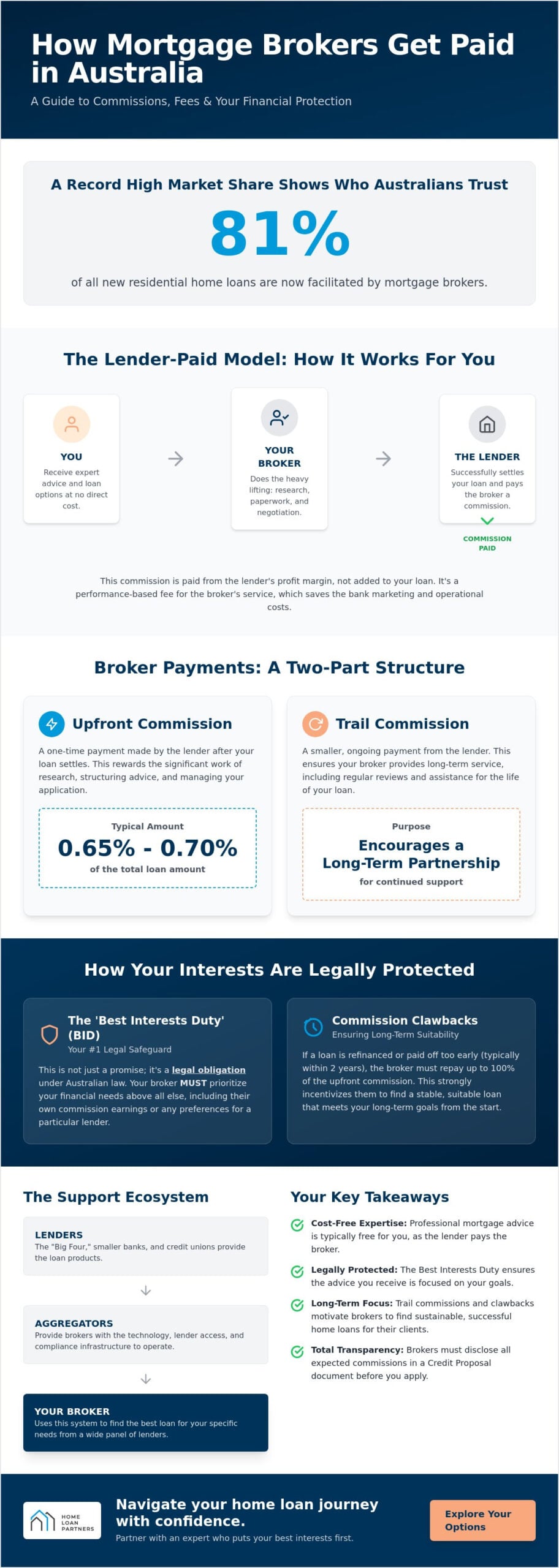

Did you know that 81% of all new residential home loans in Australia are now facilitated by mortgage brokers? This record high market share proves that most Australians prefer having an expert handle the heavy lifting. However, it’s common to feel a sense of hesitation when a professional service is offered without an upfront fee. You might wonder exactly how do mortgage brokers get paid in australia and whether that payment structure influences the advice you receive.

We understand that financial transparency is the foundation of a trusting relationship. You want to be certain that your broker is working for your future, not just the bank’s bottom line. This 2026 guide explains how commissions actually work, why most services are cost-free to you, and how the Best Interests Duty ensures your goals remain the top priority. We’ll explore the mechanics of upfront and trail payments so you can move forward with total confidence. By the end of this article, you’ll understand why the broker-client relationship is built for the long term, protecting your interests well after you’ve moved into your new home.

Key Takeaways

- Understand the lender-paid model that typically makes professional mortgage advice cost-free for residential borrowers.

- Get a clear breakdown of how do mortgage brokers get paid in australia, including the roles of upfront commissions and ongoing trail payments.

- Discover how the Best Interests Duty (BID) provides a legal safeguard that requires your broker to prioritize your needs above all else.

- Learn how industry mechanisms like clawbacks encourage your broker to focus on the long-term success and stability of your home loan.

- Realise the value of a dedicated partner who manages the heavy lifting throughout your entire property journey, from first home to retirement.

How Mortgage Broker Commissions Work in Australia

The standard Australian model for home lending is designed to be accessible. For the vast majority of residential borrowers, including first home buyers and those looking at refinancing, the service provided by a broker comes at no direct cost. Instead, lenders pay brokers for the work involved in introducing and managing the loan application. This means you gain the expertise of a professional who handles the paperwork and negotiations without having to pay an invoice yourself. A deeper look at how mortgage broker commissions work reveals that the Australian system is specifically structured to promote competition across the banking sector.

