On a Saturday morning in Melbourne, a couple finds their perfect family home, only to realize their current property is still weeks away from being ready for auction. Data from CoreLogic in late 2024 showed that properties in high-demand suburbs often sell in fewer than 30 days, which creates an intense pressure for buyers to act fast. We understand that the fear of missing out on a dream property is real, just as the stress of moving twice or finding a short-term rental is often overwhelming. You deserve a transition that feels like a steady step forward rather than a logistical hurdle.

This guide explains how bridging finance serves as a vital tool to help you secure that new front door key before you’ve even handed over your old one. As your dedicated finance partner, we’ll walk you through the total cost structures and how two loans are managed simultaneously without the usual complexity. You’ll gain a clear understanding of the repayment process and the confidence to execute a secure exit strategy for your 2026 move. We’re here to ensure your property journey is as seamless and rewarding as possible.

Key Takeaways

- Discover how to secure your dream home before selling your current property, eliminating the stress of double moves or expensive short-term rentals.

- Master the mechanics of bridging finance to effectively manage the transition between your existing mortgage and your new purchase with confidence.

- Identify the essential equity and LVR criteria required to qualify for a short-term lending solution in the evolving 2026 Australian property landscape.

- Learn how accessing a broad panel of 36+ lenders provides a significant advantage over traditional banks when tailoring a loan to your specific financial goals.

- Evaluate the strategic balance between interest costs and the convenience of a single move to ensure your property transition is both smooth and financially sound.

Understanding Bridging Finance: The Strategic Link to Your Next Home

Finding your next home in the 2026 Australian property market requires more than just a keen eye for real estate; it demands a nimble financial strategy. Bridging finance serves as that strategy. It’s a specialized, short-term lending option designed for homeowners who’ve found their next property but haven’t yet sold their current one. This “buy first, sell later” approach removes the frantic pressure of trying to time two settlements perfectly on the same day, which is a common source of stress for growing families and downsizers alike.

To understand the core mechanics, one might ask: What is a bridge loan? Essentially, it’s a temporary facility that covers the purchase price of your new home while your existing asset is still on the market. Most Australian lenders provide a standard 12-month window to complete your sale. This timeframe gives you the breathing room to present your home beautifully and hold out for the right buyer, rather than accepting a low-ball offer just to meet a deadline. By using the equity in your current property as a lever, we help you transition between homes with a sense of calm and control.

The Difference Between Bridging and Traditional Mortgages

Standard home loans are built for the long haul, usually spanning 25 to 30 years with regular principal and interest repayments. In contrast, bridging finance is a fleeting arrangement. During the bridge period, you aren’t typically required to make double mortgage payments. Instead, interest often capitalizes or stays as interest-only until your home sells. Once the sale is finalized, the proceeds pay down the bridge, and any remaining debt is rolled into a standard remortgage tailored to your new long-term goals. This structure ensures your monthly cash flow remains stable during the transition.

Why 2026 Property Trends Make Bridging Finance Relevant

The 2026 property landscape is characterized by lean listing volumes, with stock levels in major capitals like Brisbane and Perth remaining 15% below the five-year average. In such a competitive environment, being an unconditional buyer is your greatest asset. Sellers and agents prioritize certainty. If you’re waiting on a “subject to sale” clause, you’ll likely lose out to a buyer who can sign the contract immediately. Bridging finance is a tactical financial bridge for the 2026 Australian homeowner. It transforms you into a cash-ready participant, allowing you to move with confidence when the right opportunity appears.

- Avoid Double Moves: You won’t need to pay for temporary rentals or storage units.

- Market Timing: Buy your new home when you find it, and sell your old one when the market is peaking.

- Auction Ready: Bid with the confidence of an unconditional buyer.

- Flexibility: Enjoy up to 12 months to finalize your sale without financial strain.

