What if you could secure your next home in 2026 without the paralyzing fear of being stuck with two full mortgages at once? Most homeowners feel a genuine sense of dread when they consider the gap between buying and selling, especially with Australian property prices rising by an average of 4.1% over the last twelve months. By using a precise bridging loan calculator australia, you can strip away the mystery and see exactly how the numbers stack up for your specific situation. It is natural to feel confused by interest capitalisation or uncertain about how much equity you can actually use for your deposit.

We are here to act as your partner in this transition. Our guide will help you master the math behind your move, ensuring you have a clear figure for your monthly costs and the confidence that you won’t overextend your finances. You will learn the vital difference between peak and end debt, giving you a steady hand as you move toward a new front door. This article provides a clear roadmap for managing your peak debt and understanding the long-term journey of your loan.

Key Takeaways

- Understand why the “buy-before-you-sell” strategy requires a specialized financial approach to manage the transition between properties with confidence.

- Discover how to use a bridging loan calculator australia to accurately estimate your “peak debt” while holding two homes and your final “end debt” after settlement.

- Uncover the mechanics of interest capitalisation and how this feature allows you to manage cash flow by adding interest costs to your loan balance during the bridge.

- Learn to stress-test your property strategy by evaluating Loan-to-Value Ratios (LVR) to ensure your financial plan remains robust in the 2026 market.

- Explore how a dedicated mortgage partner transforms complex numbers into a tailored, low-stress path toward your next Australian home.

Decoding the Bridging Loan: Why You Need More Than Just a Number

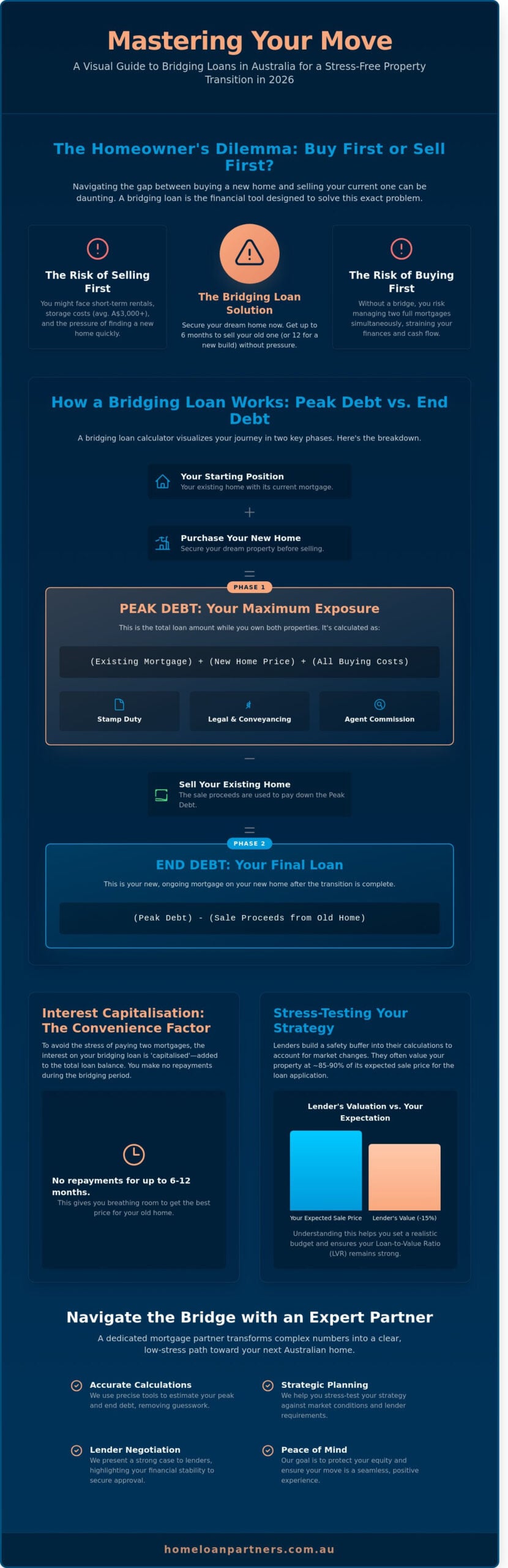

Finding your next home often feels like a race against time. In Australia’s fast-moving property markets, you might spot your dream home before you’ve even listed your current residence. This creates a classic “Catch-22” situation. Do you sell first and risk having nowhere to live, or buy first and struggle to cover two mortgages at once? A bridging loan acts as your financial bridge, allowing you to secure the new property immediately while your current one is still on the market. While a standard mortgage tool looks at simple monthly repayments, a bridge loan definition involves more moving parts, including peak debt and interest capitalisation. Using a specialized bridging loan calculator australia helps you visualize these two distinct phases: the initial bridging period and the final end loan.

