What if the traditional 3-month “genuine savings” rule isn’t the brick wall you’ve been told it is? Many Australians find themselves with a deposit ready to go, perhaps from a family gift or a work bonus, only to be told by their bank that it doesn’t count because it hasn’t “seasoned” in an account for 90 days. It’s incredibly frustrating to feel locked out of the property market when you have the funds but don’t meet a rigid, technical requirement. We understand that your journey is unique, and we’re here to show you exactly how to get a home loan with no genuine savings by leveraging specific lender policies that reward your actual financial behavior.

You deserve an expert partner who looks beyond standard checklists to find a solution that fits your life. In this 2026 guide, you’ll discover how to use your consistent rent history as a powerful substitute for savings and which Australian lenders accept gifted deposits without the usual waiting period. We’ll walk you through a clear, stress-free path to securing your loan so you can stop worrying about banking red tape and start focusing on your new front door.

Key Takeaways

- Understand the distinction between accumulated funds and lump-sum gifts to better position your application with Australian lenders.

- Learn how to get a home loan with no genuine savings by leveraging alternative pathways like consistent rental history or family guarantor support.

- Identify which non-genuine sources, such as inheritances or windfalls, are accepted by specific banks and the documentation required to prove their value.

- Follow a clear, two-step audit process to verify your deposit sources and credit health before approaching a lender.

- Discover how an expert broker acts as your steady guide to navigate complex policy niches and secure a tailored approval.

What Is the Difference Between Genuine and Non-Genuine Savings?