When considering how do mortgage brokers get paid in australia, it’s vital to understand that the commission is paid out of the bank’s own profit margin. It isn’t added to your interest rate or hidden within your loan setup fees. In fact, because brokers have access to a wide variety of products, they often secure rates that are lower than what a customer might find by walking into a local branch. The broker-lender payment relationship is a professional service fee for credit assistance provided by the broker to ensure the borrower secures a suitable financial product.

The “Free” Service Myth vs. Reality

It’s natural to be skeptical of “free” services, but the reality is grounded in simple business economics. Banks are willing to pay brokers because it reduces their own marketing and operational costs. Rather than paying for expensive television ads or maintaining a massive network of physical branches with thousands of staff, banks pay brokers only when a loan successfully settles. It’s a performance-based model that saves the lender money, which they then pass on as a commission. While rare, a broker might charge a fee for extremely complex scenarios, such as certain commercial loans or very small loan amounts. However, transparency is a legal requirement. Your broker must disclose every cent they expect to receive from a lender within a document called a Credit Proposal before you even apply.

The Role of the Aggregator

Most brokers don’t receive money directly from the bank. Instead, they work with a middleman known as an aggregator. This aggregator provides the technology and infrastructure that allows a broker to access a panel of 36+ lenders, ranging from the “Big Four” to smaller, niche credit unions. The lender pays the commission to the aggregator, who then passes the majority of it to the broker. This ecosystem is strictly regulated. To operate within this space, brokers and aggregators must either hold their own Australian Credit Licence (ACL) or be registered as an authorised representative of one. This ensures that the person helping you with your home loan is qualified, insured, and held to the highest professional standards in the country.

Upfront vs. Trail Commissions: Breaking Down the Numbers

Understanding how do mortgage brokers get paid in australia involves looking at two distinct phases of the loan lifecycle. The payment structure is split into an initial payment for the work performed to get you into the loan and an ongoing payment for the service provided throughout the years that follow. This two tiered system ensures that your broker is rewarded for their immediate expertise while remaining motivated to support your financial health long after the keys have been handed over.

This structure was examined in detail during ASIC’s review of mortgage broker remuneration, which highlighted how these payments support a competitive lending market. By diversifying how they are compensated, brokers can maintain sustainable businesses while offering their services to borrowers without requiring an upfront fee. If you are curious about your current position, exploring your refinancing options with a dedicated expert is a great place to start.

The Upfront Payment: Rewarding the Heavy Lifting

The upfront commission is a one time payment made by the lender to the broker after your loan successfully settles. This payment covers the significant amount of work that happens behind the scenes before you even sign a contract. It compensates the broker for the initial discovery meetings, the hours of product research across dozens of lenders, and the complex task of managing your application through to approval. Typically, this is calculated as a percentage of the total loan amount, usually ranging between 0.65% and 0.70%. It’s important to remember that this is not a fee you pay; it is a payment from the bank’s profit margin to the broker for introducing a high quality client and managing the administrative burden of the loan setup.

Trail Commission: The Incentive for Ongoing Support

Trail commission is a smaller, ongoing monthly payment made to the broker for the life of your loan. Usually set between 0.15% and 0.20% per annum of the remaining loan balance, it serves as a service fee for the continued management of your file. This payment is why your broker remains available to answer questions about your offset account, perform annual “health checks” on your interest rate, or help you request a rate review from your current bank. It transforms the transaction into a partnership. Because the trail is based on the declining balance of your loan, the broker has a vested interest in your continued satisfaction. If you become unhappy and move your loan elsewhere, the trail stops immediately. This keeps the broker focused on ensuring your loan remains competitive and suitable for your needs year after year.

The ‘Best Interests Duty’ (BID): Why Your Interests Come First

Since January 2021, the Australian lending landscape has fundamentally shifted in favour of the consumer. While we have explored the mechanics of how do mortgage brokers get paid in australia, the more vital question is what prevents these payments from influencing a broker’s advice. The answer lies in a powerful legal safeguard known as The ‘Best Interests Duty’ (BID). This legislation ensures that a broker must always prioritise your financial needs above their own commission or the interests of any lender.

This duty is not just a professional guideline; it is a statutory obligation enforced by the Australian Securities and Investments Commission (ASIC). It effectively mitigates “commission bias” by making it illegal for a broker to recommend a loan simply because it pays a higher fee. Instead, brokers are legally required to document exactly why a specific loan is the best fit for your unique goals, comparing various options to prove their recommendation is superior for your circumstances.

