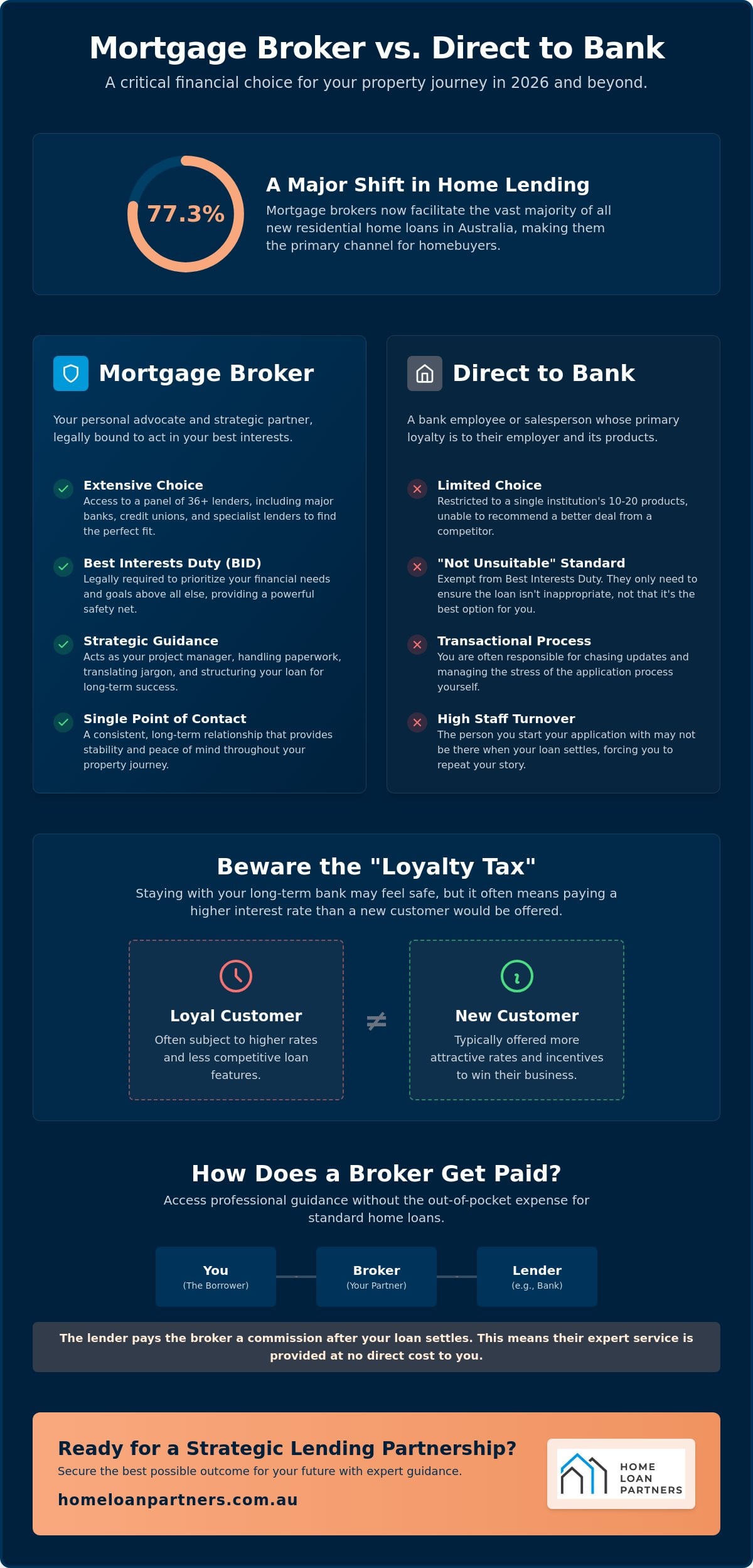

With mortgage brokers now accounting for 77.3% of all new residential lending, the traditional path of walking into a local branch is becoming the exception rather than the rule. As we move through 2026, the choice between a mortgage broker vs going direct to bank has shifted from a matter of convenience to a critical financial strategy. Many homeowners feel a sense of loyalty to their long-term bank, yet they often find themselves hit with a “loyalty tax” in the form of higher rates than those offered to new customers. You deserve a lending structure that respects your financial goals and your time, rather than one that simply fills a bank’s quarterly quota.

It is completely normal to feel overwhelmed by the paperwork and the technical jargon that comes with securing a loan. We understand that you want a lower interest rate and a flexible structure without the stress of managing every detail yourself. This article will show you the critical differences between bank lenders and mortgage brokers so you can secure the best possible outcome for your future. We’ll explore the impact of the 2026 Homebuyers Privacy Protection Act, compare current market rates such as the 6.56% average for 30-year fixed terms, and help you decide which path offers the steady guidance you need.