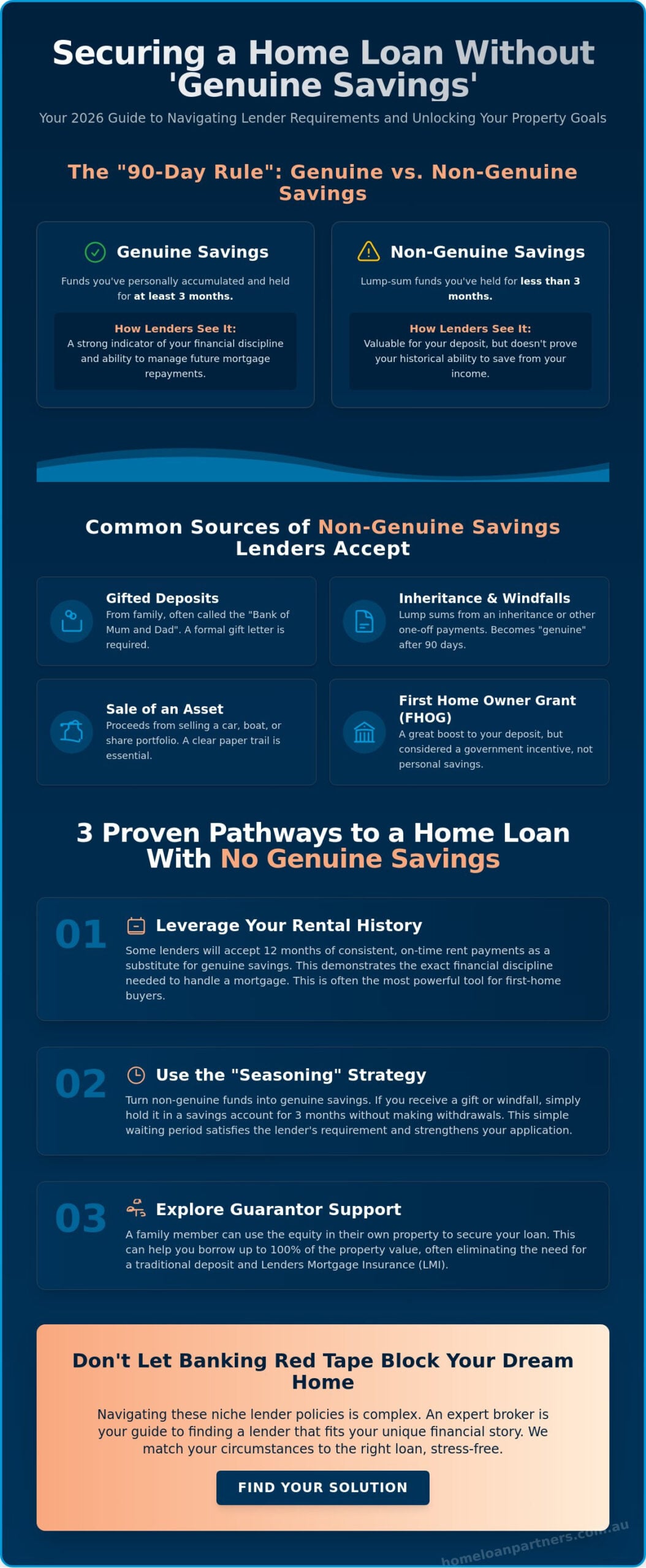

When you’re researching how to get a home loan with no genuine savings, the first step is understanding how Australian lenders categorize your deposit. Genuine savings are funds you’ve personally built up over time, typically held in a bank account for at least three consecutive months. Lenders view this as a practical stress test. It demonstrates that you can manage your income and expenses while consistently setting money aside, which mirrors the discipline required to meet monthly mortgage repayments. Our experts often see this history as the foundation of a successful application.

Non-genuine savings include lump sums that haven’t been in your possession for long. These are often gifts from parents, tax refunds, inheritance, or even the sale of a personal asset like a car. While these funds contribute toward your down payment, they don’t prove your historical ability to save from your regular salary. If you’re looking at how to get a home loan with no genuine savings, you’ll need to work with a partner who knows which lenders accept alternative equity sources.

The 90 day seasoning rule is a vital tool for many first-home buyers. If you receive a gift or a bonus, you can transform these non-genuine funds into genuine savings simply by holding them in a savings account for three months. This period of inactivity tells the bank that the money is stable and under your control, which significantly improves your risk profile in the eyes of credit assessors.

Why Banks Are Strict About Savings History

The Australian Prudential Regulation Authority (APRA) mandates that banks maintain high standards for capital stability. Because savings patterns are a reliable predictor of loan default rates in fluctuating markets, lenders use your history to gauge future behavior. They want to ensure you won’t struggle when interest rates shift or unexpected expenses arise. Genuine savings are a measure of financial discipline demonstrated through consistent accumulation or maintenance of funds over a 90 day period.

The Impact on Your Loan-to-Value Ratio (LVR)

Your savings history determines your borrowing limit and the cost of your debt. Most lenders require at least 5% of the purchase price to be genuine savings if you intend to borrow 90% or 95% of the property value. If your deposit is entirely non-genuine, you might be restricted to a lower LVR, or you may face much higher premiums for Lenders Mortgage Insurance (LMI). You can use our Mortgage Repayment Calculator to test different LVR scenarios and see how your deposit type influences your monthly commitment. This clarity helps you plan a seamless transition into homeownership without the stress of hidden financial hurdles.

Common Sources of Non-Genuine Savings and Lender Views

Lenders typically look for a 5% deposit saved through consistent effort over time. However, many Australians reach their property goals using alternative funds. Understanding how to get a home loan with no genuine savings starts with identifying which “non-genuine” sources lenders actually accept. These funds are often just as valuable as a traditional savings account, provided you document them correctly.

- Gifted deposits: This is the most frequent path for first-home buyers. Around 60% of new entrants to the Australian market now receive financial help from the “Bank of Mum and Dad.”

- Inheritance and lump-sum windfalls: Receiving a windfall is a life-changing event, but lenders view its timing strictly. If the money has been in your account for less than 90 days, it’s non-genuine. Once it passes that three-month mark, most banks reclassify it as genuine savings.

- Sale of non-real estate assets: You can use proceeds from selling a car or a share portfolio. You must provide a clear paper trail, including the contract of sale and the bank statement showing the A$10,000 or A$20,000 deposit.