Broker vs. Bank: The Regulatory Difference

There is a stark contrast between visiting a local bank branch and partnering with a broker. Bank staff are essentially “product sellers” for their employer. They are only required to ensure the loan they offer is “not unsuitable” for you. They won’t tell you if the bank across the street has a better rate or more flexible features. Brokers, however, act as your personal advisors. Because they work across a panel of dozens of lenders, they must prove that the loan they suggest is the best possible option available from that entire range. This provides immense peace of mind for first home buyers and investors who need to know they aren’t missing out on a better deal elsewhere. Understanding why use a mortgage broker in australia often comes down to this specific legal protection that bank employees simply do not have.

Transparency in Documentation

The BID framework relies heavily on transparency. Every recommendation a broker makes must be backed by a Credit Proposal Disclosure document. This report is your window into the research process. It clearly outlines the interest rates, fees, and features of the recommended loan compared to other alternatives. It also explicitly discloses the exact amount of commission the broker will receive from the lender. By providing this level of detail, the industry ensures that how do mortgage brokers get paid in australia is never a mystery. You receive a clear, evidence-based justification for your home loan, ensuring your path to property ownership is built on a foundation of trust and legal accountability.

Understanding Clawbacks and the Long-Term Relationship

While we’ve discussed the immediate payments involved in home lending, there is a secondary mechanism that ensures your broker remains committed to your loan for the long haul. This is known as a clawback. It sounds a bit clinical, but it’s a vital part of the Australian regulatory framework. A clawback happens when a lender reclaims the upfront commission they paid to a broker if the loan is closed or refinanced within the first two years. This might occur if you sell your property or move your debt to a different bank very quickly after settlement.

While this might seem like a concern only for the professional, it actually provides a significant layer of protection for you as a borrower. It effectively removes the incentive for “churning,” which is the practice of moving clients between loans just to generate new fees. This mechanism is a key reason behind how do mortgage brokers get paid in australia in a way that prioritises quality over quantity. Because the broker carries the financial risk of the loan being closed early, they are deeply motivated to ensure the initial structure is robust and suited to your long-term trajectory. You can rest easy knowing that your broker is looking for a stable home for your mortgage, not just a temporary stopgap. Best of all, Australian regulations prevent brokers from passing these clawback costs on to you, meaning your financial position remains unaffected even if your circumstances change.

The 24-Month Rule

Most lenders operate on a sliding scale for clawbacks over a 24 month period. If a loan is refinanced within the first 12 months, the lender typically reclaims 100% of the commission. Between 13 and 24 months, this often reduces to 50%. This scaling structure is why your broker will often ask detailed questions about your plans for the next few years. They want to ensure that if you plan to sell or renovate, the loan they choose accommodates those milestones without needing a premature restructure. This alignment of interests is what makes the broker channel so dependable for everyday Australians.

Building a Partnership, Not a Transaction

This payment model fosters a relationship built on steady expertise rather than a one-off encounter. When you work with The Home Loan Partners, we view ourselves as your long-term collaborators. We aren’t just filing paperwork; we are helping you navigate the complexities of property ownership across different life stages. Having a professional who understands your financial history makes every subsequent move, from your first home to your third investment, much smoother and less stressful. This focus on longevity ensures that the advice you receive today is designed to support your goals for years to come. If you’re looking for a guide who is committed to your success well beyond the settlement date, reach out to our experts for a personal consultation.

Navigating Your Home Loan Journey with The Home Loan Partners

Choosing the right mortgage is one of the most significant financial decisions you’ll ever make. Throughout this guide, we’ve demystified exactly how do mortgage brokers get paid in australia to show you that professional advice isn’t just accessible; it’s designed to protect your interests. By removing the burden of direct fees for residential lending, the Australian system allows you to partner with a dedicated expert who handles the heavy lifting of research, negotiation, and administration. This ensures that your path to property ownership or debt consolidation is guided by data and legal accountability rather than sales pressure.

The competitive advantage of working with a broker lies in the breadth of choice. While a single bank can only offer you their specific products, our team provides access to a panel of 36+ lenders. This variety is the engine that drives a better outcome for your specific situation. Because of the Best Interests Duty, we’re legally bound to find the most suitable fit from that entire range. We act as your advocate, ensuring the bank’s profit margin works for you through a commission structure that prioritizes your long term satisfaction.