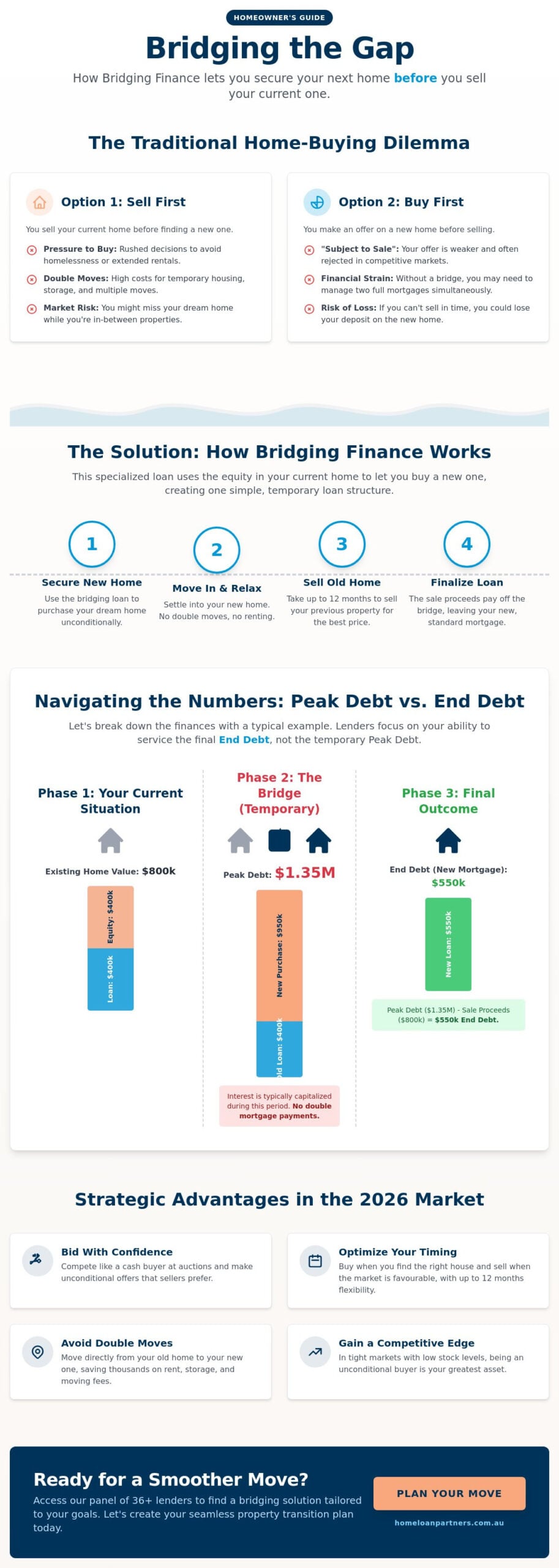

How Bridging Loans Work: Navigating Peak Debt and End Debt

Bridging finance acts as a temporary financial span that allows you to secure your next home before selling your current one. This facility combines your existing mortgage with the purchase price of your new property into one streamlined arrangement. By using the equity built up in your current residence as security, you can often access the funds needed for a deposit and stamp duty without needing to liquidate assets first. This process removes the intense pressure of perfectly timing two settlements on the same day.

Defining Peak Debt vs. Ongoing (End) Debt

The mechanics of a bridge involve two distinct phases. Peak debt is the total amount you owe while you own both properties. It includes your original mortgage, the new purchase price, and closing costs. For example, if you have a A$400,000 mortgage and buy a new home for A$950,000, your peak debt climbs to A$1.35 million plus costs. Lenders focus heavily on your ability to service the end debt, which is the balance remaining after your original home sells and the proceeds clear the bulk of the peak debt. Most Australian lenders grant a bridging period of up to 12 months for established homes, giving you ample time to find the right buyer. Deciding is a bridge loan right for you? often depends on how comfortable you feel with this temporary peak figure and the projected sale price of your current asset. Using a bridging loan calculator Australia homeowners trust can help you model these figures accurately before committing to a purchase.