- First Home Owner Grant (FHOG): While the grant provides a significant boost, often A$10,000 depending on your state, it doesn’t count as genuine savings. It’s a government incentive rather than a demonstration of your personal ability to manage a budget.

Most major banks require a 5% genuine savings component if you’re borrowing more than 90% of the property value. If you don’t have this, we often look toward non-bank lenders or specific products designed for those with strong incomes but alternative deposit sources.

The Gift Letter Requirement

Lenders require a formal declaration to ensure your deposit is a true gift. This letter must state the money is unconditional and requires no repayment. If a lender suspects the gift is actually a private loan, they’ll count those “repayments” against your borrowing capacity. Common mistakes include vague wording or failing to have all parties sign the document. A clear, professionally drafted letter ensures the bank views the funds as a permanent increase in your equity.

Tax Refunds and Work Bonuses

One-off payments like a A$6,000 tax refund or a performance bonus can help bridge the gap to a 20% deposit. While helpful, a tax refund is a return of income but not a savings pattern. To make these funds more attractive to a lender, you can “park” them in a high-interest account for three months to satisfy the 90-day rule. If you’re looking for a way to use these funds sooner, a dedicated mortgage partner can identify lenders who accept rental history as a substitute for a savings pattern. This strategy helps you move into your home faster without waiting for the next financial year.

Alternative Pathways: Rent as Genuine Savings and Guarantors

The traditional path to property ownership often feels blocked by the requirement for a 5% deposit held in a bank account for three months. However, the Australian lending market in 2026 offers several flexible routes for those who have the income to support a loan but haven’t yet built a cash reserve. Understanding how to get a home loan with no genuine savings involves looking at your existing financial habits and your family network as powerful tools for security.

Using Your Rent History to Qualify

Lenders like Westpac, St. George, and several credit unions now recognize that consistent rental payments are a reliable indicator of financial discipline. If you’ve been renting for at least 12 months, your rent can often act as a proxy for genuine savings. This policy acknowledges that paying A$600 or A$800 per week in the private rental market leaves little room for additional cash accumulation, yet proves you can manage a mortgage-sized commitment.

To use this pathway, you must provide a formal rental ledger from a licensed real estate agent. Private board arrangements usually don’t qualify because they lack the third-party verification banks require. You’ll also need a current, signed lease agreement. This strategy works best when combined with a gift from parents or a small personal loan for the initial deposit. For more details on state-specific support that can complement this strategy, explore our First Home Buyer Guide for NSW residents.

The Power of a Family Guarantor

A guarantor loan remains the most effective way to enter the market with zero dollars upfront. By using a portion of the equity in a family member’s home, usually a parent’s property, the bank gains the security it needs to waive the deposit requirement. This structure often allows you to borrow 100% of the property value plus purchase costs like stamp duty.

The primary financial benefit is the total removal of Lenders Mortgage Insurance (LMI). On a A$750,000 purchase, avoiding LMI can save you upwards of A$25,000. It’s a significant head start that puts you in a position of immediate equity growth. We work closely with families to ensure guarantors understand their obligations; they aren’t responsible for the whole loan, but rather a specific, limited portion of the security.

Equity in Existing Assets

If you own other assets, you might not need cash at all. Lenders may consider the following as collateral:

- Share Portfolios: Large holdings in ASX-listed companies can sometimes be used as security.

- Existing Real Estate: Equity in a small investment unit or a plot of land can be leveraged.

- Tax Refunds: While not “savings,” a large lump sum from the ATO can often be used as a deposit if your rent covers the “genuine” component.

Comparing Your Options

Each pathway has distinct advantages depending on your long-term goals. Choosing the right one ensures your journey remains stress-free and sustainable.

- Rental Pathway: Best for those with high disposable income but low cash. Pro: Independence from family. Con: You still need to find the 5% cash from somewhere, like a gift.

- Guarantor Loans: Best for fast-tracking entry. Pro: Zero deposit needed and no LMI fees. Con: Relies on family property and their financial consent.

- Asset Leveraging: Best for diversified investors. Pro: Keeps your cash liquid. Con: Volatile assets like shares may be valued conservatively by the bank.