Our Collaborative Approach

We believe that financial processes shouldn’t be a source of stress. Our role is to act as your steady hand, translating complex industry jargon into a practical, clear path forward. Whether you’re looking at refinancing to secure a better rate or structuring complex investment property loans, we focus on the precision of the setup. We don’t just settle a transaction and disappear. We view our involvement as a long term journey, staying by your side to perform regular health checks and rate reviews. This partnership ensures that as your life milestones change, your home loan evolves with you.

Ready to Explore Your Options?

The first step toward a more secure financial future is understanding your current position. We invite you to a no obligation discovery session where we can assess your borrowing power and discuss your aspirations. To make this initial conversation as productive as possible, it’s helpful to have a basic summary of your income, existing debts, and a general idea of your property goals. This allows us to provide immediate, tailored insights into the options available across our lender panel. Our commitment to transparency means you’ll always know where you stand and how we’re working to achieve your goals. Book a stress-free consultation with The Home Loan Partners today.

Take the Next Step Toward Your Property Milestones

Empowering yourself with the facts about the Australian lending landscape is the best way to ensure a stress-free experience. We have explored how the lender-paid model removes the barrier of upfront fees while the Best Interests Duty provides a robust legal safety net for every borrower. This transparent structure ensures that your financial goals remain the focal point of every recommendation. Understanding how do mortgage brokers get paid in australia allows you to use professional expertise as a strategic advantage rather than a source of confusion.

Our team provides national support for first home buyers and investors, offering access to over 36 leading Australian lenders. We manage the heavy lifting and ensure strict Best Interests Duty (BID) compliance so you can focus on the excitement of your new property. Get a personalised mortgage quote and expert advice from The Home Loan Partners to begin your journey with a steady, reliable guide. Your future security is our priority, and we look forward to supporting you through every life milestone ahead.

Frequently Asked Questions

Do I pay a mortgage broker directly for their services?

No, you typically don’t pay a mortgage broker directly for residential loan services. The lender pays the broker a commission for the work performed in managing the application and introducing a high quality borrower. This covers the cost of the broker’s time and expertise, meaning you receive professional guidance without an upfront invoice. While complex commercial or SMSF loans might occasionally involve a fee, your broker will always disclose this clearly before you proceed.

Does using a broker mean I pay a higher interest rate?

No, you do not pay a higher interest rate when using a broker. Lenders offer the same rates to brokers as they do to direct customers, and often, brokers can negotiate even better deals because of their industry relationships. The commission is paid from the bank’s marketing budget and profit margin. This ensures your loan remains competitive while you benefit from the broker’s ability to compare dozens of different products simultaneously.

What happens if I refinance my loan within the first year?

If you refinance within the first year, the lender will likely “claw back” the commission they paid to the broker. This is an industry mechanism designed to ensure loan stability and prevent unnecessary churning of products. It’s important to know that these costs are never passed on to you as the client. Your broker carries this risk, which is why they work hard to ensure the initial loan structure is right for your long term plans.

How much commission does a mortgage broker actually make?

A mortgage broker typically earns an upfront commission between 0.65% and 0.70% of the loan amount at settlement. They also receive an ongoing trail commission, usually between 0.15% and 0.20% per year, based on the remaining balance of the loan. These figures represent how do mortgage brokers get paid in australia to provide both the initial heavy lifting and the long term support you need throughout your property journey.

Are all mortgage brokers in Australia paid the same amount?

No, commission rates can vary slightly between different lenders and aggregators. While most stay within a standard industry range, each bank has its own specific remuneration schedule. However, regardless of the payment amount, the Best Interests Duty (BID) legally requires your broker to recommend the product that is best for you rather than the one that pays the highest commission. This ensures your financial goals always take priority.

Is it better to go to a bank or a mortgage broker?

A mortgage broker is often the preferred choice because they offer access to a wide panel of 36+ lenders, whereas a bank can only sell its own products. Brokers are also legally bound by the Best Interests Duty to prioritise your needs. This provides a significant advantage over walking into a single branch, as you get a broader comparison of the market and a dedicated advocate for your specific property goals.

Do brokers get paid more by certain banks?

Yes, there are minor differences in commission structures between various banks and credit unions. Some lenders might offer slightly different upfront or trail percentages depending on their current business goals. To address any concerns about bias, the law requires total transparency. Your broker must disclose these payments in writing, ensuring you understand how do mortgage brokers get paid in australia while knowing your interests are protected by strict regulations.

Can I see how much my broker is being paid for my loan?

Yes, you have a legal right to see exactly how much your broker is being paid for your loan. This information is clearly documented in the Credit Proposal Disclosure provided before you submit your application. We believe in total transparency, so you can feel confident that the advice you receive is based on your financial success. This disclosure includes both the upfront and trail amounts paid by the lender.