial future and let us handle the complexities for you. You can Book a consultation with The Home Loan Partners to review your commercial lending options today. We’re ready to help you achieve your next major milestone with precision and care.

Empower Your Business for the Long Term

Navigating the commercial lending landscape requires more than just a quick comparison. It’s about understanding that interest rates for commercial loans are a reflection of your business’s unique story and risk profile. By refining your financials and choosing the right security structure, you position your enterprise for sustainable success. Whether you choose the flexibility of a variable rate or the certainty of a fixed term, your strategy should always align with your major business milestones.

We’ve explored how risk-based pricing works and why a diverse lender panel is your greatest asset in a shifting economy. You don’t have to carry the weight of these complex decisions alone. Our team provides national service with a client-centric approach, offering expert guidance for even the most complex commercial structures. We’re here to act as your steady hand and expert collaborator throughout the duration of your financial journey.

To take the next step toward your goals, Speak with a Commercial Lending Expert at The Home Loan Partners today. With access to over 36 Australian lenders, we’ll manage the heavy lifting while you focus on growth. We look forward to supporting your journey and helping you achieve the milestones that define your success.

Frequently Asked Questions

What is the current average interest rate for a commercial loan in Australia?

Commercial interest rates currently range from approximately 6.37% to 10.74% for variable options, depending on your security type and lender tier. These figures are influenced by the RBA cash rate, which sits at 4.35% as of May 2026. Because every commercial facility is risk-priced, your specific quote will depend on your business’s financial health and the nature of the asset provided as security.

How much deposit do I need for a commercial property loan?

Most traditional lenders require a deposit of 30% to 40% of the property’s value, which equates to a Loan-to-Value Ratio (LVR) of 60% to 70%. If you can offer residential property as additional security, you may be able to access a higher LVR. This strategy reduces the upfront cash contribution required and can often help you secure a more favourable pricing tier.

Can I get a commercial loan with a low doc application?

Yes, you can access finance through a low doc application if you don’t have traditional tax returns or financial statements ready. These loans often rely on accountant letters or bank statement equity to prove your ability to service the debt. While they offer vital flexibility for self-employed business owners, interest rates for commercial loans on a low doc basis are typically higher to account for the reduced documentation.

Are commercial loan interest rates tax-deductible?

Interest payments are generally tax-deductible if you use the loan funds for income-producing business purposes or to purchase an investment property. This can significantly reduce the effective cost of your borrowing over the long term. We always recommend speaking with your tax professional to confirm how these deductions apply to your specific company structure and current financial goals.

What fees should I expect when taking out a commercial loan?

You should prepare for several upfront costs, including valuation fees of around $1,500 and legal fees that typically range from $2,000 to $5,000. Many lenders also charge an origination fee, which is often 1% of the total loan amount. Ongoing costs may include monthly service fees or annual review charges, so it’s essential to factor these into your total cost of capital.

How long does it take to get a commercial loan approved?

Approval timeframes vary by lender, with major banks often taking four to six weeks to complete their thorough due diligence. If your business needs a faster turnaround, some non-bank and private lenders can provide approvals within 48 to 72 hours for well-prepared applications. We manage the communication with these lenders to ensure your file moves through the system as efficiently as possible.

Is it possible to refinance a commercial loan to a lower rate?

Refinancing is an excellent way to improve your cash flow, especially if your business’s financial position has strengthened since you first took out the loan. As you build more equity or increase your turnover, you become more attractive to a wider range of lenders. We regularly help clients compare their existing debt against the latest interest rates for commercial loans to ensure their finance remains competitive.

What happens if I want to pay off my commercial loan early?

Your ability to settle the debt early without penalty depends on whether your loan is on a variable or fixed rate. Variable loans generally offer the freedom to make extra repayments or clear the balance at any time. Fixed-rate loans, however, often incur significant break costs if you exit before the term expires. We can help you calculate these potential fees to determine if an early payout is financially sound.