How to Apply for a Home Loan Without Genuine Savings

Securing your first property is a milestone that shouldn’t be delayed just because your deposit didn’t come from a long-term savings account. Understanding how to get a home loan with no genuine savings involves shifting the focus from how you saved to how you manage your financial life today. We’ve broken this process into five manageable steps to help you move forward with confidence.

- Step 1: Audit your deposit sources. Collect every piece of evidence for your funds, whether it’s a gift from parents, a work bonus, or an inheritance. Documenting the paper trail early prevents delays during the assessment phase.

- Step 2: Verify your credit health. Lenders often view non-genuine savings as a higher risk. You should ensure your credit report is spotless; even a small A$250 utility default from three years ago can trigger an automated rejection in this category.

- Step 3: Target specific lenders. Many major banks have strict “genuine savings” hurdles that require 5% of the purchase price to be held for three months. You need a lender whose policy specifically caters to alternative deposit sources.

- Step 4: Prove your stability. Your application must highlight a steady career and reliable income. Banks generally look for at least 12 months of continuous employment to offset the lack of a traditional savings history.

- Step 5: Secure a formal pre-approval. This provides a clear ceiling for your property search and signals to real estate agents that you’re a serious, vetted contender.

Pre-Application Checklist

Before we submit your file, we ensure your financial profile is ready for bank scrutiny. You’ll need evidence of 12 months of continuous employment and bank statements from the last six months showing zero overdraws or late payment fees. If you’re using a gift, a signed statutory declaration from the donor is essential. This document confirms the money is a non-repayable gift rather than a hidden debt that could impact your borrowing capacity.

Choosing the Right Lender Panel

Walking into your local branch often leads to a dead end because they only have one set of rules. We act as your expert partner by accessing a panel of over 36 lenders. Some banks weight non-genuine funds differently; for instance, one lender might accept a 10% gift immediately, while another requires you to hold that gift in your account for 90 days first. We navigate these nuances to find the right fit for your goals. If you’re ready to see which options fit your specific situation, you can book a free strategy session with our team today.

Learning how to get a home loan with no genuine savings is about presenting a professional, low-risk narrative to the right bank. By focusing on your current income stability and clean account conduct, we can often overcome the hurdle of a non-traditional deposit and get you into your new home sooner.

Partnering with a Broker to Secure Your Approval

Securing a mortgage without a traditional deposit history requires more than just a standard application; it demands a strategic approach. At Home Loan Partners, we take on the heavy lifting by filtering through hundreds of credit policies to find the specific lenders that cater to your unique situation. We understand that life doesn’t always fit into a neat box, and your path to homeownership shouldn’t be blocked by rigid, outdated criteria.

Our team accesses policy niches that aren’t visible to the general public. While a local bank branch might tell you a 5% genuine savings deposit is mandatory, we know which lenders accept rental history or a 12 month history of on-time personal loan repayments as a substitute. We focus on tailoring your loan structure to ensure your long-term financial health, looking at offset accounts and flexible repayment options that protect your cash flow. Our support doesn’t end when the bank says yes; we stay by your side from the initial strategy session through to settlement and the years that follow.

The Advantage of Expert Guidance

We translate complex bank-speak into clear, actionable advice. Banks often use confusing terminology like “LVR caps” or “HEM benchmarks” that can make the process feel overwhelming. We simplify these concepts so you can make informed decisions with confidence. Our commitment is to find a seamless path to homeownership that aligns with your specific career trajectory and lifestyle goals.

To see this in practice, consider a recent case involving a teacher in Sydney. She had a A$65,000 gift from her parents but no 3 month history of personal savings. Most major lenders rejected her because she didn’t meet the “genuine savings” threshold. By applying our knowledge of how to get a home loan with no genuine savings, we identified a lender that accepts a 12 month rental ledger as proof of financial discipline. We secured her a 95% loan approval within 10 business days, allowing her to purchase her first apartment before prices climbed further.