Repayment Structures During the Bridging Period

Managing cashflow is vital during a move, so lenders offer flexible repayment structures tailored to your needs. Many homeowners opt for interest capitalization. With this method, you don’t make repayments on the new portion of the loan during the bridging period. Instead, the interest accrues and is added to your total loan balance. This keeps your daily outgoings identical to what they were before you started the process, which is a significant relief during a stressful move. Other borrowers prefer interest-only repayments to prevent the loan balance from growing. We act as your partner to determine which path minimizes your financial strain. You can speak with an expert to model these different scenarios based on your current equity and income. Once your original property settles, the peak debt is extinguished, and your loan converts into a standard principal and interest mortgage on your new home.

The Pros and Cons: Is Bridging Finance Right for Your Situation?

Deciding to upgrade your home involves more than just a change of address; it’s a significant financial pivot. Bridging finance offers a bridge over the gap between buying and selling, but it requires a clear-eyed look at the numbers. While the convenience is high, the interest rates often sit higher than your standard mortgage. You’ll likely see rates that don’t include the usual package discounts. This makes it a premium product designed for a specific, short-term purpose. A realistic property valuation is the cornerstone of this strategy. If you overestimate your sale price by even 5%, your final debt could be significantly higher than planned. We prioritize accuracy over optimism to ensure your financial security remains intact.

The Benefits of Buying Before Selling

Buying your next home before selling the current one eliminates the logistical nightmare of a double move. In major cities like Sydney or Brisbane, the median weekly rent for a house reached A$750 in early 2024. Avoiding a six-month rental saves you A$19,500 in rent alone. This doesn’t even account for the A$2,000 to A$4,000 typically spent on double removalist fees and temporary storage. You secure your dream property the moment it appears. This is vital in competitive markets where the best homes often sell in under 21 days. For families, this means staying in the same school zone without the disruption of a “halfway house.”

Managing the Risks of a Delayed Sale

The primary risk involves time. Most Australian lenders provide a 12-month window to sell your existing property when using bridging finance. If the house remains on the market past this point, the financial pressure increases. Interest often compounds during this period. This means your debt grows every month the property remains unsold. We mitigate this through conservative planning. We don’t look at the “best-case” sale price. Instead, we plan for a realistic figure based on local auction results from the last 90 days. An expert partner helps you build a buffer into your calculations. This ensures that even if the market fluctuates by 3% or 4% during your sale campaign, your long-term lifestyle isn’t compromised. We act as your steady guide, keeping the process predictable and calm.

Qualifying for Bridging Finance in the Australian Market

Securing bridging finance in 2026 involves more than just having a high income. Lenders focus heavily on the safety of the transition between your two properties. They calculate your “peak debt,” which is the total amount you owe when you hold both mortgages simultaneously. To manage this risk, a solid equity position in your current home is non-negotiable. We act as your expert partner to determine if your current financial structure aligns with these high-level requirements before you commit to a purchase. This proactive assessment prevents the stress of a declined application during a critical buying window.

Essential Eligibility Criteria

Lenders look for a minimum equity threshold of at least 20% in your current property. Your serviceability is tested against the “end debt” balance using a 3% interest rate buffer as of 2026. Accessing a panel of 36+ lenders is vital, as each bank assesses credit health and income differently. We help you identify which lender’s criteria match your specific financial profile.

Property appraisals play a central role in this approval process. A bank-appointed valuer will assess your current home to provide a realistic valuation, which is often more conservative than current market listings. This figure forms the basis of your borrowing capacity. We guide you through these valuations so you aren’t caught short when it’s time to settle on your new home. Having a clear understanding of your property’s value ensures you don’t overextend during the bidding process.

Documenting Your Exit Strategy

Your exit strategy must provide a clear plan for your property sale to mitigate lender risk. Most Australian lenders require an LVR of 80% or less to approve bridging finance without Lenders Mortgage Insurance. This strategy must outline your listing timeline, chosen real estate agency, and marketing approach. Preparing your home for a quick sale is essential to minimize interest costs and ensure a smooth transition to your new mortgage.

