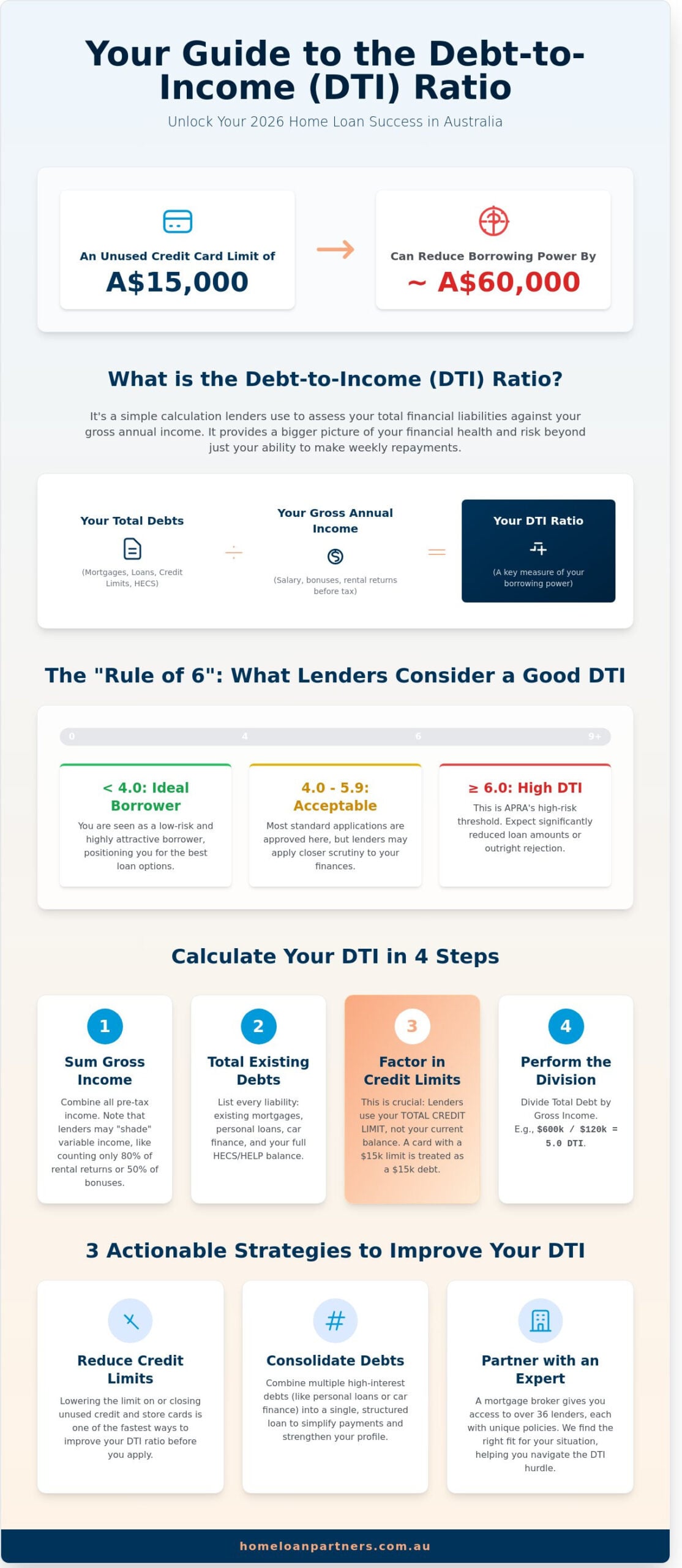

Last Tuesday, a couple in Brisbane discovered that their unused A$15,000 credit card limit reduced their borrowing capacity by nearly A$60,000. It’s a common shock for many Australians entering the 2026 property market. This happens because banks look beyond your savings and focus heavily on your debt to income ratio. You’ve likely spent years meticulously saving for a deposit, only to feel frustrated when a lender offers a much lower amount than you expected. It’s stressful to feel like your HECS debt or a simple credit card is standing between you and your homeownership goals.