Take the First Step Today

Many prospective buyers believe they must wait 90 days to “season” their funds in a bank account before applying. This delay can be costly in a rising market where property values might increase by A$10,000 or more in a single quarter. A quick consultation with our team can clarify your options immediately. We often find that clients are ready to apply much sooner than they realized once we apply the right policy exceptions.

Don’t let technicalities stand between you and your property goals. We provide the steady hand and expert precision needed to move forward. Partner with us to find your home loan solution today and discover how to get a home loan with no genuine savings through a stress-free, professional process tailored to your future security.

Take the First Step Toward Your 2026 Property Goals

Securing a property in the 2026 Australian market doesn’t always require years of disciplined bank deposits. You can leverage alternative pathways like rent as genuine savings or family guarantor support to bypass traditional deposit hurdles. These strategies turn non-genuine sources like gifts or work bonuses into a viable path toward homeownership. Understanding how to get a home loan with no genuine savings is simply about finding the right lender who values your actual financial behavior over a static bank balance.

At Home Loan Partners, we act as your dedicated expert partner to navigate these complex requirements. We provide access to a panel of over 36 bank and non-bank lenders, ensuring you receive unbiased advice tailored to your 2026 goals. Our team specializes in complex first-home buyer scenarios and takes the stress out of the application process by doing the heavy lifting for you. We’re here to ensure your journey to settlement is smooth, steady, and supportive.

Your dream of owning a home is closer than you think, and we’re ready to help you make it happen with confidence.

Frequently Asked Questions

Can I get a home loan if my deposit is 100% gifted?

Yes, you can secure a home loan with a 100% gifted deposit through specific specialist lenders or by using a family guarantor. While most Australian banks require at least 5% of the property value to be saved over a 90 day period, 4 to 6 lenders currently accept a gift as the full deposit. You’ll simply need a signed statutory declaration from the donor confirming the funds don’t need to be repaid.

Does a tax refund count as genuine savings in Australia?

A tax refund doesn’t count as genuine savings the moment it hits your bank account. Lenders usually view these funds as a one off windfall rather than a demonstrated habit of financial discipline. To use your refund as genuine savings, you must hold the funds in your account for at least 3 months. This timeframe allows the bank to reclassify the money under standard Australian lending criteria.

How much extra does a no genuine savings loan cost?

You’ll typically pay a slightly higher interest rate, which often ranges from 0.2% to 0.5% above standard market products. This small premium acts as a buffer for the lender to manage the perceived risk of the application. Our team focuses on finding a tailored path to refinance you into a lower rate once you’ve built 20% equity in your home, ensuring your long term financial health.

Can I use my rental history instead of a 5% deposit?

Yes, you can use a strong rental history to satisfy the genuine savings requirement with several Australian lenders. If you’ve paid your rent on time for 12 consecutive months and your lease is managed by a licensed real estate agent, this often replaces the need for a personal savings history. This strategy is a popular way to understand how to get a home loan with no genuine savings.

What happens if I have the deposit but it hasn’t been in my account for 3 months?

Your funds will be classified as non-genuine savings if they’ve been held for less than the required 90 day period. In this situation, you might need a family guarantor to secure an immediate approval or choose a lender that accepts higher risk profiles. We’ll help you track this timeline so you can apply at the exact moment your funds meet the bank’s strict criteria.

Is a guarantor loan the same as a no genuine savings loan?

A guarantor loan isn’t the same thing, though both serve as a bridge to homeownership. A guarantor loan uses a portion of a family member’s home equity as additional security, which often removes the need for any cash deposit. A no genuine savings loan still requires a physical deposit, but that money can come from a gift, inheritance, or tax refund rather than your own bank balance.

Do I still have to pay Lenders Mortgage Insurance (LMI) without genuine savings?

You’ll almost certainly pay LMI if your total deposit is less than 20% of the property’s purchase price. This insurance protects the lender rather than the borrower, and the cost is usually added to your total loan balance so you don’t have to pay it upfront. Navigating these costs is a vital step when learning how to get a home loan with no genuine savings and planning your future.