What if the most important part of your mortgage interview isn’t the interest rate, but the depth of the partnership you’re building? It’s natural to feel overwhelmed by complex loan jargon or anxious about missing out on a better deal while the RBA holds the cash rate at 4.35%. You deserve to know exactly how your broker is paid and whether their recommendations truly align with your unique goals. Learning exactly what questions to ask a mortgage broker is the first step in transforming a stressful transaction into a clear, confident path toward homeownership.

We understand that navigating the 3% serviceability buffer and shifting debt-to-income limits feels like a heavy lift to manage on your own. This guide provides you with a precise roadmap to master your interview and secure your financial future. You’ll learn how to identify hidden fees, decode commission structures, and ensure your loan is structured for long-term savings rather than just a short-term win. By the end of this article, you will have the tools to choose a broker who acts as a steady, expert guide for your entire property journey.

Key Takeaways

- Learn how to distinguish a transactional middleman from a dedicated credit advisor who can navigate Australia’s 36+ lenders on your behalf.

- Discover why evaluating a broker’s lender panel and professional qualifications is essential for finding a loan that fits your unique situation.

- Master precisely what questions to ask a mortgage broker to reveal hidden costs and ensure every recommendation protects your financial future.

- Gain the confidence to request a full breakdown of commissions and fees, ensuring your broker’s interests are perfectly aligned with your own.

- Understand how to secure a tailored loan structure that evolves with your life milestones and maximizes your long-term savings.