As your partner in this journey, we want to help you move forward with confidence. You’ll discover exactly how lenders use your debt to income ratio to determine your borrowing power and how you can optimize your profile for a successful application. We’ll provide the specific DTI target lenders look for, a simple way to calculate your own figures, and three actionable steps to strengthen your position before you apply.

Key Takeaways

- Learn why Australian lenders in 2026 prioritize your debt to income ratio over traditional serviceability tests to determine your true borrowing capacity.

- Understand the “Rule of 6” and how keeping your total debt under four times your gross annual income can position you as a low-risk, highly attractive borrower.

- Discover practical steps to strengthen your application, such as consolidating high-interest debts and reducing unused credit limits before you apply.

- See how partnering with an expert broker gives you access to over 36 lenders, each with unique policies tailored to help you navigate the path to homeownership.

What is the Debt to Income Ratio and Why Does it Matter?

Your debt to income ratio is a straightforward calculation that compares your total financial liabilities to your gross annual earnings. It’s a snapshot of your financial health that goes beyond your monthly budget. While many borrowers focus on whether they can afford their weekly mortgage repayments, lenders in 2026 use this metric to see the bigger picture. To understand the foundational mechanics of this calculation, you can explore more about What is the Debt to Income Ratio and how it has historically shaped global lending.

In the current Australian market, banks prioritize DTI over simple serviceability tests because it reveals your total exposure to risk. A serviceability test checks if you can handle interest rate hikes, but the DTI ratio measures if your total debt load is sustainable relative to your income. It’s vital to distinguish this from the Debt Service Ratio (DSR). While DSR focuses on the percentage of income used for monthly debt payments, DTI looks at the total mountain of debt you’re carrying. Even if you have A$100,000 in savings, a high DTI signals to a bank that you’re overextended, making you a higher risk during economic shifts.

The Shift in Australian Lending Standards

The Australian Prudential Regulation Authority (APRA) has significantly tightened its oversight of the debt to income ratio over the last few years. As of 2026, Australian banks are strictly required to report and monitor “High DTI” loans, which are defined as any lending where the total debt is six times your gross annual income or greater. This regulatory focus means your borrowing power is now dictated more by this ceiling than by interest rates alone. If your total debt, including credit cards and existing personal loans, exceeds this 6x threshold, many lenders will automatically reduce your maximum loan amount to bring you back into a safer bracket.

The Emotional Weight of Debt Assessment

We understand that the mortgage application process feels deeply personal and often stressful. It’s easy to feel like a set of numbers on a spreadsheet, especially when a bank questions your financial choices. At Home Loan Partners, we view the DTI ratio as a tool for your long-term financial safety rather than just another hurdle to clear. Our role is to act as your expert partner, helping you see these metrics through the eyes of a lender while protecting your interests. We’ll guide you through the complexities of your assessment, ensuring your path to homeownership is steady and secure. We don’t just process applications; we partner with you to build a foundation for your future security in the Australian property market.

How to Calculate Your Debt to Income Ratio: A Step-by-Step Guide

Calculating your debt to income ratio is a vital first step in understanding your borrowing power. It provides a clear snapshot of your financial health from a lender’s perspective. Our team at Home Loan Partners helps you navigate this process to ensure you present the strongest possible application. Follow these four steps to find your number.

- Step 1: Sum your gross annual household income. This includes your base salary before tax, along with other consistent revenue streams like regular bonuses or rental returns.

- Step 2: Total your existing debts. List every liability you currently hold. This covers your existing mortgages, personal loans, car finance, and your HECS/HELP balance.

- Step 3: Factor in credit card limits. Lenders don’t look at what you owe on your card today; they look at the total limit available to you. A A$15,000 limit is treated as a A$15,000 debt.

- Step 4: Perform the final division. Divide your total debt by your gross annual income. For example, if you have A$600,000 in debt and earn A$120,000, your ratio is 5.0.