Key Takeaways

- Learn the legal distinction between a bank salesperson and a broker who is bound by the Best Interests Duty to prioritize your specific financial needs.

- Uncover the reality of the “loyalty tax” and why staying with your current bank may result in higher interest rates compared to the broader market.

- Compare the outcomes of a mortgage broker vs going direct to bank to see how access to a panel of 36+ lenders provides greater long-term flexibility.

- Gain clarity on the commission-based payment model that allows you to access professional guidance for standard residential loans without paying out-of-pocket fees.

- Discover how a strategic lending partnership can transform a complex 30-year commitment into a manageable, stress-free path toward your property goals.

Mortgage Broker vs Bank: Understanding the Core Differences

Choosing between a mortgage broker vs going direct to bank is often the first major decision you’ll make in your property journey. It is a choice between a single product shelf and a global marketplace. A bank representative is, at their core, a salesperson for that specific institution. They are experts in their own suite, but their loyalty lies with their employer. In contrast, a broker works for you. They act as a professional bridge between you and a vast range of lending options, ensuring the structure of your debt matches your long-term life goals.

The scale of choice is the most visible difference. A typical bank might offer 10 to 20 internal products. A mortgage broker, however, compares 30 to 40 different lenders, including major banks, credit unions, and specialized non-bank lenders. This variety is not just about finding a lower rate; it’s about finding a lender whose specific “appetite” for risk aligns with your financial profile. Whether you are a first-home buyer or looking into investment property loans, the breadth of choice ensures you aren’t forced into a product that doesn’t quite fit.

The Role of the Bank Lender

When you walk into a local branch, you are speaking with an employee who is limited by the policies of their specific firm. They cannot advise you to visit a competitor, even if that competitor offers a product that would save you thousands of dollars over the life of the loan. This relationship is often transactional and subject to the internal shifts of the banking world. Staff turnover is common in large institutions. You might start your application with one person only to find they’ve moved roles before your loan settles, leaving you to repeat your story to a stranger.

The Role of the Mortgage Broker

What is a mortgage broker? Think of them as your personal project manager for the entire lending process. They take the time to understand your aspirations before they even look at a rate sheet. A broker manages the heavy lifting, from the initial analysis of your borrowing capacity to the final settlement. They provide a single, steady point of contact who stays with you for the long haul. Because they understand the nuances of various credit policies, they can navigate hurdles that might cause a direct bank application to stall. This collaborative approach turns a complex financial hurdle into a clear, guided path forward.

The emotional difference between these two paths is significant. Going direct to a bank can feel cold and administrative. You are often the one chasing updates and managing the stress of the paperwork. A broker acts as an expert collaborator who prioritizes your peace of mind. They translate industry jargon into everyday language, making sure you feel empowered and secure in your decisions.

The Broker Advantage: Choice, Strategy, and Best Interests Duty

While having access to a panel of 36+ lenders is a clear benefit, the true value of a broker lies in the legal and strategic protection they provide. When comparing a mortgage broker vs going direct to bank, many borrowers don’t realize that the level of accountability is fundamentally different between the two paths. A broker isn’t just a middleman; they’re a partner with a legal mandate to put your needs first.

Why Best Interests Duty (BID) Is Your Safety Net

It’s a common misconception that all mortgage professionals work under the same set of rules. In reality, bank staff are exempt from the Best Interests Duty. Their primary obligation is to their employer, and they only need to ensure a loan is “not unsuitable” for you. They aren’t required to tell you if a competitor down the street has a better rate or a more flexible structure. Brokers, however, are bound by a statutory obligation to prioritize your interests above their own. We must research, compare, and document exactly why a specific loan is the superior choice for your unique situation. This transparency acts as a powerful safety net, ensuring you aren’t just another number in a sales pipeline.

Beyond the Interest Rate: Loan Structuring

A great loan isn’t just about the lowest number on a page. It’s about how that loan behaves over the next five to ten years. Brokers look at your life through a wide-angle lens. Are you planning a major renovation or starting a family? Do you need bridging loans to buy your next home before you sell your current one? We focus on these strategic details to ensure your debt doesn’t become a hurdle. By matching features like multiple offset accounts or redraw facilities to your specific budgeting style, we help you maintain maximum flexibility.

Brokers also carry significant negotiation power that an individual borrower rarely possesses. Because we manage high volumes of applications across dozens of institutions, we often have access to “broker-only” rates or fee waivers that aren’t advertised to the general public. This allows us to secure a structure that is both cost-effective and highly functional for your long-term journey. If you’re ready to see how a tailored strategy can protect your financial future, our team can help you explore your loan options with total clarity.