Understanding the Role: Why Your Questions Matter in 2026

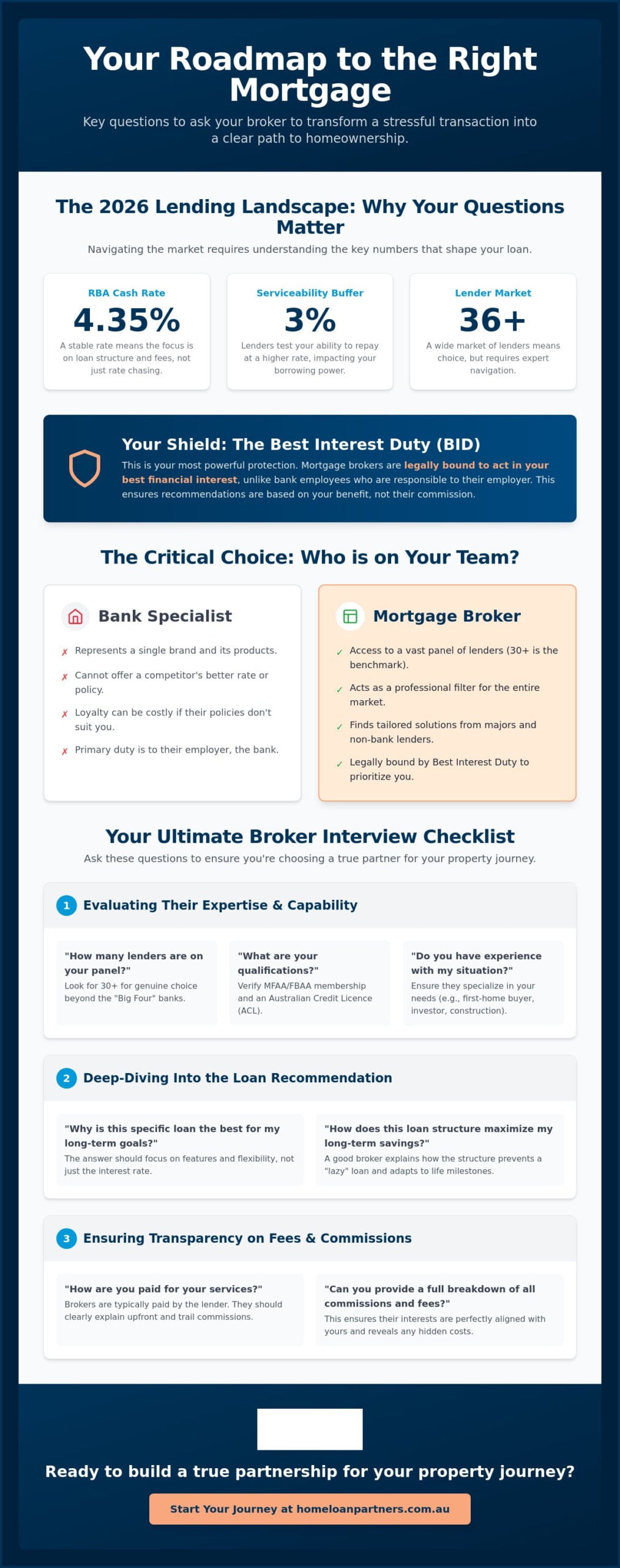

The Australian lending environment has shifted significantly. With the RBA cash rate holding steady at 4.35% as of June 2026, the margin for error in your mortgage strategy has narrowed. A mortgage broker is no longer just a facilitator who fills out paperwork; they are professional credit advisors. Understanding What is a mortgage broker? helps you see them as an intermediary who translates complex industry jargon into a plan that protects your future security.

Navigating over 36 different lenders requires more than just a quick internet search. It demands a steady hand to manage the 3% serviceability buffer and current debt-to-income limits. Knowing what questions to ask a mortgage broker ensures you aren’t just another transaction in a crowded market. It allows you to verify that your broker is looking beyond the headline rate to find a structure that actually saves you money over the life of your loan. This proactive approach prevents you from falling into “lazy” loan structures that fail to account for your long-term aspirations.

What is the Best Interest Duty (BID)?

The Best Interest Duty (BID) is your most powerful protection. Unlike bank employees, who are primarily responsible to their employer, brokers are legally bound to prioritize your needs. This regulation ensures they recommend products based on your financial benefits rather than the commission they might receive. Best Interest Duty is the legal requirement to act in the client’s best financial interest. It acts as a shield against biased advice, ensuring that the path forward is chosen for its precision and alignment with your specific goals.

The Difference Between a Bank Specialist and a Broker

Think of a bank specialist as a representative for a single brand. They can explain their own products perfectly, but they can’t offer you an alternative, even if a competitor has a rate or policy that suits you better. Brokers, however, have access to a vast panel of lenders. Staying loyal to a single bank can be a costly mistake. It may add thousands in interest over time if that bank’s specific credit policies don’t favor your current financial position.

A broker acts as a professional filter for you. They understand which lenders are currently tightening rules on trust lending and which ones are offering the best grants for first-home buyers. Learning what questions to ask a mortgage broker helps you identify if they are truly exploring the whole market or just sticking to a few familiar names. This distinction is what separates a standard loan from a tailored financial strategy.

Essential Questions to Ask When Choosing Your Mortgage Broker

Choosing a partner for your financial journey requires more than a gut feeling. It’s about data, transparency, and a shared commitment to your long-term goals. While the previous section highlighted the broker’s role as a credit advisor, your success depends on your ability to vet their specific expertise. Knowing what questions to ask a mortgage broker during your initial meeting will help you separate a standard service provider from a dedicated collaborator who can navigate the complexities of the 2026 market.

Evaluating the Lender Panel

Your first question should be: “How many lenders do you have on your panel and who are the top three you use?” A panel of 30 or more lenders is the industry benchmark for providing true choice. If a broker primarily relies on the “Big Four” banks, you might miss out on more competitive rates or flexible credit policies offered by non-bank lenders. A high-quality answer includes a diverse mix of major institutions and boutique lenders. This variety is essential because non-bank lenders often provide more tailored solutions for unique situations, such as self-employed income or specific property types.