Understanding what constitutes a Good DTI Ratio in Australia is essential, as the Reserve Bank of Australia has observed how these figures influence broader economic stability. Most Australian banks in 2026 prefer to see a ratio below 6.0 for standard residential applications.

Defining “Gross Income” for the Calculation

Gross income is the total pre-tax earnings an individual or household receives from employment, investments, and government transfers on a recurring basis. While your base salary is straightforward, lenders often “shade” other income. This means they might only count 80% of your rental income or 50% of your performance bonuses to account for potential fluctuations. Casual work usually requires a 12 month history to be included in the calculation.

The Credit Card Trap: Limits vs. Balances

Many applicants are surprised to find that a zero balance on a credit card still counts against them. If you hold a card with a A$10,000 limit, the bank assumes you could spend that entire amount tomorrow. This “potential debt” disproportionately inflates your debt to income ratio. We often suggest that clients reduce their unused limits to A$1,000 or A$2,000 before applying. This simple move can immediately lower your ratio and boost your borrowing capacity.

Accounting for HECS/HELP and Student Debt

In 2026, lenders remain focused on how student debt impacts your monthly cash flow. While HECS doesn’t have a traditional interest rate, its indexation and the mandatory repayments deducted from your salary reduce your net take-home pay. If your ratio is sitting right on the edge of a bank’s threshold, paying off a small remaining HECS balance could be the key to approval. However, if the balance is large, it’s often better to keep that cash for your deposit. You can chat with our expert team to determine which path serves your long-term goals best.

The “Rule of 6”: What is a Good DTI Ratio in Australia?

In the current 2026 lending environment, the “Rule of 6” acts as a primary benchmark for Australian homeowners. Most “Big 4” banks categorize a debt to income ratio above 6.0 as high risk. This isn’t just a suggestion; it’s a threshold that triggers intense manual credit assessment. When you cross this line, banks look much closer at your spending habits and lifestyle choices.

If your ratio sits below 4.0, you’re in the “goldilocks zone.” Lenders view this as low risk, which often translates to faster approvals and access to the most competitive interest rates. You’ll find the path to settlement is much smoother when your total debt is less than four times your gross annual income. This level of borrowing provides a comfortable buffer against future interest rate hikes or unexpected life events.

Entering the “Hard Refusal” zone happens when your ratio climbs to 7.0 or 8.0. Data from the March 2025 APRA residential mortgage lending statistics shows that loans with a DTI of 6 or higher now represent less than 11% of new bank lending. For most traditional institutions, a ratio of 7.0 is a non-starter. It suggests you’re over-leveraged, leaving very little room for daily living expenses after the mortgage is paid.

- Under 4.0: Highly attractive to all lenders; qualifies for “best-in-class” rates.

- 4.0 to 6.0: Standard risk; requires clear evidence of stable employment.

- 6.0 to 7.0: High risk; often requires manual intervention or Tier 2 lenders.

- Above 7.0: Extremely difficult to secure through traditional channels.

Tier 1 vs. Tier 2 Lender Perspectives

Major banks face strict oversight from APRA, which limits how many high-DTI loans they can hold on their books. This pressure often makes them conservative. In contrast, Tier 2 or non-bank lenders frequently show more appetite for a debt to income ratio between 6.0 and 7.0. You’ll likely pay for this flexibility through a higher interest rate, sometimes 0.50% to 0.85% above the market average, to compensate the lender for the extra risk they’re carrying.

The Intersection of DTI and LVR

Lenders don’t look at your debt in a vacuum. Your Loan-to-Value Ratio (LVR) serves as a vital counterbalance. If you’ve saved a 25% deposit, a lender might overlook a DTI that’s slightly north of 6.0 because your equity provides a safety net. We act as your partner to highlight these mitigating factors, such as high career growth potential or significant liquid assets. This ensures the bank sees the person behind the percentages and understands your long-term financial security.