Going Direct to a Bank: Pros, Cons, and the Loyalty Tax

Many people default to their primary bank because it feels like the path of least resistance. You already have the app on your phone, your salary is already deposited there, and the brand is familiar. However, deciding between a mortgage broker vs going direct to bank requires looking beneath the surface of that convenience. While a bank offers the comfort of an existing relationship, it often comes at a hidden cost that impacts your financial flexibility for years to come.

The Myth of Bank Loyalty

Banks are commercial entities that prioritize their profit margins. They rely heavily on “set and forget” customers who don’t regularly question their interest rates. This leads to the “loyalty tax,” which is the financial penalty you pay for not comparing the market regularly. It’s common to see a bank offer a lower rate to a brand-new customer while keeping their existing, loyal clients on a rate that might be 0.20% higher. Over a 30-year term, that small gap translates into thousands of dollars in extra interest. Even if you call your bank and they offer a “loyalty discount,” that figure is often still less competitive than what is available through the broader market.

When Going Direct Might Seem Easier

There are specific scenarios where going direct feels like a logical choice. If you have a 20-year history with an institution, a low Loan-to-Value Ratio (LVR), and a very simple financial profile, the process might be relatively quick. Some borrowers also find comfort in the brand security of a “big four” bank. They might value the ability to bundle their home loan with credit cards or insurance products. While these bundles can simplify your life, they require a careful cost-benefit analysis. The convenience of a single login rarely outweighs the savings of a more tailored loan structure found elsewhere.

The biggest risk of going direct is the “single-point-of-failure.” If your chosen bank declines your application due to a minor policy mismatch, your journey stops there. You’re left to start from scratch with another lender, potentially wasting weeks of time. When comparing a mortgage broker vs going direct to bank, remember that a broker has a plan B, C, and D ready to go. They understand which lenders have an appetite for your specific profile, whereas a bank only knows its own narrow criteria. In 2026, “direct-only” specials are increasingly rare as lenders shift their focus toward the broker channel, which now handles more than three-quarters of all new residential loans.

Cost Comparison: How Mortgage Brokers Get Paid

A common question many borrowers ask is how a broker can provide such a comprehensive service without charging the client an upfront fee. When you compare a mortgage broker vs going direct to bank, the financial mechanics of the relationship are quite different. For most standard residential loans, the broker’s professional expertise is available to you at no direct cost. This isn’t because the service is a gift, but because the lender pays the broker for the work they do in preparing and managing your application.

Upfront vs Trail Commissions

Brokers are compensated through two main types of commissions. The upfront commission is a one-off payment from the lender after your loan settles. This covers the hundreds of hours spent on research, lender liaison, and the complex paperwork required to secure an approval. The trail commission is a smaller, ongoing payment that continues for as long as you stay with that lender. This second payment is particularly beneficial for you. It incentivizes your broker to check in regularly and ensure you still have a competitive rate. If the market shifts, your broker is motivated to call you and suggest refinancing to a better product. These commissions come from the bank’s profit margin; they aren’t added on top of your interest rate.

The Transparency Report

Transparency is the foundation of a trusting partnership. Every broker must provide you with a Credit Proposal that clearly discloses the commissions they expect to receive from different lenders. This document ensures there are no hidden agendas. Because of the Best Interests Duty we discussed earlier, brokers cannot simply choose the lender that pays the highest commission. The law requires us to document why the recommended loan is the right fit for your specific goals. This legal framework prevents commission-driven advice and protects your financial future.

Understanding these costs makes the choice between a mortgage broker vs going direct to bank much simpler. When you choose a broker, you’re receiving a high-value professional consultation that saves you time and stress. If you’re ready to secure a loan structure that prioritizes your long-term wealth, our team is here to guide you through the process with total clarity. We manage the heavy lifting so you can focus on the excitement of your new home or investment.

Making the Choice: Why a Strategic Partnership Wins

Your home loan is likely the largest financial commitment you’ll ever make. It’s a commitment that often spans 25 to 30 years, yet many people treat the application as a one-off administrative hurdle. When weighing up a mortgage broker vs going direct to bank, you’re choosing more than just a rate; you’re choosing the level of support you’ll receive for the next few decades. A bank’s involvement usually ends once the loan is settled. In contrast, a strategic partnership with a broker ensures your debt remains aligned with your career, your family, and your long-term wealth goals.

One of the most significant advantages of this collaborative approach is the proactive annual health check. It’s a simple reality that a bank won’t call you to suggest that a competitor’s new product could save you money. A dedicated broker does exactly that. We monitor the market to ensure your structure remains optimized as your equity grows. This ongoing care is especially vital for complex financial paths. If you’re navigating SMSF loans, construction loans, or renovation loans, the margin for error is slim. These specialized products require technical precision and a deep understanding of varying credit policies that a general bank lender often lacks.