Experience and Specialisation

Ask about their specific experience: “What are your qualifications and how long have you been a broker?” You should also look for membership in professional bodies like the MFAA or FBAA. It’s vital to check if they hold an Australian Credit Licence (ACL) or are an Authorised Representative. Beyond the paperwork, you need a broker who understands your specific milestone. A first-home buyer has vastly different needs than an investor looking into SMSF lending or someone requiring a construction loan. For more guidance on vetting your advisor, you can review these government-recommended questions to ask your mortgage broker to ensure they meet the highest standards of professional conduct.

Don’t be afraid to dig into complex scenarios. Ask how they handle bridging loans or the increased scrutiny on trust lending seen in 2026. A seasoned expert will explain their internal process with precision, from the initial application to the final settlement. They should be able to describe their communication rhythm so you never feel left in the dark during the high-pressure moments of a property purchase. If you’re looking for a team that prioritises your long-term security over a simple transaction, our experts at Home Loan Partners can guide you through every step of this process.

Finally, ensure you understand the “why” behind their recommendations. When you know what questions to ask a mortgage broker, you can challenge them to explain why a specific product is the best fit for your future, not just the easiest one to get approved today. This level of inquiry builds a foundation of trust and ensures your loan structure is built to last.

Deep-Dive Questions About Your Loan Recommendation

Once you’ve selected a broker, the focus shifts to the specific financial products they present. It’s not enough to simply accept a recommendation; you must understand the mechanics of the deal. Knowing what questions to ask a mortgage broker regarding their specific suggestions ensures you aren’t just getting an “easy” approval, but a structure that serves your long-term wealth. This stage of the process is where your broker’s expertise truly translates into tangible savings.

Ask your broker: “Why is this specific loan product the best fit for my long-term goals?” A quality response should compare at least three different options, weighing the pros and cons of each. Be wary of recommendations that seem based solely on how quickly a lender processes applications. You also need to look at the total cost beyond the headline interest rate. The comparison rate includes both the interest rate and most upfront or ongoing fees. This figure is your true north for comparing different products fairly. For a comprehensive checklist to keep your interview on track, you can refer to the ASIC-backed Questions to ask your mortgage broker.

The “Why” Behind the Recommendation

A professional advisor won’t just hand you a single flyer. They should explain how a lender’s credit policy aligns with your income type or deposit size. If they only suggest one lender, ask if that’s because it’s the best price or simply the path of least resistance for their paperwork. Your financial security depends on a broker who is willing to do the heavy lifting to find a superior deal, even if the application process is more rigorous. This transparency ensures that the recommendation is built on your needs rather than the broker’s convenience.

Features That Save You Money

Interest rates get all the attention, but loan features often dictate how much you actually pay over thirty years. Ask: “Does this loan offer features like offset accounts or redraw facilities?” Understanding the nuances between a Redraw vs Offset Account: Which Is Better For You? is crucial for managing your monthly cash flow. An offset account can save thousands in interest by using your savings to reduce the principal balance, while a redraw facility might be better for those who want a simpler structure. You should also inquire about portability and flexibility. If you plan to renovate or sell in the next few years, you don’t want to be locked into a rigid product with high exit costs.

Finally, inquire about the lender’s current turnaround time. In a competitive property market, a slow lender can mean missing out on your dream home. Using these targeted what questions to ask a mortgage broker ensures your loan remains an asset, not a burden, as your life evolves. By digging into these details, you transform the loan process from a confusing transaction into a clear, strategic partnership.

Transparency: Questions About Fees and Commissions

Financial transparency is the cornerstone of any healthy partnership. When you’re deciding what questions to ask a mortgage broker, focusing on their remuneration is vital for your peace of mind. Many borrowers feel anxious about hidden costs or wonder if a broker is pushing a specific lender just for a higher payout. Addressing these concerns directly in your first meeting sets a professional tone and ensures your interests remain the priority.

Ask your advisor: “Do you charge a fee for your service, or are you paid solely by the lender?” Most Australian brokers, including our team at Home Loan Partners, don’t charge the client a direct fee for standard residential home loans. Instead, we are paid by the lender once your loan settles. This model makes expert credit advice accessible, but it requires you to understand how those payments work to ensure you’re getting the best possible structure for your future.