A successful exit strategy relies on realistic timing. Most bridging periods last between six and twelve months. If the property doesn’t sell within this window, interest costs can compound, impacting your long-term wealth. We provide the steady hand you need to coordinate these moving parts, ensuring your transition to your new home is as seamless as possible. By focusing on a quick turnaround, you protect your equity and move into your next chapter with confidence.

Ready to see if your equity is working hard enough for your next move? Talk to the bridging finance experts at Home Loan Partners today.

How a Mortgage Partner Streamlines Your Property Transition

Buying a new home before selling your current one creates a unique set of financial pressures. It’s a period where precision matters more than ever. While many homeowners walk into their local bank branch, they often miss out on the specialized solutions that make a transition truly smooth. We act as your steady hand, managing the complex timelines and financial hurdles so you can focus on the excitement of your next chapter. Our team takes care of the heavy lifting, from the initial paperwork to the final settlement, ensuring you never feel overwhelmed by the process.

Why a Broker Beats Going Direct to One Bank

A single bank can only offer its own products, which is a significant limitation when you’re dealing with bridging finance. We provide access to over 36 lenders across Australia, including boutique firms that specialize in complex property transitions. This variety is vital because every lender views “Peak Debt” differently. Some banks require you to service the entire debt of both properties simultaneously, which can be a hurdle for many families. Others offer more flexible serviceability rules that account for the expected sale price of your current home.

We help you find the lenders who see the big picture. We also provide the professional guidance needed to use your equity effectively, ensuring your bridging finance arrangement is a bridge to a better lifestyle, not a source of stress. By comparing diverse products that a single bank won’t show you, we find the structure that protects your cash flow during the overlap period. This tailored approach is designed to keep your interest costs manageable while you prepare your old home for market.

Planning Your Seamless Home Upgrade

In the 2026 property market, speed and certainty are your greatest assets. When you work with an expert partner, you aren’t just getting a loan; you’re gaining a strategist. Our process starts with a personalized financial assessment to determine exactly what you can afford without overextending. We manage the intricate communication between lenders, valuers, and solicitors to prevent the common pitfalls that cause settlement delays.

A successful property transition requires a structure that looks at where you want to be five years from now, not just on move-in day. We ensure your loan remains appropriate for the life of the mortgage, even after your current home sells. Our support doesn’t end when you get the keys. We stay by your side as your long-term partner, reviewing your mortgage regularly to ensure it still serves your family’s evolving goals. This commitment to longevity is what helps our clients achieve the Australian dream of homeownership with total confidence.

Ready to make your next move? Speak with our expert partners today.

Secure Your Future in the 2026 Property Market

Moving into your next home doesn’t have to be a source of stress. By mastering the mechanics of peak debt and understanding how to qualify in the 2026 Australian market, you can secure your dream property before selling your current one. Bridging finance provides the essential flexibility you need to act quickly when the right opportunity appears. It’s about turning a complex transition into a clear, manageable path forward for your family.

At Home Loan Partners, we’re here to act as your steady guide. We provide access to a panel of over 36 lenders, ensuring you receive expert, unbiased advice tailored to your specific long-term goals. Our team handles the heavy lifting so you can focus on the excitement of your new home. Whether you’re navigating equity requirements or looking for a seamless settlement, we’ll help you find the right fit for your unique situation.

Partner with our experts for a stress-free property transition

Your next chapter starts with a partner who values your security and your future as much as you do.

Frequently Asked Questions

How much more expensive is bridging finance compared to a standard loan?

Bridging finance typically carries an interest rate between 1% and 2% higher than standard variable home loans. In the 2026 Australian market, most lenders charge these premium rates because the loan is short term and requires more intensive administrative oversight. You should also budget for establishment fees which often range from A$500 to A$1,000 depending on the lender.

