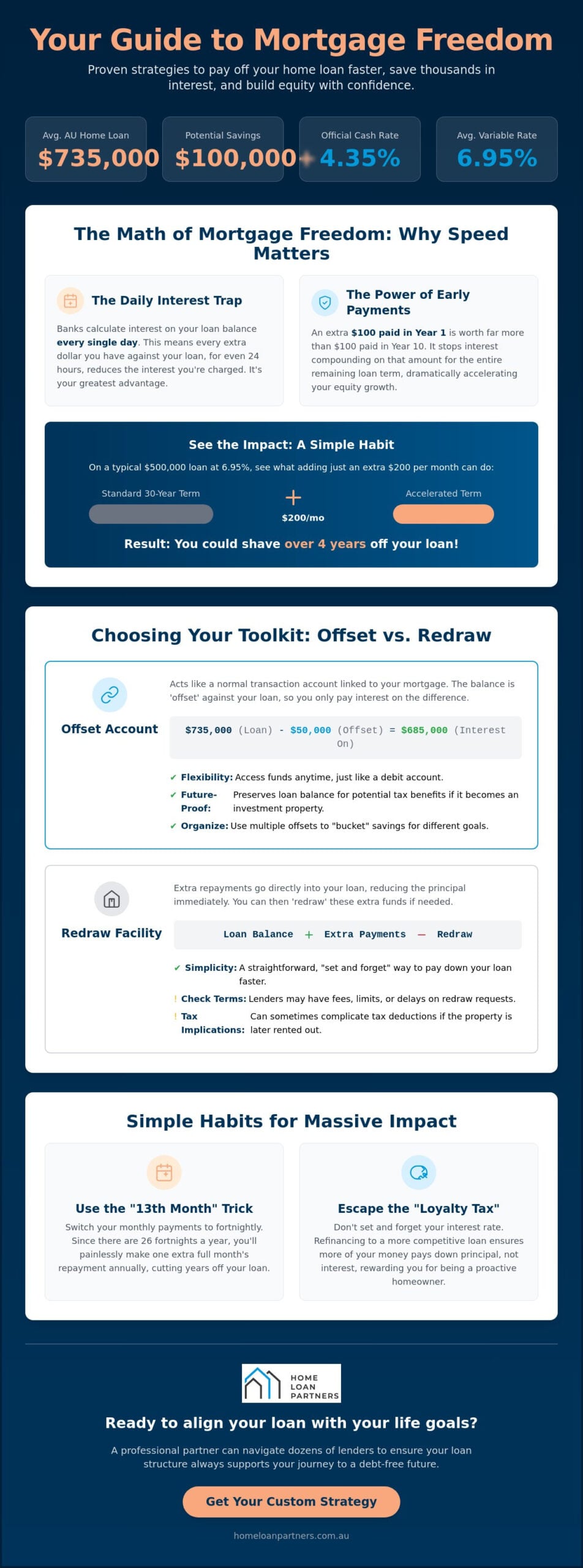

Did you know that with the average Australian home loan now sitting at $735,000, even a small shift in how you structure your debt could save you over $100,000 in interest? It’s easy to feel like the bank is winning the long game, especially with the official cash rate at 4.35% and average variable rates near 6.95%. You likely want to build equity faster, yet the technical confusion between offset accounts and redraw facilities often makes the process feel overwhelming. If you’re looking for clear, actionable strategies to pay off home loan faster, you’re in the right place.

We believe that mortgage freedom is achievable when you align your loan structure with your natural cash flow. Our goal is to help you shave years off your mortgage and save thousands in interest through smart structural changes and simple payment habits. In this guide, we’ll walk through ten proven methods to regain control of your financial future. You’ll discover which loan features truly work for your lifestyle and gain the confidence that you have the best possible deal for the long journey ahead.

Key Takeaways

- Learn why interest is calculated daily and how early principal reductions significantly decrease the total cost of your loan.

- Master the structural differences between offset accounts and redraw facilities to identify the best strategies to pay off home loan faster based on your cash flow.

- Discover how escaping the “Loyalty Tax” through refinancing ensures more of your monthly payment goes toward your equity rather than interest.

- Identify simple habits, like the “13th month” trick, that allow you to pay down your mortgage sooner without feeling the pinch in your daily budget.

- Understand the value of a professional partnership that navigates dozens of lenders to keep your loan aligned with your long-term goals.

The Math of Mortgage Freedom: Why Speed Matters

To truly understand The Math of Mortgage Freedom, you first need to look at how your debt is structured. Most homeowners view their mortgage as a static monthly bill, but it’s actually a dynamic balance that shifts every single day. Because of how interest is calculated, the choices you make in the first few years of your loan carry far more weight than those made toward the end. Embracing specific strategies to pay off home loan faster isn’t just about being good with money; it’s about reclaiming your future from the compounding interest that banks rely on.