A standard mortgage calculator fails here because it doesn’t account for the “Peak Debt” period. This is the total amount you owe when you hold both loans simultaneously. We guide you through this complexity by breaking down the costs into manageable steps. Your transition should be seamless, not a source of constant stress. By understanding how interest accrues during the bridging phase, you gain a clear picture of your total commitment before you sign a contract.

The Problem a Bridging Loan Solves

Moving house is stressful enough without doing it twice. Bridging loans eliminate the need for short-term rentals, which can cost upwards of A$3,000 in lease breaks, bond transfers, and storage fees. Most Australian lenders provide a 6-month window to sell an existing home, or 12 months if you’re building a new one. This timeframe gives you the breathing room to hold out for the right sale price rather than accepting a low-ball offer in a rush to settle. It’s about maintaining control over your financial journey.

Why “Commercial Intent” Matters When Calculating

When you use a bridging loan calculator australia, you’re doing more than just checking numbers; you’re building a purchase strategy. Accurate property valuations are the foundation of this process. Lenders typically apply a safety margin to your expected sale price, often around 15 percent, to protect against market fluctuations. Understanding these figures early helps you set a realistic bidding limit at auction. We act as your expert partner, translating these bank requirements into a clear, stress-free path forward that protects your equity and your future security.

How a Bridging Loan Calculator Works: Peak Debt vs. End Debt

Using a bridging loan calculator australia helps you visualize the two distinct phases of your financial transition. It simplifies a complex process into two manageable figures: your peak debt and your end debt. By inputting your current mortgage balance, the purchase price of your new home, and estimated selling costs, you gain a clear view of your temporary and long-term commitments. This clarity allows you to move forward with confidence rather than guesswork.

The core logic of the calculation follows a straightforward formula: (New Purchase Price + Existing Debt + Buying Costs) – Sale Proceeds. This equation identifies how much you’ll owe at the height of the move and what your mortgage will look like once the dust settles. Understanding how bridging finance in Australia works as a strategic tool is essential because it highlights that you aren’t just managing one loan, but a shifting financial structure that requires careful oversight.

Calculating Your Peak Debt

Peak Debt is the maximum financial exposure during the transition. It represents the total amount you owe the bank while you hold titles to two properties simultaneously. To get an accurate figure, you must include more than just the property prices. You need to account for:

- Government stamp duty, which can exceed A$30,000 on a median-priced home in many Australian states.

- Legal and conveyancing fees for both the sale and the purchase.

- Real estate agent commissions, typically ranging from 1.5% to 3.5% of your sale price.

Lenders look closely at this peak figure. They want to ensure your equity levels remain safe even if the market fluctuates. We act as your dedicated mortgage partner to help you present a strong case to lenders, ensuring they see the full picture of your financial stability during this peak period.

Estimating the End Loan Result

The End Debt is the remaining balance of your mortgage after you’ve sold your original property and applied the proceeds to the peak debt. This is the loan you’ll be left with for the long term. It’s the figure that truly impacts your daily lifestyle and future retirement goals. When you use a bridging loan calculator australia, it’s vital to be conservative with your sale price estimates.

Adding a “buffer” of 5% to 10% to your expected selling costs or lowering your expected sale price provides a safety net. If the market cools and your home sells for A$50,000 less than the optimistic appraisal, your end debt will be higher. By testing these “what-if” scenarios, you ensure your long-term borrowing power remains within a comfortable range. This proactive approach takes the stress out of the waiting game, allowing you to focus on settling into your new home.

Interest Capitalisation: The Hidden Cost of Convenience

Most Australian homeowners are familiar with standard principal and interest repayments. You pay a set amount each month; a portion covers the interest, and the rest reduces your debt. Bridging finance works differently. Because you’re often carrying two mortgages at once, many lenders allow you to “capitalise” the interest. This means you don’t make any repayments during the bridging period. Instead, the bank adds the monthly interest cost directly to your loan balance.

This mechanism offers a significant cash flow advantage during a stressful transition. You won’t need to find extra cash while your current home is still on the market. However, this convenience carries a compounding cost. Every month the interest is added to the balance, the next month’s interest is calculated on that new, higher figure. Using a bridging loan calculator australia helps you see exactly how this compounding debt grows over a four or six-month period. Without this visual aid, it’s easy to underestimate how quickly a $500,000 bridge can expand.