How Mortgage Brokers Are Paid

Brokers typically receive two types of payments from lenders. The upfront commission usually ranges from 0.5% to 0.7% of the total loan amount. This payment covers the initial work of researching products, managing the application, and seeing the loan through to settlement. The second part is the trail commission. This is an ongoing payment, typically between 0.1% and 0.3% of the remaining loan balance annually.

Trail commission is actually a significant benefit for you. It incentivizes the broker to provide ongoing support throughout the life of your loan. Because they receive a small payment as long as you stay with that lender, they’re motivated to ensure you remain happy with the product. If your needs change or rates become uncompetitive, a broker receiving trail is more likely to proactively suggest refinancing to keep your financial strategy on track. It transforms a one-off transaction into a long-term relationship focused on your milestones.

The Credit Proposal Disclosure

You don’t have to rely on verbal promises alone. Before you sign any loan documents, your broker must provide a Credit Proposal Disclosure. This document outlines exactly what commissions they’ll receive from the recommended lender. It also details any other fees or charges associated with the loan. Transparency at this stage is a non-negotiable trust factor. If a broker is hesitant to provide a breakdown of commissions from different lenders, it’s a clear signal to look elsewhere.

Finally, ask: “How do you manage potential conflicts of interest?” Your broker should explain how the Best Interest Duty (BID) guides every recommendation. They should demonstrate that their choice is based on your savings and goals, not the commission percentage. Using these specific what questions to ask a mortgage broker ensures you build a partnership based on clarity and mutual respect.

Building a Partnership with The Home Loan Partners

Mastering the list of what questions to ask a mortgage broker is a powerful starting point. It gives you the clarity needed to evaluate the expertise of your advisor and ensures you aren’t settling for a generic solution. At The Home Loan Partners, we welcome this level of scrutiny because our approach is built on transparency and a genuine commitment to your long-term financial health. We don’t view a home loan as a single transaction. Instead, we see it as a significant life milestone that requires a steady, expert hand to navigate successfully.

Our national reach allows us to find the best loan structures across Australia, regardless of where you’re looking to buy. Whether you’re a first-home buyer in Sydney or an investor looking for SMSF loans in Brisbane, we provide access to a panel of 36+ lenders. This variety ensures you have a genuine choice, moving beyond the limited options of a single bank. We take care of the heavy lifting, from the initial research and application through to settlement and beyond. This proactive management alleviates the inherent stress of the process, allowing you to focus on the excitement of your new property.

Our Commitment to Long-Term Support

Our involvement doesn’t end when your loan settles. In the fluctuating 2026 interest rate market, staying competitive requires constant vigilance. We review our clients’ rates annually to ensure their loan structure remains aligned with their goals. While we are deeply rooted in our NSW-based expertise, our systems are designed for national success. This ongoing relationship means you’ll always have a reliable guide to help you manage your mortgage as your life evolves. Whether you need to discuss refinancing or are planning a renovation loan, we are here to provide supportive, professional guidance.

Your Next Steps to a Stress-Free Home Loan

Taking the next step toward your property goals should feel encouraging, not overwhelming. When you book your initial consultation with our collaborative team, we focus on understanding your aspirations first. To get the most value from this meeting, it’s helpful to have a few items ready:

- Proof of identity, such as a passport or driver’s licence.

- Recent payslips or proof of income if you are self-employed.

- A clear summary of your current debts and monthly living expenses.

- A brief outline of your specific property goals for the next five to ten years.

Preparing these details allows us to dive deeper into the specific what questions to ask a mortgage broker that matter most to your unique situation. We’ll translate the complex credit policies of our 36+ lenders into practical, everyday language you can trust. This precision ensures that the path we choose together is the one that best secures your financial future.

Ready to start your journey? Contact The Home Loan Partners today.