The Daily Interest Trap

Australian banks calculate interest based on your outstanding balance at the end of each day, even though they only charge it to your account once a month. This small detail is actually your greatest advantage. Every extra dollar that stays against your principal for even 24 hours reduces the interest you’re charged that evening. While a standard 30-year term is the default, switching to an accelerated 22-year path through consistent extra contributions can save you a staggering amount of money. It’s the difference between being a passive borrower and an active homeowner who understands the value of time.

The Power of Early Principal Reduction

There’s a unique financial logic to mortgages: an extra $100 paid in year one is worth significantly more than $100 paid in year ten. This happens because that early payment stops interest from compounding on that specific $100 for the remaining 29 years of the loan. Seeing your equity grow faster than the bank’s interest charges provides a powerful psychological boost. It transforms the mortgage from a burden into a measurable journey toward a Mortgage Freedom Date that you control.

Let’s look at the numbers. On a hypothetical $500,000 loan with a variable rate of 6.95%, adding just $200 to your monthly repayment could potentially shave over four years off your loan term. This simple habit doesn’t just shorten the time; it keeps more of your hard-earned money in your pocket rather than the bank’s vault. We view this as a long-term journey where we act as your steady hand, ensuring your loan structure supports these goals. Starting today is the most effective of all strategies to pay off home loan faster, as time is the one resource you can’t get back once it’s gone.

Offset vs Redraw: Choosing the Right Structural Tools

Understanding the structure of your loan is just as important as the interest rate itself. Two of the most powerful features available to Australian borrowers are offset accounts and redraw facilities. While they both serve as effective strategies to pay off home loan faster, they function in distinct ways that can impact your financial flexibility and future tax position. Choosing between them isn’t just about saving interest today; it’s about ensuring your loan remains a helpful tool for your long-term journey.

The Offset Account Advantage

An offset account acts like a standard transaction account but is linked directly to your mortgage. The balance in this account is “offset” against your loan principal, meaning you only pay interest on the difference. For example, if you have a $735,000 loan and $50,000 in your offset, the bank only charges interest on $685,000. This setup is perfect for future-proofing your finances. If you eventually decide to turn your home into an investment property, keeping your savings in an offset rather than paying down the loan directly preserves the original loan balance. This can be a significant advantage for tax deductibility later on. You can even set up multiple offset accounts to “bucket” your savings for holidays or home maintenance while still reducing your daily interest charge.

Redraw Facilities: The Simple Saver’s Choice

A redraw facility works slightly differently. Instead of a separate account, any extra payments you make go directly into your loan balance, reducing the principal immediately. A redraw facility then allows you to “pull back” those extra funds if you need them later for an emergency or a large purchase. It’s often the preferred choice for those who want a “set and forget” approach. However, it’s vital to check with your lender about potential fees or minimum withdrawal amounts. Some banks place restrictions on how often or how much you can redraw. Unlike an offset, redrawing money can sometimes be seen as a “new” loan by the ATO, which might complicate tax deductions if the property becomes an investment in the future.

A common concern we hear is whether your money is safe and accessible in these structures. Generally, funds in an offset account are as accessible as any other bank account via a debit card or bank transfer. Redraw funds are also secure, though they usually require a manual transfer to move the money into your spending account. Choosing the right tool depends entirely on your lifestyle and your plans for the property. If you aren’t sure which structure fits your needs, our team can help you compare options across 36+ lenders to ensure your loan is working as hard as you are. We take the heavy lifting out of the process, providing a steady hand to help you reach your goals sooner.

Refinancing: Escaping the “Loyalty Tax” to Save Sooner

Many homeowners believe that staying with the same lender for decades is a sign of financial stability. However, the reality of the Australian banking market is often quite different. Banks frequently offer their most attractive rates to attract new business while allowing existing customers to drift onto higher “back-book” rates. This phenomenon, known as the Loyalty Tax, means you could be paying significantly more than a new customer for the exact same loan. Refinancing acts as a vital reset button for your debt, ensuring that your monthly repayments are actually working to build your equity rather than just padding the bank’s profits.

A lower interest rate doesn’t just reduce your monthly bill. It changes the fundamental balance of your repayment. When your rate drops, the portion of your payment going toward interest decreases, while the amount hitting your principal increases. This shift is one of the most effective strategies to pay off home loan faster because it accelerates the amortization process. You can see this impact for yourself by using a mortgage repayment calculator to compare your current rate against the market leaders. For a deeper look at the specific fees involved in switching, you can also reference our Home Loan Refinancing: A Complete 2026 Guide for cost breakdowns.