Practical Strategies to Lower Your DTI Before You Apply

Improving your debt to income ratio isn’t just about earning more; it’s about refining how your current financial commitments appear to a lender. In the first quarter of 2026, Australian lenders have tightened their scrutiny on existing liabilities. Every dollar you owe on a high-interest personal loan or a credit card limit carries more weight than you might expect. Banks don’t just look at what you owe; they look at your potential to spend.

- Consolidate high-interest debt: Roll personal loans or car finance with 12% to 18% interest rates into a single, lower-rate facility to reduce your monthly outgoing commitments.

- Slash credit limits: A credit card with a A$15,000 limit is often assessed as a A$450 monthly liability, even if the balance is zero. Closing unused cards or dropping limits to A$2,000 can significantly boost your borrowing power.

- Document every dollar: If you’ve earned consistent overtime or bonuses over the last 24 months, ensure your tax returns and payslips clearly reflect this. Lenders in 2026 typically require a two-year average to include variable income in your DTI calculation.

- Pause major spending: Delaying a A$60,000 car loan until after your home loan settlement could prevent your application from being flagged as high-risk by the big four banks.

The “Clean Slate” Approach for Refinancing

If you already own property, a strategic refinance can act as a financial reset. By using your existing equity to consolidate “bad debt” like high-interest store cards or personal loans, you replace fragmented, expensive repayments with a single, manageable mortgage payment. This move lowers your total monthly debt obligations, which directly influences your debt to income ratio assessment. You can explore our Refinancing Guide to see how debt consolidation structures work in the current market.

Timing Your Application

Patience is a financial asset. Taking a 90-day to 180-day window to aggressively pay down small balances can move your application from a “marginal” to an “automatic” approval. Before you submit your paperwork, conduct a “health check” with your partner to ensure no new Zip or Afterpay accounts have been opened, as these digital credit facilities are now visible on comprehensive credit reports. Waiting six months to clean your balance sheet is a small price to pay for a lifetime of lower interest rates.

How a Mortgage Broker Partner Helps You Beat the DTI Hurdle

Managing a debt to income ratio in the 2026 property market requires more than a healthy salary. It demands a strategic approach to how your financial profile is presented to lenders. While many major banks apply rigid caps, we understand that your financial story is unique. We act as your professional advocate, ensuring that a single number doesn’t stand between you and your property goals.

Our team provides direct access to over 36 lenders, including major banks and specialist credit providers. This variety is a significant advantage for borrowers. Every institution has a different appetite for risk and its own way of calculating your debt to income ratio. For example, while one lender might “shade” your rental income by 20%, another may recognize 100% of that cash flow, which immediately shifts your borrowing capacity in your favor.

- Expert Structuring: We look for income strengths that automated bank systems often ignore, such as consistent overtime, tax-effective salary packaging, or performance bonuses.

- Lender Matching: We identify the right lender for your specific ratio before you apply, protecting your credit score from the impact of a “bank rejection.”

- Professional Advocacy: We handle the complex negotiations and paperwork, presenting your application in the best possible light to meet internal credit policies.

By doing the heavy lifting, we remove the stress of the unknown. You won’t have to guess which banks are currently tightening their DTI limits. We stay across the daily changes in the Australian lending environment so you don’t have to.

Tailored Loan Structures

We look far beyond the immediate transaction to find a fit for your 10-year goals. In a complex regulatory environment, unbiased advice is your greatest asset. We aren’t just here for a one-time service; we act as your long-term partners through every rate cycle. By choosing the right lender for your specific financial situation from the start, we ensure your path to homeownership remains steady and predictable. Our focus is on building a structure that supports your lifestyle today and your equity growth tomorrow.

Ready to Check Your Borrowing Power?

The first step is a simple, no-obligation conversation. We take the heavy lifting out of the math by calculating your exact borrowing capacity across our entire lending panel. You don’t need to guess your limits or fear a bank’s rigid assessment. Let The Home Loan Partners guide you to a better loan structure today and gain the confidence to move forward with your property plans.