Repayment Options During the Bridge

In 2026, borrowers generally choose between interest-only repayments or full capitalisation. Interest-only payments keep your “End Debt” stable but require a healthy monthly cash surplus. For many families, capitalisation is the only viable path to avoid financial strain while waiting for a settlement. If your budget allows, making even small, ad-hoc payments of A$200 or A$500 can change the trajectory of your loan. These contributions reduce the amount being compounded, which protects your equity and lowers the final balance you’ll need to refinance into a long-term mortgage.

The Impact on Your Final Equity

The true cost of bridging becomes clear when you look at your final equity. If you have an $800,000 “Peak Debt” at a 6.75% interest rate, a six-month bridge with full capitalisation adds roughly A$27,500 to your total loan. This isn’t just a fee; it’s a direct reduction of the profit you expected from your sale. You should identify your “tipping point” early. This is the moment where the cost of holding the loan outweighs the benefit of waiting for a higher sale price. A bridging loan calculator australia allows you to compare different lender rates to see which one preserves more of your wealth. By running these numbers, we help you stay in control of your property journey rather than letting the interest dictate your financial future.

Interpreting Your Results: Stress-Testing Your Property Strategy

A bridging loan calculator australia tool provides a vital starting point, but it shouldn’t be your final destination. Real estate markets fluctuate, and relying solely on a best-case scenario where your home sells for top dollar in two weeks can lead to unnecessary pressure. We recommend running multiple scenarios to ensure your plan remains robust even if the market cools or buyers become hesitant.

Lenders look closely at your Loan-to-Value Ratio (LVR) during the bridging period. Typically, most Australian banks prefer an LVR below 80% to avoid Lenders Mortgage Insurance (LMI). If your current property sells for less than anticipated, your debt remains the same while your equity shrinks. This shift can push your LVR higher, potentially impacting your long-term interest rates or the final approval conditions of your permanent mortgage.

The “What-If” Analysis

Run your numbers again with a 5% and 10% reduction in your expected sale price. If your A$900,000 home sells for A$810,000 instead, how does that affect your “peak debt”? This exercise helps you find your break-even point. It’s the minimum price you must accept to cover the bridge and transition into your new mortgage comfortably. Creating this safety buffer in your purchase budget prevents a longer-than-expected sales campaign from becoming a financial burden.

Lender Requirements and Eligibility

Every lender uses a different formula for their internal calculations. Some may allow you to capitalise interest by adding it to the loan balance, while others require monthly payments throughout the bridge. The most critical hurdle is the “servicing test.” You must prove you can afford the “end debt” once the bridge is closed. Our team helps you compare options across our panel of 36+ lenders to find the right fit for your specific situation.

Preparing for a sales campaign that lasts 90 days instead of 30 is a smart move for any homeowner. Interest costs accumulate every month the bridge remains open. By using the bridging loan calculator australia results to factor in an extra three months of interest, you ensure your cash flow stays steady. Use these steps to stress-test your strategy:

- Calculate your peak debt at a 7% lower sale price to see the impact on your equity.

- Check if your LVR stays below the 80% threshold to avoid extra fees.

- Factor in an additional 60 to 90 days of interest costs to your total budget.

We’re here to help you move forward with total confidence and clarity. You can speak with an expert partner to refine your bridging strategy today.

Navigating the Bridge: How a Mortgage Partner Adds Value

While a bridging loan calculator australia provides a vital starting point, it can’t account for the nuances of your specific financial situation. Transitioning from a digital estimate to a tailored structure requires a human touch. At The Home Loan Partners, we focus on managing the “peak debt” phase. This is the period when you carry the debt of both your current home and your new purchase. It’s often the most stressful part of the journey. Our team guides you through this window, ensuring you have the liquidity needed to secure your new home without compromising your daily lifestyle or financial safety net.

We look beyond the immediate settlement. Our experts analyze how the bridge affects your long-term wealth. We find specialized bridging products that aren’t available to the general public, often featuring lower interest rates or more flexible capitalized interest options. This proactive approach ensures that when the dust settles on your sale, you’re left with a mortgage that’s sustainable and aligned with your future goals.

Why Work With a Broker for Bridging?

Bridging finance is a specialized niche in the Australian credit market. Many high-street banks have strict criteria that might not suit every buyer’s timeline. We do the heavy lifting by comparing options from over 36 lenders. This includes smaller, agile lenders who specialize in rapid turnarounds. We manage the complex timeline of coordinating two settlements simultaneously. If a buyer’s finance stalls on your sale, we’re there to pivot the strategy. Our advice stays unbiased because our goal is your security, not just a quick approval.

Your Next Steps to a Seamless Move

Taking the next step doesn’t have to be daunting. Once you’ve used the bridging loan calculator australia to get your bearings, it’s time to look at the bigger picture. You should use our mortgage repayment calculator to understand what your debt will look like after your current home sells. This ensures the “end loan” remains affordable for the next 20 to 30 years. We recommend booking a strategy session to verify your calculator results and ensure the numbers hold up against current bank valuations.