The Real Cost of a 0.50% Rate Difference

A difference of just 0.50% might sound minor, but over the life of a standard loan, it can be life-changing. For a homeowner with a $735,000 balance, securing a rate that is half a percent lower could potentially shave two to three years off the total loan term. It’s essential to look past the headline rate and focus on the Comparison Rate. This figure includes most upfront and ongoing fees, giving you a true picture of the loan’s cost. By reducing the interest drag, you empower every dollar you earn to do more heavy lifting for your future security.

When Is the Right Time to Refinance?

Refinancing isn’t always about chasing the lowest number. It requires a calm, logical analysis of your “Break-Even Point.” This is the moment when the interest savings from your new, lower rate outweigh the costs of switching, such as discharge fees or application costs. Generally, the most competitive deals are available to those with an LVR (Loan-to-Value Ratio) of less than 80%. If you’ve built up more than 20% equity in your home, you’re in a prime position to negotiate. Our role as your expert collaborator is to scan the market across 36+ lenders, identifying the hidden gems that offer both a great rate and the structural features you need to reach mortgage freedom sooner. We take the stress out of the process, ensuring you have a clear plan and the best possible deal among all available strategies to pay off home loan faster.

Behavioral Strategies: Small Habits, Massive Impact

While structural features provide the framework for success, your daily habits are the engine that actually drives you toward debt freedom. Implementing small, consistent strategies to pay off home loan faster doesn’t require a radical lifestyle change or extreme frugality. Instead, it’s about making your money work more efficiently in the background while you focus on living your life. Success in the long-term journey of home ownership is often found in the quiet, repetitive actions that compound over time.

The Fortnightly Payment Hack

Most Australian pay cycles occur every two weeks, making the fortnightly payment hack one of the easiest habits to adopt. There are 52 weeks in a year, which means there are 26 fortnights. By taking your monthly repayment amount, halving it, and paying that figure every two weeks, you’ll effectively make 13 full monthly payments each year instead of 12. This “13th month” trick happens automatically without you needing to find extra room in your budget. This single, effortless change can shave approximately four years off a standard 30-year mortgage.

Managing Windfalls and “Found Money”

Your tax refund or an unexpected work bonus can be a powerful mortgage-killing weapon if handled with precision. The psychological trick is to “pay your future self” by moving these windfalls directly into your loan or offset account before the temptation to spend arises. Using an offset account is particularly effective here. It allows you to reduce your interest charge immediately while keeping the cash accessible for genuine emergencies. It’s about finding that balance between security today and freedom tomorrow.

Another quiet but effective strategy is the “Repayment Stay.” If interest rates begin to fall in 2027 as some economists forecast, you should resist the urge to lower your monthly contribution. By keeping your repayments at the higher level, 100% of the interest savings goes directly toward your principal. This accelerates your equity growth at a time when the bank expects you to slow down. You can also try the “Round-Up” strategy, where you add a small, unnoticeable amount like $20 or $50 to every repayment. These tiny additions might feel insignificant, but they eat away at the principal during the early years when interest is at its highest. If you’re ready to see how these habits could transform your specific situation, you can book a strategy session with our team. We’ll help you build a personalized plan that turns these small habits into a massive impact on your financial journey.

Your Partnership for a Debt-Free Future

Reaching the end of your mortgage journey is rarely the result of a single financial “hack.” Instead, the most effective strategies to pay off home loan faster are those that align perfectly with your specific lifestyle, income patterns, and long-term aspirations. While the technical side of interest rates and offset accounts is vital, the human element of the process is what ensures you stay the course. We believe that every homeowner deserves a steady hand to help them navigate the complexities of the Australian lending market. At The Home Loan Partners, we specialize in providing that guidance across more than 36 different lenders.

Our role as your expert collaborator is to manage the heavy lifting. We take the stress out of the process by handling the dense paperwork and technical negotiations required to secure a better deal. A common mistake many borrowers make is setting their loan and forgetting it for a decade. We recommend a comprehensive Home Loan Health Check every 12 to 18 months. This regular review ensures that your loan hasn’t drifted onto a higher rate and that your features, like those we discussed earlier, are still serving your needs as the market evolves.

Beyond the Transaction: A Long-Term Relationship

Our commitment to your financial security doesn’t end when your loan settles. We view our involvement as a long-term journey where we monitor your interest rate for the life of the loan. As your life changes through marriage, growing a family, or perhaps venturing into investment property loans, your debt structure needs to change with you. Having a single point of contact who understands your history and your future goals provides a level of consistency that a call center simply cannot match. The Home Loan Partners act as your advocate, constantly scanning the horizon for new strategies to pay off home loan faster so you don’t have to.