The Home Loan Partners Difference

We believe in managing the heavy lifting so you can focus on the excitement of your move. Our team provides access to over 36 lenders, but our real value is the steady, reassuring hand we provide during the stress of the Australian property market. Whether you need bridging loans to secure a new home before selling your current one, or investment property loans to build your portfolio, we act as your expert collaborator. We translate complex industry jargon into a clear, predictable path forward, ensuring you feel protected at every milestone of your journey.

Next Steps for Your Property Journey

Moving from confusion to clarity is a straightforward process when you have the right guide. To begin, we recommend collating your basic documents, such as your recent payslips and tax returns. This preparation allows us to provide a precise assessment of your borrowing power during our initial strategy session. From there, we can map out a loan structure that prioritizes your future security. You don’t have to navigate the complexities of the lending world alone.

Choosing between a mortgage broker vs going direct to bank is ultimately about deciding what kind of relationship you want for your financial future. If you value transparency, expert strategy, and a partnership that lasts well beyond settlement, we’re ready to help. Start your stress-free home loan journey with The Home Loan Partners today and secure a financial structure designed for your life.

Securing Your Financial Future with Clarity

Deciding between a mortgage broker vs going direct to bank is about more than just your first home; it’s about the decades of milestones that follow. You’ve seen how this choice affects your interest rate, your legal protections under the Best Interests Duty, and the long-term flexibility of your loan structure. While a bank offers a familiar app, a broker offers a lifelong strategy tailored to your specific goals.

We are here to manage the heavy lifting so you can focus on building your future. With access to 36+ lenders and specialized expertise in complex bridging and SMSF loans, we provide the steady guidance you need in a shifting market. Our Best Interests Duty certification ensures that every recommendation we make puts your needs first, today and for the years ahead.

Take the first step toward a stress-free lending experience with a team that values your journey as much as you do. Book a Personalised Loan Strategy Session today. Your property goals are within reach, and we’re ready to help you navigate the path with precision and care.

Frequently Asked Questions

Is it cheaper to go direct to a bank or use a mortgage broker?

It is often more cost-effective to use a broker because they compare the market to help you avoid the “loyalty tax.” While a bank might offer a specific “special” to new customers, a broker has the tools to verify if that deal actually stacks up against the broader market. Since most brokers don’t charge you for standard residential loans, you gain expert negotiation power without an extra bill.

Do mortgage brokers have access to the same rates as banks?

Yes, brokers have access to the same public rates as banks, and they frequently have access to “broker-only” specials or discounted rates not advertised in branches. When comparing a mortgage broker vs going direct to bank, remember that brokers can often negotiate fee waivers or rate sharpeners based on their high volume of business with a particular lender.

Will a mortgage broker charge me a fee for their service?

Most brokers in Australia do not charge a fee for standard residential lending because they are compensated by the lender. If a fee is applicable for highly complex commercial or specialized structures, this is always disclosed upfront in your credit quote. For the vast majority of home buyers and renovators, the professional guidance is provided at no direct cost to the client.

Can a mortgage broker help me if my bank has already said no?

A broker is often the best person to call if a bank has declined your application. Every lender has a different “appetite” for risk and unique credit policies. While one institution might say no due to your employment type or deposit size, another lender on our panel may welcome your profile. We help find the specific lender whose criteria match your financial situation.

How many lenders does a typical mortgage broker have access to?

A typical mortgage broker provides access to a panel of 30 to 40+ lenders. This range includes the “big four” banks, mid-tier institutions, and specialized non-bank lenders that don’t have physical branches. This variety ensures your loan structure is tailored to your specific life goals rather than being limited to one institution’s narrow and rigid product suite.

Does using a mortgage broker take longer than going to a bank?

Using a broker can actually speed up the process because they ensure your application is “bank-ready” before it is even submitted. By managing the paperwork and anticipating lender questions, a broker reduces the back-and-forth that often slows down direct applications. We act as your project manager to keep the timeline on track and alleviate the stress of the application.

What happens to my broker relationship after the loan settles?

Your relationship with a broker is a long-term partnership that continues well after you receive your keys. We perform regular reviews to ensure your rate remains competitive as market conditions change. If your circumstances evolve, such as starting a family or planning a major renovation, we’re here to adjust your lending strategy to match your new milestones.

Is it better to use a broker for refinancing or just for a new purchase?

It is highly beneficial to use a broker for both scenarios. When comparing a mortgage broker vs going direct to bank for refinancing, a broker can quickly scan the market to see if your current lender is still providing value. For new purchases, we provide the essential guidance needed to navigate auctions and contract deadlines with total confidence and precision.