Follow this final checklist for a stress-free property transition:

- Verify your available equity to confirm you meet the 20% to 40% margin most lenders require for bridging.

- Review the “bridge period” terms, which typically last between 6 and 12 months in Australia.

- Organize a contract review for both your sale and purchase to align settlement dates as closely as possible.

- Confirm your exit strategy, whether it’s a standard private sale or an upcoming auction.

We’re here to make sure your move is a celebration, not a source of anxiety. By partnering with us, you gain a steady hand to navigate the complexities of dual-property ownership with confidence.

Securing Your Property Future in 2026

Using a bridging loan calculator australia tool provides a helpful starting point for your next move. It’s essential to look beyond the initial estimate and understand how peak debt levels impact your long-term financial health. You must also account for interest capitalisation, as these costs can quietly erode your equity if they aren’t managed with precision. These calculations are the first step in a much larger journey toward your new home. A successful transition requires a strategy that balances your current equity with your future goals.

You don’t have to navigate these technical details alone. At Home Loan Partners, we act as your steady guide through the entire process. We provide access to a panel of 36+ Australian lenders to find a structure that fits your specific needs. Our team specialises in complex bridging arrangements, ensuring your transition remains professional and stress-free. We do the heavy lifting so you can focus on the excitement of your new property. Let our experts guide your property move; book a strategy session today. Your dream home is within reach, and we’re here to help you bridge the gap with confidence.

Frequently Asked Questions

How much can I borrow for a bridging loan in Australia?

You can typically borrow up to 80% of the combined value of your current home and your new property. This total amount, known as the peak debt, covers your existing mortgage plus the purchase price and associated costs of the next home. Most Australian lenders require at least 20% equity across both properties to avoid Lenders Mortgage Insurance. Using a bridging loan calculator australia helps you estimate this peak debt and your final end debt once your current home sells.

Do I need a deposit for a bridging loan?

You don’t usually need a cash deposit because the equity in your current home secures the new purchase. Lenders treat the available equity in your existing property as the down payment for the next one. This allows you to bid at auction or sign a contract without waiting for your current sale to settle. We guide you through assessing your equity levels to ensure your transition remains seamless and stress-free.

What happens if my house doesn’t sell within the bridging period?

Most bridging periods last for 6 months for existing homes or 12 months for new builds. If your property hasn’t sold by the end of this term, your lender may require you to lower your asking price or convert the entire peak debt into a standard principal and interest loan. This conversion depends on your ability to meet serviceability requirements for the larger amount. Our team acts as your partner during this time to help navigate these deadlines.

Are bridging loan interest rates higher than standard home loans?

Bridging loan interest rates are typically higher than the discounted or honeymoon rates found on standard home loans. Many lenders charge their standard variable rate, which averaged between 6.5% and 7.8% for major banks in late 2024. Because these loans are short-term and carry higher administrative costs, you won’t usually find the same aggressive discounts offered on long-term mortgages. We help you compare these costs to ensure your long-term journey remains affordable.

Can I use a bridging loan for a new construction or renovation?

You can use a bridging loan for construction, and lenders often extend the bridging period to 12 months to accommodate building timelines. This provides a steady hand while you manage two sites simultaneously. It’s particularly useful if you want to stay in your current home until the new build is finished. A bridging loan calculator australia can help you factor in the progressive drawdowns required during the construction phases.

How long does it take to get a bridging loan approved in 2026?

Approval times in 2026 generally range from 5 to 10 business days as digital valuation tools and automated processing continue to speed up. While the initial assessment is fast, physical property valuations can still add a few days to the timeline. We manage the heavy lifting by coordinating with lenders and valuers to keep your purchase on track. This proactive approach ensures you’re ready to act when the right property appears.

Is interest capitalisation better than making repayments?

Capitalising interest is often better for your monthly cash flow because you don’t make repayments during the bridging period. Instead, the interest adds to your total loan balance and is paid off when your house sells. While this keeps your daily budget clear, it does increase the total amount of interest you pay over the life of the loan. We’ll help you weigh these options to find a tailored fit for your financial security.

What are the typical fees associated with a bridging loan?

You should expect to pay application fees ranging from A$600 to A$1,000, along with valuation costs for both properties. Lenders also charge legal fees and government registration fees, which can total approximately A$1,500 to A$2,500 depending on your state. There’s also a discharge fee once the bridge is closed. Our role is to provide clarity on these costs upfront, so there are no surprises during your homeownership journey.