Secure Your Property Future with Expert Guidance

Navigating the 2026 property landscape requires more than just a deposit; it demands a clear understanding of how lenders view your financial health. Your debt to income ratio remains a primary factor in loan approvals, with the “Rule of 6” serving as a vital benchmark for most Australian banks. By proactively lowering your non-mortgage debt and structuring your finances correctly, you’ll position yourself as a low-risk borrower. You don’t have to navigate these complex bank requirements alone. Home Loan Partners provides access to over 36 leading Australian lenders, ensuring your loan is structured for long-term success. Our team offers expert guidance to first home buyers and investors, taking the stress out of the application process. We focus on your unique goals to turn the dream of homeownership into a reality. Let us do the heavy lifting while you focus on finding the right property. Our professional, stress-free loan structuring ensures you’re supported at every step of the journey. Book a free strategy session with our expert mortgage brokers to secure a steady hand for your property goals. We’re here to help you move forward with total confidence.

Frequently Asked Questions

What is a high debt to income ratio for a home loan in Australia?

A debt to income ratio of 6 or higher is generally considered high by Australian lenders and the Australian Prudential Regulation Authority (APRA). In 2024, APRA data showed that banks monitor this threshold closely to manage systemic risk. If your total debts are six times your annual gross income, you’ll likely face stricter assessment criteria or a higher interest rate. We’ll help you navigate these limits to find a path forward.

Does HECS debt count towards my debt to income ratio?

Yes, your HECS or HELP debt is included in the total debt calculation for your debt to income ratio. While it doesn’t carry a commercial interest rate, lenders view the total balance as a significant liability. This can reduce your borrowing capacity because the mandatory repayments decrease your take-home pay. We’ll look at your specific balance to see how it impacts your overall application strength.

Can I get a home loan with a DTI ratio over 6?

It’s possible to secure a loan with a DTI over 6, but your options will be more limited. Major banks often cap high-DTI lending at 15% of their total new loan portfolio to meet regulatory guidelines. Our team can help you identify specialist lenders who may accept higher ratios if you have a strong deposit of 20% or more and stable employment history. We’re here to be your partner in finding these opportunities.

How do credit card limits affect my borrowing power?

Lenders assess your full credit limit rather than your actual balance when calculating your debt to income ratio. For example, a credit card with a A$10,000 limit is treated as a A$10,000 debt even if you owe nothing on it. Reducing your total limits by A$5,000 can significantly improve your standing during the application process. It’s a simple step that shows lenders you’re in control of your financial future.

Is gross or net income used for DTI calculations?

Lenders typically use your gross annual income, which is your total earnings before tax, to calculate your debt to income ratio. This includes your base salary, consistent overtime, and 100% of most rental income. Using the gross figure provides a standardized benchmark that helps our team compare different loan products for your specific needs. We’ll do the heavy lifting to ensure every dollar of your income is correctly represented.

How can I quickly lower my debt to income ratio?

The fastest way to lower your ratio is to close unused credit facilities or pay down small personal loans. Reducing a car loan balance by A$15,000 or cancelling a high-limit credit card can move your DTI from a 6.2 down to a 5.8. This small shift often makes the difference between a loan rejection and a competitive approval. We’ll guide you through which debts to prioritize for the best result.

Do lenders look at DTI for refinancing as well as new purchases?

Yes, lenders apply the same DTI scrutiny to refinancing applications as they do for new home purchases. If your ratio has climbed above 6 since you first took out your loan, you might find it harder to switch banks. We guide you through this process by reviewing your current liabilities to ensure your profile meets the 2026 lending standards. Our goal is to make your transition to a better rate as seamless as possible.

What is the difference between DTI and serviceability?

DTI measures your total debt against your gross income, while serviceability calculates if you can afford monthly repayments after all expenses. A DTI of 5.5 might be acceptable, but if your living costs are high, you could still fail the serviceability test. Both metrics are vital for a successful application in the current Australian market. We’ll help you understand both numbers so you can feel confident in your borrowing power.