Take the Lead on Your Financial Future

Securing a home loan in 2026 requires more than just finding a competitive rate; it’s about establishing a relationship built on trust and strategic foresight. By mastering what questions to ask a mortgage broker, you’ve taken the most important step in protecting your financial security. You now understand how the Best Interest Duty acts as your legal shield and why a diverse panel of 36+ lenders is essential for true choice. Whether you’re navigating your first home purchase, an investment property, or a strategic refinance, you have the tools to ensure your broker is a dedicated collaborator.

Our team is ready to manage the heavy lifting for you. We combine national reach with a deeply personalised, client-centric approach to find the loan structure that fits your specific life milestones. We’ll translate the jargon, manage the paperwork, and provide the steady expertise you need to move forward with confidence. We’re here to ensure your path is clear and your future is protected at every turn.

Book a Stress-Free Consultation with The Home Loan Partners

Your journey toward homeownership doesn’t have to be a source of anxiety. With the right information and a dependable partner by your side, you can achieve your property goals with precision and peace of mind. We look forward to helping you start this next chapter with total confidence.

Frequently Asked Questions

Do I have to pay a mortgage broker for their services?

Most Australian brokers don’t charge you a direct fee for standard residential home loans because the lender pays them a commission. This payment structure makes professional credit advice accessible to everyone without increasing your out-of-pocket costs. While some brokers might charge a fee for complex commercial or business loans, we prioritize transparency by disclosing all payment details upfront. It ensures our partnership is based on clarity rather than hidden expenses.

How many lenders should a good mortgage broker have access to?

A professional broker should provide access to a panel of at least 30 to 35 lenders to ensure you have a genuine choice. This panel should include the major banks alongside smaller, niche lenders that offer specialized products. Having a broad selection is vital because it allows your advisor to find a loan structure that matches your specific milestones, such as a construction loan or SMSF lending.

Is it better to go to a bank or a mortgage broker in 2026?

Choosing a broker is often better because they act as a professional filter across the entire market rather than a single bank’s menu. While a bank specialist can only offer their own products, a broker compares dozens of options to find the most competitive rate. With the RBA cash rate currently at 4.35%, having a steady hand to navigate different credit policies can save you thousands over the life of your loan.

What documents should a mortgage broker provide me with?

Your broker must provide a Credit Guide, a Credit Proposal Disclosure, and a Statement of Credit Assistance during the process. These documents outline their licensing details, the commissions they receive from lenders, and the specific reasons why a loan was recommended. Reviewing these papers is a key part of knowing what questions to ask a mortgage broker to ensure they are meeting their legal Best Interest Duty obligations.

Can a mortgage broker help me if I have a small deposit?

Brokers specialize in navigating low-deposit options and government schemes like the First Home Guarantee. They understand which lenders accept a 5% or even a 2% deposit for eligible single parents without requiring Lenders Mortgage Insurance. Your advisor will guide you through the specific thresholds for stamp duty concessions in your state to maximize your savings and help you reach your homeownership goals sooner than you might expect.

What happens if my mortgage broker recommends a loan I don’t like?

You aren’t obligated to accept any recommendation that doesn’t feel right for your future goals. A collaborative broker should present at least three options and explain the pros and cons of each with precision. If a suggestion doesn’t align with your cash flow habits, ask for a different structure, such as switching from a redraw facility to an offset account. Your comfort and long-term security are the most important factors.

How often should I talk to my mortgage broker after the loan settles?

We recommend a formal review of your loan at least once a year to ensure your interest rate remains competitive. Market conditions shift quickly, and a proactive broker will monitor your loan to see if refinancing could save you money. This ongoing partnership ensures your loan evolves with your life milestones. It’s a steady way to manage your debt as interest rates fluctuate in the broader Australian economy.

Does using a mortgage broker affect my credit score?

Using a broker doesn’t hurt your credit score; in fact, it can protect it from unnecessary damage. Instead of you making multiple applications that result in several hard inquiries, a broker performs a preliminary assessment first. They only submit a formal application to a lender once they are confident you meet the specific credit criteria. This strategic approach keeps your credit file clean and maintains your borrowing power for the future.