Take the First Step Toward Mortgage Freedom

The path to owning your home outright begins with a few simple, decisive actions. First, take a moment to check your current interest rate against the competitive market benchmarks. Next, assess whether your savings are sitting in a standard account or working for you in a linked offset account. Finally, reach out to a professional who can provide a clear, stress-free plan tailored to your household budget. We understand the emotional weight that significant debt can carry. There is a profound sense of relief that comes from knowing you have the best possible deal and a predictable path forward.

You don’t have to navigate these financial waters alone. Our team is ready to provide the precision and expertise you need to reach your milestones sooner. If you are ready to stop wondering if you could be saving more, Book a stress-free Home Loan Health Check with our team today. We’ll help you turn these proven strategies into a reality for your future.

Reclaim Your Future and Reach Mortgage Freedom Sooner

Achieving a debt-free life is about more than just finding a lower rate; it’s about building a sustainable plan that respects your lifestyle. By mastering structural tools like offset accounts and adopting simple habits like fortnightly repayments, you’ve already taken the first steps toward success. Remember that escaping the “loyalty tax” through regular refinancing is essential to ensure your hard-earned money builds your equity rather than the bank’s profits. These strategies to pay off home loan faster work best when they are consistently monitored and adjusted as your life evolves.

You don’t have to manage this complex process alone. Our NSW-based team provides expert guidance and access to over 36 leading Australian lenders to find the perfect fit for your goals. We provide ongoing loan monitoring so you’re always on the most competitive deal available. Let us find a smarter way to pay off your home loan—Talk to a partner today. Your home is your greatest investment, and with the right support, you can own it outright years ahead of schedule. We look forward to walking this path with you.

Frequently Asked Questions

Is it better to pay off my home loan or invest in the stock market?

Deciding between debt reduction and investing depends on your risk tolerance and the gap between your mortgage rate and potential market returns. Paying down your loan offers a guaranteed, tax-free return by eliminating interest charges, which is highly appealing when variable rates are around 6.95%. While stocks can offer higher long-term growth, they come with volatility. Many homeowners choose a balanced approach to ensure they build equity while also diversifying their wealth.

Can I pay extra principal on a fixed-rate home loan without penalties?

Most fixed-rate loans allow for limited extra repayments, typically capped between $10,000 and $30,000 per year depending on your specific lender. If you exceed this threshold, you may be required to pay break costs or economic cost adjustments. It is vital to review your contract before making large lump-sum payments during a fixed term. If you intend to pay down debt aggressively, we can help you structure a split loan to provide more flexibility.

How much faster can I pay off my mortgage with fortnightly payments?

Making fortnightly payments can shave approximately four years off a standard 30-year mortgage term. This occurs because you complete 26 half-payments, which equates to an entire extra month of repayment every year. It’s one of the most popular strategies to pay off home loan faster because it integrates seamlessly with your existing pay cycle. By reducing the principal balance more frequently, you consistently lower the daily interest calculation that banks use to charge you.

Does an offset account reduce my monthly repayment amount?

An offset account does not usually lower your required monthly repayment, but it does change how that payment is applied. The balance in your offset account reduces the amount of principal the bank can charge interest on, meaning a larger portion of your monthly payment goes toward the principal. This accelerates your equity growth and shortens the life of the loan. It provides the same interest-saving benefit as a direct payment while keeping your funds fully accessible.

Is it worth refinancing if I only save 0.25% on my interest rate?

Refinancing for a 0.25% saving can be highly beneficial if the long-term interest savings outweigh the upfront costs of switching. On a $735,000 loan, even a quarter-percent drop can save you thousands of dollars over a few years. We help you calculate your break-even point by comparing discharge and application fees against your monthly savings. If your current lender has you on an uncompetitive “back-book” rate, a small shift today can create significant momentum.

What happens to my redraw facility if I refinance to a different lender?

Your redraw facility does not transfer between lenders; any extra funds in your current redraw are absorbed into the loan principal when the debt is paid out. If you need access to those funds, you should consider withdrawing them before the refinance or ensuring your new loan includes a similar feature. We manage the heavy lifting during this transition to ensure your equity is correctly calculated and your access to cash remains uninterrupted.

How often should I review my home loan strategy with a broker?

We recommend a comprehensive review of your home loan strategy every 12 to 18 months to ensure your deal remains competitive. Lending markets change rapidly, and a rate that was market-leading last year might now be subject to a loyalty tax. Regular health checks allow us to adjust your structure as your life milestones change. This proactive partnership ensures your loan remains a helpful tool for your long-term journey rather than a stagnant burden.

Are there any tax implications for paying off my home loan early?

For your primary place of residence, there are generally no negative tax implications for paying off your loan early in Australia. However, if you plan to convert your home into an investment property later, reducing the principal now could limit the interest you can deduct in the future. Using an offset account is often one of the most effective strategies to pay off home loan faster while preserving the potential for future tax benefits. We always suggest consulting with an accountant for personalized tax advice.