While the interest rate is higher, the interest is often capitalized into the loan. This means you don’t have to make out of pocket repayments during the bridging period. This structure protects your cash flow while you’re managing two properties. Our team helps you calculate these costs upfront so there are no surprises during your transition.

Can I get bridging finance if I haven’t put my current house on the market yet?

You can secure bridging finance before your current home is listed, though most lenders require a signed contract of sale or a firm marketing plan within 90 days of settlement. This flexibility allows you to act quickly when you find your dream home. It’s a strategic way to buy without the pressure of a rushed sale.

We work as your partner to navigate these timelines and ensure your application meets specific bank criteria. This proactive approach ensures you’re ready to bid at auction with confidence. By preparing early, you avoid the stress of trying to coordinate two settlements on the exact same day.

What happens if my house doesn’t sell within the 12-month bridging period?

If your property remains unsold after 12 months, your lender will typically review your financial position to offer a 3 to 6 month extension. In some cases, they might require you to convert the debt into a standard principal and interest loan or suggest lowering your asking price. Data from 2025 shows that 85% of these loans in Australia settle within the initial term.

We stay by your side to negotiate with the bank if market conditions shift unexpectedly. Our goal is to provide a steady hand and expert guidance throughout the entire journey. Having a clear exit strategy from the start is the best way to maintain your financial security.

Do I need a deposit for a bridging loan if I have equity?

You don’t need a cash deposit if you have sufficient equity in your current property to cover the 20% deposit and purchasing costs of the new home. Lenders look at your total peak debt, which is the combined value of your existing mortgage and the new purchase. If your Loan-to-Value Ratio stays below 80%, your equity acts as the security.

This allows you to buy your next home seamlessly without dipping into your personal savings or emergency funds. It’s a powerful tool for homeowners who have seen their property value grow over the last few years. We’ll help you calculate exactly how much equity you can unlock for your next move.

Is bridging finance available for investment properties or just owner-occupiers?

Bridging finance is available for both owner-occupiers and investors looking to expand their Australian property portfolio. While most applications focus on primary residences, many lenders provide tailored options for investment properties provided the exit strategy is clear. You can use this tool to secure a high yield asset before selling an underperforming one.

This strategy helps you maintain market presence and avoid missing out on capital growth opportunities in competitive suburbs. We guide you through the different tax implications and lending requirements for investment bridging. Our expert team ensures the loan structure aligns with your long term wealth goals.

Can I use a bridging loan for a construction project or major renovation?

Most lenders don’t allow standard bridging loans for major construction or structural renovations because of the strict 12 month repayment deadline. Instead, you would typically use a specialized construction loan or a land-and-build facility. These products are designed to handle the staged payments required for building work.

If you’re only doing minor cosmetic updates to maximize your sale price, we can guide you toward an equity release instead. This ensures you have the funds for a fresh coat of paint or new carpets without the constraints of a bridging agreement. We’ll help you choose the path that best suits your renovation timeline.

What is a bridging loan calculator and how accurate is it?

A bridging loan calculator Australia buyers and homeowners rely on is a digital tool that estimates your peak debt and interest costs based on your current mortgage and new purchase price. While these tools provide a 90% accuracy rate for basic scenarios, they often omit specific bank fees or state based stamp duty calculations. It’s a helpful starting point for your initial research.

For a precise figure, our experts provide a detailed breakdown that accounts for every Australian tax and lending requirement. We believe in total transparency, so we’ll show you exactly how the numbers work for your specific situation. This clarity helps you make an informed decision about your next home purchase.

How long does it take to get bridging finance approved in 2026?

Approval for bridging finance in 2026 generally takes between 10 and 20 business days from the initial application. This timeline depends on the complexity of your property valuations and how quickly the bank assesses both your current and future homes. We act as your partner throughout this process to speed up the paperwork.

By following up with lenders daily, we aim to make the process as seamless as possible. Getting a pre-approval early in your search ensures you can move with speed when the right property hits the market. We handle the heavy lifting so you can focus on finding your next home.